Print

PrintSubodh Mishra is the Global Head of Communications at ISS STOXX. This post is based on an ISS-Corporate memorandum by Kevin Kim, Senior Associate for Compensation & Governance Advisory; and Toby Huang, Senior Associate for Data Analytics, at ISS-Corporate.

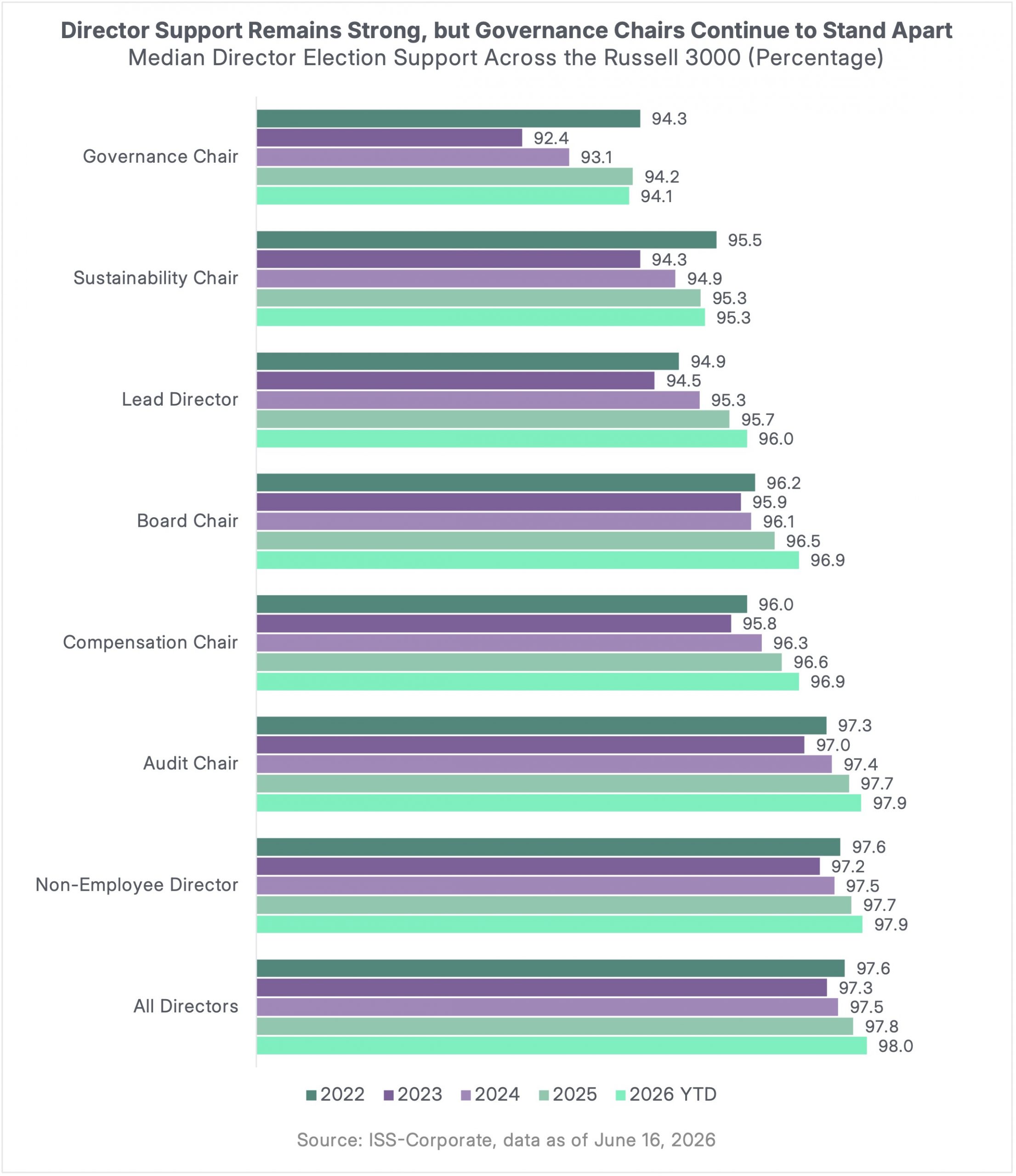

Director support remains uneven: governance chairs continue to see the lowest backing, while overall support has only recently rebounded from 2023 lows, highlighting persistent investor scrutiny of accountability and oversight.

