Print

PrintSubodh Mishra is the Global Head of Communications at ISS STOXX. This post is based on an ISS-Corporate memorandum by Jun Frank, Head of Compensation & Governance Advisory, and Pinak Parikh, Compensation & Governance Advisor, at ISS-Corporate.

The corporate governance landscape is undergoing unprecedented changes. In the 2026 season, boards are heading into uncharted territory, with long-held governance norms upended, paradigm shifts challenging conventional wisdom, and changing investor priorities resulting in diverging definitions of “accepted best practice.” At the same time, AI is disrupting not only company operations but also the entire proxy ecosystem. Boards must face this brave new world without the guiding light of an established norm, and a lack of awareness of potential risks and varying investor expectations may lead to unexpected pushbacks from shareholders. This paper examines early trends emerging for the US proxy season.

Key Takeaways

- The Securities and Exchange Commission’s overhaul of the shareholder proposal process shifts power to companies, empowering them to decide which proposals to exclude and raising litigation risk and investor scrutiny. However, more than 70% of proposals for confirmed meetings have proceeded to a vote, reflecting a cautious approach to avoid the potential downsides of aggressive exclusions – at least among early filers.

- Early 2026 data show traditional governance and environmental proposals are resurging, while anti‑ESG proposals decline.

- While boards have enjoyed rising support in recent years, accountability pressures are intensifying. Investors may oppose directors, particularly governance committee chairs, based on how the board handles shareholder proposals, and there is heightened sensitivity to director compensation.

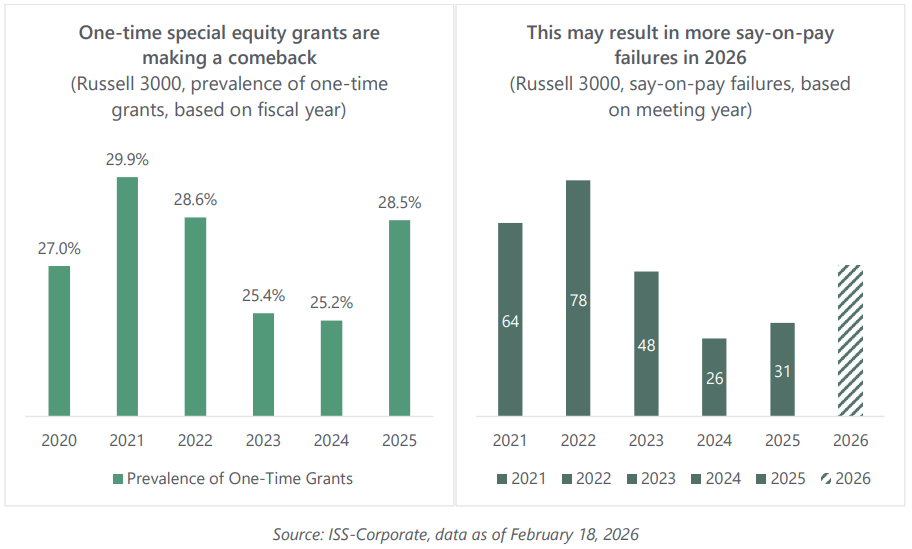

- The strong support on say-on-pay seen in 2024-2025 may be short-lived as executive compensation expectations shift toward longer time horizons with emphasis on pay and performance alignment over a five-year period, and a resurgence of one-time grants may result in more say-on-pay failures in 2026.

- AI is beginning to reshape governance and proxy ecosystems. Companies are expanding board‑level AI oversight disclosures, and institutional investors and service providers are beginning to incorporate AI tools into proxy voting value chain.

- Investor expectations are becoming more fragmented, with choice and customization increasing. Boards will have to navigate conflicting investor signals, identify common drivers of voting behavior, and tailor their engagement and disclosures across multiple viewpoints.

SEC Shift Upends Shareholder Proposal Votes

In a November 17, 2025 statement, the U.S. Securities and Exchange Commission’s Division of Corporate Finance announced a major change in how it will administer Exchange Act Rule 14a-8, fundamentally changing the balance of authority between corporate issuers, institutional shareholders, and the SEC itself, with significant governance, legal, and market implications.

Under the new guidance, the Division of Corporate Finance has largely retreated from its historic role as the arbiter of shareholder proposal disputes. While companies must still notify the SEC and proponents under Rule 14a-8(j), they now largely determine whether to exclude a proposal on their own, subject only to internal documentation that there was a reasonable basis for exclusion. This effectively shifts decision-making authority from the regulator to issuers, enhancing corporate control over proxy inclusion decisions.

