Print

PrintLauren Shatanof is a Consultant at FW Cook. This post is based on an FW Cook memorandum by Ms. Shatanof, James Lutz, and Voytek Sokolowski.

INTRODUCTION

This Top 250 Report details executive long-term incentive practices at the 250 largest companies by market capitalization, with special focus on trends over the last five years.

The past five years have shown that company performance and plan payouts can be influenced by a number of factors such as stock price volatility, regulatory updates, changing investor expectations, supply chain disruptions, geopolitical events, inflation, and evolving labor markets. In response, companies have continued to tweak the design of their long-term incentive plans to promote stability and retention

Overview and Background

Since 1973, FW Cook has published annual reports on long-term incentive grant practices for executives. This report, our 52nd edition, presents information on long-term incentives granted to executives at the 250 largest U.S. companies in the S&P 500 Index. It is intended to inform boards of directors and compensation professionals in designing and implementing long-term incentive programs that promote company success by supporting strategic objectives and aligning pay delivery with performance.

Scope of Study

The report covers the following topics:

- Long-term incentive grant type prevalence and mix, with a focus on CEO awards.

- Key performance-based award plan design, including types of performance measures, absolute versus relative performance measurement, overlap of metrics between annual and long-term incentive plans, inclusion of relative TSR measures, performance goal ranges, total performance and vesting period length, and cumulative versus annual performance measurement.

- Time-based award vesting, considering number of years and format.

- The Appendix includes information on additional performance-based award detail and statistics by industry.

Historical comparisons focus on a five-year lookback (2024 versus 2019) to highlight trends.

Source of Data

All information was obtained from public documents filed with the Securities and Exchange Commission (“SEC”), including proxy statements and Form 10-K and 8-K filings.

Top 250 Company Selection

The Top 250 companies are selected annually based on market capitalization (share price multiplied by common shares outstanding). The sample in this report consists of the 250 U.S.-listed companies in the S&P 500 with the largest market capitalizations as of April 30, 2024, limited to those granting long-term incentives. See the Appendix for the list of companies reviewed. Twenty-three of the 250 companies (9%) are new to this 2024 report (i.e., not in the 2023 Top 250 sample), with the majority of changes due to fluctuations in market capitalization between April 30, 2023 and April 30, 2024 (the dates used to determine the 2023 and 2024 Top 250 company lists, respectively).

The following table displays the industry sectors represented in the Top 250 for 2024, defined by the Global Industry Classification System (“GICS”).

Methodology – Definition of Long-Term Incentive

This report presents the most recently disclosed long-term incentive grant types in use at the Top 250 companies as of mid-2024. A grant type is considered in use at a company if grants were made in the current or prior year and there is no evidence the grant practice has been discontinued, or if the company indicates the grant type will be awarded in the future.

To be considered a long-term incentive for the purposes of this report, a grant must reward performance and/or continued service for a period of one year or more and cannot be limited by both scope and frequency.

- A grant with limited scope is awarded to only one executive or select executives.

- A grant with limited frequency is not part of a company’s regular grant practice. For example, a grant made as a hiring incentive, replacement of compensation forfeited at a prior employer, or a promotion award is not considered in this report.

- A grant with limited scope but without limited frequency (e.g., annual grants made only to the CEO) may be considered, and vice versa (e.g., one-time grants made to all executives).

Methodology – Definitions

Award Vehicles: Long-term incentive award vehicles include, but are not limited to, the following:

- Stock Options and Stock Appreciation Rights (“SARs”), which are derivative securities with value dependent upon stock price appreciation; stock options are rights to purchase company stock at a specified exercise price during a stated term; SARs are rights to receive the increase between the grant price and the market price of a share of stock at exercise.

- Restricted Stock, which includes actual shares or share units that are earned for continued employment and are often referred to as time-based awards.

- Performance Awards, which consist of stock-denominated shares or share units (“performance shares”) and grants of cash or dollar-denominated units (“performance units”) earned based on performance against predetermined objectives over a period of more than one year, including long-term incentives with one-year performance periods that have additional time-vesting requirements.

Types of Measures: “Measures” in this report include metrics, which have an independent weighting (e.g., revenue at 50% weighting), and modifiers. A modifier is an adjustment factor applied to the outcome of metrics; it can either increase or decrease the metric payout. Companies may use an additive approach or a multiplicative approach. With an additive modifier, a percentage payout is added or subtracted from the metric payout. Multiplicative modifiers use a performance factor that is multiplied by the metric payout (typically still capped by the overall maximum payout).

