Print

PrintThe 2026 proxy season unfolds amid significant shifts in the regulatory, political, and investor landscape, reshaping how shareholder proposals are filed, evaluated, and voted. Following record activity in 2024 and a modest pullback in 2025, companies now face a proxy environment defined less by volume and more by discretion, legal complexity, and evolving investor expectations.

Trusted Insights for What’s Ahead®

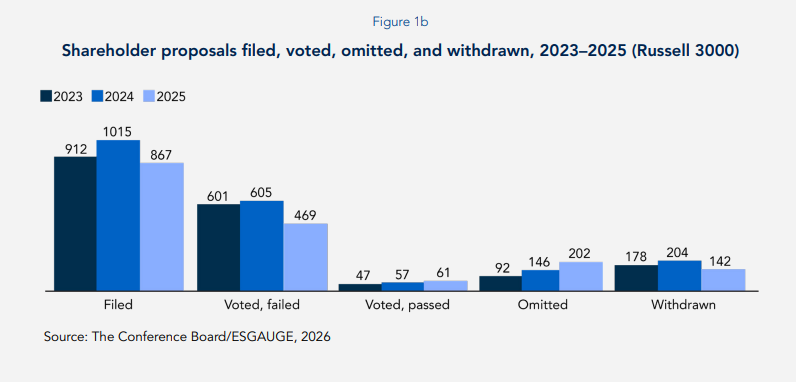

- More shareholder proposals are being resolved off the ballot rather than put to a vote. Negotiation, withdrawal, and omission increasingly shape outcomes, raising the bar for proposals to advance.

- Procedural changes have materially reshaped the shareholder proposal process. Record no-action activity, the US Securities and Exchange Commission’s (SEC’s) retreat from routine staff review, and tighter rules on exempt solicitations place greater responsibility—and risk—on issuers and proponents.

- Voting outcomes are becoming less predictable as decision-making grows more contextual. Asset managers and proxy advisors continue to rely less on rigid policy frameworks and more on issuer-specific facts, disclosure quality, and demonstrated responsiveness.

- Proxy disclosure is emerging as a central stewardship tool in a more constrained engagement environment. As informal engagement and procedural guardrails narrow, clear, decision-oriented proxy disclosure plays an increasingly important role in shaping investor understanding and voting behavior.

Shareholder Proposals

Overall trends

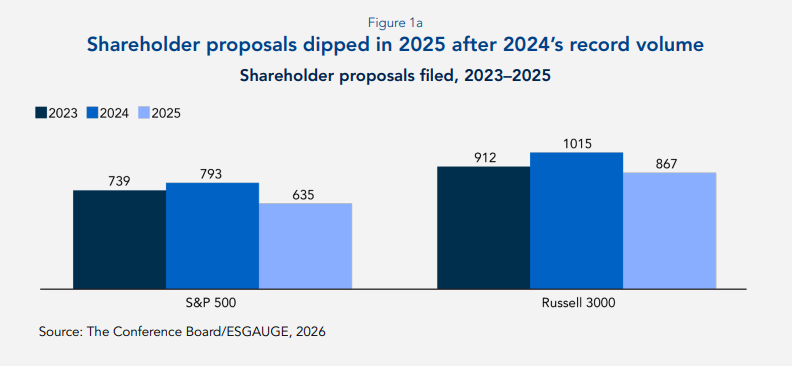

After reaching record levels in 2024, shareholder proposal activity moderated in 2025 across both the Russell 3000 and the S&P 500. While fewer proposals were filed, a larger share were resolved through negotiation, withdrawal, or omission rather than votes at annual meetings, reflecting heightened issuer caution following changes to SEC guidance under Rule 14a-8.

Looking ahead to 2026, proposal volume may remain subdued, but scrutiny of proposal design, engagement practices, and exclusion decisions is expected to intensify.

