Print

PrintThis post is by Jeffrey N. Gordon of Columbia Law School.

Despite last year’s near-miss of a Money Market Fund catastrophe, the SEC’s current Money Market Reform proposal asks for only modest reforms that fail to address the key issues of this $3.8 trillion financial intermediary; indeed, that may well aggravate systemic risk. First, the proposal does not appreciate that there are really two separate MMF types, retail MMFs and institutional MMFs, with different regulatory needs. Retail MMF investors are looking for a bank account that combines safety with a higher rate of interest. For them there is no substitute for fixed NAV, “safety and soundness” portfolio constraints and deposit insurance paid for with risk-adjusted premiums. Institutional MMFs, which now account for approximately 60% of MMF assets, function as low-cost providers of a corporate treasury function for large business entities. This outsourcing saves these entities (corporations, life insurers, pension funds) the need to assemble individual portfolios of money market instruments the value of which would of course fluctuate. Institutional MMFs thus should not carry a fixed NAV or the associated portfolio constraints. Second, the SEC proposal fails to appreciate how MMF regulation creates systemic risk by artificially increasingly the supply of short term finance. The consequence is to shift maturity transformation away from banks to short term credit markets, which, as last fall demonstrated, may seize-up in times of financial distress. As suggested by the Group of 30’s report in February 2009, whether money market funds are a desirable innovation needs full scale examination.

These ideas are developed in a comment letter I submitted to the SEC on its Money Market Reform Proposal. Here’s the text of the letter:

This letter is submitted by me personally in response to the SEC’s request for comments on its proposed Money Market Reform Rule announced in Release No. IC-28807. This letter proposes a different direction to reform, one that begins with the division between retail and institutional money market funds and that takes account of the different motives and needs of the investors in each.

“Reform” is of course timely in light of the fragility of Money Market Funds (“MMFs” ) revealed in the financial distress that followed the failure of Lehman Brothers. As the Commission describes quite well in the Release, Lehman’s failure unexpectedly led to the “busting of the buck” by the Reserve Fund, which held a large amount of Lehman’s commercial paper in its portfolio. The problems at the Reserve Fund in turn triggered a “run” especially by institutional investors on non-Treasury MMFs that was staunched only by an extraordinary MMF guarantee program provided by Treasury and by the creation of a special MMF liquidity facility by the Federal Reserve. It is also widely believed that FDIC decisions in addressing bank failures – whether or not to protect bank creditors – were influenced by concerns about the solvency of MMFs that held bank paper. Various MMFs undertook their own safeguards against the risk of runs, principally by selling off commercial paper (that is, making use of the Fed’s facility) and by shifting their portfolio composition towards Treasury instruments (Federal agency debt for the adventurous) and by shortening maturities. These measures had their own consequence, namely a sharp contraction in the demand for commercial paper and other short term credit instruments that industrial and financial firms had come to rely upon in their corporate finance plans. The Federal Reserve responded with another special liquidity facility in which the Fed’s became a buyer of last resort of commercial paper.

In response to this very unsettling episode, a near-calamitous run on a form of financial intermediary that accounts for nearly $4 trillion in assets, the SEC has come up with a quite modest set of reform proposals: improve the quality of MMF portfolio securities, shorten maturities, enhance portfolio liquidity, and provide a smoother resolution process for occasions when an MMF has “busted the buck.” With all respect, I think the SEC has failed to grapple with the fundamental problems with MMFs that last fall’s financial crisis revealed and, in the main, its proposals will exacerbate systemic fragility, not reduce it.

Rather, the SEC should be preparing the way for serious consideration of proposals like those made by the Group of Thirty in February 2009, which call for a sharp division between funds that offer “withdrawals on demand at par, and assurances of maintaining a stable net asset value” and those that offer a “conservative investment option … with no explicit or implicit assurances to investors than funds can be withdrawn on demand at stable NAV.” The former accounts should be offered through special banks that include government deposit insurance. The latter accounts might be styled as “money market funds,” subject to customary mutual fund valuation rules and no promise of a stable NAV.[1]

Barring such a wholesale rethinking, a minimum reform strategy should begin with a sharp division between MMFs sold to retail investors, “retail MMFs,” and those that are sold to corporations, life insurers, pension funds and other large purchasers, “institutional MMFs.” Retail MMFs should be covered by deposit insurance that is funded by risk-adjusted premiums. Institutional MMFs should give up the promise of a fixed NAV, and disclosure rules should replace mandatory portfolio composition rules. These changes will reduce the systemic risk created by the present MMF regulatory structure both by reducing the risk of “runs” and by reducing distortions in short term credit markets.

