Print

PrintMichael Tae is Group President, Chuck Callan is Senior Vice President, and Mike Donowitz is Vice President at Broadridge Financial Solutions. This post is based on their Broadridge memorandum.

Highlights from the 2025 proxy season

We provide data on ownership and voting by retail and institutional segments of investors, across the major proposal types, showing the trends over a 5-year timeline.

The data is unique because it is based on a “see-through” into voting on an account-by-account basis for most shareholders and investors. (Ownership and reporting for these segments is in the aggregate.) The data is based on Broadridge’s processing of shares held beneficially in street name at the custodian banks and broker dealers for whom we provide communications and voting services, and on our coding of proposal types.

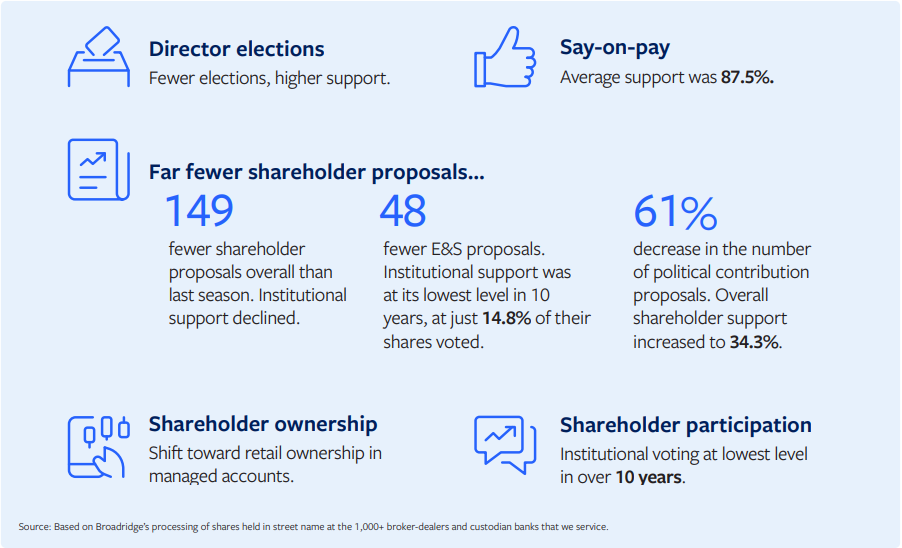

Director elections

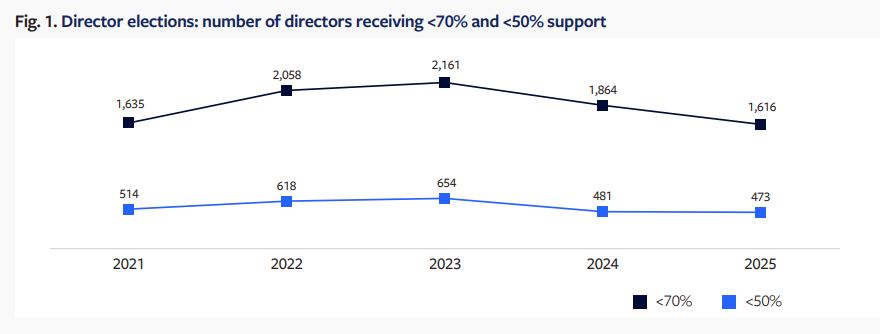

The number of directors that stood for election in the 2025 season was the lowest since 2020. Despite fewer elections, support for directors increased slightly to 91.8%, on average, of the votes cast.1 In comparison to last year, the support of institutional investors rose (up to 90.4% from 89.5% in 2024). Retail investor support remained strong at 91.1%.

The number of directors who failed to surpass the 70% support threshold fell to 1,616, or 7% of the total, while 2% of directors (473 of 22,797) failed to obtain majority support (at least 50%). Increased support is likely related to relaxed voting policies from certain large investors.2

Say-on-pay

Average support for say-on-pay proposals this past season was 87.5%. A closer look at the data shows that low levels of support for say-on-pay are correlated with low levels of support for corporate directors. 28.6% of the corporate issuers who failed to achieve at least 50% favorability on their say-on-pay proposal also had at least one director fail to attain majority support.

