Print

PrintAvrohom J. Kess is partner and head of the Public Company Advisory Practice at Simpson Thacher & Bartlett LLP. This post is based on a Simpson Thacher memorandum by Mr. Kess, Karen Hsu Kelley, and Yafit Cohn. The complete publication, including footnotes, is available here.

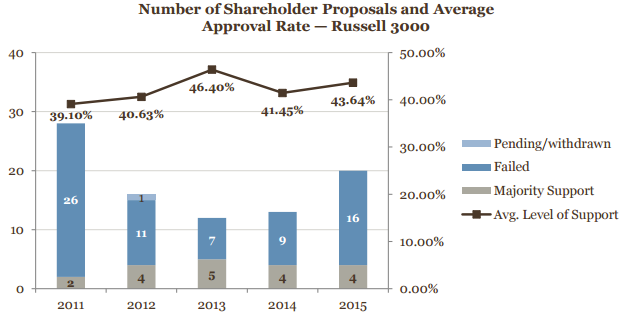

Shareholders petitioning the board for the special meeting right propose either to create the right or, in circumstances where the right already exists, to lower the minimum share ownership threshold required to exercise the right. As of June 30, 2015, 339 companies in the S&P 500 and Fortune 500 already provided their shareholders with the right to call a special meeting outside of the usual annual meeting. During the 2015 proxy season, 20 special meeting shareholder proposals went to a vote at Russell 3000 companies. Of these, six proposed to create the right, and 14 proposed to lower the ownership threshold with respect to an existing right. Only four special meeting shareholder proposals received majority support: three created the right for the first time and one lowered the threshold for an existing right to 25%. Overall, shareholder proposals relating to special meetings received average shareholder support of 43.6% this proxy season.

Positions of the Proxy Advisory Firms

Institutional Shareholder Services Inc. (“ISS”)

ISS prefers a 10% minimum shareholding threshold as opposed to the 20%-25% threshold typically favored by management. Notwithstanding its preference, ISS recommended a vote “for” nearly all shareholder proposals in 2015, even those that proposed a threshold greater than 10%. Likewise, ISS recommended a vote “for” nearly all (12 of 14) management proposals in 2015, even though none of them proposed a threshold of 10% and some were submitted together with a directly conflicting shareholder proposal. Presumably, ISS takes the position that some right is better than no right.

Equally important is ISS’s policy on substantial implementation—if ISS determines that a proposal that received majority support was not substantially implemented by the board, ISS will recommend a vote “against” one or more directors the following year. Failure to substantially implement the proposal includes situations where the board implements the proposal at a different ownership threshold than the one proposed and/or where the board imposes significant limitations on the right.

In addition, ISS takes into account the “inability of shareholders to call special meetings” as a factor in considering whether to recommend a vote against an entire board of directors where the board “lacks accountability and oversight, coupled with sustained poor performance relative to peers.”

Finally, ISS considers the special meeting right when calculating its Governance QuickScore in both the Board Structure Pillar and the Shareholder Rights & Takeover Defenses Pillar. For the former pillar, ISS considers a unilateral board action that diminishes shareholder rights to call a special meeting an action that “materially reduces shareholder rights,” which could affect a company’s score. In calculating the latter pillar, ISS takes into account “whether shareholders can call a special meeting, and, if so, the ownership threshold required.” It also considers whether there are “material restrictions” to the right, which include restrictions on timing, “restrictions that may be interpreted to preclude director elections,” and restrictions that effectively raise the ownership threshold.

Glass Lewis

Glass Lewis provides specific guidelines for voting on special meeting rights. Generally, Glass Lewis is in favor of providing shareholders with the right to call a special meeting, preferring an ownership threshold of 10-15%, depending on the size of the company, in order to “prevent abuse and waste of corporate resources by a small minority of shareholders.” In forming its recommendation, Glass Lewis also takes into account several other factors, including whether the board and management are responsive to proposals for shareholder rights policies, whether shareholders can already act by written consent and whether anti-takeover measures exist at the company.

