Print

PrintRay Garcia is a Leader, Matt DiGuiseppe is Managing Director, and Paul DeNicola is a Principal at PricewaterhouseCoopers LLP. This post is based on their PwC memorandum.

Stewardship survey at a glance:

| Investors believe the stewardship work they do can impact investment performance

72% of investors expect their stewardship activities to have an impact on investment performance over the next three to four years. |

Relationship-building is a key factor for accepting an engagement, but timing matters

51% of investors say their relationship with portfolio company management influences their decision to take a meeting during proxy season. Yet, 81% say the chance to build a relationship with that same management team is a factor in agreeing to an offseason engagement. |

| Boards have an opportunity to improve engagement

23% of investors say they are dissatisfied with the quality of engagement discussion with board members. |

Companies have an opportunity to provide enhanced disclosures to help investors understand how sustainability impacts the business

55% of investors are dissatisfied or very dissatisfied with how management connects sustainability to the company’s long-term growth in engagements and communications. |

| Investors are incorporating sustainability into their analysis, but are split on the importance of targets

46% of investors say achieving sustainability targets will have no or low impact on financial performance. But they are considering the quantitative and qualitative impacts of sustainability factors like climate and talent on financial performance. |

The proposed action matters most when stewardship teams make voting decisions on shareholder proposals

62% of investors say a proponent’s political views are somewhat or not at all important when evaluating a shareholder proposal. Instead, 86% see the alignment of the resolved clause with a perceived risk to be a more important factor in their analysis. |

Introduction

The relationship between corporate directors and investors is getting more complicated as companies handle global supply chains, adapt strategies for growth and competition, face new risks, and deal with increased pressure to be transparent about the board’s oversight role. In our 2024 Stewardship Investor Survey, we sought to better understand this dynamic by polling investment stewardship professionals, chief investment officers and analysts who represent a range of investors, from small pension funds to large asset managers, on their approaches to proxy voting and engagement.

Our goal with this survey is to clarify the structure of stewardship programs, the process they use to prioritize investment themes and the factors that influence proxy voting and portfolio company engagement. In a time of great change, the results show what companies are doing well and where there may be room for improvement.

Engagement — meetings between companies, frequently including board members and their investors in an “active ownership” capacity — is an accepted part of being a public company, with significant investments of time and resources from both sides. However, as recently as 2007, the idea of investors and boards meeting together was described as “corporate governance run amok.” In the short time that it has evolved to a best practice, there has been much supposition about what drives these discussions, their impact on investment decisions and overall value creation.

Investors are clearly focused on value creation. When asked, 72% of survey respondents say they expect their stewardship activities to have an impact on investment performance over the next three to four years, 17% are looking for an immediate impact and 10% have a longer vision. Further, just 16% of respondents report that there is no relationship between their stewardship and investment decision-making teams. Companies may use the insights from the survey to enhance their relationships with investors.

What is asset stewardship?

Asset stewardship, particularly in the realm of proxy voting and engagement, is a critical practice aimed at encouraging the companies in which investors hold shares to be managed in a way that promotes long-term value. This involves actively participating in the governance processes of these companies through proxy voting — when shareholders vote on various corporate matters — and direct engagement with company management and boards. The main objective is to influence corporate behavior and policies to align with shareholders’ best interests.

Asset stewardship, particularly in the realm of proxy voting and engagement, is a critical practice aimed at encouraging the companies in which investors hold shares to be managed in a way that they believe promotes long-term value.

The teams engaged in proxy voting and engagement are typically composed of a diverse group of professionals with specialized skills. These teams often include governance analysts who meticulously review proxy materials and company performance to make informed voting recommendations. Environmental, social and governance (ESG) specialists bring their expertise to evaluate and advocate for sustainable and responsible business practices. Legal advisors help ensure that all actions comply with regulatory requirements and help navigate complex governance issues. Additionally, portfolio managers and investment analysts provide insights into how governance and ESG factors impact financial performance and investment outcomes. These multidisciplinary teams work collaboratively with the goal of executing effective proxy voting and engagement strategies that promote long-term value creation and responsible corporate governance.