While this new guidance at first glance appears to give a blank check to issuers to omit a shareholder proposal without staff evaluations of legal arguments, companies that exclude a proposal without SEC concurrence may face heightened litigation risk. Historically, SEC no-action letters provided informal assurance that enforcement action was unlikely, acting as a potential deterrent to shareholder court challenges. Under the revised process, shareholders dissatisfied with exclusions may seek redress through the courts or formal SEC appeals, increasing costs, uncertainty, and potential delays tied to annual meetings.

Investor advocates and stewardship groups say that this guidance weakens shareholder voices and could undermine long-established governance mechanisms. Critics argue that the absence of an SEC referee removes an orderly, time-honored means for resolving disputes and may lead to a chilling effect on shareholder proposals, especially on social and environmental topics. Proxy advisors, institutional investors and other market observers may also increase their scrutiny of exclusion decisions. Weakly supported exclusions could be seen as governance failings, potentially influencing voting for directors or other agenda items.

The SEC also issued an updated Compliance and Disclosure Interpretation on January 23, 2026, that could limit the reach and impact of vote no campaigns. Moving forward, the SEC will object to voluntary filings of Notice of Exempt Solicitation (Form PX14A6G). These filings are required for shareholders holding more than $5 million in a company’s securities when they solicit other shareholders without acting as a proxy, but often, smaller shareholders initiating a public campaign to urge other shareholders to support or oppose specific ballot items voluntarily file the form to raise awareness of the campaign. SEC’s objections to voluntary filings could limit smaller shareholders’ ability to reach other shareholders.

Legal and policy commentators see this change as part of a wider regulatory reassessment of shareholder rights, proxy advisory influence, and ESG-related engagement at US public companies. The Commission’s own statement emphasizes resource constraints but aligns with broader deregulatory trends that limit direct staff intervention in rule enforcement and defer to corporate self-analysis where extensive precedent exists.

Key changes in the SEC’s No-Action Process for the 2026 Proxy Season

Suspension of Most No-Action Responses

The Division will not review or issue no-action responses to companies’ requests to exclude shareholder proposals under Rule 14a-8 for the 2025-26 proxy season, except for requests under Rule 14a-8(i) (1) (i.e., that a proposal is an improper subject for shareholder action under applicable state law). Under the traditional process, companies sought staff concurrence that exclusion was appropriate. Under the new guidance, that substantive review is suspended.

Continued Rule 14a-8(j) Notice Requirement

Companies seeking to exclude a shareholder proposal must still comply with Rule 14a-8(j) by notifying the Commission and the proponent at least 80 calendar days before filing their definitive proxy statement. The notice must include the proposal and the company’s explanation for why it believes exclusion is appropriate.

Optional Non-Objection Response

Although the staff will not provide substantive no-action letters for most exclusions, a company may include in its Rule 14a-8(j) notice an “unqualified representation” that it has a reasonable basis to exclude the proposal based on Rule 14a-8, prior published guidance, and/or judicial decisions. If this representation is included, the staff may issue a simple letter stating it will not object to the exclusion, based solely on the company’s representation, without evaluating the legal merits.

No Impact on Rule 14a-8(i) (1) Process

The staff will continue to review and respond to no-action requests under Rule 14a-8(i) (1) – that a proposal is not a proper subject for shareholder action under state law – recognizing that there is an insufficient body of guidance for companies and proponents on state-law questions such as whether nonbinding proposals are permissible under state corporate law.