Shareholder proposals

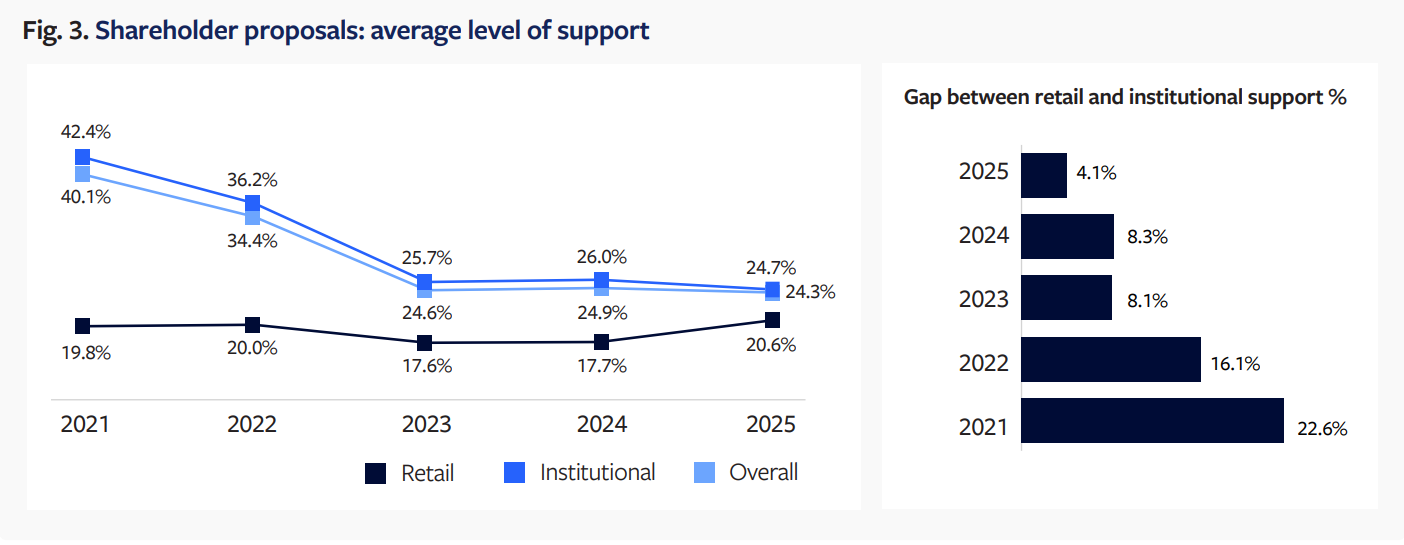

The SEC’s guidance3 this past February made it easier for companies to exclude shareholder proposals from their proxy ballots. Overall, 149 fewer shareholder proposals went to a vote this past season (430) compared to the prior season (579). Across the proposals that were voted on, retail support increased by 3 percentage points to 20.6%, while institutional support dropped markedly by over 2 points to 24.3%. Combined support levels continued their decline since 2021, and the gap between retail and institutional segments narrowed to its tightest margin in 9 years.

