Print

PrintBackground

New Disclosure Requirements

Reportable Segment Disclosures

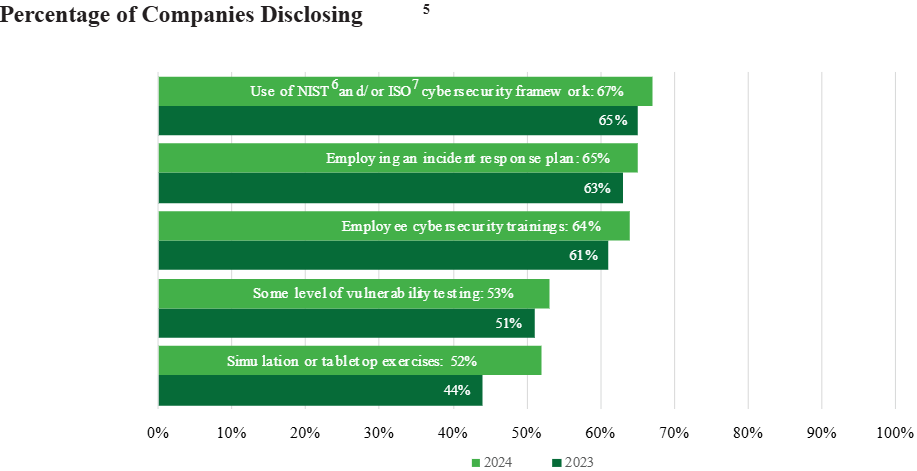

Cybersecurity (Form 10-K, Item 1C)

[5] These percentages reflect a comparison of a population of Fortune 500 companies’ Form 10-K filings between (1) March 1, 2024, to March 3, 2025 (“2024”), and (2) December 15, 2023 (the date on which the final rule became effective), to February 29, 2024 (“2023”).

[6] National Institute of Standards and Technology.

[7] International Organization for Standardization.

Executive Compensation Clawback

In 2023, the SECmandatedthat all listed registrants use two new checkboxes on the cover page of Form 10-K to address executive compensation “clawback” policies. [9] In the 2024 reporting period:

- Fifteen Fortune 500 registrants [10] marked Box 1 (up from thirteen in 2023), indicating that they were correcting an error in previous financial statements. Among these, eleven companies reported changes to the statements of financial position, income, or cash flows, while four companies noted adjustments solely in the footnotes.

- Six registrants also checked Box 2 (up from two in 2023), indicating that a corrected error prompted a clawback analysis.

Disclosure Trends

Artificial Intelligence

Income Taxes — Pillar Two

Global Trade

Sustainability

Conclusion

Footnotes

1 FASB Accounting Standards Update (ASU) No. 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures.(go back)

2 We examined the adoption of ASU 2023-07 by Fortune 500 companies that have filed as of March 3, 2025, and whose fiscal years began on or after December 15, 2023. This represents approximately 70 percent of the Fortune 500; the remainder consists of non–calendar-year-end companies. See Deloitte’s November 30, 2023 (last updated September 10, 2024), Heads Up for a discussion of ASU 2023-07.(go back)

3 Earnings before interest, taxes, depreciation, and amortization.(go back)

4 SEC Final Rule Release No. 33-11216, Cybersecurity Risk Management, Strategy, Governance, and Incident Disclosure. See Deloitte’s July 30, 2023 (updated December 19, 2023), Heads Up for a discussion of the final rule.(go back)

5 These percentages reflect a comparison of a population of Fortune 500 companies’ Form 10-K filings between (1) March 1, 2024, to March 3, 2025 (“2024”), and (2) December 15, 2023 (the date on which the final rule became effective), to February 29, 2024 (“2023”).(go back)

6 National Institute of Standards and Technology.(go back)

7 International Organization for Standardization.(go back)

8 The population covered in the Deloitte and CAQ joint report differs from that used in this publication (see footnote 5); therefore, the applicable cybersecurity percentages may vary from those shown herein. However, it is clear from both populations that reporting to the audit committee and quarterly reporting are key components of cybersecurity oversight.(go back)