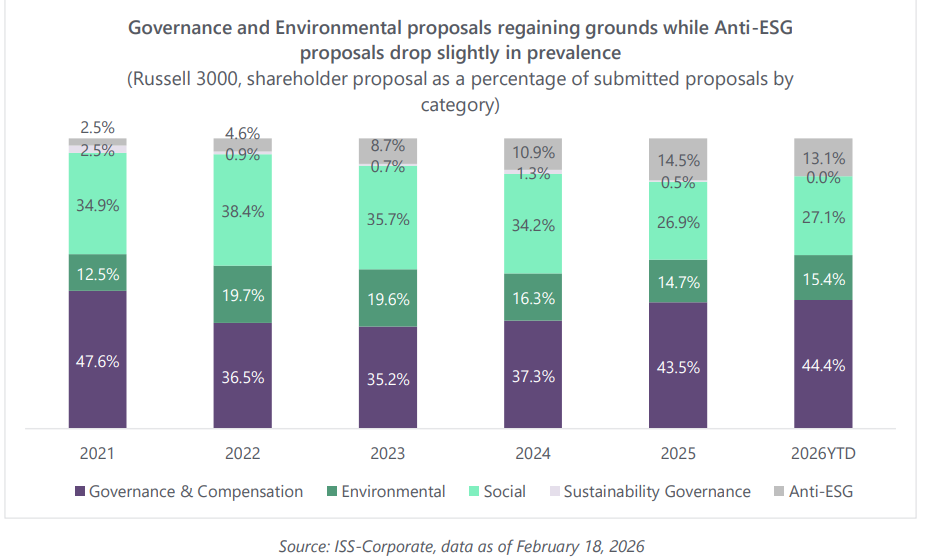

So far this year (as of mid-February), we are tracking 214 shareholder proposal submissions, and early indications suggest a meaningful shift in their composition. Governance & Compensation and Environmental proposals appear to be regaining prominence, while anti-ESG proposals represent a smaller portion of proposal submissions thus far. While it is still early to draw any firm conclusions, this provides a useful snapshot of what proponents are prioritizing. Governance and environmental themes are not only persisting, but may be strengthening relative to other categories. This trend is consistent with a broader reversion to “traditional” shareholder rights and oversight themes, alongside sustained investor focus on climate-related risks and environmental disclosure. By contrast, the relative decline in anti-ESG submissions suggests that the surge observed in prior years may be moderating. Many factors may be contributing to the reduction, including reduced proponent activity, evolving corporate response strategies, a lack of investor support for previous proposals, and corporate actions curtailing DEI or environmental activities and disclosures.

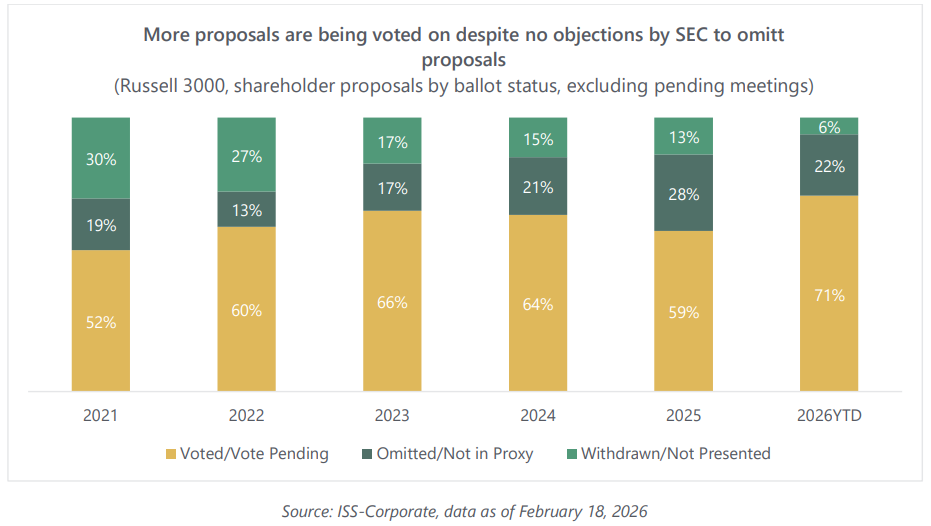

Among the subset of companies that have already filed definitive proxy statements, the treatment of shareholder proposals is particularly notable. Despite the SEC’s new approach to shareholder proposal exclusions and procedural scrutiny, more than 71% of proposals submitted are being put on the ballot, excluding proposals where the proxy statement has not been filed yet. By contrast, omissions spiked last year following the new Staff Legal Bulletin no. 14M (CF). Omitted proposals rose from 21% in 2024 to nearly 30% in 2025, suggesting that issuers were more willing to pursue exclusion as a primary response strategy, and the SEC was more permissive in granting no-action relief.

Early outcomes this year suggest that there may not be a sustained escalation in omissions. This would be a striking reversal from 2025 and implies that issuers may be reassessing the strategic value of omissions and the risks associated with it. If the SEC staff is less willing to engage in detailed substantive analysis, making exclusion outcomes more uncertain, the cost-benefit calculus may favor letting proposals go to a vote rather than risk litigating the boundaries of Rule 14a-8. The corporate response strategy may change as the season unfolds, but so far many issuers have taken a cautious approach to avoid the cost, uncertainty, and reputational downside of aggressive exclusion.