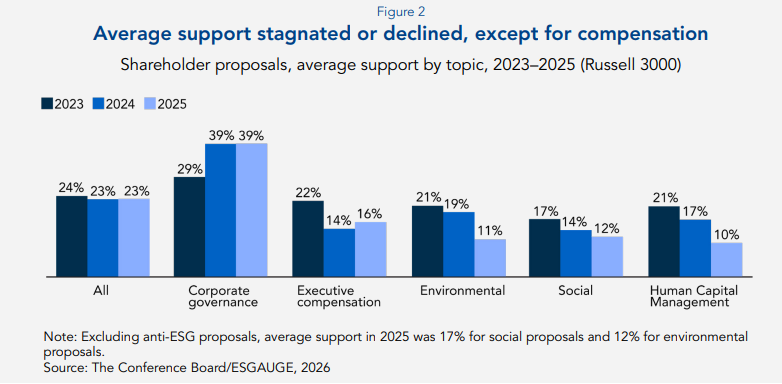

Average shareholder support for proposals remained stagnant or declined slightly in 2025 across most categories, continuing patterns observed in recent years. Governance and executive compensation–related proposals were most likely to attract support, reinforcing investor prioritization of issues perceived as directly tied to board accountability, pay alignment, and oversight effectiveness. Support for environmental, social, and human capital management proposals was comparatively subdued, reflecting investor concerns about prescriptive requests, limited economic relevance, and duplication of existing disclosures. Proposals that are narrowly tailored, company specific, and clearly linked to material risk or performance are more likely to gain traction.

Anti-ESG proposals: rising filings, higher omission rates

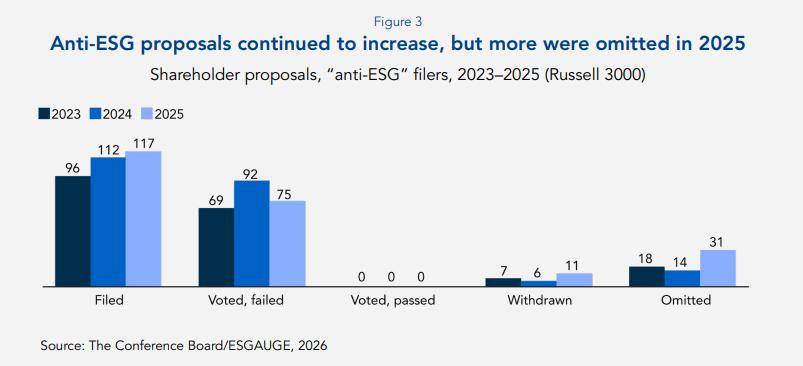

Anti-ESG proposals increased as a share of filings in 2025 but were more frequently omitted or withdrawn than in prior years, suggesting that issuers were more willing to challenge or negotiate such proposals under a shifting regulatory framework. Despite sustained media attention, these proposals continued to receive minimal shareholder support, reinforcing that they remain outside the mainstream of institutional investor priorities.

Heading into the 2026 proxy season, issuers may continue to face pressure from anti-ESG proponents, but data suggest that support outcomes will remain limited absent a clearer connection to financial materiality or governance risk.

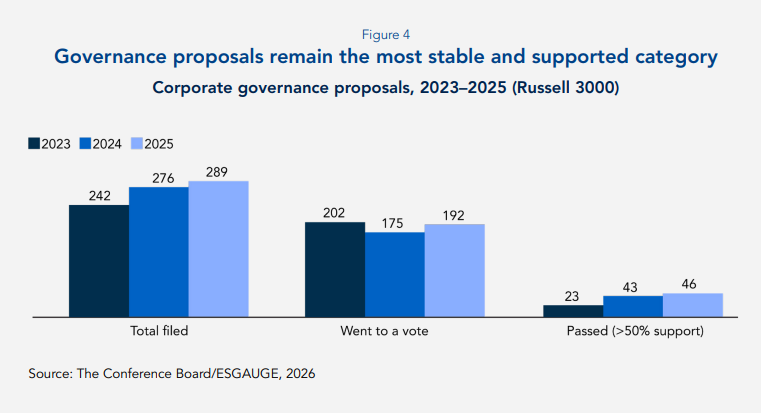

Governance and executive compensation proposals

Governance proposals continued to represent the most stable and consistently supported category of shareholder proposals in 2025. Such proposals accounted for the largest share of filings and attracted the highest average support, reflecting sustained investor emphasis on board accountability and structural oversight.

Proposals addressing shareholder rights—such as the ability to call special meetings, eliminate supermajority voting thresholds, or declassify boards—continued to perform relatively well, reflecting investor receptiveness to structural governance changes that enhance accountability without prescribing specific operational outcomes. By contrast, governance proposals perceived as duplicative of existing practices or insufficiently tailored to company-specific circumstances were more likely to receive limited support or to be withdrawn or omitted.

Looking ahead to the 2026 proxy season, governance proposals are likely to remain a focal point of shareholder activity. However, proposals that are narrowly framed, grounded in clearly articulated governance gaps, and aligned with prevailing market norms will continue to be favored. As investor voting frameworks become more discretionary, issuers that proactively address governance concerns through disclosure and engagement may reduce both proposal volume and the likelihood of contentious votes.