9 SEC Final Rule Release No. 33-11126, Listing Standards for Recovery of Erroneously Awarded Compensation. For more information about the final rule, see Deloitte’s November 14, 2022, Heads Up.(go back)

10 These amounts refer to our comparison of a population of Fortune 500 companies’ Form 10-K filings (excluding amendments) between (1) March 1, 2024, to March 3, 2025 (“2024”), and (2) March 2, 2023, to February 29, 2024 (“2023”). All error corrections were reported as immaterial restatements and did not result in amendments to prior filings.(go back)

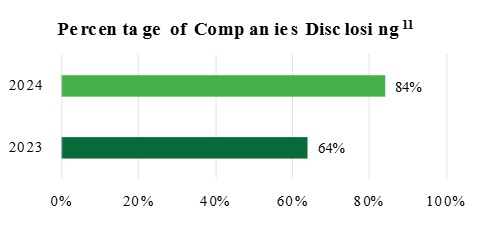

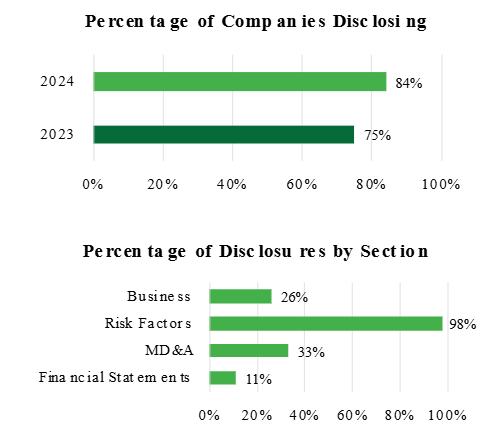

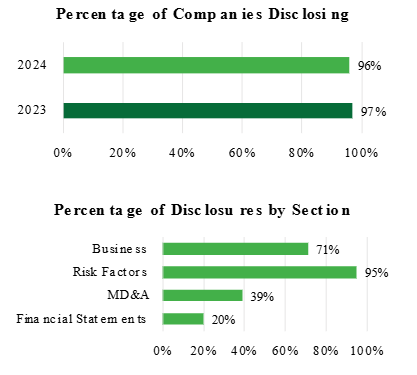

11 Hereafter, “percentage of companies disclosing” refers to our comparison of a population of Fortune 500 companies’ Form 10-K filings between (1) March 1, 2024, to March 3, 2025 (“2024”) and (2) March 2, 2023, to February 29, 2024 (“2023”).(go back)

12 “Percentage of disclosures by section” in the tables throughout this publication refers to our comparison of (1) the number of registrants in a population of Fortune 500 companies that discussed a given topic in a specific section of their 2024 Form 10-K (i.e., filings between March 1, 2024, and March 3, 2025) with (2) the total number of registrants that addressed that topic in their Form 10-K filings. We based the comparison on a search of keywords related to the topic being discussed in each section. If registrants discussed a topic in multiple annual report sections, the total percentages for that topic may exceed 100 percent.(go back)

13 For more information and answers to frequently asked questions about Pillar Two, see Deloitte’s March 5, 2024 (last updated November 8, 2024), Financial Reporting Alert.(go back)

14 The Organisation for Economic Co-operation and Development (OECD) provides jurisdictional legislation updates on its Web site.(go back)

15 SEC Final Rule Release No. 33-11275, The Enhancement and Standardization of Climate-Related Disclosures for Investors. See Deloitte’s March 6, 2024 (last updated April 8, 2024), and March 15, 2024 (last updated April 8, 2024), Heads Up newsletters for an executive summary and comprehensive analysis, respectively, of the SEC’s climate rule.(go back)

16 See Deloitte’s August 17, 2023 (updated February 23, 2024), Heads Up for responses to frequently asked questions about the CSRD.(go back)

17 IFRS S2, Climate-Related Disclosures.(go back)