Print

PrintLinda Pappas is a Principal and Tara Tays is a Partner at Pay Governance LLC. This post is based on their Pay Governance memorandum.

Key Takeaways

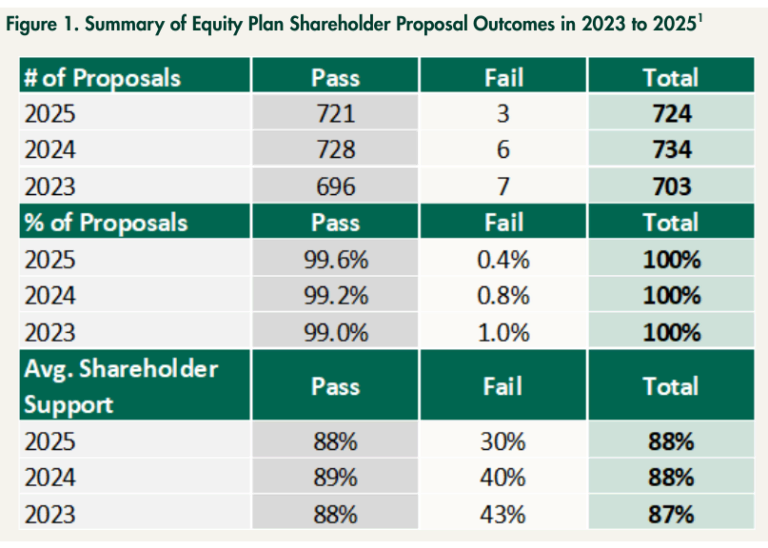

- Nearly 25% of Russell 3000 companies submitted an equity plan proposal in 2025. Shareholder support was strong at 88% on average, and less than 1% of proposals failed to receive majority support, consistent with 2023 and 2024 levels

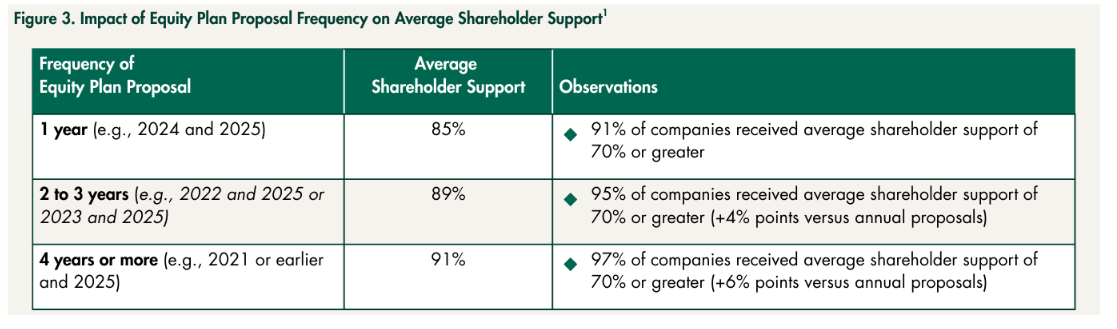

- It is most common for companies to return to shareholders every 2 to 3 years to seek equity plan approvals

- While proxy advisor opposition to equity plan proposals typically results in lower shareholder support, the proposal failure rate increases only modestly (to a failure rate of less than 4%)

- Among the limited number of companies that failed to receive shareholder support over the last two years, approximately half were in the health care (e.g., pharma/biotech) sector

- Companies can take several steps to improve the likelihood of a successful shareholder vote outcome, including: analyzing share reserve needs, assessing potential dilution, understanding top shareholder voting policies and proxy advisor concerns, and clearly disclosing the shareholder-friendly features of the equity plan