Board Accountability in Sharper Focus

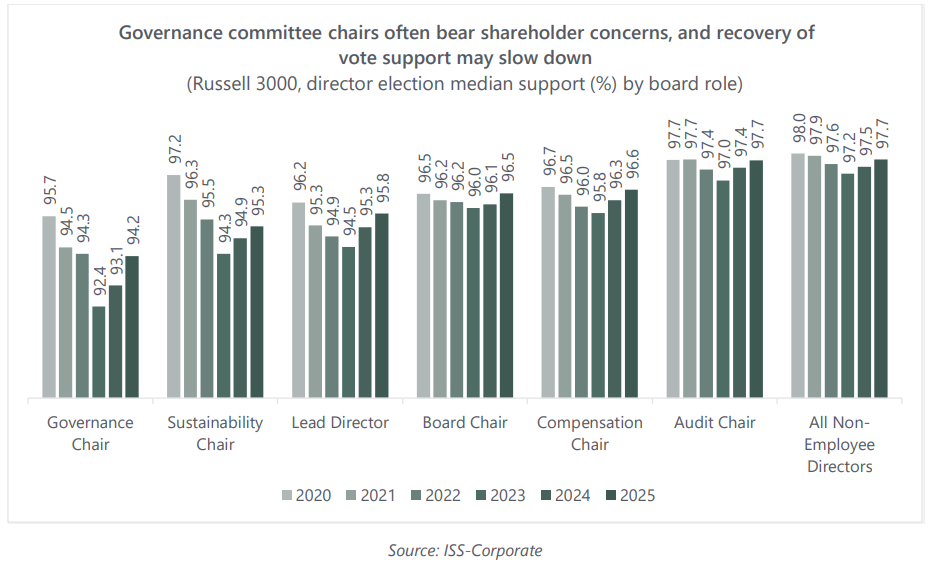

After years of declining support, support for director elections has rebounded recently, with boards receiving strong investor backing in 2025. However, the recent trend of improving support may come to a halt.

Shareholder proposals have long been a key channel for investors to express their preferences and concerns. If shareholders are prevented from voting on proposals that they view as potentially beneficial, they may instead register their dissatisfaction by opposing director elections—much as they once used compensation committee elections to signal concerns before the advent of say-on-pay. Shareholders may hold board members accountable when they disagree with the board’s handling of shareholder proposals or when governance issues arise without a specific ballot item to address them.

Governance committee chairs consistently receive the lowest support among directors, reflecting shareholders’ inclination to target those responsible for the company’s governance when they are concerned with its practices or the board’s composition. Although support for these chairs has improved significantly in recent years—driven by easing pressure on board diversity, greater investor deference on governance and sustainability issues and better overall practices—future support is uncertain. Directors, especially governance committee chairs, may face increased scrutiny this proxy season depending on how boards handle shareholder proposals and broader governance matters.