Environmental and social

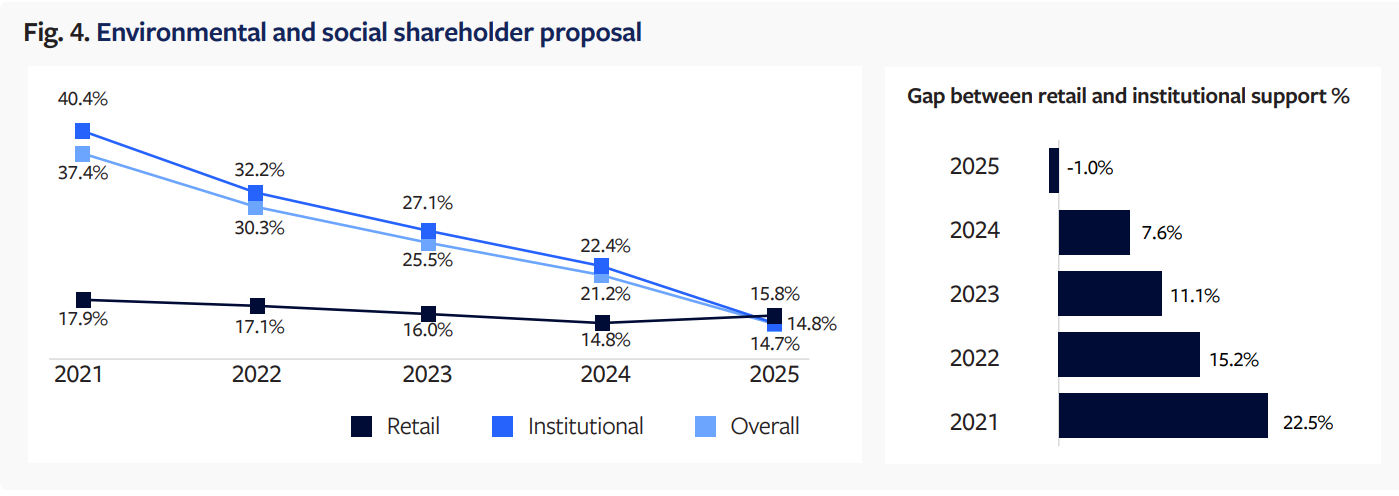

The total number of environmental and social proposals declined by 48, from 166 last season to 118 in the 2025 season. Overall shareholder support also declined to 14.7% of the shares voted. Institutional support was at its lowest level in 9 years, at just 14.8%. Legal, regulatory, and legislative pressure factored into decisions by institutional investors to vote against these proposals. The relative lack of support for anti-ESG proposals also drove down overall support.

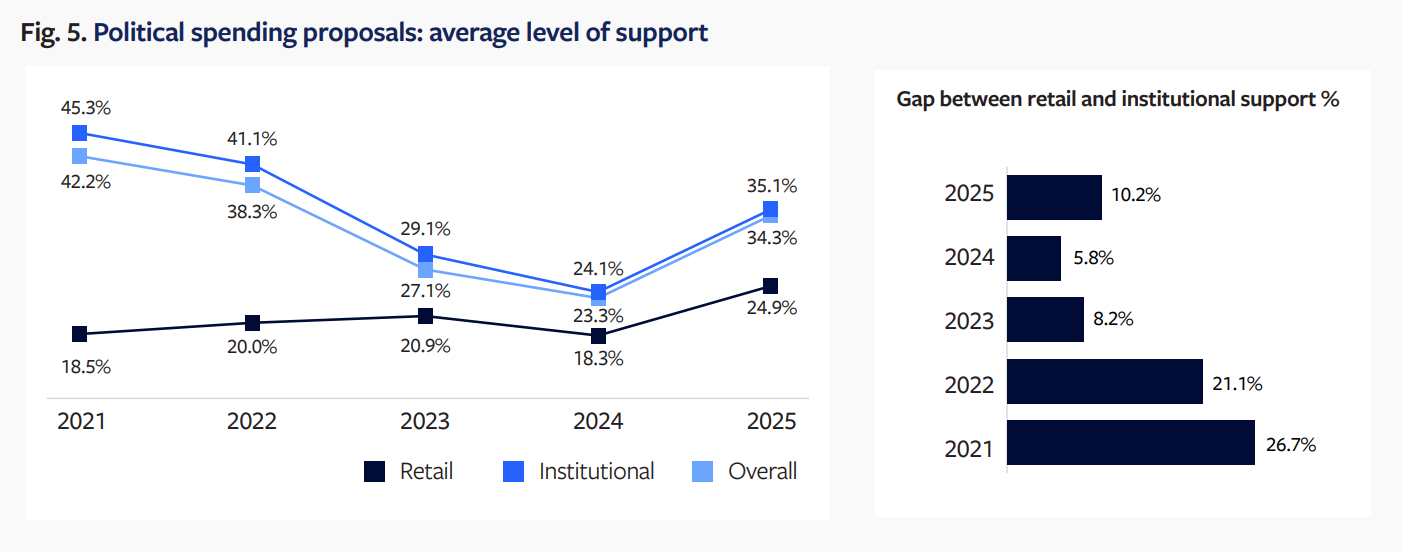

Political contributions

There was a 61% decrease in the number of these proposals, from 46 last season to 18 this season. However, overall shareholder support rose to 34.3%.

