Print

PrintJason Frankl and Brian G. Kushner are Senior Managing Directors at FTI Consulting. This post is based on their FTI Consulting memorandum. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism by Lucian A. Bebchuk, Alon Brav, and Wei Jiang (discussed on the Forum here); Dancing with Activists by Lucian A. Bebchuk, Alon Brav, Wei Jiang, and Thomas Keusch (discussed on the Forum here); and Who Bleeds When the Wolves Bite? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System by Leo E. Strine, Jr. (discussed on the Forum here).

Introduction and Market Update

With proxy season underway, FTI Consulting’s Activism and M&A Solutions team welcomes readers to our quarterly Activism Vulnerability Report, which highlights the findings of our Activism Vulnerability Screener for 4Q22 and discusses other notable themes and trends in the world of shareholder activism.

The U.S. stock market in 2022 experienced increased volatility relative to 2021. Persistently high inflation, coupled with the fastest Fed tightening cycle seen since 1988, contributed to making 2022 the worst performing year for the S&P 500 Index since 2008, thrashing growth and technology stocks in particular. [1] Geopolitical concerns added to poor investor sentiment approaching the new year.[2] However, as 2023 began, stocks and bonds each rallied in January, partly due to reported fourth quarter growth in real GDP for the United States, even while various economic factors were flashing warnings signs.[3] However, these gains quickly eroded in February, as economic data on the labor market and consumer spending remained stronger than expected, prompting investors to reassess their expectations for inflation and further monetary policy. [4] Silicon Valley Bank’s (“SVB”) recent collapse, along with troubles at several other prominent banks, has called into question the frequency of further interest rate increases, amid concerns of contagion spreading through the wider global banking industry. [5] Though the Fed subsequently announced a quarter-percentage-point interest-rate increase following the turmoil, officials signaled that rate hikes are nearing an end in their post-meeting policy statement.[6]

In 2022, perhaps due to higher levels of market volatility and sinking investor sentiment, shareholder activists increased their activity, with a heavier focus on the Telecom, Media & Technology (“TMT”), Healthcare & Life Sciences and Retail & Consumer Products sectors. Even in Canada, the activism winter seemed to thaw a bit, as shareholder demands north of the U.S. border almost doubled year-over-year. The increased activity may be a sign of changing tides, as investors start picking through the wreckage for undervalued investments.