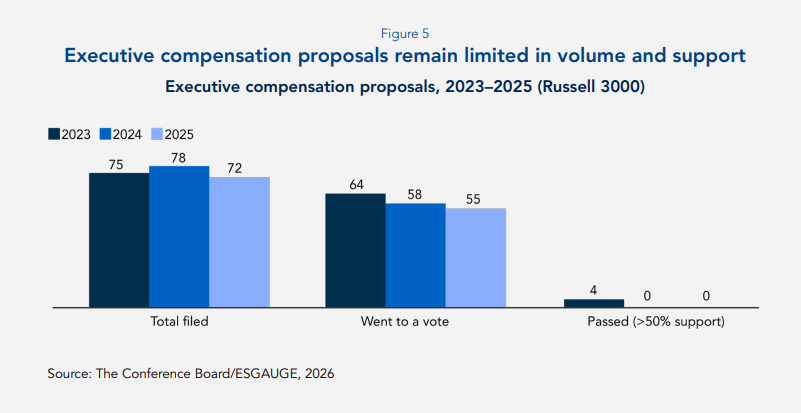

Executive compensation proposals, while lower in volume, continued to serve as an important signaling mechanism, with investors favoring engagement and say-on-pay votes over prescriptive shareholder resolutions. Proposals that advanced were often viewed as duplicative of existing disclosure requirements or insufficiently responsive to company-specific performance context, limiting their effectiveness as a mechanism for driving change.

Heading into the 2026 proxy season, executive compensation proposals are expected to remain a secondary channel for shareholder engagement on pay issues. Investors appear more likely to focus on pay-for-performance alignment, the use of discretion, and responsiveness to prior voting outcomes through say-on-pay and director elections, reinforcing the importance of clear, decision-oriented disclosure and proactive engagement around compensation design and outcomes.

Environmental and social proposals

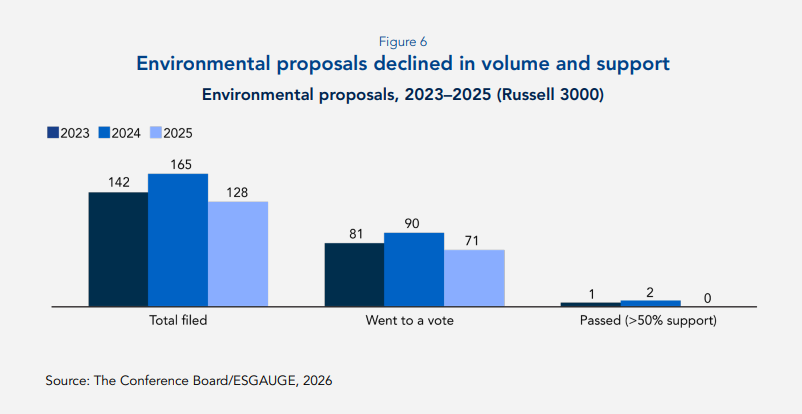

Compared to the preceding two years, environmental proposals declined in both volume and shareholder support in 2025: fewer proposals were filed, fewer reached a vote, and none received majority support. Average support levels remained low for climate-related proposals, the dominant topic within this category, reflecting sustained investor skepticism about proposals perceived as prescriptive, duplicative, or insufficiently tied to company-specific financial risk.

Several factors appear to be shaping this outcome. Improved corporate climate disclosures and governance practices have reduced investor appetite for additional reporting-focused proposals, while regulatory uncertainty and legal risk have increased caution around mandates that could constrain board or management discretion. At the same time, large institutional investors have emphasized a preference for engagement and oversight of climate risk through existing governance channels rather than through shareholder-submitted resolutions.

Heading into the 2026 proxy season, environmental proposals are likely to remain a challenging path for proponents. Proposals that advance are expected to be narrow in scope, sector specific, and explicitly linked to material operational or financial risks, while broad or highly prescriptive climate requests are likely to continue facing limited shareholder support.