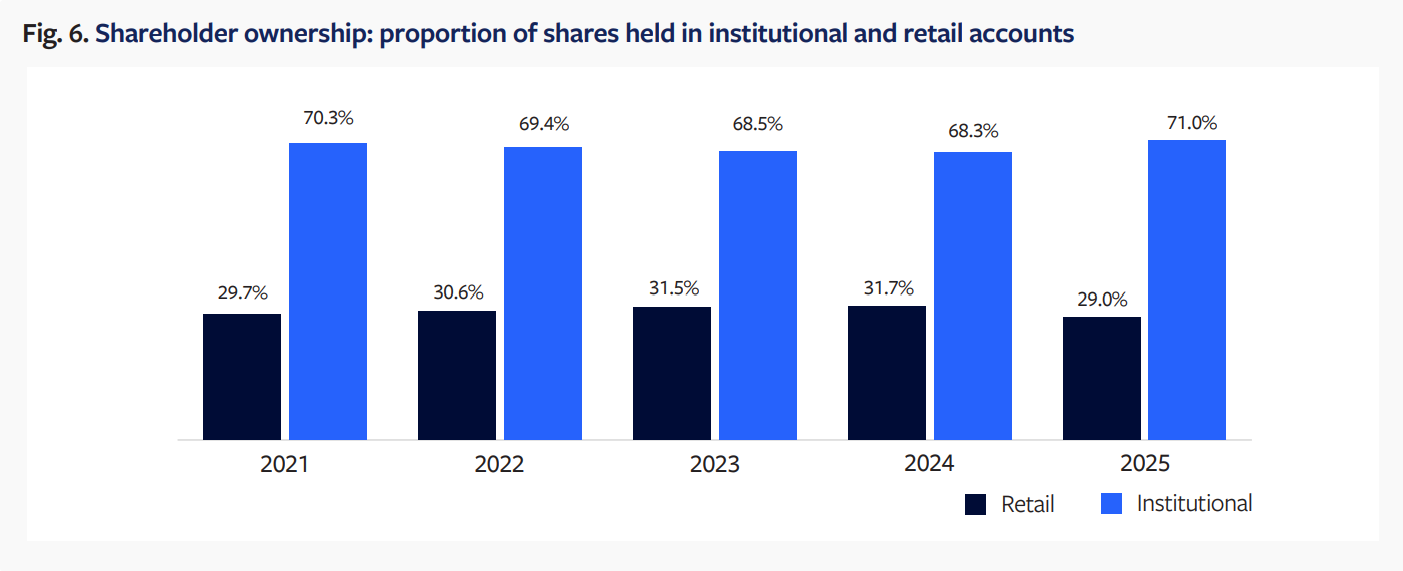

Share ownership

Although retail ownership increased by 25 million shares in 2025,4 the number of shares held by institutional investors rose by 22 billion, reflecting, in part, a continuing trend toward managed accounts and younger investors entering the markets.5