It is widely appreciated that MMF holders receive an unpaid-for benefit through an implicit, if imperfect, government guarantee of their accrued balances. The flaw with the SEC’s approach is that the regulatory effort to substitute for the absence of explicit deposit insurance and to limit the implicit subsidy through restrictions on MMF portfolios adds systemic risk to financial intermediation by heightening the pressure on short-term money markets in the critical function of maturity transformation. This flaw turns out to be fundamental and requires a rethinking of the general MMF framework.

To understand this objection, it is necessary to appreciate the origin and consequences of MMF growth in the financial system. MMFs arose in the 1970s as an evasion of the regulatory ceiling on interest rates that depository institutions, banks and thrifts, could offer to depositors, so-called “Reg Q.” At a time of high short interest rates, MMFs provided retail savers access to money market rates and became a substitute for both savings and checking accounts. The industry and the SEC understood this substitution. As a marketing tool, as consumer protection, and presumably as systemic risk mitigation, the industry and the SEC collaborated on a series of portfolio constraints, principally to limit maturities and to assure credit quality, in order to lower the risk that MMF shares would fall below a fixed net asset value, typically $1 a share. The SEC also provided a form of regulatory forbearance that permitted MMFs to use “hold to maturity” rather than “mark to market” valuations to smooth over small deviations from par. The SEC also from time to time has granted regulatory relief to permit MMF sponsors to support $1 net asset values through buying distressed securities in MMF portfolios. The limitations of these SEC-crafted substitutes for deposit insurance became apparent in the financial market distress of fall 2008.

The deposit insurance gap for MMFs is relatively well-understood and appears to animate the SEC’s reform proposal. Portfolios of shorter maturities and higher credit quality should be less exposed to default risk; this enhanced security partially substitutes for explicit deposit insurance in bolstering investor confidence. What is not appreciated is how MMFs have distorted financial intermediation by shifting the process of maturity transformation from banks to securities markets, which are prone to seize-up at times of financial distress. Indeed, by shortening maturities the SEC proposal will increase rather than reduce the fragility of these markets because it makes it easier for MMFs to “run” at a time of financial distress.

What is “maturity transformation?” It is the conversion of the short term liquidity needs of depositors into long-term funding commitments for borrowers. Banks have traditionally performed this function. Depositors put funds into checking accounts and savings accounts and certificate of deposit, which can be withdrawn from the bank on demand, though perhaps with some notice in the case of savings accounts and the forfeiture of some interest in the case of CD’s. In turn, the bank lends these deposited funds to borrowers on typically much longer-lived terms, whether to fund specific projects or asset purchases, or by way of a long term lending commitment. This bank activity thus “transforms” short term liabilities into long term assets, hence “maturity transformation.” Under this arrangement, the bank will not necessarily have cash immediately available in the event of unexpected depositor withdrawals. But the bank can borrow money from other financial institutions on the security of its assets, and, in the case of systemic liquidity pressure, can borrow from a “lender of last resort,” like the Federal Reserve. The process by which the different time horizons of depositors and borrowers are nevertheless matched up is at the core of a successful system of financial intermediation.

The entry of MMFs shifts the process of maturity transformation away from banks and into the short term securities markets, the money market. This is because the issuers of MMF-qualified debt under the SEC rules – commercial paper, for example – often use money market proceeds to fund long term projects or long term assets, counting on their ability to refinance, or “roll-over,” their short term obligations as they come due. There are “demand” side reasons for the increasing use of money markets in this way. If the yield curve is “upward sloping,” meaning that short run rates are less than long term rates, a borrower may be able to finance a long term asset more cheaply through successive rollovers than through a bank loan. The borrower can deal with the possibility of interest changes through interest rate swaps and other hedging techniques. But there are also “supply side” reasons for the turn to money markets to finance long term commitments, linked to the regulatory set up of MMFs. First, MMF investors do not pay for the implicit government guarantee, which means that MMFs have a pricing advantage over banks in competing for deposits. This increases the supply of short term finance. Second, the NAV stability requirements imposed by the SEC artificially limit MMF purchases to short term instruments, currently a weighted average portfolio maturity of 90 days but more broadly, instruments of approximately one year or less. This augments the supply of short term finance generally. Third, the “weighted average” rules permits funds to balance off longest maturity instruments that pay highest interest with shortest maturity instruments; this increases the supply of the instruments like overnight repurchase agreements. Fourth, the “quality” requirements for MMF-eligible instruments favor the highest rating securities; this gives issuers a reason to create credit vehicles that can receive high ratings from the credit rating agencies. MMFs thus provide a stimulus to the creation of short term instruments through “structured finance.” In sum, the regulatory set-up of MMFs increases the supply of short term credit and also distorts its particular forms.