In this iteration of our ongoing series covering the 2026 U.S. proxy season, we examine trends surrounding director support in the Russell 3000. Over the past five years, director support levels for all positions were at their lowest in 2023, though support has increased since then. However, median director support continues to vary depending on the director’s role. In particular, governance chairs continue to receive the lowest levels of support, which may be driven by ongoing shareholder concerns over issues for which they are generally held accountable. In this iteration of our ongoing series covering the 2026 U.S. proxy season, we examine trends surrounding director support in the Russell 3000. Over the past five years, director support levels for all positions were at their lowest in 2023, though support has increased since then. However, median director support continues to vary depending on the director’s role. In particular, governance chairs continue to receive the lowest levels of support, which may be driven by ongoing shareholder concerns over issues for which they are generally held accountable.

Director Support Trends Across Board Roles

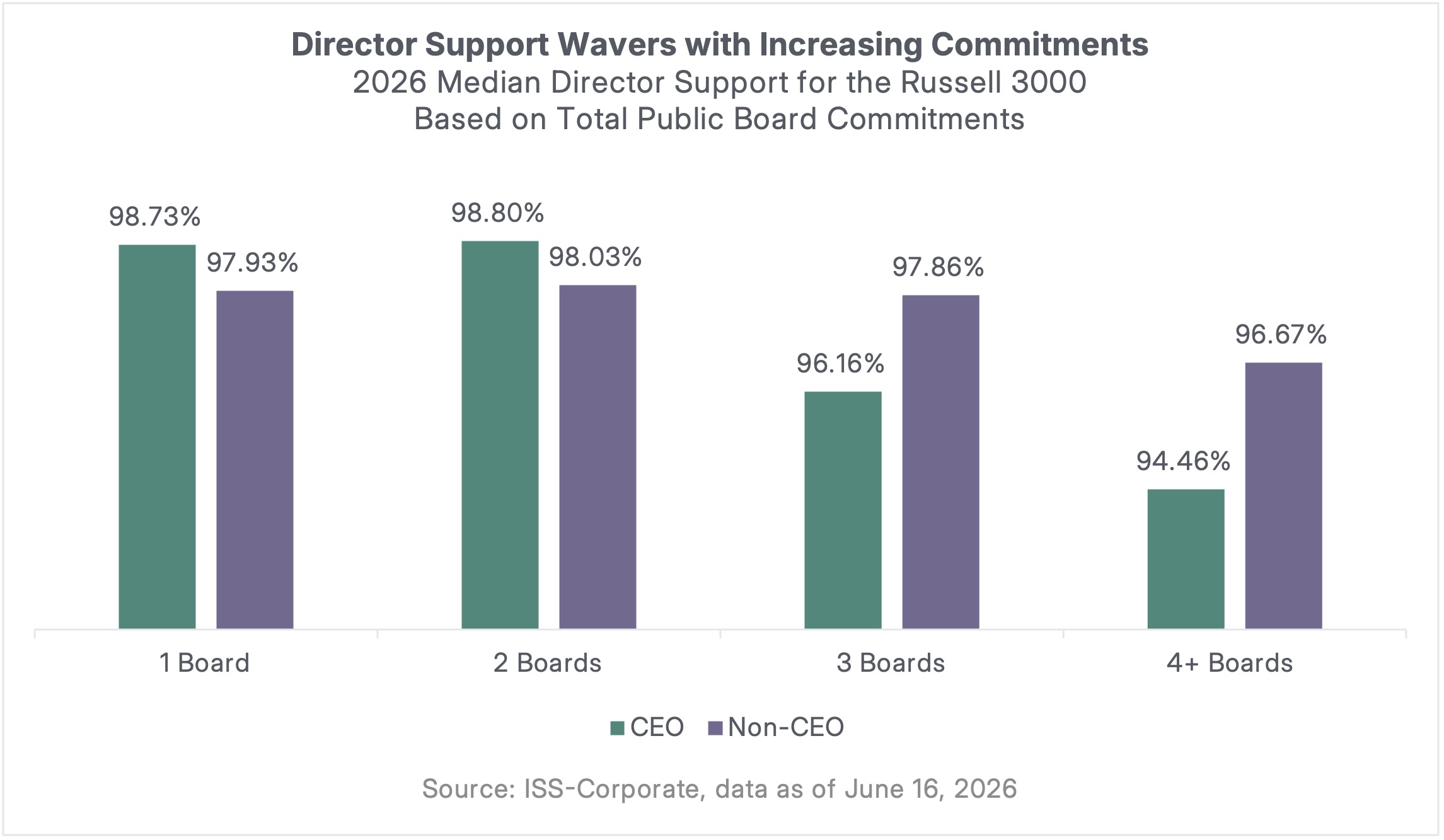

Other factors also continue to affect director support. Notably, director support may decline based on an increasing number of public company board seats a director holds at a given time. Some investors may scrutinize these additional commitments, as concerns arise regarding a director’s ability to devote sufficient time to fulfill their responsibilities to a company and its shareholders. Furthermore, some investors may also consider the director’s role on the board in conjunction with these commitments.