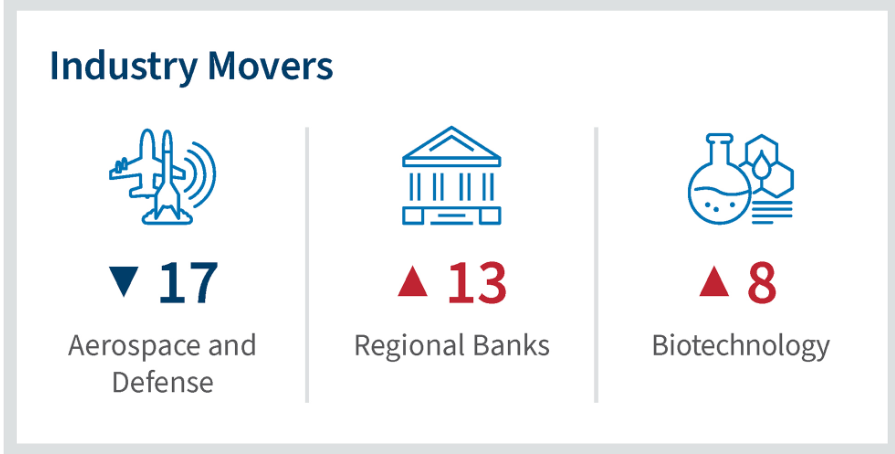

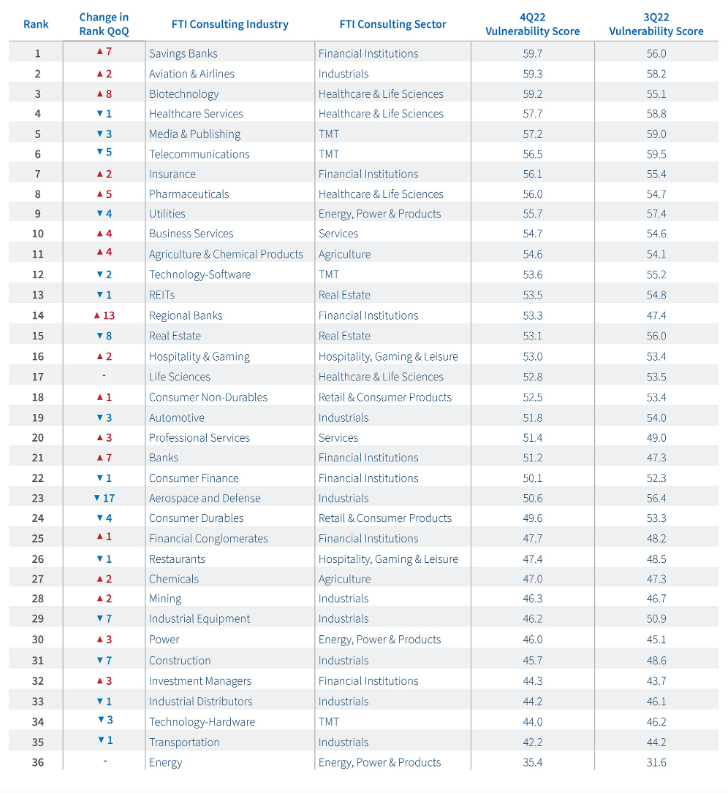

Our Activism Vulnerability Screener for 4Q22 found the Aerospace and Defense industry making the largest quarterly move, decreasing 17 spots in vulnerability versus other industries. The industries with the largest increase in vulnerability were Regional Banks and Biotechnology, jumping 13 and eight positions, respectively, in the rankings, aided by challenging shareholder returns.

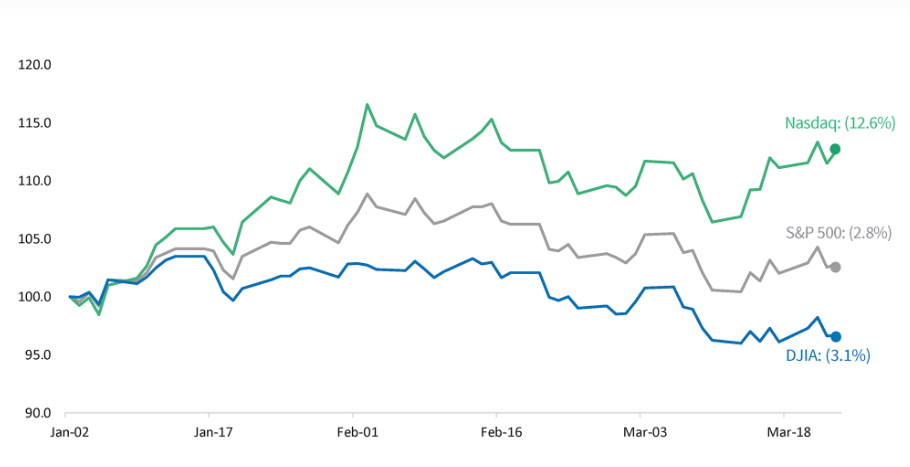

As of March 23, 2023, the Nasdaq Composite was higher by 12.6% year-to-date, the S&P 500 increased by 2.8% and the Dow Jones Industrial Average (DJIA) was down by 3.1% (see graphic below). Over the same period, the CBOE Volatility Index (VIX) was up over 4.9%. [7] Short-term U.S. Government interest rates are currently higher than long-term rates, leading to an inverted yield curve, which many analysts believe to be a harbinger of an upcoming recession. [8]

Year-to-Date Performance (2023) [9]