Last fall vividly illustrates the consequence of shifting maturity transformation towards the money markets. At a time of financial distress, commercial paper and other forms of short term debt did not “roll.” Maturity transformation abruptly broke down as credit suppliers simply stopped lending. Money market funds were major participants in a “run” on the financial system. Not only did investors in money market funds, especially investors in so-called “institutional funds, cash out of their MMF positions, which required MMF liquidation of credit positions, but the MMFs independently withdrew from the commercial money market in favor of government money markets. This in turn contributed to the immediate crisis for investment banks, which were highly dependent on short term finance, resolved in the case of Goldman Sachs and Morgan Stanley only by their conversion to bank holding companies. It also contributed to the funding crisis faced by commercial issuers, resolved by the Federal Reserve’s creation of the special credit facilities referred to previously.[2] It is worth repeating that the SEC’s proposal to shorten average portfolio maturities will make it easier for MMFs to run in the future, simply by refusing roll over credits. Moreover, the pressure on MMFs to maintain a $1 NAV adds to the impetus to run both by converting current holdings to cash and by shifting purchases from commercial paper to government instruments.

These analytic points can be buttressed by looking at the data relating to patterns of MMF growth and practices over the past 35 years, drawn from data compiled by the Federal Reserve in its Flow of Funds reports.