Throughout this report, we use investors, shareholders and asset stewardship professionals interchangeably and in all cases are referring to the asset stewardship perspectives that were shared through the survey.

Regulatory developments, material issues and macroeconomic conditions drive stewardship focus areas

Many investment stewardship programs generate themes that influence engagement topics and how they vote on shareholder proposals and management resolutions. The emphasis on these themes — say, boardroom diversity — can change from year to year, so it’s in the best interest of companies to understand how the themes are derived. But just 54% of respondents say their firms both publish their investment stewardship themes and explain the rationale behind them. Slightly more than a quarter (27%) of respondents don’t even publish this information. That leaves a lot of directors in the dark.

To gain some clarity, we asked how influential nine factors are in the creation of stewardship themes. Almost all investors (95%) say regulatory attention has some or significant influence on their themes and focus areas. That’s not surprising, given the wave of new regulatory disclosure rules that are transforming corporate reporting on cyber, environmental and social issues.

Our survey also finds that the thinking behind themes is closely linked to what investors believe will drive the financial performance of their holdings. Almost nine out of 10 (89%) investors say issues that are likely to have a material impact on their funds’ largest holdings had some or significant influence on their themes. Investors also list macroeconomic issues (78%) as influencing their focus areas, which could be a signal they are concerned with 2024’s market volatility.

What can companies do? Think beyond regulatory disclosure requirements, and proactively address investor concerns. One approach might be to analyze some stewardship programs to determine their focus areas and supplement those with broader topics that are top of mind in the capital markets, such as artificial intelligence. By doing this, companies can develop a sense of which additional disclosures would be most useful for their investors.

Stewardship professionals tell us they would like to see enhanced corporate disclosure in certain areas

The relationship between companies and investors is grounded in corporate reporting. Disclosures — whether in the financial statements, another part of the annual report, the proxy or elsewhere — are a central way the company communicates how it operates. This is especially true of communication by the board, whose members shareholders elect to oversee management on their behalf. In turn, investors analyze this information when performing qualitative and quantitative assessments of issues such as executive compensation, oversight of strategy and risk and board composition.

Despite the growth in volume and depth of reporting in recent years, asset stewardship teams tell us they see an opportunity for enhancement in certain areas. Some of their focus is reserved for issues covered by the new regulations, such as sustainability. Just 38% of investors are satisfied or very satisfied with the way management tells a story that connects sustainability to potential long-term growth. Their concern also carries over to foundational board topics that companies have been reporting on in the proxy for years, such as the approach for identifying new director candidates (41% satisfied or very satisfied), succession planning (51%), upskilling efforts (38%) and crisis management (52%).

What can companies do? Similar findings were revealed in PwC’s June 2024 Pulse Survey, which showed that just 27% of directors said they were very satisfied with the reporting they receive from management on the adoption of emerging technologies and about the same were very satisfied with reporting on supply chain resilience (29%) and ESG reporting (31%). Both surveys serve as a reminder to management to reevaluate longstanding disclosures that may have become boilerplate; management may want to enhance reporting in certain areas, considering the new generation of regulations. Disclosure can also be an engagement topic so companies can better understand where they may fall short of investor expectations.

Engagement meetings are dependent on aligning your agenda with when investors want to talk about it

Asset stewardship teams have made it clear to us that access to board members is essential to their process. While nearly half (49%) of respondents say that over the last two years there has been no change in their ability to engage with board members, 19% say it has become more difficult and 5% say they have not been able to meet with any board members over that period. The responses are similar across investment firm size and passive and active management. Given that many investors may rely heavily on disclosures for their analyses, these responses on engagement are a reminder of the importance of companies communicating clearly with stakeholders.

For their part, directors often tell us that they would like to know more about the factors that drive investors’ outreach or their decision to accept an engagement request from the company, whether the meetings are scheduled during proxy season or in the offseason.