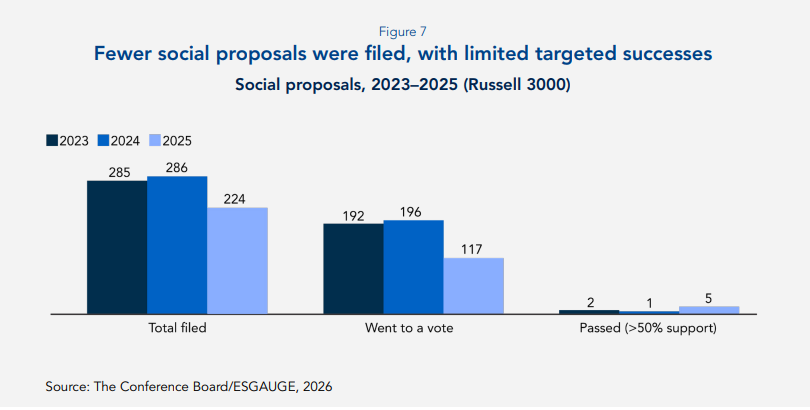

Social proposals also experienced a meaningful decline in filing volume and voting activity in 2025, although a small number of targeted proposals achieved successful outcomes, contributing to a modest increase in the number of proposals passing despite lower overall support levels.

Political spending and lobbying disclosure remained the most frequently filed social topic, and proposals in this area accounted for the majority of successful outcomes in 2025. By contrast, proposals addressing broader social or public policy concerns—particularly those perceived as symbolic, duplicative, or lacking a clear connection to company performance—continued to receive limited support.

Looking ahead to 2026, social proposals are likely to remain few in number and selective in scope. Proposals that focus on governance-adjacent issues—such as political activity oversight or risk management frameworks—may continue to find traction, while expansive or ideologically framed proposals are expected to face continued headwinds.

| Artificial intelligence (AI) proposals

Proposals addressing AI governance, transparency, and risk management have increased steadily since 2022. To date, these proposals have attracted limited shareholder support, reflecting investor preference for board-level oversight and engagement over prescriptive resolutions. Heading into 2026, AI proposals are likely to remain selective and company specific, with greater emphasis on governance readiness than on operational mandates. |

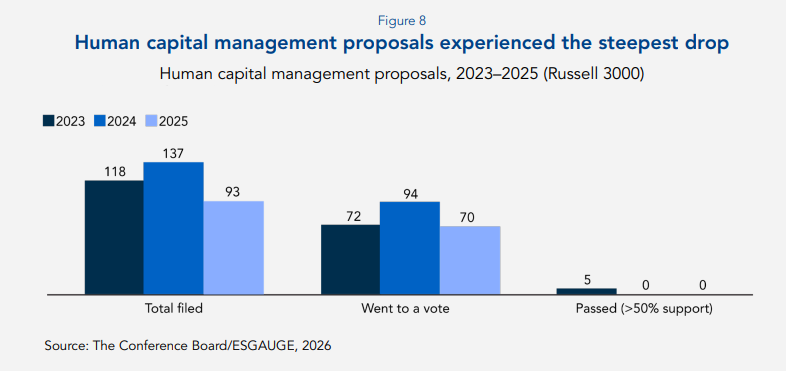

Human capital management proposals

Human capital management (HCM) proposals recorded the steepest decline of any proposal category in 2025. Filings dropped sharply, fewer proposals advanced to a vote, and average shareholder support fell to the lowest level across all proposal types. This contraction followed a peak in 2024 and reflects growing investor selectivity amid heightened legal, political, and regulatory scrutiny of workforce-related issues.

While investors continue to view workforce risks—such as pay equity, workplace safety, and talent management—as financially material, many HCM proposals were viewed as overly prescriptive, duplicative of existing disclosures, or insufficiently tailored to company-specific circumstances. Proposals related to diversity, equity & inclusion (DEI) were particularly affected, as legal challenges and political developments increased caution among both issuers and investors.

As companies look ahead to the 2026 proxy season, HCM proposals are likely to remain limited in number and closely scrutinized. Investors appear more inclined to address human capital issues through engagement and board oversight than through shareholder resolutions, suggesting that clear disclosure of workforce strategy, governance structures, and risk management practices will be increasingly important in shaping investor confidence.