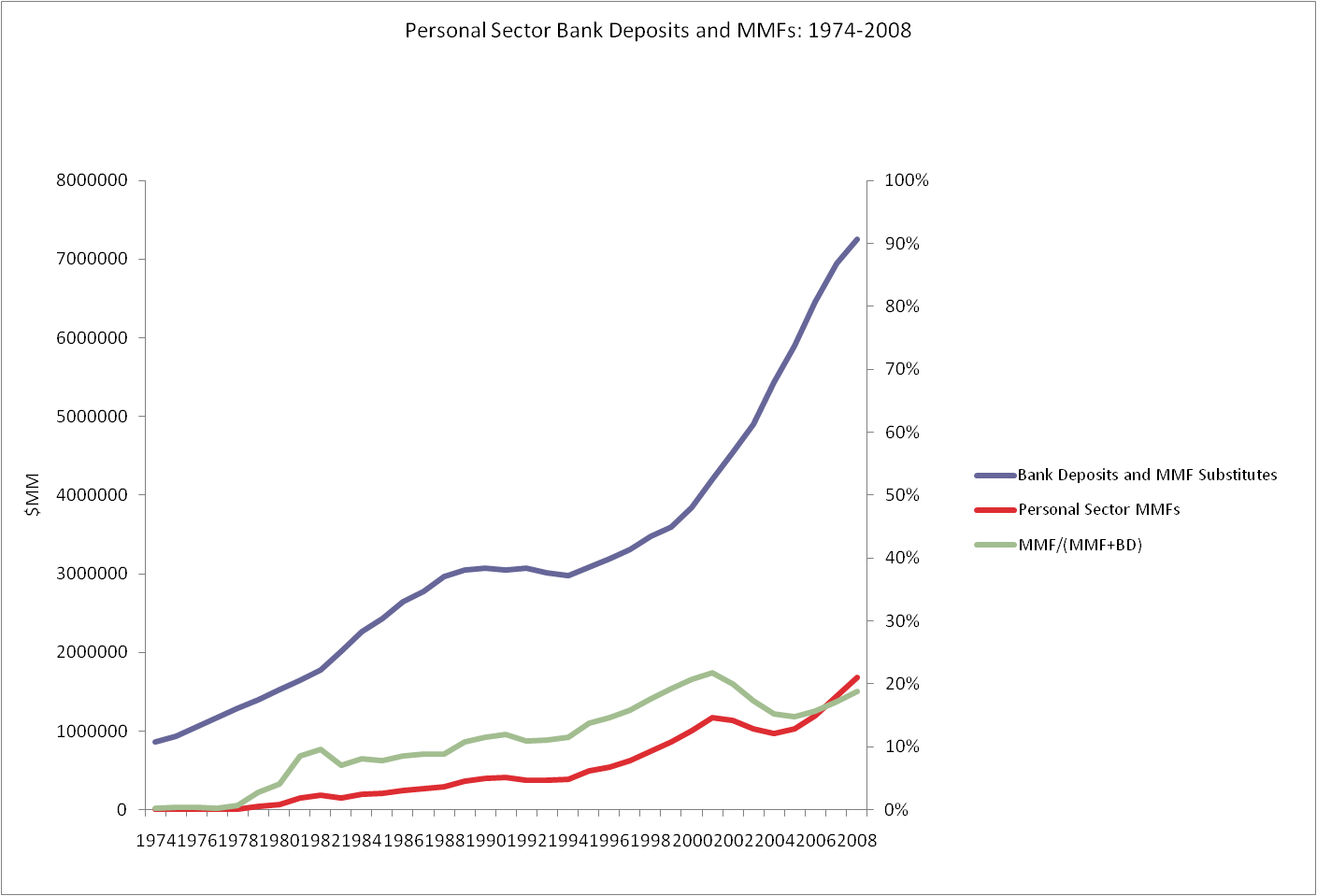

Figure 1 shows the substitution of money market funds for retail bank deposits, now at the rate of approximately 20 percent. The top line reflects (on the left y-axis) the sum of “personal sector” bank deposits plus retail MMFs, what might be thought of as bank deposits plus MMFs that substitute for bank deposits. The second line shows (on the left y-axis) the dollar amount of retail MMFs, and the third line (which is in the middle line during most of the time period) shows (on the right y-axis) the percentage of bank deposits and substitutes represented by MMFs. Figure 1 shows that retail MMFs have steadily increased over the 1974-2008 period, now amounting to nearly $1.5 trillion. The figure also shows the substitution effect, which has also increased throughout most of the period, leveling off in the 20 percent range.

Figure 1

Source: Federal Reserve, Flow of Funds, Table L.5 (2009).