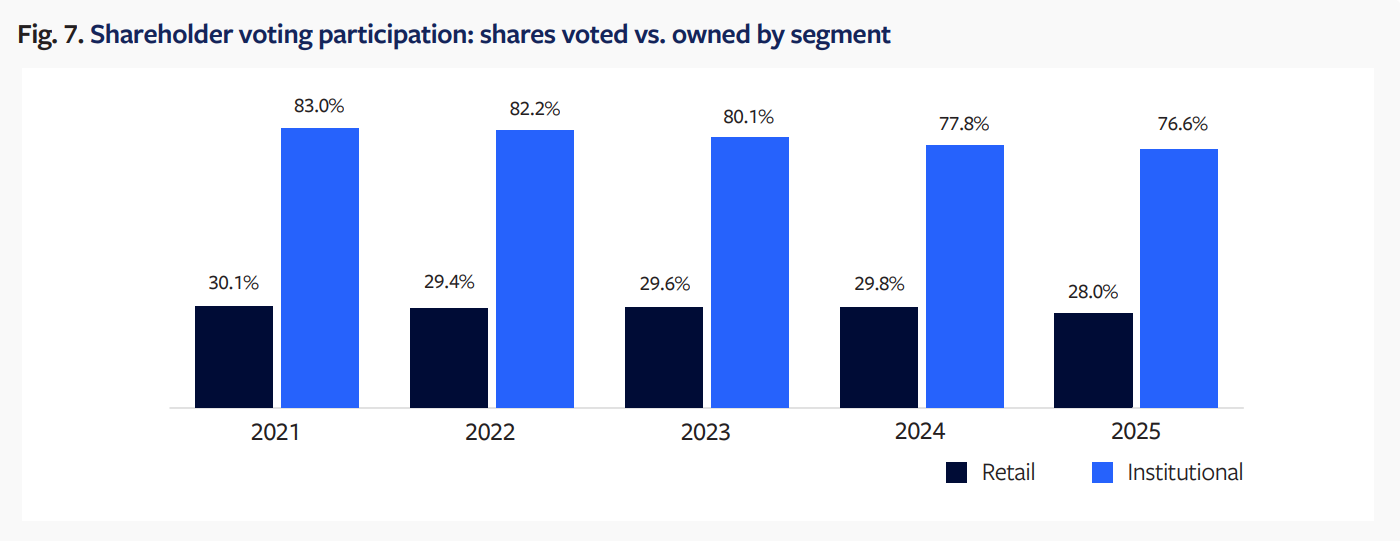

Shareholder voting

Voting by retail investors as a group declined to 28% of their shares owned in 2025, the lowest level in 9 years. Similarly, there was a decline in voting participation by institutional investors to 76.6%, the lowest level in at least 10 years. This downward trend is primarily due to decreased voting by smaller institutional investors, particularly at small and microcap companies.

Technology developments

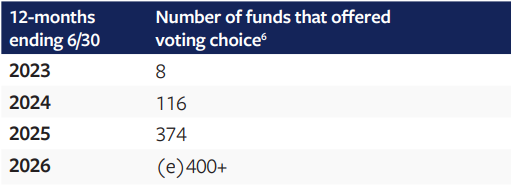

Voting choice

Broadridge is making it easier than ever for investors to have a voice in the governance of the companies they own, reflecting broader trends of increasing shareholder engagement and the democratization of investing. Today nearly 400 funds, managing a total of $1.8 trillion, offer a Broadridge voting choice solution to their shareholders. In 2025, a significant number of new funds (including international offerings and fund-of-fund structures) began to provide new ways for the voices of both U.S. and international owners to be heard. This trend is becoming a cornerstone of investment stewardship programs. Issuers are also expressing interest in technologies that enable more retail voices to be heard.

Virtual shareholder meetings

Companies continue to use Virtual Shareholder Meetings (VSM), with a record 1,931 VSMs in the first half of 2025, with 93% of VSMs providing a “live” question feature and 81% open to viewing by non-shareholder guests. As the regulatory environment remains fluid, effective digital and traditional communication and responsiveness to all stakeholders will be increasingly vital for successful corporate governance.

Data voting services

New services are emerging to provide institutional investors with greater access to publicly-available data and tools to analyze proposals and manage voting workflow.

What to expect in the 2026 proxy season

The corporate governance landscape is undergoing rapid change due, in large part, to executive, legislative, regulatory, and legal action. The data shows that these actions have had a measurable chilling effect on the number of shareholder proposals overall and on voting by institutional investors on environmental and social (“E&S”) issues. We expect this trend to continue.

The SEC is considering rule amendments and guidance to clarify and simplify disclosures on executive compensation, to reverse prior guidance on climate, and to further restrict the number of shareholder proposals.7 At the same time, technology developments, such as “pass-through voting” for mutual fund investors, are providing more opportunities for investors, shareholders, and companies to engage in governance matters. In addition, new services are emerging to provide institutional investors with greater access to publicly-available data and tools to analyze proposals and manage voting workflow. Use of Virtual Shareholder Meetings is expanding and most are now providing a “live” question capability for shareholders to engage directly with boards.

1The overall support level (based on the mean) is higher than both investor segments because overall averages can mask or reverse subgroup patterns (Simpson’s paradox).(go back)

2EY Center for Board Matters: 2025 proxy season review: four key takeaways (2025), p.8, https://www.ey.com/content/dam/ey-unified-site/ey-com/en-us/campaigns/ board-matters/documents/ey-cbm-2025-proxy-review-final-us-score-us.pdf(go back)

3Shareholder Proposals: Staff Legal Bulletin No. 14M (CF) (February 12, 2025), https://www.sec.gov/about/shareholder-proposals-staff-legal-bulletin-no-14m-cf(go back)

40.8 percentage points of the decline in retail ownership was due to one issuer that held a meeting in 2024 but not in 2025.(go back)

5Broadridge Investor Pulse (2025), https://investorpulse.broadridge.com/#/home.(go back)

6This includes the funds offering pass through voting utilizing Broadridge technology.(go back)

7The SEC has included “Rationalization of Disclosure Practices” on their Spring 2025 Regulatory Agenda, https://www.reginfo.gov/public/do/eAgendaMain/(go back)