SEC developments

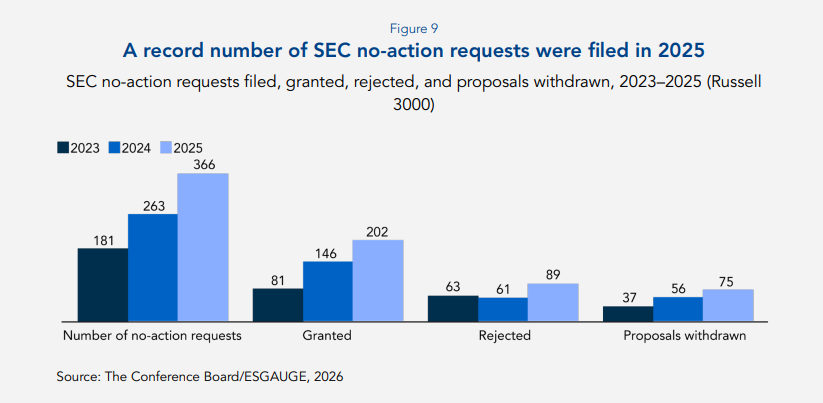

The use of SEC no-action requests under Rule 14a-8 has fluctuated but remained elevated in recent years, reflecting sustained issuer reliance on the staff process to address shareholder proposal eligibility.

The relative dip in no-action requests observed in 2023 followed the SEC’s issuance of Staff Legal Bulletin No. 14L, which emphasized broad societal impact and limited the availability of the “ordinary business” and “economic relevance” exclusions under Rule 14a-8, narrowing the bases on which companies could exclude shareholder proposals. As a result, issuers were less likely to pursue exclusion challenges—particularly for environmental and social proposals—and more inclined to include proposals or engage with proponents.

This dynamic reversed in 2025 as Staff Legal Bulletin No. 14M rescinded SLB 14L and reinstated a more restrictive interpretation of the “ordinary business” and “economic relevance” exclusions, prompting a surge in no-action requests as issuers reassessed exclusion opportunities under the restored framework. Later in November 2025, the SEC’s Division of Corporation Finance announced that it would no longer provide staff review or “no-action” responses for most shareholder proposal exclusions, marking a sharp departure from the staff’s historic gatekeeping role. Beginning in the 2025–2026 proxy season, companies may exclude proposals without first obtaining staff concurrence, subject to notice requirements under Rule 14a-8(j) and the risk of post-filing challenges by proponents.

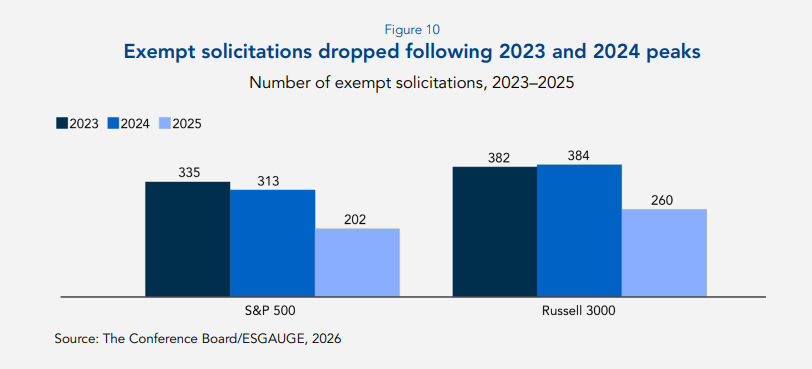

Following elevated use in 2023 and 2024, exempt solicitations declined in 2025. This pullback suggests that while exempt solicitations—originally intended to facilitate limited communications around proxy voting—have evolved into a tactical tool for shareholder signaling, their use has remained episodic and sensitive to procedural risk and regulatory scrutiny. The SEC’s January 2026 guidance, which clarified that shareholders below the $5 million ownership threshold may no longer submit voluntary Notices of Exempt Solicitation and tightened the definition of what constitutes a permissible solicitation, appears calibrated to this pattern, reinforcing narrower use of exempt solicitations at a time when issuers and proponents alike are reassessing escalation strategies.

With fewer procedural guardrails and diminished opportunities for informal SEC intervention, companies are expected to exercise greater caution in close-call exclusion decisions, strengthen internal legal and governance review processes, and engage earlier with proponents to mitigate litigation, regulatory, and reputational risk. At the same time, proponents may increasingly rely on negotiation, litigation, or exempt solicitation strategies—now subject to heightened scrutiny—rather than traditional staff-mediated exclusion challenges.