Measure Categories: Performance measure categories include, but are not limited, to the following:

- Total Shareholder Return (relative or absolute stock price appreciation plus dividends)

- Profit (EPS, Net Income, EBIT, EBITDA, Operating/Pretax Profit, Operating Margin)

- Capital Efficiency (Return on Equity, Return on Assets, Return on Capital)

-

Revenue (Sales, Net Revenue)

- Cash Flow (Free Cash Flow, Operating Cash Flow) • Other (e.g., Other Specific Financial Measures, Safety, Quality Assurance, New Business, Individual Performance, Environment/Social/Governance (“ESG”)

How Has Program Design Changed?

Within the following sections, we seek to understand how long-term incentive programs have evolved over the last five years 2019 – 2024

LONG-TERM INCENTIVE GRANT TYPES & PREVALENCE

Which Long-Term Incentive Vehicles Are Most Utilized?

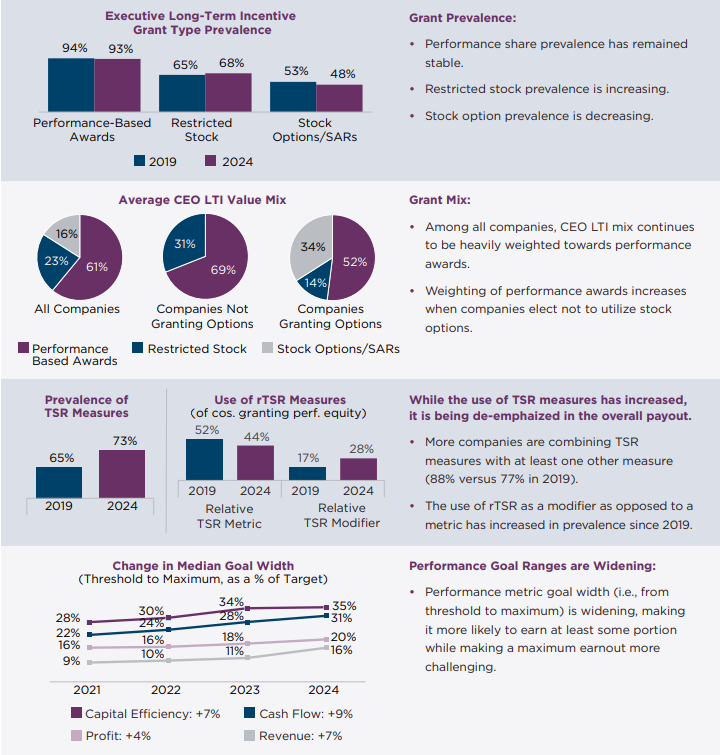

Most companies continue to utilize a portfolio approach of multiple long-term incentive grant types, with performance-based awards most heavily emphasized in both prevalence and overall grant value mix. Since 2019, stock options have declined in weighting in favor of restricted stock and performance shares.

Grant Type Prevalence

The use of performance shares has remained relatively stable over the past five years, while there has been a slight increase in the use of restricted stock (+3% since 2019) and a decline in the use of stock options (-5% since 2019).

General industry use of stock options/SARs has declined over the last decade. Potential reasons for this change include:

- Proxy advisors hold the view that stock options are not sufficiently performance-based absent a premium exercise price or performance-vesting condition, contributing to an elevated emphasis on pay-for-performance.

- Stock options can result in higher and more volatile compensation expenses due to the complexities of valuation methods used, such as Black-Scholes. Performance-based awards often result in lower associated costs while still providing executives with upside potential based on outperformance.

- Most Top 250 companies de-emphasize stock options in favor of restricted stock and performance-based awards, which have greater retentive value in flat or negative stock price environments, more efficiently use stock plan reserves, and in the case of performance-based awards, can target specific performance goals other than absolute stock price appreciation.

Note that companies of earlier business maturity (generally not reflected in the Top 250 sample) or in certain industries (e.g., healthcare) rely more heavily on stock options/SARs.

Number of Grant Types

In 2024, 84% of companies granted two or more grant types, generally consistent with 2019 practice. The use of three grant types declined in prevalence from 32% in 2019 to 26% in 2024 as more companies moved away from stock options / SARs (see above).