In addition, Glass Lewis considers the right to call special meetings an “important shareholder right” and recommends voting against members of the governance committee who hold office while management infringes upon “important shareholder rights,” such as when the board unilaterally removes such rights or when the board fails to act after a majority of shareholders has approved such rights.

Positions of Large Institutional Shareholders

While their current positions on special meeting proposals vary, the major institutional investors generally favor shareholders having the right to call special meetings and usually focus on a few key variables, e.g., the minimum ownership threshold associated with the right. Some investors, like State Street Global Advisors, recommend voting for a proposal if the threshold is 25% or less, while others, like Fidelity Management & Research Co., recommend voting for a proposal if the threshold is 25% or more. Sometimes, investors’ policies take into account whether or not the company already provides for a shareholder right to act by written consent. In addition, some investors support management proposals outright but are more wary of shareholder proposals that may support the narrow interests of one or few shareholders.

SEC No-Action Letters

On January 16, 2015, Securities and Exchange Commission (“SEC”) Chair Mary Jo White announced that she had directed the staff of the SEC’s Division of Corporation Finance (the “Division”) to review the scope of Rule 14a-8(i)(9) under the Securities Exchange Act of 1934, which permits the exclusion of a shareholder proposal from a company’s proxy statement if it “directly conflicts” with a management proposal to be submitted to shareholders at the same meeting. Also on January 16, 2015, the Division announced that it would not express any view with respect to requests for exclusion based on Rule 14a-8(i)(9) during the 2015 proxy season.

While the Division’s announcement was a reaction to controversy over a no-action letter issued on the basis of Rule 14a-8(i)(9) with regard to a proxy access proposal (and the subsequent influx of similar no-action requests), the announcement impacted no-action requests pertaining to other shareholder proposals, including those relating to special meetings. Out of a total of 17 no-action requests seeking exclusion of special meeting shareholder proposals for the 2015 season, 12 were predicated on Rule 14a-8(i)(9). Three companies—BorgWarner Inc., Illinois Tool Works Inc., and Deere & Company—submitted no-action requests based on Rule 14a-8(i)(9) prior to the Division’s announcement and were granted relief. In response to the respective proponents’ requests for reconsideration after the Division’s announcement, the SEC subsequently revoked the no-action relief it had granted BorgWarner and Illinois Tool Works, causing each of these companies to include the special meeting shareholder proposal in its proxy materials. Deere & Company, however, excluded the proposal; the proponent never requested reconsideration, perhaps because the company’s annual meeting was scheduled to be held shortly after the Division’s announcement. In addition, AGL Resources, another company among the 12 that had requested no-action relief under Rule 14a-8(i)(9) and received no response, later implemented the shareholder proposal unilaterally and requested an exclusion under Rule 14a-8(i)(10) due to its “substantial implementation” of the proposal. The SEC granted this request. Thus, 11 of the 12 no-action requests originally arguing for exclusion under Rule 14a-8(i)(9) ultimately received no substantive response, though AGL Resources later received no-action relief under Rule 14a-8(i)(10). This is in stark contrast to 2014, in which 66.7% of no-action requests (or 12 of 18) pertaining to special meeting proposals were granted on the basis of Rule 14a-8(i)(9), and 2013, in which 76.9% of no-action requests (or 10 of 13) were similarly granted.

Of the five remaining no-action requests pertaining to special meeting proposals during the 2015 proxy season, two were based on substantive grounds. As in the case of AGL Resources, one of these requests was granted on the basis that the company had substantially implemented the proposal. In that case, Windstream Holdings, Inc. had received a shareholder proposal seeking the right to call special meetings for holders of 20% of the company’s outstanding stock, and the company’s board later approved and planned to “submit for a shareholder vote at the upcoming annual meeting, an amendment to the company’s certificate of incorporation and bylaws to permit shareholders who have held at least a 20% net-long position in the company’s outstanding common stock for at least one year to call a special meeting.” Based on this information, the Division agreed that the company could omit the proposal from its proxy materials.