Management Proposals

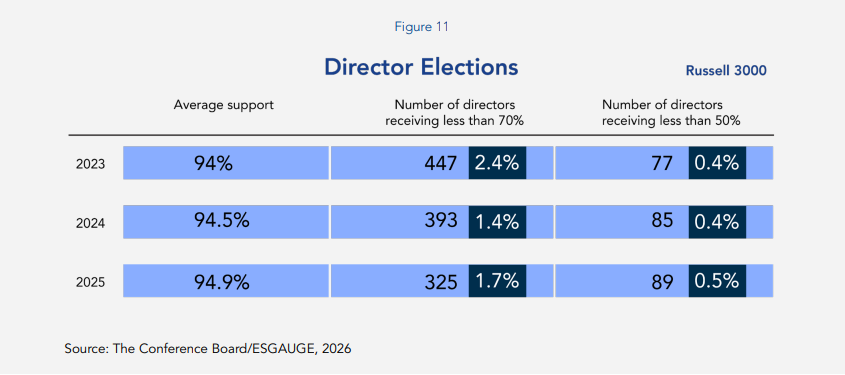

Director elections

Support for director elections remained high in 2025, though targeted dissent persisted where investors identified company-specific governance concerns. As in prior years, votes against directors appear to be driven less by broad dissatisfaction and more by company-specific issues such as poor attendance, insufficient responsiveness to prior shareholder proposals, sustained low say-on-pay support, overboarding, problematic committee decisions, or perceived oversight failures related to strategy, risk, or compliance. These patterns reinforce the importance of proactive engagement and clear disclosure around board oversight and decision-making.

Recent proxy voting policy updates suggest that while average support for directors is likely to remain high in 2026, opposition votes may become more targeted. Major institutional investors and proxy advisors have softened prescriptive language in their guidelines and emphasized case-by-case evaluation, but they continue to signal willingness to withhold support where boards fall short on governance, pay alignment, risk oversight, or shareholder responsiveness. Under these refined approaches, directors overseeing egregious or persistent issues—particularly nomination and governance and compensation committee chairs—may face increased scrutiny, even as mechanical or purely numerical triggers for opposition play a diminished role.