Shareholder Activism Update

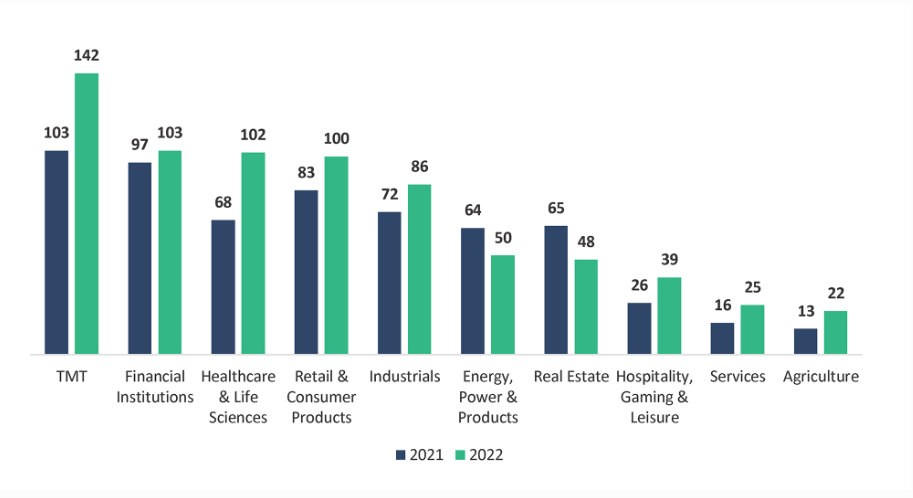

U.S. and Canadian shareholder activism recovered in 2022 from the lows witnessed in 2021. Activist demands were up 18.1% compared to the prior year. [10] The TMT sector was the most targeted sector in 2022, followed by the Financial Institutions and Healthcare & Life Sciences sectors. The heightened activist activity observed in the TMT sector may have been partially driven by technology company valuations, which compressed during 2022 (e.g., Nasdaq-100 Technology Sector Index fell 39.5%) [11] Alphabet Inc., Meta Platforms, Inc. and Pinterest, Inc. were just some of the targets activists identified last year, and interest in the sector does not appear to be waning in 2023.

So far in 2023, we have seen campaigns launched against Snap, Inc., and multiple activists targeting Salesforce, Inc. [12] To date at least five activists – Elliott Management, Inclusive Capital, Starboard Value, Third Point Management and ValueAct Capital (“ValueAct”) – have separately circled the tech giant, criticizing the company for purchasing Slack Technologies, Inc. and Tableau Software, Inc. at high multiples, slowing revenue growth and delivery of margins below its peer group, resulting in share price underperformance. In late January 2023, the company settled with ValueAct Capital by adding that firm’s CEO, Mason Morfit, to its Board. [13]

Activist Targets by Sector – 2022 Year-Over-Year Change [14]

Though more board seats were gained through settlement in 2022 compared to the prior year (140 in 2022 vs. 112 in 2021), seats won via settlement as a percentage of total seats won actually decreased slightly from 2021 (81.9% in 2022 vs. 84.8% in 2021). [15] Looking at 4Q22 in isolation, however, paints a different story. Settlement seats represented 91.2% of all seats gained during the quarter (31 of 34 seats total), compared to just 68.4% in 4Q21 (26 of 38 seats total). [16] Several analysts have hypothesized that the new universal proxy rules (effective September 1, 2022) may be increasing a targeted company’s willingness to settle with activists in order to shield their most vulnerable directors, but one quarter does not make a trend. [17]

Perhaps this year’s highest profile activist situation ended in a settlement, despite the activist receiving no board representation. On January 11, 2023, Trian Partners (“Trian”) announced that it had nominated its CEO, Nelson Peltz, to the Board of The Walt Disney Company (“Disney”). [18] Trian criticized Disney for corporate governance, lack of cost discipline within its streaming segment and overpaying for acquisitions.[19] When Disney reported results on February 8, 2023, it announced an organizational restructuring; cost savings, mainly within streaming; a Board committee to lead a search for the next CEO; and a plan to restore the dividend. [20] Within hours, and after Disney’s stock popped considerably, Nelson Peltz surprisingly announced on CNBC that Trian had ended its campaign. [21] “Now Disney plans to do everything we wanted them to do,” Peltz explained. [22] The stock has since retreated to pre-announcement levels. We will watch with interest whether Trian, or another activist, circles back around on Disney’s execution of its transformation plan.