The second substantive request for exclusion was based on Rule 14a-8(i)(3), which permits the exclusion of proposals that are contrary to any of the SEC’s proxy rules, “including Rule 14a-9, which prohibits materially false or misleading statements in proxy solicitation materials.” In that case, AT&T Inc. had argued that the proposal and its supporting statement contained two material misstatements of fact and one material omission, rendering the proposal excludable. The Division, however, did not agree, and AT&T included the shareholder proposal in its proxy materials.

Special Meeting Proposal Trends

Overall Trends

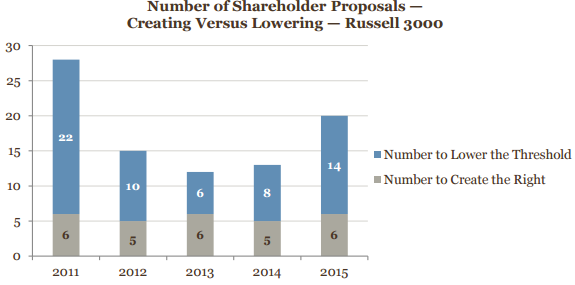

- This proxy season saw the highest number of special meeting proposals since 2011. The number of proposals submitted by shareholders seeking either to create the right to call special meetings or to lower the threshold requirement for share ownership spiked during 2015, with 20 proposals going to a vote at Russell 3000 companies, 14 compared with 13 such proposals going to a vote in 2014. This marked increase in the prevalence of special meeting shareholder proposals has not been seen since 2011, when 28 proposals went to a vote among the Russell 3000.

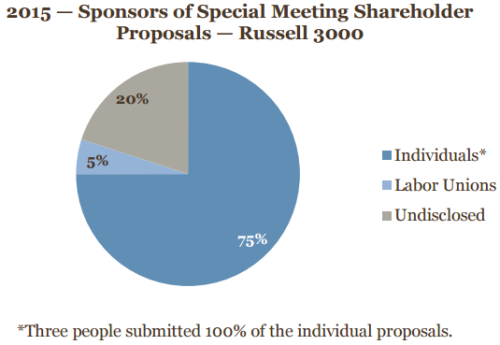

- The majority of proposals were submitted by individual activist shareholders.

- Fewer proposals received majority support, as compared with previous years. While more special meeting shareholder proposals were submitted to a vote during 2015, the proposal’s success rate decreased compared to the past three years—20.0% (or four of 20) received majority support in 2015, while 41.7% of proposals received majority support in 2013 and 30.8% received majority support in 2014. This decrease in success rate may be due to this season’s relatively high proportion of proposals to lower the threshold for an already existing right, as discussed further below.

- Shareholder approval rates remain high, consistent with past years. The average approval rate for special meeting shareholder proposals in 2015 was 43.6%, slightly higher than last year’s average approval rate of 41.5% and generally consistent with average shareholder support for special meeting proposals over the last five years.

Creating the Right Versus Lowering the Threshold

Shareholder proposals to create the right to call a special meeting have historically been more likely to receive majority or close-to-majority support than shareholder proposals to lower the threshold. Over the past five years, 10% of all proposals (or six of 60) to lower the threshold of an existing right have passed, whereas 46.4% of proposals (or 13 of 28) to create the right have passed.

Creating the Right

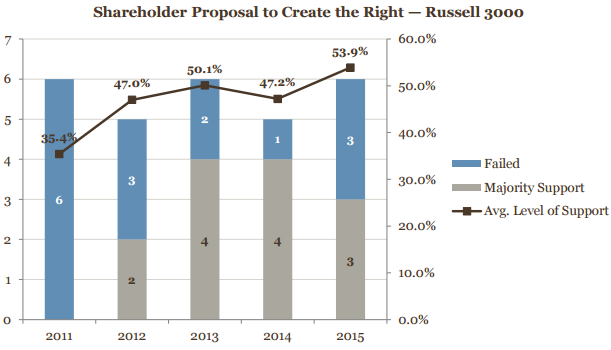

Of the 20 proposals that went to a vote in 2015, six sought to create the special meeting right for the first time. Three out of six proposals to create the right received majority support this proxy season, consistent with previous years.

