Print

PrintGabriel Rauterberg is a Professor of Law and Jeffery Y. Zhang is an Assistant Professor of Law at the University of Michigan Law School. This post is based on their article forthcoming in the Stanford Law Review.

Shadow banking may be the single greatest challenge facing financial regulation. Financial institutions that function like banks, but outside the scope of banking regulation—aptly termed, “shadow banks”—were at the heart of the 2007-2008 Global Financial Crisis and most episodes of serious financial stress since then. The direct costs of shadow banking can be significant, and when it precipitates broader economic crisis, shadow banking can cause long-lived harm to economic growth and social welfare. For the most part, leading economists and legal scholars have converged on a shared approach: the solution to shadow banking is to apply banking regulation to it, in part or in whole, to encompass shadow banks “in the banking regulatory perimeter.” Yet whatever the significant merits of this view, regulators and politicians have made little headway in adopting the more dramatic reform proposals.

Our forthcoming article, “Shadow Banking and Securities Law,” explores the uneasy case for a different approach to regulating shadow banking—securities law. Our first contribution is analytical: We show how securities regulators already enjoy enormous jurisdictional authority over shadow banking. While shadow banking is often said to be unregulated, in reality, it does not completely fall through the regulatory cracks. Instead, under existing law, all major forms of domestic shadow banking lie within the jurisdiction of the Securities and Exchange Commission (“SEC”).

This pattern—where financial activities designed to evade banking law end up qualifying as securities—is not an accident. It has deep roots in the architecture of U.S. financial regulation and in a fundamental contrast between banking and securities regulation. Famously, banking law adopts a narrow and formalistic definition of banking. This has been called banking law’s “original sin.” Securities law does no such thing. Instead, it defines its foundational categories in extraordinarily capacious, open-ended, and functional terms. “Security” includes not only a laundry list of familiar financial instruments, like stocks and bonds, but also include “investment contracts” and any “note.” Even more importantly to our analysis, the securities law define the category of “investment company”—colloquially, funds—to include not only any entity whose primary business is investing in securities, but also any business that invests in securities and whose assets consist in significant part (40 percent or more) of securities.

Just as one illustration, consider the role of one central securities category—“investment company”—in shadow banking. The three largest domestic shadow banking markets are money market mutual funds, repo, and commercial paper. In each of those markets, investment funds play a central role, though the role varies, from issuer in money funds to dealer in repo to purchaser in commercial paper. The empirical reality of these markets motivates our claim that securities regulators enjoy broad jurisdiction over shadow banking.

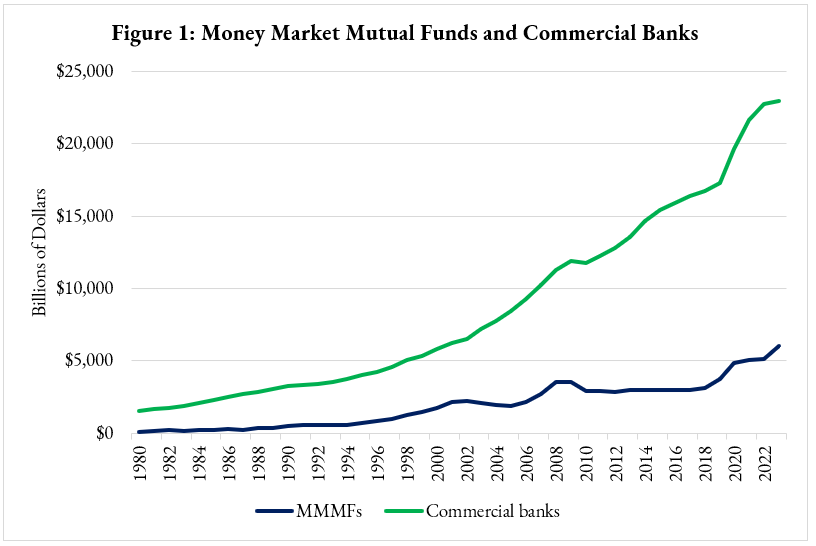

The largest domestic shadow banking markets involves money market mutual funds. Using the Federal Reserve’s flow of funds data, Figure 1 shows that since 1980, the total assets of money market mutual funds have grown substantially relative to the growth of the commercial banking sector. While total commercial bank assets still far exceed total money market fund assets, the growth of money market funds has been astonishing: since 1980, they have grown from near-nonexistence to more than a quarter of the assets of the banking system ($6.4 trillion and $23.4 trillion, respectively).