In 2022, we also witnessed a familiar trend of increased activist attention on large-cap (>$10 billion market-cap) companies. Excluding companies with less than $50 million in market capitalization, in 2022, large-cap corporations represented 30.8% of all public demands made against U.S.- and Canada-based corporations compared to 26.4% of public demands in 2021 and 20.1% in 2020. [23] The increased focus on large- and mega-cap activism in 2022 may be at least partly due to the greater stability of free cash flows offered by larger companies during the current environment of increased stock market volatility and resurgent inflation.

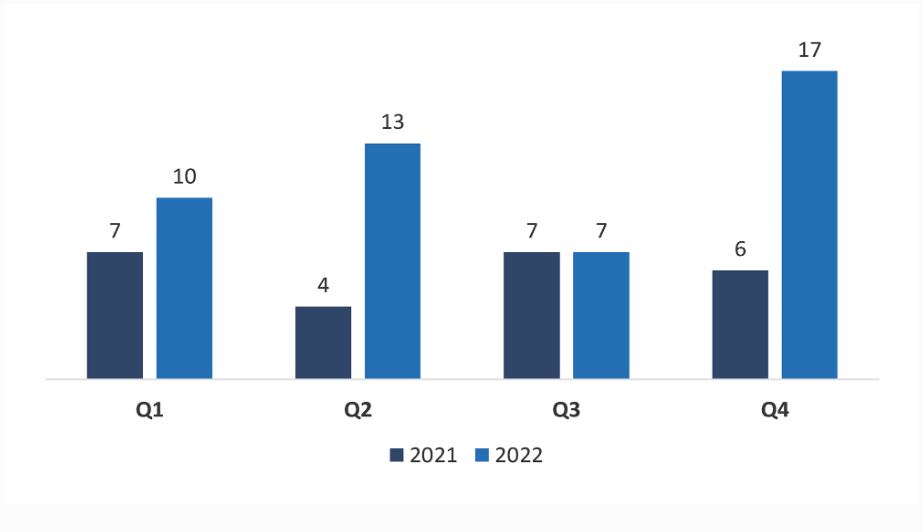

Interestingly, we observed an impressive 95.8% uptick in the number of public demands made against Canadian companies in 2022 compared to 2021 (47 demands in 2022 vs. 24 demands in 2021). [24] Increased shareholder activism in Canada was perhaps emboldened by newly passed federal laws that give activist investors more power to choose directors. [25] Previously, shareholders could only vote “For” a candidate or “Withhold” their vote, and directors were not required to resign if they did not secure a majority of “For” votes. Since this amendment to the Canada Business Corporation Act was passed in August 2022, activists can now target specific directors by voting “Against” each director nominated to a company’s board. [26] Theoretically, activists in Canada, which was already considered to be a favorable regulatory environment for activism, could now have even greater leverage. So perhaps it is not surprising that public demands in 4Q22 increased to 17, compared to six from the same quarter in 2021, representing a 183.3% increase. [27] We will be watching closely to see how the Canadian proxy season plays out in the coming months to determine the impact of this new regulation.

