Print

PrintDimitri Zagoroff is Senior Editor at Glass, Lewis & Co. This post is based on a Glass Lewis’ 2024 Policy Survey by Mr. Zagoroff, Brianna Castro, Courteney Keatinge, Chris Rushton, Eric Shostal, and Maria Vu.

This post provides an overview of a section of Glass Lewis’ 2024 Policy Survey, conducted to inform their annual “benchmark” policy guideline updates.

Board Response to Failed Advisory Proposal

Investors and non-investors expressed very different expectations for how a board should respond when an advisory management proposal does not receive majority support. The most popular answer among investors was that the board should generally refrain from the requested action (41.1%, vs 9.0% among non-investors). As one Canadian investor put it:

“Why put it to shareholder opinion if you aren’t going to follow their views?”

Other investors took a more balanced view:

“This would depend on the ask and the level of shareholder opposition.” (U.S. investor)

“In some cases, not proceeding may be impractical. For example, refusing to pay a CEO their new salary or trying to clawback bonuses will destabilize the business and may result in legal action against the company. But a majority vote against should still send a clear message to the Board that it must take action on the main issues raised.” (U.S. investor)

Meanwhile, non-investors were far more likely to defer to the board’s judgment (23.9%, vs 5.5% among investors).

“The Board should consider the views of the shareholders, particularly as it solicited those views, but shouldn’t be required to go ask a subset of shareholders for permission, and should implement the action if the Board believes it is appropriate.” (U.S. non-investor)

“I think a lot depends. Remember that a meeting typically only requires a majority of shares to be present. And to pass typically requires a majority of those shares. I think more context is required.” (U.S. non-investor)

Although responses were generally aligned across regions, non-investors from outside North America appear to put more emphasis on consultation with shareholders (32.0%, vs 22.0% among North American non-investors).

Defining ‘Significant’ Opposition

The most popular answer among both types of respondent was “20-30%” (49.4% among investors, vs 31.3% among non-investors); however, investors were twice as likely to view shareholder opposition of 30% or less as significant (80.5%, vs 39.9% among non-investors), and non-investors were much more likely to see no need for a response so long as the proposal is approved (23.9%, vs 1.3% among investors).

Notably, respondents from both groups highlighted the relevance of ownership & voting structure:

“depends on the company shareholding structure. Eg. if 40% of the company voting rights are controlled by a shareholder then 20% is a significant dissent. If the largest shareholders has less than 5%, then 30% is a significant dissent.” (European non-investor)

“Where there is a multi-class structure, dissent should be calculated to reflect the views of non-affiliated shareholders.” (Canadian investor)

“Degree of opposition from non-controlling shareholders is also relevant.” (U.S. investor)

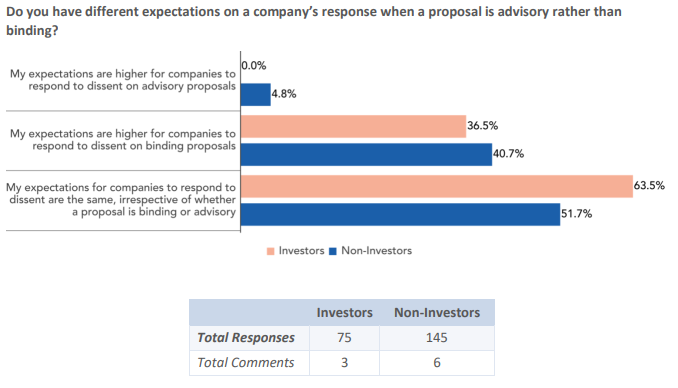

Company Responsiveness to Binding/Advisory Votes

Across different regions and types of respondent, there appears to be a general consensus that expectations for how a company responds to significant levels of shareholder dissent are not influenced by whether the proposal is binding or advisory.

Investor Escalation on Binding/Advisory Pay Votes

Similarly, nearly three-quarters of investors do not approach escalation of the executive pay vote differently based on whether that proposal is binding or advisory (72.4%). Notably, this response was more common among North American investors (78.7%) than other markets (62.1%). Looking specifically at regions where a mix of binding and advisory pay proposals are standard, this view was more common in the UK (85.7%), and less so on the European continent (56.3%).

Link to the full report can be found here.