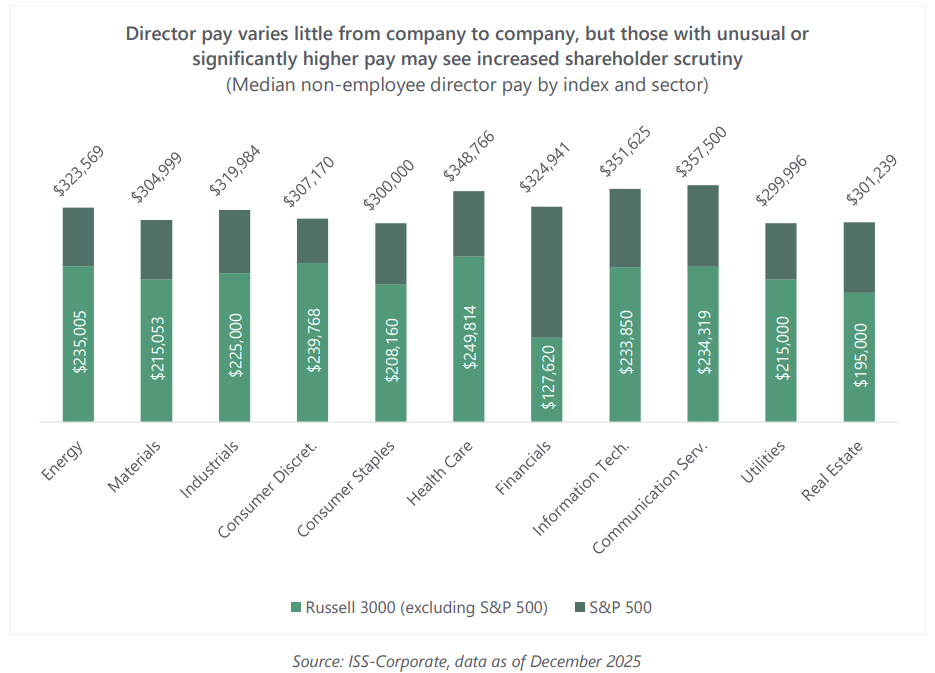

Not only will boards’ handling of shareholder proposals face closer scrutiny this proxy season, but so will how directors pay themselves. Director compensation has long influenced investors’ views on independence and accountability, and it has drawn renewed attention amid debates over the Tesla board’s independence and whether high pay affected its judgement. In the 2017 ISS Policy Survey, most investor respondents favored opposing directors when they perceived a pattern of excessive non-employee director pay. In the 2025 survey, more than 98% of investor respondents said that problematic non-employee director pay warrants immediate opposition regardless of whether there is a pattern, underscoring heightened concern over the issue. In this environment, boards with compensation practices that significantly diverge from market norms or with directors whose pay far exceeds peers may face stronger investor pushback this season.

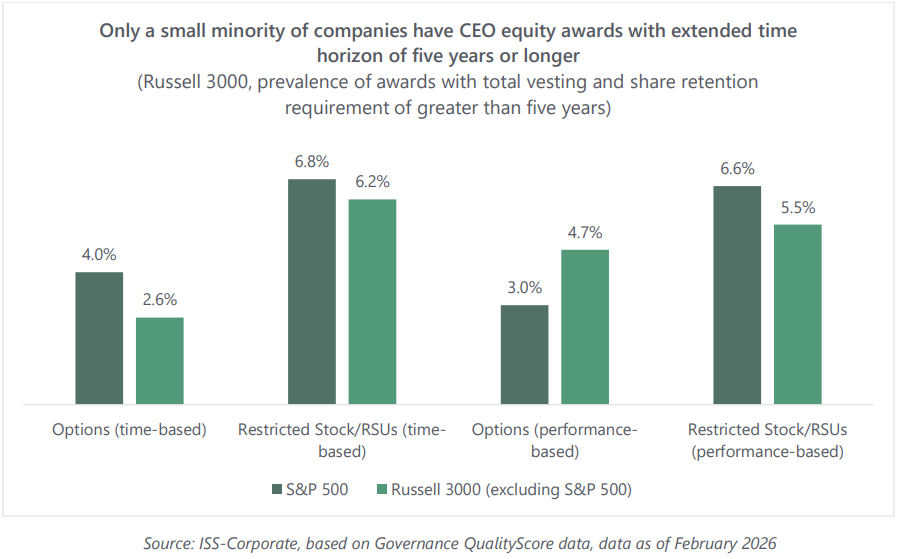

Emphasis on Longer-Term Time Horizon

As scrutiny of director pay grows, investor perspectives on executive compensation are also shifting, with greater emphasis on longer time horizons. Some investors have been voicing concerns over executive incentives, calling for a simplification of long-term incentives (LTI) and extending horizons beyond the typical three years. The Council of Institutional Investors defines “long-term” as at least five years; Norges Bank advocates for time-based awards vesting over five to ten years; and CalPERS evaluates CEO pay-forperformance alignment using a five-year framework. Against this backdrop, both Glass Lewis and Institutional Shareholder Services (ISS) have updated their policies, extending the time horizon used in analyzing pay and performance alignment from three years to five years.

These developments signal growing skepticism toward performance-based awards and increasing acceptance of time-based equity with an extended horizon as a way to align executives with shareholders’ long-term interests. In the 2025 ISS Policy Survey, investor respondents indicated general support for use of extended time-based awards in place of performance-based awards, with the extended time horizon achieved through a combination of vesting and addition share retention requirements. However, CEO equity awards with extended time horizons remain uncommon, and it remains to be seen if they will become more widely used. Regardless, as companies prepare for proxy filings, boards should consider the heightened emphasis on longer time horizons and evaluate how their pay programs and disclosures will be assessed under these evolving expectations.