- Relying on a single equity vehicle can expose compensation to market fluctuations. For example, stock options might lose value in a declining market, but restricted stock still hold some value. Performance shares may also be impacted by unexpected challenges. By using multiple vehicles, companies can diversify and reduce the volatility impact on total compensation.

Grant Value Mix

Performance-based awards continue to comprise the majority of the average CEO’s grant value mix (61% weighting), up slightly since 2019 (+3%). The remaining value is granted as time-based restricted stock for retention or stock options/SARs to incentivize absolute stock price growth.

For companies granting stock options/SARs, the average weighting of performance-based awards is about 50% of CEO total LTI. For companies not granting stock options/SARs, the average weighting of performance-based awards is almost 70% of CEO total LTI.

PERFORMANCE-BASED AWARD DESIGN

What Measures Are Used to Assess Performance?

Total Shareholder Return (“TSR”) has become the most prevalent measure, used by 73% of companies, up from 65% in 2019. Profit measures are the second most prevalent measure, used by approximately half of all companies.

Performance Measure Prevalence

Most companies use TSR as either a metric or a modifier because it directly aligns payouts with shareholder outcomes and performance can be easily measured relatively (see following page for details).

The use of “other” performance measures has steadily risen since 2019, driven in part by the incorporation of Environmental, Social, and Governance (“ESG”) goals. In 2024, 18 companies included an ESG measure in their LTI plans (8% of companies that grant performance shares, up from 3% in 2020). While some companies incorporate ESG goals in their long-term programs to support objectives that require a multi-year focus, ESG is more commonly found in annual incentive plans. Use of ESG measures in LTI plans is more common in the Energy and Consumer Discretionary sectors.

Performance Measure Overlap Between Annual and Long-Term Incentive Plans

| Of the 232 companies using performance-based awards, 72 (31%) use at least one identical measure in both their annual and long-term incentive programs. The most common to overlap were revenue and profit goals. |

Investors and proxy advisory firms generally prefer that companies use distinct measures between annual and long-term incentive plans to diversify performance outcomes. Although proxy advisors may mention the metric overlap in their qualitative assessments, it is unlikely to be a driving factor of their say-on-pay recommendation.

How Is TSR Used in Plans?

The majority of companies using TSR continue to measure performance relative to an index or other comparator group of companies. Additionally, although prevalence of TSR is increasing, companies are de-emphasizing its effect on overall payouts.

Absolute versus Relative Performance Measurement

98% of companies that use a TSR metric or modifier do so on a relative basis (including 3% that measure both absolute and relative TSR).

- Relative performance measurement is an attractive approach when it is difficult to confidently forecast multi-year financial performance and set appropriate long-term goals. As a result, TSR is typically measured on a relative basis due to the macroeconomic sensitivity of stock prices and participants’ limited control over external factors that influence stock price movement.

- Use of relative TSR also aligns with the preferences of investors and proxy advisory firms, which have contributed to the increase in its prevalence.

Emphasis of Relative TSR (“rTSR”)

While more companies have adopted rTSR, a decreasing proportion are using it as the sole performance measure (44%, down from 51% in 2019).

Additionally, the use of rTSR as a modifier versus metric has increased in prevalence since 2019 (+11%). A modifier may only apply an adjustment to the calculated financial payout. In terms of modifier use, practice is split between a multiplicative and additive approach. (refer to methodology section for explanation of each approach). Among both approaches, the majority practice is to increase or decrease payouts by 20-25%.

Companies often prefer modifiers over a weighted metric to de-emphasize the overall impact of rTSR on PSU payouts to improve line-of-sight to financial outcomes.