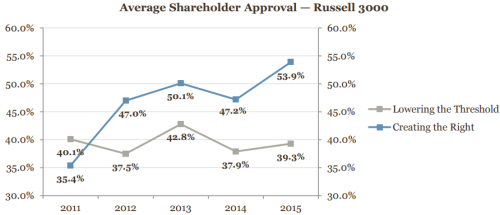

This year, the average level of shareholder support for proposals seeking to create the right was 53.9%, representing an increase compared with previous years.

Lowering the Threshold

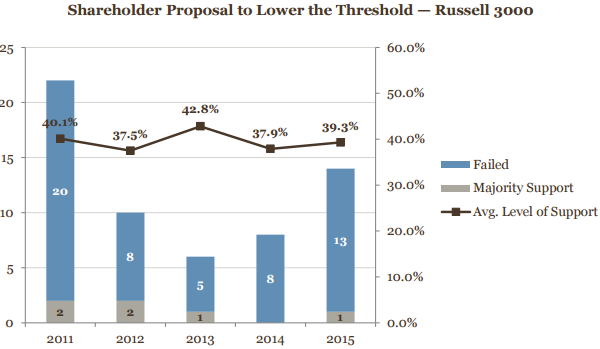

Of the 20 special meeting shareholder proposals that went to a vote in 2015, 14 proposed to lower the ownership threshold of an existing right. This is a marked increase compared to 2013, in which six such proposals went to a vote, and 2014, in which eight such proposals went to a vote. Notwithstanding the increase in proposals, only one of these proposals (submitted to The Timken Company) received majority support, which is consistent with the low success rate of these proposals in previous years.

The average level of shareholder support in 2015 for proposals seeking to lower the threshold was 39.3%, generally comparable to the shareholder support these proposals received over the past five years, which ranged from 37.5% to 42.8%.

Management Responses to Special Meeting Shareholder Proposals

Following the Division’s announcement that it would not consider no-action requests on the basis of Rule 14a-8(i)(9), issuers that received special meeting shareholder proposals were left with three options, aside from negotiating with the proponents. These options are represented in the chart below, along with the companies that chose each option, the breakdown of which proposals sought to create the right and which sought to lower the threshold, and the results of the vote.

| Option | Companies | Results |

|---|---|---|

| 1) Include the shareholder proposal with an opposition statement from management

(13 companies) |

AT&T Inc.; L-3 Communication Holdings, Inc.; Alexion Pharmaceuticals, Inc.; The Timken Company; Kansas City Southern; Newell Rubbermaid Inc.; Morgans Hotel Group Co.; Ford Motor Company; JP Morgan Chase & Co.; Southwestern Energy Company; ITC Holdings Corp.; The Home Depot, Inc.; Chevron Corporation | Two of the 13 proposals sought to create the right; one received majority support (Average Support = 49.2%) 11 of the 13 proposals sought to lower the threshold; one received majority support |

| 2) Include the shareholder proposal with directly conflicting management proposal

(6 companies)* |

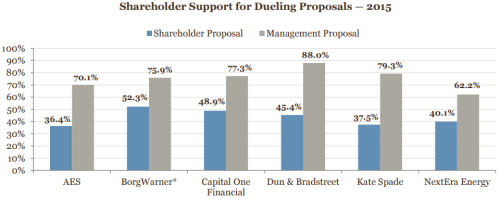

The AES Corporation; BorgWarner Inc.; Capital One Financial Corporation; The Dun & Bradstreet Corporation; Kate Spade & Company; NextEra Energy, Inc. | Three of the six proposals sought to create the right; one received majority support (Average Support = 45.9%) Three of the six proposals sought to lower the threshold; none received majority support |

| 3) Include and support the shareholder proposal

|

Illinois Tool Works, Inc. | One proposal sought to create the right (Received 87.3%) |

*In each case where the company submitted a directly conflicting management proposal, the management proposal garnered majority support, receiving average support of 75.5%.

Trends Among Companies Submitting Dueling Proposals

Of the six shareholder proposals that were submitted with conflicting management proposals, five failed, and one received majority support.

*BorgWarner’s bylaws require 80% of the vote to amend its certificate of incorporation, which is what BorgWarner’s management proposal suggested. Accordingly, as a technical matter, the management proposal did not pass despite receiving higher shareholder support.