Public Activist Demands in Canada – 2022 Year-Over-Year Change [28]

The Relationship Between Activist Campaign Success and Proxy Advisors

Last summer, FTI Consulting’s Activism and M&A Solutions team published research on proxy contests where activists sought board seats at U.S.-listed companies with market capitalizations of at least $100 million, and where ISS and Glass Lewis published voting recommendations. That study covered 80 contests from January 1, 2021 through June 30, 2022. We found that activists almost always won at least one seat if both ISS and Glass recommended for them. In only two situations did an activist obtain a board seat while winning the endorsement of just one proxy advisor. Not a single activist won a board seat without securing the endorsement of at least one of the two primary proxy advisors. [29]

As an update to this analysis, we examined proxy contests under the same criteria listed above. From July 1, 2022 to March 17, 2023, 11 contests have come to a close. [30] We found two instances in which dissidents were successful in their pursuit for board representation, without winning recommendations from both ISS and Glass Lewis.

The first of these two instances took place last December, when Land & Buildings Investment Management (“Land & Buildings”) sought two board seats at Apartment Investment & Management Company (“Aimco”). Land & Buildings gained a recommendation from ISS but not Glass Lewis, but it still won one board seat through the shareholder vote. [31]

Something more interesting occurred when Sarissa Capital Management (“Sarissa”) ran a campaign against U.S.-listed Amarin Corporation Plc (“Amarin”). Both ISS and Glass Lewis recommended that shareholders vote with the company, against all of Sarissa’s proposals. However, Sarissa’s proposals won easily, resulting in the election of seven new directors, all by wide margins. [32]

Our sample size of 11 proxy contests is undoubtedly limited, but this will be a trend that our team will continue to track as we analyze incoming results throughout proxy season.

Observations & Insights

“With 239 companies publicly subjected to activist demands year to date (2023), the number of shareholder activism campaigns is on pace to surpass the totals from each of the last three years. This surge in activism is largely attributable to the current dislocation in equity valuations, particularly in the Technology and Life Sciences industries, as well as the SEC’s adoption of the universal proxy regime in the United States that took effect September 1, 2022.

While there has been an increase in activism, thus far there has not been the uptick in proxy contests in the United States that many predicted as a result of universal proxy. After six-plus months under the universal proxy regime, we have only seen one proxy contest go to a vote.

One initial trend we are seeing as a result of universal proxy in the United States and more generally on a global scale that we think will continue into the 2023 proxy season is that there is an increasing number of campaigns that are being resolved by settlement or otherwise. In this regard, year to date over 46% of activism campaigns have been at least partially satisfied. To put this in context, this percentage has been between 21% and 29% from 2017 to 2022.

Even with the early resolution of campaigns, there are lessons to be learned from the only universal proxy contest in the United States to go to a vote under the new universal proxy rules. In this contest, Land & Buildings nominated two directors for election to the Board of Aimco.

The three main takeaways from the Aimco/Land & Buildings proxy contest that should be considered as we head into the heart of proxy season are the following. First, the activist obtained a Board seat with one of Land & Buildings’ nominees being elected to the Board. It is notable that the Aimco nominee that was not elected to the Board is 73 years old and served on the Board for 18 years. Second, ISS issued a split-ticket recommendation in which it recommended for one of the activist’s nominees and one of the company’s nominees. The two candidates recommended in favor of ISS won by a wide margin. Lastly, the cost of the proxy contest for the activist was not significantly reduced, as Land & Buildings indicated in its proxy statement that it expected to spend $1,000,000 on the proxy contest. In this regard, we believe that economic activists will continue to spend significant amounts of money in an effort to prevail in proxy contests that go to a shareholder vote.”

— Sean Donahue, Capital Markets and Shareholder Activism & Takeover Defense Practices, Chair of Public Company Advisory Practice, Goodwin Procter LLP

Screener Results

Tracking with what we observed in 3Q22, only two industries moved 10 or more spots in vulnerability during 4Q22: Regional Banks and Aerospace and Defense. The former jumped 13 spots to enter the top 15, while Savings Banks jumped seven spots to rank as the industry most vulnerable to activism. The financial strength of many banks decreased over the year, as rising interest rates have substantially reduced the value of U.S. Treasuries and other fixed income securities they own. According to the FDIC, U.S. banks were sitting on $620 billion in unrealized losses at the end of 2022. [33] The implication of these losses suddenly came to light in early March, when such losses led SVB to attempt to raise capital; instead, that announcement inadvertently led to a run on the bank that resulted in its takeover by regulators. Several other banks, both in the U.S and Europe, saw their share prices fall dramatically in a short time, as investors began to perceive them as riskier. [34]