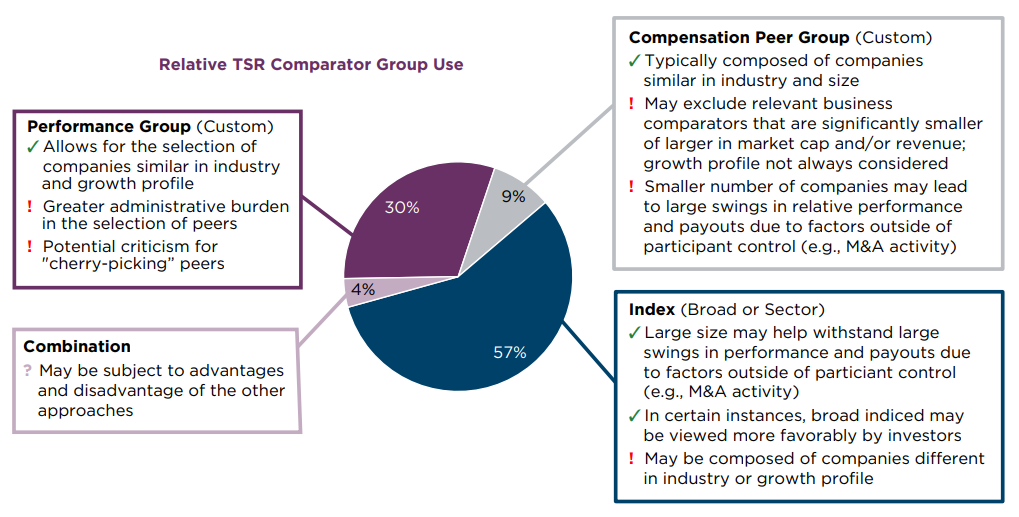

Relative TSR Comparator Group Types and Prevalence

More than half of Top 250 companies (57%) with relative performance goals use indices (e.g., broad indices such as the S&P 500 or industry-focused indices such as the Dow Jones U.S. Health Care Index) as comparator groups, with remaining practice split between a performance peer group, compensation peer group, or combination of approaches. A performance peer group is a custom group of companies that is different from the compensation peer group used for executive benchmarking. Performance peer groups are typically composed of direct competitors. Although more administratively burdensome to develop, performance peer groups allow for a significant degree of customization compared to indices or compensation peer groups. This allows companies to choose prominent competitors who could be outsized or otherwise unfit for inclusion in a compensation peer group.

Considerations in comparator group selection include the following:

- Smaller comparator groups may be subject to higher degrees of volatility in relative performance due to unplanned changes to constituents (e.g., M&A activity).

- Companies similar in industry and financial/growth profile are more likely to be subject to the same macro-economic factors.

- Proxy advisors and investors could criticize for “cherry-picking” companies to improve payouts if the companies selected are not similarly sized or reasonable business or talent competitors.

- Indices may be viewed favorably by investors in certain instances (e.g., in underperforming industries that compete for investor capital against broader, higher-performing companies).

Relative TSR Performance Goal setting and Ranges

The most prevalent relative TSR performance level for achieving threshold payouts continues to be the 25th percentile. The median continues to be most prevalent target goal although the recent proxy advisor preference for above-median target performance explains the increase in prevalence of above-median target goals (55th percentile is most common among companies not targeting the median). The 75th percentile continues to be the most common goal for a maximum payout.

In times of volatility, it is possible for relative TSR performance to exceed target when absolute TSR is negative (i.e., stock price depreciation). Absolute TSR caps, typically limiting payouts to 100% of target when absolute TSR is negative, have grown in prevalence in recent years.

There are differing views on this topic. Some may argue that high relative performance in a depressed stock price environment still justifies above-target payouts, while others (proxy advisors included) may view above-target payouts as inconsistent with the shareholder experience. We also note that the use of an absolute TSR cap can be a provision to lower the fair value of performance awards that use a relative TSR measure.

How Are Financial Measures Used in Plans?

Performance goal ranges have expanded in recent years due to continued market uncertainty and challenging operating environments. Additionally, the vast majority of awards with financial goals continue to be measured on an absolute basis. Relative measurement of financial goals has increased in prevalence, likely due to macroeconomic volatility, but remains a minority practice.

Absolute versus Relative Performance Measurement

Most financial goals continue to be measured on an absolute basis. While use of relative measurement for financial goals has increased, it can be administratively challenging for companies to compare financial operating data. This is due to M&A and other extraordinary activities, differing fiscal years and timing of financial disclosures, as well as varying adjustments for non-GAAP definitions. In contrast, stock price data driving TSR are directly comparable and reported in real-time.

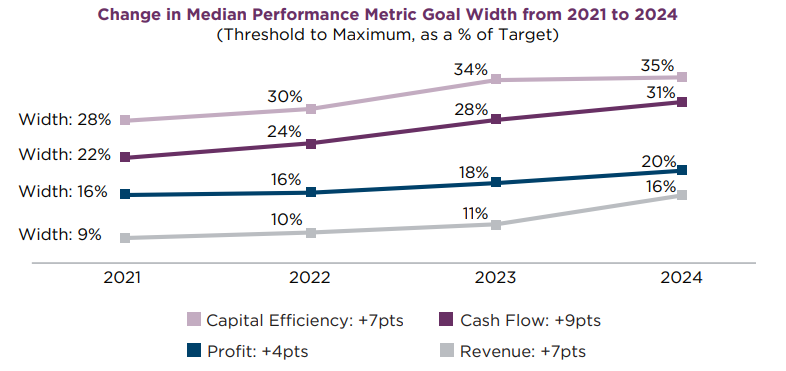

Financial Goal Width

Performance goal setting is often informed by company-specific factors including company budget, internal and investor performance expectations, historical performance, and compensation philosophy. Performance goal width is the range between threshold and maximum performance goals, where:

- Threshold is the minimum performance to warrant any payout at all, and maximum is the performance required to achieve the highest possible payout.