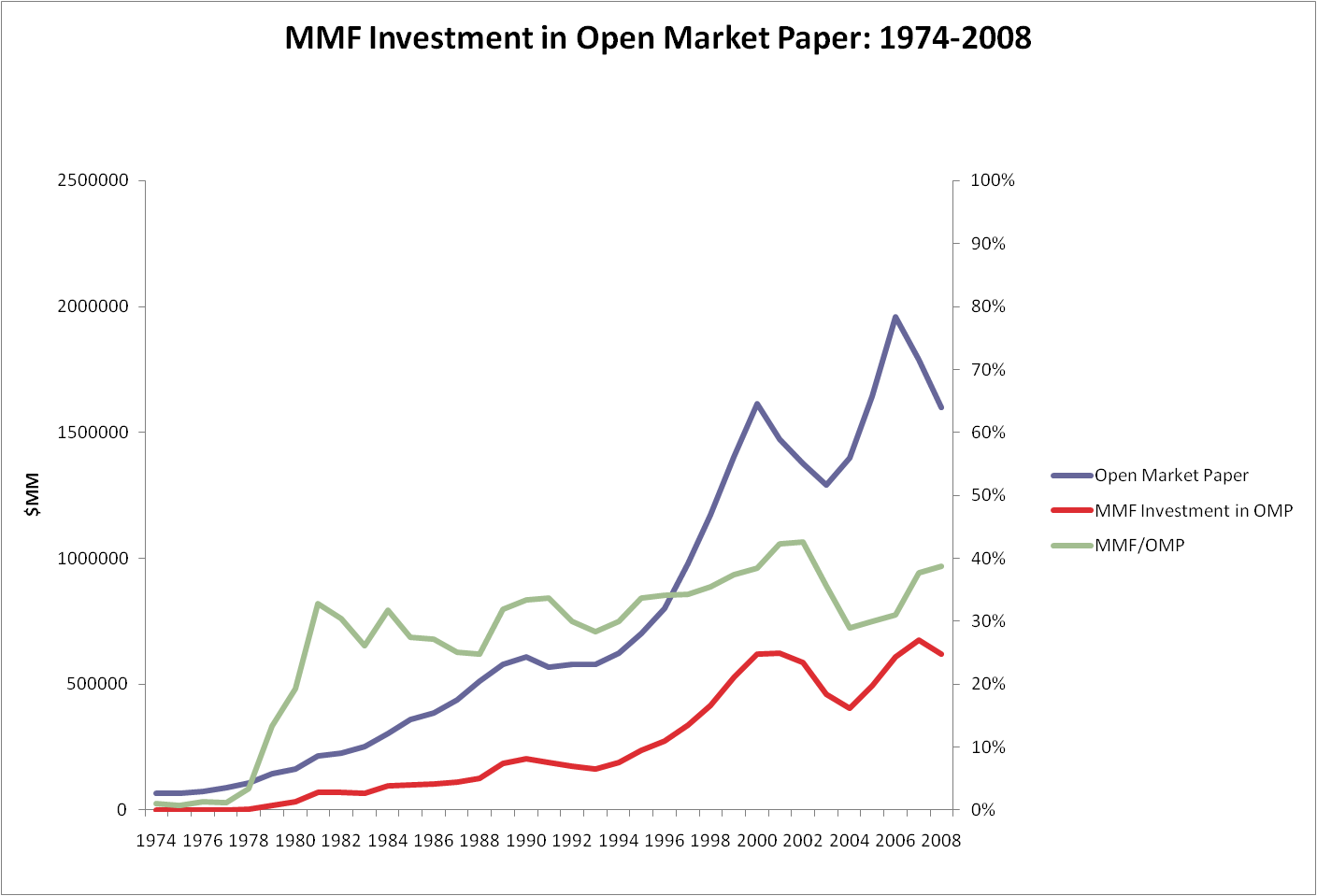

Figure 2 shows how the growth of MMFs has contributed to the expansion of money markets more generally, here categorized as “Open Market Paper” (principally commercial paper). The growth of the commercial paper market over the 1974-2008 period (top line, left y-axis) has been matched by the growth of MMF investment in commercial paper (bottom line, left y-axis). The fraction of MMF participation in the commercial paper market has remained at 30 percent or more from early in the period, peaking at 40 percent (middle line, right y-axis).

Figure 2

Source: Federal Reserve, Flow of Funds, Table L. 208 (2009)