Focusing more specifically on shareholder activism, one notable campaign in the Regional Banks industry began in early 2022, when activist Driver Management and a shareholder group led by George Norcross called for a new CEO and board refreshment at Republic First Bancorp. The company’s Board stripped CEO Vernon Hill of his Chairman title after one of his Board allies passed away, and Hill subsequently stepped down as CEO in July 2022. Though the company settled with Driver Management by adding one director in October 2022, Norcross has continued his proxy campaign against the company, offering to invest $100 million in exchange for three board seats and the CEO position. The 2022 annual meeting has been delayed until May 31, 2023. [35]

By contrast, the Aerospace and Defense industry reversed course, dropping 17 spots after sitting in the top 10 most vulnerable industries the previous three quarters. This industry gained momentum in 2022 from increases in new aircraft and military orders, partly due to the Russia-Ukraine war, coupled with rising demand for air travel.[36] Though the risk of supply chain disruptions and rising jet fuel prices can impact market volatility, aircraft manufacturers have been investing in fuel-efficient aircraft and engine designs. [37] In particular, we observed a drop in balance sheet and operating performance vulnerability in the Aerospace and Defense industry during the quarter.

What This Means

The continued volatility in the equity markets has not appeared to dampen activist interest and activity in 2023, though much uncertainty remains following SVB’s collapse in March. [38] With so much unpredictability in the financial markets, we may see more activists tailoring their investment demands to reflect the current macroeconomic environment.

As the SVB situation highlighted, the lingering implications of high inflation are already starting to play out in the market, including concerns related to rising interest rates and economic instability. The threat of contagion and a broader economic crisis is still looming, though large central banks and regulators are attempting to quell the shockwaves; for example, UBS Group AG purchased rival Credit Suisse Group AG for $3.2 billion and assumed $5.4 billion in losses shortly after SVB’s collapse. [39]

What remains to be seen is how businesses and investors plan to navigate these murky regulatory and macro-related waters in the year ahead. Activists will have to evaluate the current state of the global economy to hypothesize how industry dynamics and investors will ultimately react, searching for calculated opportunities to allocate capital and initiate pertinent and persuasive shareholder engagement.

FTI Consulting’s Activism Vulnerability Screener Methodology

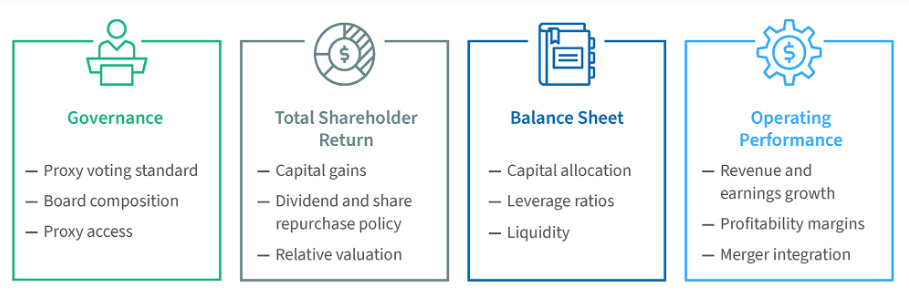

- The Activism Vulnerability Screener is a proprietary model that measures the vulnerability of public companies in the U.S. and Canada to shareholder activism by collecting criteria relevant to activist investors and benchmarking to sector peers.

- The criteria are sorted into four categories, scored on a scale of 0-25, (1) Governance, (2) Total Shareholder Return, (3) Balance Sheet and (4) Operating Performance, which are aggregated to a final Composite Vulnerability Score, scored on a scale of 0-100.