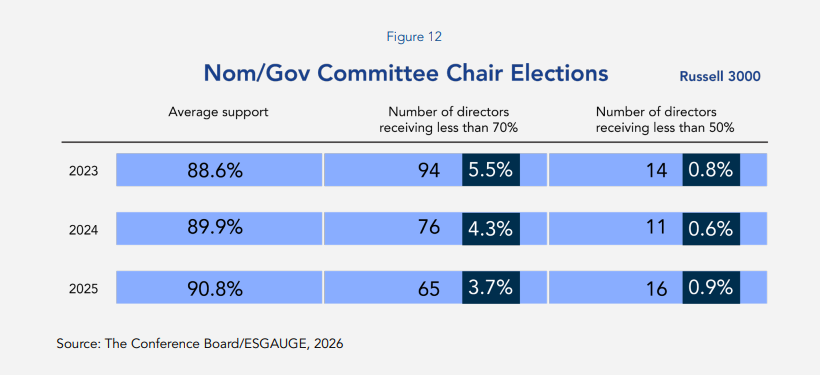

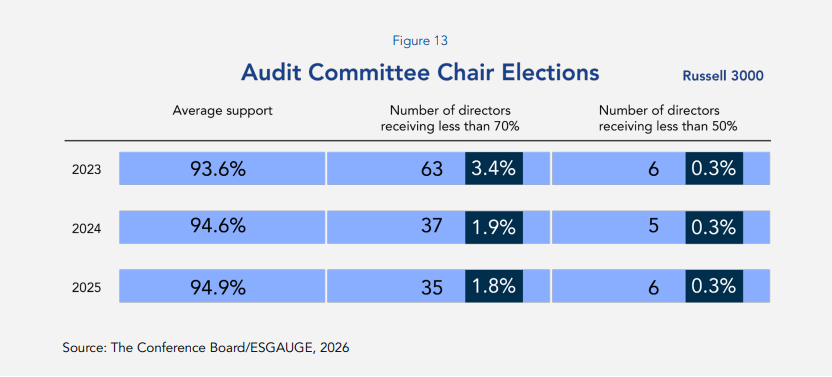

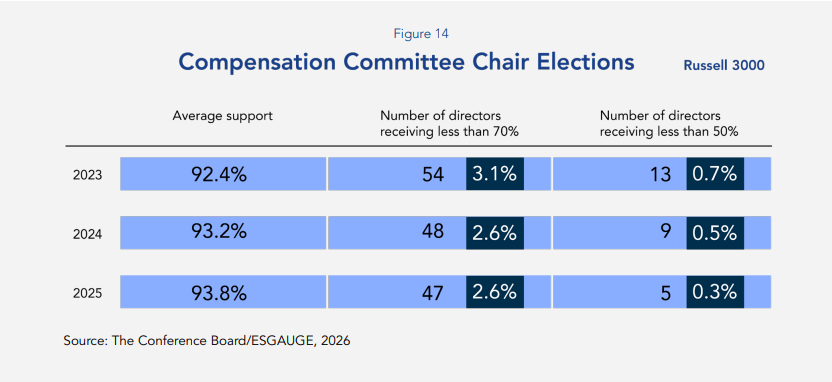

Committee chairs

Voting outcomes for committee chairs continue to highlight meaningful differences in how investors assess accountability across board functions. As these patterns persist, clear disclosure around board oversight, refreshment, and engagement outcomes is likely to remain critical in 2026.

Nomination and governance committee chairs attracted comparatively lower support than other committee leaders, although average support increased modestly in 2025. The share of nom/gov chairs receiving less than 70% shareholder support declined year over year, indicating that fewer chairs were broadly targeted. However, among those that did face opposition, a higher number and proportion received less than 50% support, suggesting that while overall pressure may have narrowed, dissent in certain cases was more concentrated and pronounced. Scrutiny of board composition, refreshment practices, and governance oversight therefore remains elevated, even if opposition is less widespread.

By contrast, support for audit committee chairs remained strong and stable, with average support levels near 95% in both 2024 and 2025. Only a very small share of audit committee chairs received less than 70% or less than 50% shareholder support, reflecting sustained investor confidence in audit oversight amid continued focus on financial reporting quality, risk management, and internal controls.

Support for compensation committee chairs also remained high, with average support increasing slightly in 2025. The share of compensation committee chairs receiving less than 70% support was unchanged year over year, while the proportion receiving less than 50% support declined slightly. Nevertheless, compensation committee chairs remain particularly sensitive to broader concerns around executive pay outcomes, incentive design, and responsiveness to shareholder feedback, reinforcing their role as a focal point for accountability when pay practices draw scrutiny.

Executive compensation

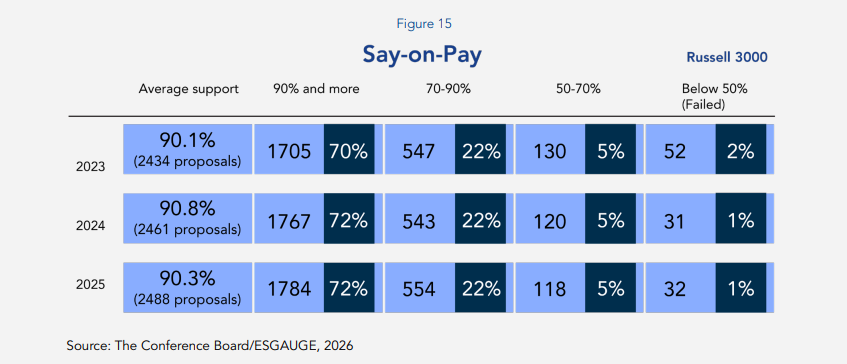

Say-on-pay outcomes in the Russell 3000 remained broadly stable in 2025, reflecting continued shareholder support for executive compensation programs at most companies. Average support declined slightly year over year, but the distribution of vote outcomes was largely unchanged. Roughly three-quarters of say-on-pay proposals received support of 90% or higher, while approximately one-fifth fell into the 70%–90% range.

Notably, failed say-on-pay votes remained rare, accounting for only about 1% of proposals in both 2024 and 2025. This stability suggests that while investors continue to scrutinize pay-for-performance alignment, most companies are meeting baseline expectations around incentive structure, disclosure, and responsiveness.

As in prior years, weaker say-on-pay outcomes were closely associated with increased scrutiny of compensation committee chairs, underscoring the link between pay decisions and board accountability. With several years of pay-versus-performance disclosure now available, investors are increasingly able to assess trends over time rather than isolated outcomes. Heading into the 2026 proxy season, companies with borderline results should expect shareholders to ask for clear explanations of pay outcomes, question the use of discretion, and assess how effectively their concerns are addressed.