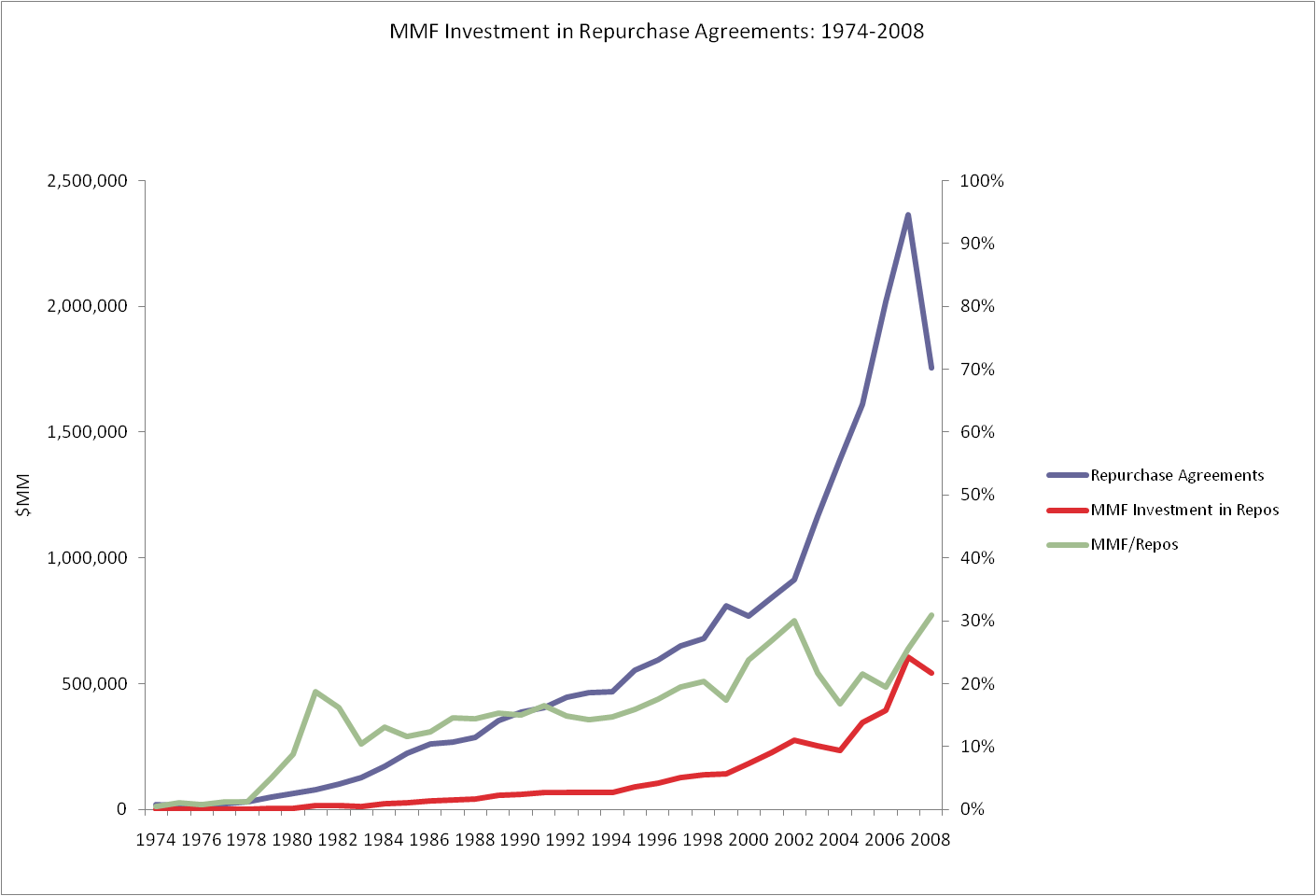

The contribution of MMFs to the fragility of financial firms is reflected in Figure 3, which shows the MMF share of repurchase agreements, a form of very short term finance often rolled over nightly. Repurchase agreements are commonly used by investment banks and other financial institutions. As Figure 3 ( top line, left y-axis) reflects, in the post-2000 period investment banks increasingly turned to overnight funding of their balance sheets, which increasingly came to include long-duration mortgage-backed securities. This is a classic case in which the money markets were employed for maturity transformation. Figure 3 (bottom line, left y-axis) shows the dollar increase in MMF participation in the repo market; the middle line, showing the ratio (right y-axis), has been 20 percent or more since early in the period, peaking at 30 percent. This regularity reflects the role of MMFs in a burgeoning financial practice that misfired in the face of financial distress. At the critical moment in fall 2008, the repo market simply froze; the buy-side participants “ran” by refusing to roll over their purchases. To be sure, many financial actors refused to roll over repo loans, but the pressure on MMFs to protect the $1 NAV gave MMFs special reason to act preemptively.

Figure 3

Source: Federal Reserve, Flow of Funds, Table L. 207 (2009)