By classifying the relevant attributes and performance metrics into broader categories, experts at FTI Consulting can quickly uncover where vulnerabilities are found, allowing for a more targeted response. FTI Consulting’s Activism and M&A Solutions team determined these criteria through research of historical activist campaigns in order to locate themes and characteristics frequently targeted by activist investors. - The following is a selection of themes that are included for each category:

- The Activism and M&A Solutions team closely follows the latest trends and developments in the world of shareholder activism. Due to the constantly evolving activism landscape, FTI Consulting’s Activism and M&A Solutions team consistently reviews the criteria and their respective weightings to ensure the utmost accuracy and efficacy of Activism Screener.

Endnotes

1Jenna Ross, The Pace of US Interest Rate Hikes is Faster Than At Any Time in Recent History. Is This Creating a Risk of Recession?, World Economic Forum (October 12, 2022), https://www.weforum.org/agenda/2022/10/comparing-the-speed-of-u-s-interest-rate-hikes-1988-2022/#:~:text=The%202022%20rate%20hike%20cycle,by%20almost%20four%20percentage%20points.(go back)

2Jesse Pound and Samantha Subin, Stocks fall to end Wall Street’s worst year since 2008, S&P 500 finishes 2022 down nearly 20%, CNBC (updated December 30, 2022), https://www.cnbc.com/2022/12/29/stock-market-futures-open-to-close-news.html.(go back)

3Dan Frost, January 2023 Market Recap, Pittenger & Anderson, Inc. (February 8, 2023), https://pittand.com/2023/02/08/january-2023-market-recap/.(go back)

4Caitlin McCabe & Alexander Osipovich, Stocks Close February With Declines, The Wall Street Journal (February 28, 2023), https://www.wsj.com/articles/global-stocks-markets-dow-update-02-28-2023-b6a5a6a8.(go back)

5Richard Partington, Silicon Valley Bank collapse ‘could force central banks to stop interest rate rises,’ The Guardian (March 13, 2023), https://www.theguardian.com/business/2023/mar/13/silicon-valley-bank-collapse-central-banks-interest-rate-rises.(go back)

6Nick Timiraos, Fed Raises Rates but Nods to Greater Uncertainty After Banking Stress, The Wall Street Journal (March 22, 2023), https://www.wsj.com/articles/fed-raises-rates-but-nods-to-greater-uncertainty-after-banking-stress-6ae9316f.(go back)

7FTI Consulting, Inc. analysis. Data provided by FactSet as of March 23, 2023.(go back)

8The Yield Curve, Current Market Valuation (updated March 17, 2023), https://www.currentmarketvaluation.com/models/yield-curve.php#:~:text=The%20US%20Treasury%20Yield%20Curve,higher%20than)%20long%20term%20rates.(go back)

9FTI Consulting, Inc. analysis. Data provided by FactSet as of March 23, 2023.(go back)

10FTI Consulting, Inc. analysis of activist campaigns. Data provided by Insightia as of December 31, 2022.(go back)

11FTI Consulting, Inc. analysis. Data provided by FactSet as of December 31, 2022.(go back)

12FTI Consulting, Inc. analysis of activist campaigns. Data provided by Insightia as of December 31, 2022.(go back)

13Jordan Novet and Scott Wapner, Third Point becomes latest activist investor to take stake in Salesforce, CNBC (February 9, 2023), https://www.cnbc.com/2023/02/09/third-point-is-latest-activist-investor-to-take-stake-in-salesforce.html.(go back)

14FTI Consulting, Inc. analysis of activist campaigns. Data provided by Insightia as of December 31, 2022.(go back)

15Shareholder Activism in 2022, Insightia, (last visited March 23, 2023), https://docs.insightia.com/issues/2023_01_25_Insightia_2022FYStats.pdf.(go back)

16FTI Consulting, Inc. analysis of activist campaigns. Data provided by Insightia as of December 31, 2022.(go back)