Resurgence of One-Time Grants

Companies have enjoyed strong say-on-pay (SOP) support in recent years, with failures dropping sharply since 2022. However, the 2026 proxy season may see an uptick in SOP failures. SOP failures spiked in 2021- 2022, coinciding with an uptick in one-time discretionary equity grants issued during and after the Covid-19 pandemic. The SOP outcomes stabilized as those grants faded. Now, uncertainty stemming from tariffs, trade tensions, AI-related disruption, and executive transitions is prompting companies to once again turn to those one-time discretionary awards. Based on fiscal 2025 disclosures to date, 28.5% of Russell 3000 companies have issued one-time awards to NEOs, excluding new hires or promotional grants. This renewed use of special awards in turn may trigger stronger shareholder rebukes against executive pay programs, and SOP failures may increase this year.

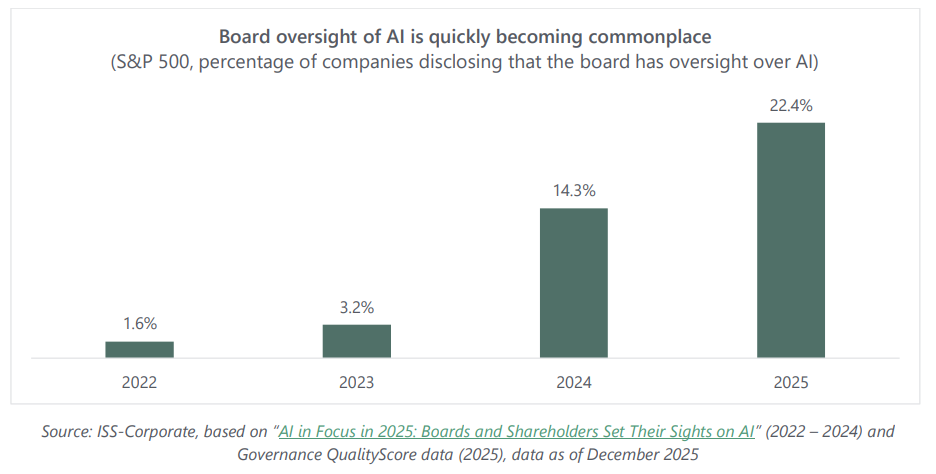

AI Takes the Center Stage

AI is expected to play a larger role this proxy season, from expanded board-level AI oversight disclosures to the use of AI in proxy analysis and voting. S&P 500 companies explicitly identifying AI as a board oversight issue have risen sharply1 , from 3.2% in 2023 to more than 20% in 2025. As investor focus on AI governance intensifies, more companies are expected to articulate how their boards monitor AI-related risks and opportunities in their proxy statements. At the same time, AI is becoming part of the proxy-related risks and opportunities in their proxy statements. At the same time, AI is becoming part of the proxy-voting-voting process itself. J.P. Morgan Asset Management has reportedly begun using an internal AI-driven tool to help cast votes at roughly 3,000 U.S. company meetings. This season, a growing proportion of votes may be influenced or assisted by AI.

Complexity in Investor Perspectives

The investor community is not monolithic, and stewardship priorities, investment philosophies, and proxy voting policies are becoming increasingly diverse and complex. Preferences may vary widely on any given topic, including executive pay design, climate change or board diversity. In response, investors and service providers are evolving to offer more choices and greater customization. Several major institutional investors are splitting their stewardship teams to accommodate differing views on stewardship. Large investors are also expanding pass-through voting and voting choice programs to further empower underlying beneficiaries to direct how votes are cast.

Proxy advisors are evolving as well. ISS recently introduced Gov360, which provides research reports without vote recommendations, and Custom Lens, which allows clients to tailor data, analyses, and recommendations. Glass Lewis has announced it will phase out its benchmark policy over the next two years, shifting clients to custom or thematic policies. In 2026, Glass Lewis plans to help clients move beyond the benchmark framework and later offer multiple policy perspectives within a single report.

This surge in customization, beneficiary empowerment, and diversified voting frameworks is adding new complexity to the upcoming proxy season. These developments may erode the notion of an accepted governance norm, making it harder to decipher investor expectations and the key drivers of voting decisions. Boards may need to consider multiple perspectives—especially on contentious issues—to secure investor support and avoid missteps. At the same time, greater choice does not mean core governance principles or shared investor values have fundamentally changed. As proxy season approaches, boards should closely track market sentiment, identify the common drivers of voting behavior, assess how their actions and disclosures align with the range of investor viewpoints, and evaluate how to address or manage diverging views.