A Review of Russell 3000 Equity Plan Proposals

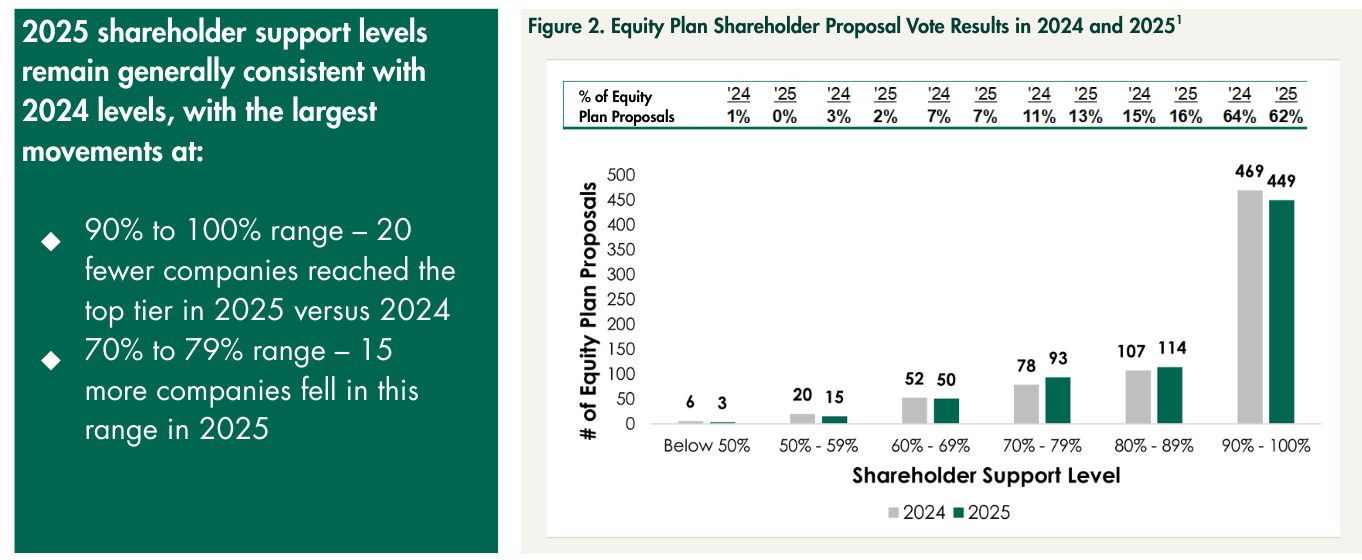

In 2025, we observed a similar number of equity plan proposals and shareholder support levels as in 2023 and 2024, with approximately 25% of the Russell 3000 (over 700 companies) submitting an equity plan proposal. Companies received significant support from shareholders on their 2025 equity plan proposals – about 88% support on average – and 0.4% of equity plan proposals failed to receive majority support.

Frequency of Equity Plan Proposals Submitted to Shareholders

We analyzed the frequency of equity plan proposals submitted for shareholder approval over the last 10 years among the Russell 3000, which resulted in the following conclusions:

- It is most common to return to shareholders every 2 to 3 years to seek equity plan approvals

- Equity share pools at utilities and consumer staples companies typically last the longest, with new requests every 4 years, on average

- Health care (e.g., pharma/biotech), information technology, and communication services (e.g., media and entertainment) industry sectors generally go back for more shares more frequently, 2 years on average

We also reviewed the correlation between frequency of equity plan proposals and average shareholder support and observed the following:

- The majority of companies received strong support regardless of how frequently the company requested additional shares

- There was a moderate decrease in average shareholder support as the frequency of proposals increased

- Among companies that submitted back-to-back equity plan proposals, the year-over-year change in shareholder support remained generally flat at +0.3% on average