In many instances, engagement allows investors to go beyond the proxy statement and learn more about the merits of a shareholder proposal or a management resolution. So, it’s not surprising that 84% of investors say a moderately or very important factor for accepting a meeting during proxy season is whether they need additional context for their vote on a shareholder proposal or management resolution. Other key factors include whether investors’ funds had identified a material risk related to a ballot item (95%), investors’ funds had a significant ownership stake (89%) and if the company had been proactively flagged for engagement (86%). Surprisingly, having a relationship with management is one of the least important factors (51%), as investors prefer to use offseason discussions for relationship-building.

Our survey shows that investors are tactically using offseason engagements. While the size of the ownership stake was still a key factor, 92% of investors say the chance to follow up on a proxy season issue with management has some or significant influence on agreeing to an offseason engagement and about nine out of 10 investors say a desire to better understand corporate strategy, ongoing low support for a voting matter and lack of shareholder rights provisions have some or significant influence on their decision to engage with company directors or management in the offseason.

What can companies do? Be thoughtful about engagement meeting agendas. Our survey reveals 76% of investors say an agenda that aligns with their stewardship themes had some or significant influence on their decision to engage. Companies should include relevant executives and board members that can speak about the topics that matter to their organization and investors.

There may be a disconnect in the value directors and investors derive from engagement meetings and companies should monitor this space. PwC’s 2023 Annual Corporate Directors Survey found that 87% of board members believe their engagements with shareholders were productive. But our stewardship survey showed that just 69% of investors are satisfied with the quality of these discussions and just 6% were very satisfied. As engagement continues to become ingrained in the relationship between companies and investors, it’s important to make sure everyone’s time is being used efficiently.

Asset stewardship investors consider many impacts on financial performance, and they may not be considered equally

While investment stewardship teams spend considerable time analyzing governance issues such as board composition and director commitments, they also have a vested interest in understanding the risks that can impact the financial performance of their portfolio companies. We sought to understand key risks, the methods investors are using to measure the impact of those risks and how far out they are looking when making their assessments.

Given the market volatility in the US, it’s not surprising that 73% of investors say the uncertain macroeconomic environment will have a medium or high impact on financial performance over the next three years. More than eight out of 10 (81%) investors say the same about geopolitical uncertainty and 78% for the US regulatory environment and shifts in consumer behavior.

Our survey results show that investors are using a combination of qualitative and quantitative analysis to measure the impact of these risks. That said, our results also show that most stewardship teams are leaning more heavily on qualitative analysis. As detailed in the chart on the next page, when not selecting both approaches, the respondents heavily favored measuring the impact of all but margin pressure qualitatively. That’s an additional sign of the importance of corporate reporting and disclosures.

In most instances, investors are focusing on the impacts of these risks in the near term. Of the 15 factors we asked about, most investors were measuring the impact over the next one to five years. The one outlier: climate. While 70% of investors say this topic will have a medium or high impact on financial performance, nearly half of investors are forecasting the impact to unfold over longer periods.

What can companies do? Consider not only what you are disclosing but also the context you provide about how management uses the information in business decisions in both the near and long term. Investors are looking at a broad range of factors that they believe will impact financial performance, but, as noted previously, half of them are looking for better disclosures on how companies think these factors will impact longer-term performance.

The proposed action matters most when stewardship teams make voting decisions on shareholder proposals

Over the past three years there has been a rapid rise in shareholder proposals with opposing interests on many ESG issues. For instance, there are proposals that ask companies to disclose the impacts of diversity, equity and inclusion (DEI) programs and proposals that ask companies to report on the risks created by having a DEI program in the first place (i.e., an anti-DEI proposal). It is useful for companies to understand how stewardship professionals are approaching the increasingly divided shareholder proposal environment when thinking about how to vote on a proposal.