Next, Figure 2 presents the growth of hedge fund intermediation in the repo market, using data from the SEC’s Form PF. This repo market is nearly $3 trillion in size. So, just counting money market funds and repo transactions alone, the SEC has existing jurisdiction over $9 trillion worth of shadow banking activities. From the perspective of traditional bank regulators, this vast amount of private money was created in the shadows outside their clear ambit. From the perspective of the SEC, this private money was created in their backyard. Hedge funds are now widely thought to play a central role as market maker-like actors in the repo and Treasury markets. As Figure 2 shows, their borrowing and lending constitute an enormous part of the market.

Although estimating the precise size of the market is challenging, money market mutual funds remain the single largest investor type in the commercial paper market. These empirical facts highlight a major theme of our paper: how securities law encompasses shadow banking matters because each securities statute carries its own regulatory approach and each applicable statutory provision carries its own authorities and limits. Within securities law, a striking fact is the centrality of investment funds—and consequently investment fund regulation—to shadow banking.

Our quick illustration also gives us a sense of why the analytical details matter. The SEC enjoys jurisdiction over each of these markets through its authority over funds. But the nature of that authority differs dramatically. In commercial paper and money markets, the funds are registered funds over which the SEC possesses clear and sprawling authority. Indeed, but for explicit exemptions from otherwise applicable rules, money market funds could not exist. But in repo, private funds—specifically, hedge funds—play a central role. In an era of forum shopping and skeptical courts, this means that SEC rule making may face an uphill battle, even purely as a matter of legal authority.

The second principal contribution of this paper is to explore the uneasy case for the SEC taking a greater role in the regulation of shadow banking. There are strong arguments on both sides. On one hand, shadow banking can exact enormous social costs, and the SEC enjoys broad jurisdiction over almost all of the domestic shadow banking sectors, with varying weapons in its regulatory arsenal. In fact, securities regulators already address financial instability to a greater extent than is widely appreciated. Moreover, the idea that the SEC should take a greater role in addressing financial stability is not as alien as it might seem. A number of senior regulators, whether during their regulatory tenures or afterward, have floated the need for greater attention by the SEC to systemic risk and financial stability, and SEC practice has evolved away from deep-seated skepticism toward close attention to these concerns. In its recent annual reports, the Federal Stability Oversight Council has identified four priorities of late, three of which relate to shadow banking. On each of those fronts, the SEC—and not banking authorities—has taken significant policy action. Securities regulators, not banking regulators, have acted. Yet should they?

There are sharp limits to even the most optimistic views of the SEC’s ambit. The SEC is not meant to design the U.S. monetary architecture, and it lacks the immense balance sheet of the Federal Reserve and its resolving authorities to act as a lender of last resort in times of crisis. What could the SEC plausibly do? We explore two distinct routes for pursuing this general proposal. The first is an incremental complementarity approach that favors reforms within the traditional institutional expertise of the SEC, with modest ambition, and which would aim to complement any reforms adopted by banking regulators (e.g., repo haircuts). The second is a structural convergent approach that favors ambitious reforms requiring the SEC to develop new competencies and which would more closely parallel reforms advocated in banking regulation (e.g., capital requirements). We offer concrete institutional proposals for improving the efficacy of the SEC in these regards.

Finally, we carefully consider a number of weighty concerns and objections to the SEC action as well. We do not view even much-improved securities regulation of shadow banking as a complete substitute for a banking regime. As noted, securities regulators simply cannot play a role as a monetary authority, limiting their ability to adequately supervise shadow banks. In the absence of improved banking regulation, however, we conclude that securities regulators should cautiously pursue an agenda to further regulate shadow banking. The money problem is thus also a securities problem and is likely to remain that way until foundational changes are made either to banking law or securities law (or both).