*BorgWarner’s bylaws require 80% of the vote to amend its certificate of incorporation, which is what BorgWarner’s management proposal suggested. Accordingly, as a technical matter, the management proposal did not pass despite receiving higher shareholder support.

Trends Among Companies That Have Adopted the Proposal

Four companies that faced shareholder-sponsored special meeting proposals chose to unilaterally amend their certificates of incorporation and bylaws to adopt the proposal and did not submit the shareholder proposal to a vote. As noted above, two of them petitioned the SEC for exclusion pursuant to Rule 14a-8(i)(10) for having “already substantially implemented the proposal.” While not publicly disclosed, it is likely that the other two companies that excluded the shareholder proposal from their proxy materials negotiated exclusion with the shareholder proponent.

Threshold Levels

As noted above, 14 of the special meeting shareholder proposals that went to a vote in 2015 sought to lower the ownership threshold of an existing right. Twelve of these proposals sought to lower the higher existing ownership threshold to a 10% ownership threshold. All of these failed, receiving average support of 37.8%. This represents a departure from prior years; in 2011 through 2014, 29 shareholder proposals sought to lower the threshold of an existing right to 10%, three of which received majority support. At two of these three companies, the existing special meeting right was set at 50%; at the remaining company, the existing right was set at 25%.

Based on current voting trends, it seems that shareholders are likely to support some right to call a special meeting. This year’s voting results indicate, however, that shareholders may not necessarily believe that a 10% threshold is the most appropriate. At 18 of the 20 companies that received a shareholder proposal in 2015, shareholders seemed to prefer thresholds of at least 15%, but most often 20-25%. The voting results at these 18 companies can be broken down as follows:

- Dueling Proposals. When confronted with a shareholder proposal that directly conflicted with a management proposal, five companies’ shareholders supported management-sponsored thresholds of 20-25% and rejected shareholder-sponsored thresholds of 10% or even 20%.

- Shareholder Proposals Seeking to Create the Special Meeting Right. When confronted with a shareholder proposal to create the special meeting right, two companies’ shareholders voted to create a special meeting right for holders of 20-25% of the company’s stock.

- Shareholder Proposals Seeking to Lower the Threshold of an Existing Right. When confronted with a shareholder proposal to lower the threshold of an existing right in the absence of a competing management proposal, the vast majority of shareholders rejected entreaties to lower the existing thresholds, which ranged from 15-50%. Of the eleven companies affected:

- At ten companies, shareholders opted to retain the companies’ preexisting thresholds of 15-50% and voted against shareholder proposals seeking to lower the threshold. Five of these existing thresholds were set at 20-25%.

- At one company, shareholders voted in favor of a shareholder proposal to lower the threshold to 25%.

These results suggest that companies that have a special meeting right in the 15-25% range could, depending on the circumstances, be more successful in warding off potential future attempts to lower the threshold.

Takeaways

If faced with a shareholder proposal relating to the ability of shareholders to call a special meeting, management should take into consideration whether the proposal seeks to create the right for the first time or to lower the threshold of an existing right. In addition, the likelihood of a proposal garnering majority support depends, in part, on the proposal’s thresholds for triggering the right.

Depending on the results of the SEC’s pending review of Rule 14a-8(i)(9), some issuers may determine to submit a management-sponsored proposal to their shareholders with a higher threshold that it deems appropriate for the company and its individual circumstances. Some companies may find it advantageous to adopt the right to call special meetings unilaterally, permitting the company to maintain control over the specifics of the bylaw and, in certain circumstances, allowing the issuer to petition the SEC for no-action relief to exclude the shareholder proposal under Rule 14a-8(i)(10) for having “substantially implemented” the proposal. Regardless, as with many governance proposals, it is critical to engage with the company’s shareholders and understand their positions prior to deciding on an approach. In addition, issuers should take into account the possibility that failure to substantially implement a special meeting shareholder proposal that received majority support can yield negative vote recommendations from the proxy advisory firms against one or more of the company’s directors.

The complete publication, including footnotes, is available here.