Overboarding and Its Impact on Director Vote Support

In general, the trend demonstrates that directors with more commitments tend to receive lower vote support. The most significant decline in support is observed for CEOs serving on four or more boards.

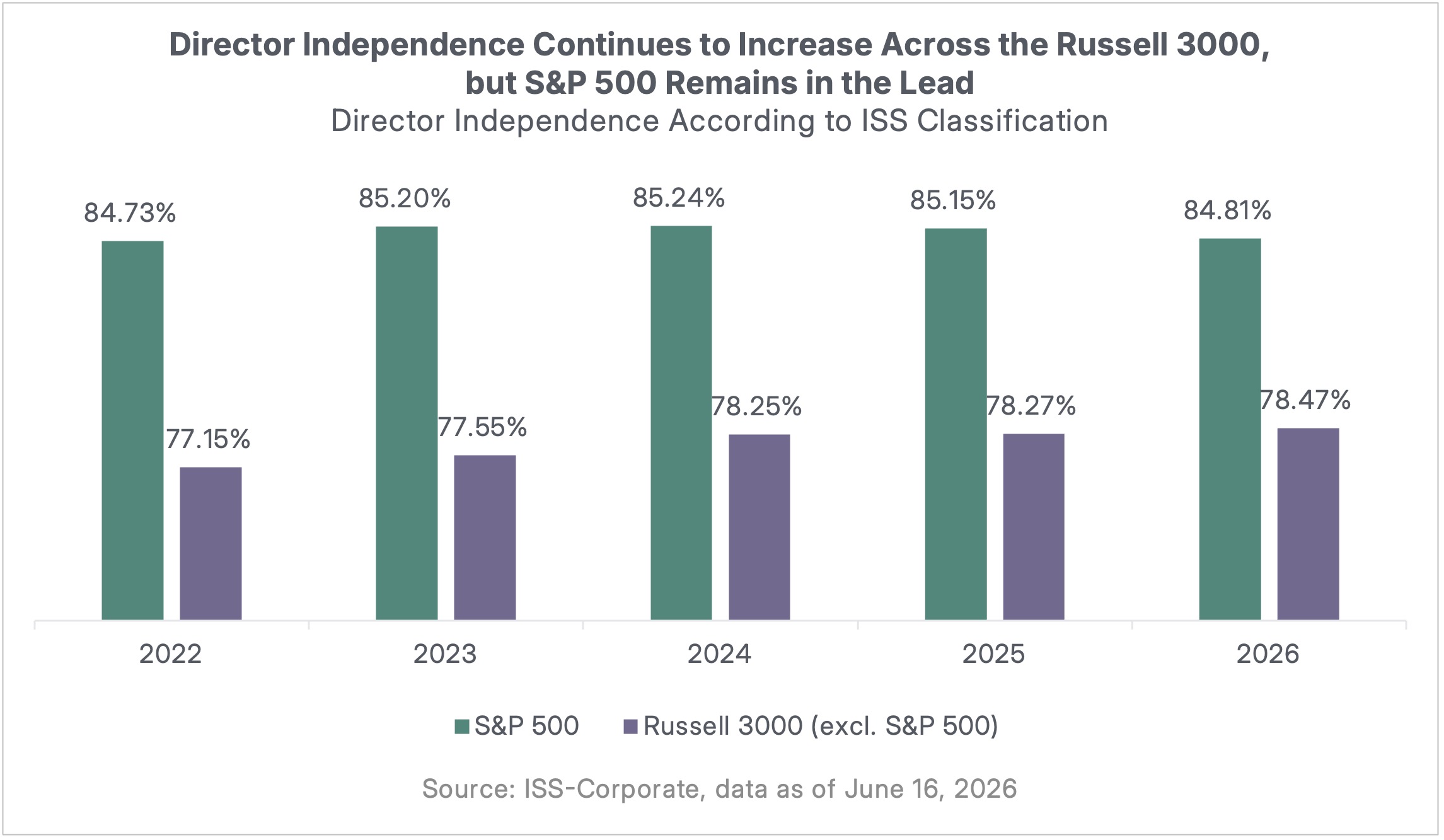

Board Independence Trends Across U.S. Markets

Over time, the aggregate level of board independence across both S&P 500 and Russell 3000 companies has increased. That said, larger and more mature S&P 500 companies continue to maintain a lead in overall independence rates relative to the broader Russell 3000. Given the prevalence of CEO board service across both indexes, further gains in board independence may be constrained.