| Executive security and perquisites

As documented in CEO and Executive Compensation Practices in the Russell 3000 and S&P 500: 2025 Edition, executive perquisites remain a small share of reported total compensation but attract outsized scrutiny, particularly around personal and home security. The prevalence of security-related benefits has increased materially in recent years, reflecting heightened executive safety concerns and evolving risk environments rather than discretionary pay expansion. For most companies, CEO personal and home security remains a limited, precautionary expense, with median spending of approximately $75,000–$76,000 across the Russell 3000 and S&P 500. By contrast, a small but growing group of companies incur substantially higher costs: among the top decile of spenders, median security expenses exceed $1.1 million, consistent with comprehensive protection models rather than discretionary perquisites. Sector patterns reinforce that elevated spending is driven by risk exposure and public visibility, particularly in communication services and information technology. Recent events have further shaped how boards, investors, and the public view executive security. High-profile incidents involving threats to senior executives have heightened awareness of personal safety risks, while company-specific decisions—such as removing caps on corporate aircraft use where tied explicitly to security considerations—underscore the evolving intersection between executive protection, travel logistics, and continuity planning. These developments have reinforced the importance of framing security-related perquisites as part of a broader risk-management strategy rather than as convenience-driven benefits. Investor attitudes toward executive security in the 2025–2026 proxy seasons are best described as conditionally supportive. Investors have shown greater acceptance where companies clearly link security and related perquisites, including private aircraft use, to identifiable risks, continuity planning, and board-level oversight. Skepticism tends to arise when disclosure is vague, when security is framed as a convenience rather than a risk-mitigation measure, or when elevated perquisites coexist with weak pay-for-performance alignment. As scrutiny of executive perquisites intensifies, companies that treat security as a governance and risk-management issue—supported by clear, proportionate, and well-documented disclosure—are better positioned to mitigate investor concern. |

2026 US Proxy Voting Guidelines and Policies

The 2026 proxy season marks a decisive shift in how proxy advisors and large institutional investors articulate—and apply—their voting policies. Across the market, prescriptive guidelines are giving way to discretionary, case-by-case decision-making, reducing predictability for issuers while increasing the importance of company-specific disclosure, engagement history, and board rationale.

Among asset managers, this shift is most evident in the simplification and recalibration of stewardship frameworks. Vanguard substantially shortened its proxy voting guidelines for 2026; removed explicit descriptions of how its teams may vote on director elections, executive compensation, and shareholder proposals; and eliminated references linking voting outcomes to board composition or ESG-specific considerations. BlackRock has similarly emphasized fundamentals-based assessments of economic materiality, noting that many environmental and social proposals are overly prescriptive or insufficiently tied to long-term shareholder value. JPMorgan has gone further by cutting ties with proxy advisory firm research and recommendations, shifting instead to an internal, AI-enabled platform to support portfolio-specific voting decisions. At the same time, major asset managers have reorganized stewardship functions across investment vehicles, meaning issuers increasingly engage with multiple teams within a single institution, each with distinct mandates and priorities.

Proxy advisors are moving in a similar direction. ISS and Glass Lewis continue to focus on board accountability and pay-for-performance alignment but are relying more heavily on contextual analysis rather than formulaic scoring. For 2026, Glass Lewis has expanded its focus on board oversight of emerging risks such as AI,1 while ISS has refined its scrutiny of executive perquisites and discretionary pay decisions.

This shift is occurring against a backdrop of heightened political and regulatory scrutiny of the proxy advisory industry. In December 2025, the White House issued an executive order calling for increased oversight of proxy advisors, citing concerns around foreign ownership, conflicts of interest, and the potential for politically motivated voting influence. While the order does not directly alter proxy voting rules for the 2026 season, it adds to existing pressures on proxy advisors to demonstrate analytical independence, transparency, and rigor—further reinforcing the move away from standardized recommendations toward more contextual, issuer-specific assessments.

Taken together, these developments reinforce a proxy voting environment that places greater weight on issuer judgment and explanation. As proxy advisors and asset managers rely more heavily on contextual analysis—and face increased scrutiny of their own methodologies—issuers should expect voting outcomes to hinge less on compliance with prescriptive guidelines and more on the clarity of board oversight, decision-making processes, and supporting disclosure. In this environment, the proxy statement plays an increasingly central role in conveying how boards assess risk, exercise discretion, and respond to shareholder concerns.

| Stewardship in a more constrained engagement environment

As regulatory developments—including tighter expectations around Schedule 13G2 eligibility and disclosure—reshape how and when institutional investors engage with issuers, proxy voting and proxy disclosure are playing a more central role in stewardship. With some investors exercising greater caution around engagement, greater weight is placed on issuer-provided context, board rationale, and demonstrated responsiveness in public disclosures, increasing both the stakes and the value of clear, decision-oriented proxy communication. |