17The Shareholder Activism Annual Review, Insightia, (last visited March 23, 2023), https://docs.insightia.com/issues/2023_02_16_Insightia_SAAR2023.pdf.(go back)

18Trian Nominates Nelson Peltz for Election to Disney Board, Business Wire (January 11, 2023), https://www.businesswire.com/news/home/20230111005991/en/Trian-Nominates-Nelson-Peltz-for-Election-to-Disney-Board.(go back)

19Securities and Exchange Commission, The Walt Disney Company – Schedule 14A (January 12, 2023), https://www.sec.gov/Archives/edgar/data/1744489/000090266423000178/p23-0113dfan14a.htm.(go back)

20Securities and Exchange Commission, The Walt Disney Company – Schedule 14A (February 9, 2023), https://www.sec.gov/Archives/edgar/data/1744489/000095015723000083/defa14a.htm.(go back)

21Svea Herbst-Bayliss and Dawn Chmielewski, Activist Peltz makes nice with Disney, ends board challenge, Reuters (February 9, 2023), https://www.reuters.com/business/media-telecom/peltz-trian-ends-disney-board-challenge-after-ceo-iger-lays-out-key-changes-2023-02-09/.(go back)

22Lillian Rizzo, Activist investor Nelson Peltz declares Disney proxy fight is over after Iger unveils restructuring, CNBC (February 9, 2023), https://www.cnbc.com/2023/02/09/activist-investor-nelson-peltz-declares-disney-proxy-fight-is-over-after-iger-unveils-restructuring.html.(go back)

23FTI Consulting, Inc. analysis of activist campaigns. Data provided by Insightia as of December 31, 2022.(go back)

24Ibid.(go back)

25Maiya Keidan, Rise in Canadian shareholder activism faces test next month with new rules in place, Reuters (February 12, 2023), https://www.reuters.com/markets/rise-canadian-shareholder-activism-faces-test-next-month-with-new-rules-place-2023-02-12/.(go back)

26Ibid.(go back)

27FTI Consulting, Inc. analysis of activist campaigns. Data provided by Insightia as of December 31, 2022.(go back)

28Ibid.(go back)

29Kurt Moeller, Activists’ Lack of Recent Success: Causes and Implications, FTI Consulting, Inc. (August 25, 2022), https://www.fticonsulting.com/insights/articles/activists-lack-recent-success-causes-implications.(go back)

30FTI Consulting, Inc. analysis of activist campaigns. Data provided by Insightia as of March 17, 2023.(go back)

31Ibid.(go back)

32Ibid.(go back)

33Nicole Goodkind, US banks sitting on unrealized losses of $620 billion, CNN Business (March 12, 2023), https://www.cnn.com/2023/03/12/investing/stocks-week-ahead/index.html.(go back)

34FTI Consulting, Inc. analysis. Data provided by FactSet as of March 23, 2023.(go back)

35Lauren Seay and David Hayes, Republic First tackles strategic review, activist challenge under new CEO, S&P Global Market Intelligence (February 24, 2023), https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/republic-first-tackles-strategic-review-activist-challenge-under-new-ceo-74345109.(go back)

36John Coykendall, Paul Wellener, and Kate Hardin, 2023 aerospace and defense industry outlook, Deloitte (last visited March 23, 2023), https://www2.deloitte.com/us/en/pages/manufacturing/articles/aerospace-and-defense-industry-outlook.html.(go back)

37Ibid.(go back)

38Jeff Cox, Fed Chair Powell says interest rates are ‘likely to be higher’ than previously anticipated, CNBC (March 7, 2023), https://www.cnbc.com/2023/03/07/fed-chair-powell-says-interest-rates-are-likely-to-be-higher-than-previously-anticipated.html.(go back)

39Stefania Spezzati, Oliver Hirt and John O’Donnell, Central banks try to calm markets after UBS deal to buy Credit Suisse, Reuters (March 19, 2023), https://www.reuters.com/business/crunch-time-credit-suisse-talks-ubs-seeks-swiss-assurances-2023-03-19/.(go back)