- For consistent comparisons across companies, performance goal width is calculated as the difference between threshold and maximum goals as a percent of target (e.g., if threshold, target, and maximum are $9.5B, $10.0B, and $10.5B in revenue, respectively, then threshold is 95% of target, maximum is 105% of target, and the goal width is 10% of target).

The goal ranges between threshold and maximum is typically narrowest for revenue metrics and becomes progressively wider for profit, cash flow, and capital efficiency metrics.

- Revenue is generally the most predictable financial measure, resulting in the narrowest goal width.

- Profit measures are determined by two types of input (e.g., revenue and various costs), typically resulting in a wider goal range.

- Cash flow and capital efficiency goal widths tend to be even wider due to the additional variable inputs that impact their results (e.g., return on assets is calculated by dividing profit by total assets).

Since 2021 (the first year that FW Cook began collecting comprehensive data on this), goal ranges have increased by 4 to 9 percentage points, depending on the metric. This trend is driven by companies prioritizing stability amid market fluctuations, regulatory shifts, changing investor dynamics, and global challenges.

How Are Performance Periods Defined?

Performance periods have been consistently set at three years. While measuring performance in annual increments (i.e., using multiple discrete, one-year goals) has increased in prevalence since 2019, cumulative performance measurement over three years remains by far the most common approach. The uptick in annual measurement is indicative of how companies are addressing recent macroeconomic uncertainty and challenges with three-year goal setting.

Overall Performance Measurement Period Length

Most performance-based awards continue to be measured over a three-year period (90%), aligning with common expectations from proxy advisors and investors.

Annual versus Cumulative Performance Measurement

Within the multi-year performance period, most companies evaluate performance over the entire period as a whole (cumulative measurement), although, there has been an increase in the number of companies evaluating performance each year within the performance period (annual measurement over three separate 1-year periods). In 2024, 11% of companies use annual performance periods, which is almost double the rate observed immediately prior to the pandemic (6% of companies in 2019).

- Annual performance measurement is more common in certain industries, with about 15% to 25% prevalence among the Communication Services, Information Technology, Health Care, and Consumer Discretionary sectors.

Cumulative measurement continues to be preferred by proxy advisors and investors. There is concern that multiple annual goals do not incentivize long-term thinking depending on the design.

- Among companies using annual measurement, the practice of setting goals for each annual tranche (such as applying a fixed growth goal to the prior year’s actual performance) grew by 10 percentage points, from 36% in 2019 to 46% in 2024. While setting goals annually helps reduce performance risk, it is generally seen less favorably than setting goals upfront for the entire period. Additionally, this approach can be viewed as effectively rewarding executives twice for the same annual performance.

- For awards where goals are set year-by-year, the grant value will be split between multiple years of proxy statement Grants of Plan Based Awards Tables.

Similarly, companies may find that annual performance measurement has unique goal-setting complexities, including when to set annual goals, how to weight each annual period in the overall payout, whether to include a cumulatively measured metric to incentivize long-term thinking, etc.

TIME-BASED AWARD VESTING

How Do Time-Based Awards Vest?

Stock options / SARs and restricted stock most commonly vest ratably over three years.

Number of Years

Three years remains the most common vesting length for stock options/SARs and restricted stock.

Vesting Type

Ratable vesting is a type of vesting schedule that allows an employee to receive a portion of their award over time at a uniform pace (e.g., 25% every year), and it is the most prevalent approach for both stock options/SARs and restricted stock. Ratable vesting includes annual, monthly, and quarterly vesting, although annual is by far the most common (96% of companies in 2024 with ratable vesting do so annually). Non-uniform/other refers to a schedule where awards vest at uneven intervals or in varying amounts over time, rather than a consistent pattern like in ratable vesting,

Link to the full report can be found here.