Impact of Proxy Advisors’ Recommendations on Equity Plan Proposal Outcomes

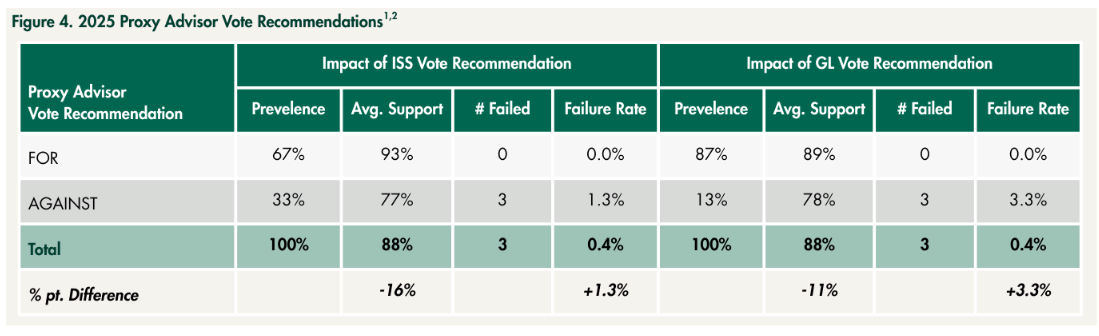

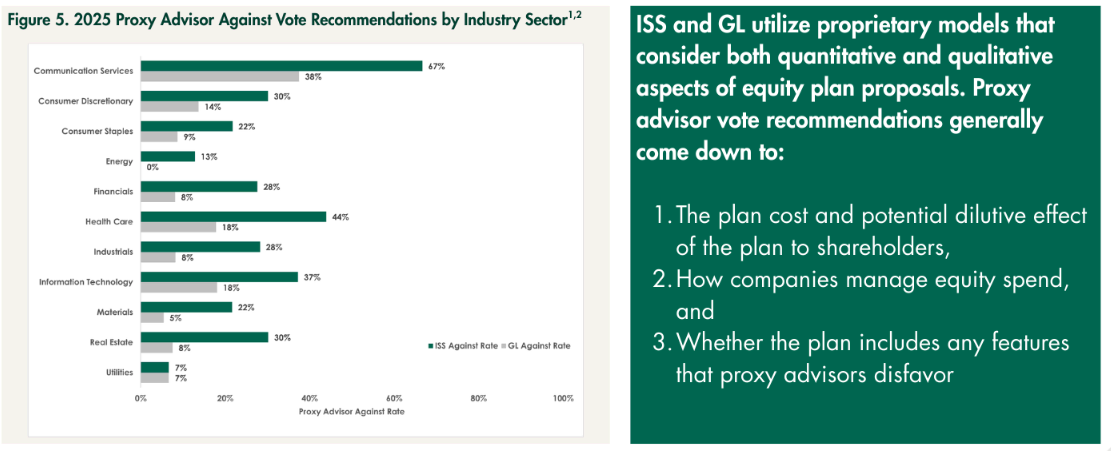

The majority of Russell 3000 companies received favorable recommendations from proxy advisors on their equity plan proposals (67% received support from Institutional Shareholder Services (ISS) and 87% received support from Glass Lewis (GL)). Companies that received ISS or GL opposition, on average, received lower shareholder support by about 16 percentage points and 11 percentage points, respectively. However, the equity plan proposal failure rate increased very modestly (to 1.3% when ISS is in opposition and to 3.3% when GL is in opposition).

When examining average shareholder support based on industry sector (2-digit global industry classification standard (GICS)) as shown in figure 5, we observed the following:

- Industry sectors with relatively high ISS opposition (30% and greater) included communication services (e.g., media and entertainment), health care (e.g., pharma/biotech), information technology (e.g., technology and telecommunications), consumer discretionary (e.g., retail), and real estate. Only the communication services sector had GL opposition above 30%

- The industry sectors with the lowest opposition from ISS and GL were utilities (7% from both ISS and GL) and energy (15% from ISS and 0% from GL)

Key Equity Plan Proposal Considerations

As companies prepare for equity plan proposals, there are several things that can be done to increase the likelihood of a successful shareholder vote outcome as highlighted below.

- Analyze the share reserve pool under various stock price scenarios to estimate how many shares are needed over the next 1 to 3 years.

- Calculate current and potential dilution levels and share usage levels on an absolute basis and relative to the company’s peer group and overall industry sector.

- Understand the voting guidelines on new share requests of the company’s largest institutional shareholders, including any brightline policies such as excessive dilution or burn rate thresholds.

- Understand proxy advisor “dealbreakers” and estimate the likelihood of proxy advisors’ vote recommendations on the proposal. If opposition is anticipated, consideration should be given to engaging with the largest shareholders well before the annual shareholder meeting.

- Ensure the proxy disclosure of the equity plan proposal is clear and complete. Within the equity plan proposal disclosure, highlight shareholder friendly design features and practices (e.g., reasonable dilution and share usage levels, requiring shareholder approval of option repricings or cash buyouts) and the role equity plays in attracting, motivating, and retaining employees as well as why it is important to the success of the company.

By thoughtfully incorporating these considerations, companies can improve the likelihood of a smooth equity plan proposal process and a successful shareholder vote outcome.