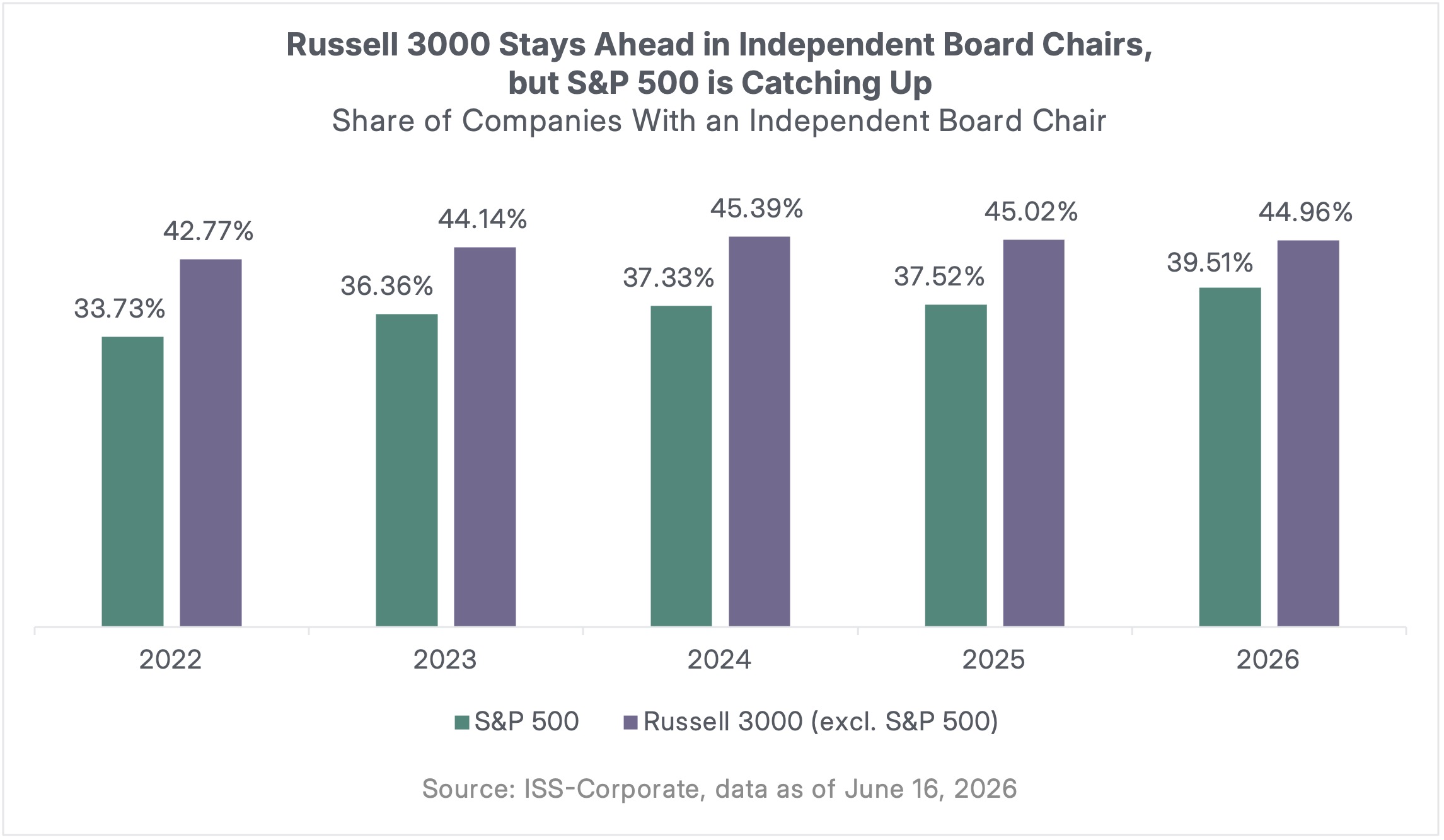

Separation of Chair and CEO Roles Gains Ground

Although the S&P 500 continues to lead in overall independence rates, companies in the remainder of the Russell 3000 have consistently held a higher prevalence of independent board chairs. There has been steady growth in the separation of board chair and CEO roles in recent years. And while this structure has not yet become the majority practice for either index, the S&P 500 has reached a nearly 40 percent threshold for independent board chairs.

ISS-Corporate’s Approach to Proxy Season Insight

ISS-Corporate analyzes proxy voting outcomes and early filing data to identify trends in emerging topics. As investor scrutiny of director accountability and time commitments continues to evolve, issuers need a clearer, earlier view of where support may soften and why. ISS-Corporate’s Governance advisors help companies assess potential vulnerabilities, contextualize voting outcomes, and develop proactive engagement strategies ahead of the annual general meeting.