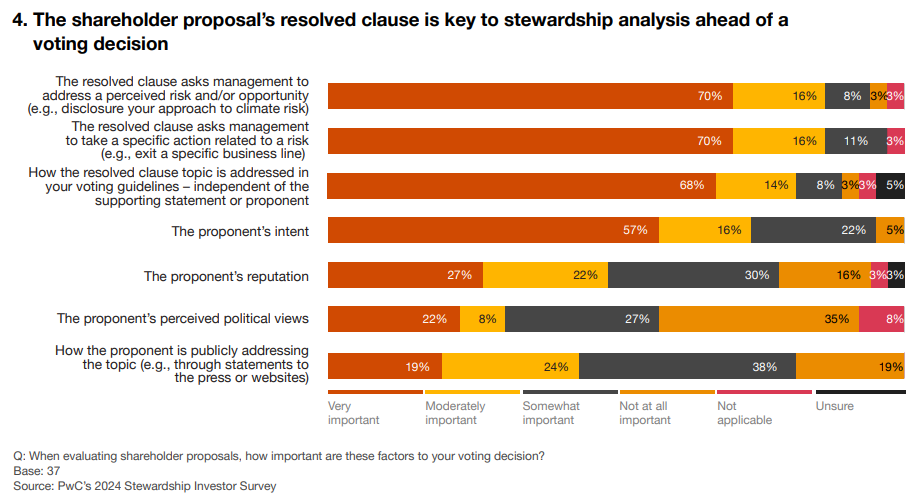

The resolved clause in the shareholder proposal, which outlines the specific request or action being voted on, is one of the most important factors in stewardship analysis ahead of a voting decision. The risk being addressed in the resolved clause (86%), the actions being requested of the company (86%) and the way the topic being raised is addressed in voting guidelines (82%) are all moderately or very important to their vote decision, with over two-thirds of respondents saying that the three are very important. In addition to the resolved clause and supporting statements that are published in the proxy, investors may also be interested in which fellow shareholder filed the proposal, known as the proponent. In contrast to the published text, factors like the proponent’s reputation (46%), public statements (57%) and perceived political views (65%) are somewhat or not at all important. Interestingly, while it may seem like the resolved clause and the proponent are considered independently, many respondents indicate that they consider when the resolved clause and the proponent’s intent as described in the supporting statement are not aligned.

What can companies do? Companies should trust that investors are taking a case-by-case approach to voting shareholder proposals and not simply looking at the headline topic being addressed or taking the resolved clause at face value. To help them in their analyses, companies can focus on disclosing how they are managing the risks raised by the proposal in a manner aligned with value creation rather than arguing against the proponent’s position.

Stewardship teams consider a range of factors when approving auditor appointment

The audit committee has direct responsibility for the appointment of the external auditor, setting the compensation and overseeing its work. The selection process sometimes doesn’t get the same amount of attention as other governance topics, but it’s nonetheless an important responsibility for the board.

Because material weaknesses occur infrequently, it is not surprising that 92% of investors say that the identification of such weaknesses in a company’s internal controls is a moderate or very important factor in determining whether to support the reappointment of an auditor when one is identified. However, just 78% of investors say the same thing about the ratio of audit fees to non-audit fees, even though most voting guidelines specify a threshold of at least the former not exceeding the latter. Rounding out the three most important factors, 76% of respondents also pointed to the robustness of the Critical Audit Matters (CAMs) identified as influencing their decisions to support the appointment of the auditor.

Overall, investors seem content with the information they receive about the board’s oversight of the auditor, with 81% saying current regulatory filings are sufficient to complete their assessment. But there are areas where they may appreciate additional disclosure (e.g., what services fall under non-audit fees and the ways in which the audit committee and auditor interact).

What can companies do? Although investors are generally satisfied with the information they are receiving, consider using the audit committee report to provide additional insights into how the audit committee oversees the auditor and its selection and reappointment to build trust with investors.

Appendix

Complete data for the survey questions referenced in this publication. Please contact us if you are interested in hearing about the full survey responses.

Note: Percentages may not add up to 100 due to rounding.

Conclusion

Our 2024 survey of asset stewardship professionals provides insights into the evolving engagement landscape as we approach two decades of expanded stewardship activity by investors.

PwC has long provided insights on key issues facing boards with our Corporate Directors and Board Effectiveness surveys. This survey adds another layer of insights to the board, management and investor triad and we look forward to discussing this unique perspective with our clients.