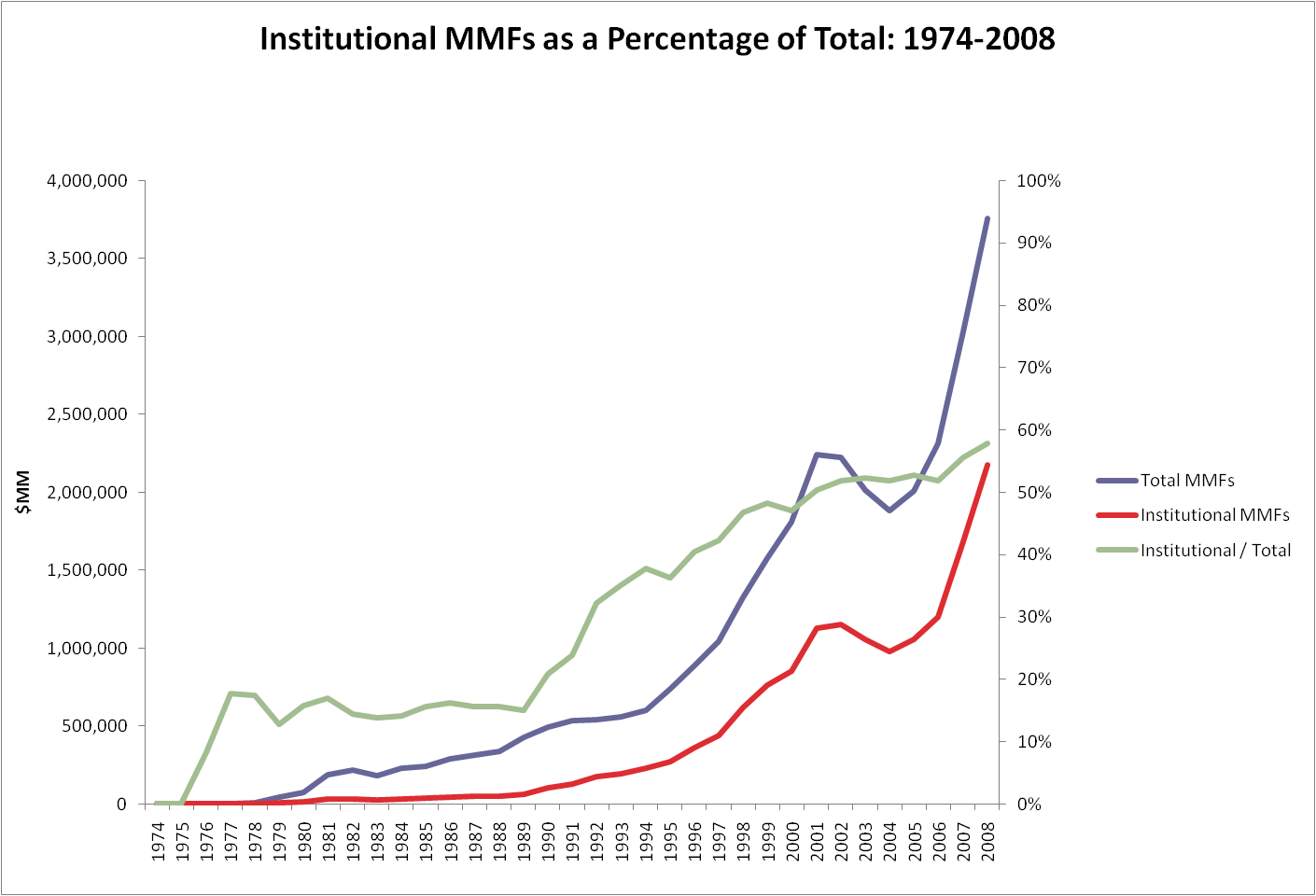

Figure 4 shows another critical feature of MMF evolution that is not sufficiently reflected in the SEC’s reform proposal: the increasing institutional use of MMFs to make money market investments. Figure 4 (top line, left y-axis) shows the growth of money market funds over the 1974-2008 period; the bottom line (left y-axis) shows the growth of institutional MMFs. Particularly important is the steadily increasing asset share of institutional MMFs, which reached nearly 60% of the total by 2008. This is a remarkable development. MMFs started as a vehicle for pooling small depositors’ funds to provide access to money market instruments that otherwise would have been unavailable or uneconomic for them to acquire. But the most important purchasers of institutional funds, large business entities, can participate in money markets directly. Thus the MMF plays a different function for the two investor classes: For the retail investor, the MMF is a risk-free (but higher yielding) substitute for a bank account covered by deposit insurance; for the business investor, the MMF is a low-cost specialized provider of a corporate treasury function. In other words, the functional substitute for the business user of an MMFs is not a bank account covered by deposit insurance; rather, it’s the entity’s direct purchase of money market instruments. Yet institutional MMFs are covered by the same safety and soundness rules as retail MMFs: the portfolio maturity, credit quality, and NAV rules that exacerbate fragility in financial distress and that distort maturity transformation. Whatever the consumer protection arguments for such protections in the case of retail MMFs (despite the distortions), no such arguments pertain for institutional MMFs. There the distortions present only costs, no benefits.

Figure 4

Source: Federal Reserve, Flow of Funds, Table L.206 (2009).

Where does this lead in terms of MMF reform? A minimum reform strategy should create a sharp divide between retail MMFs (“RMMFs”) and institutional MMFs (“IMMFs”). For IMMFs, the SEC should fundamentally change the rules. IMMFs should not be pemitted to vary standard valuation methodology to protect a fixed NAV. IMMFs should be freed of mandatory portfolio composition rules, including maturity and credit quality rules. Instead, IMMFs should be required to make detailed disclosure of their internally generated investment rules and make weekly web-site disclosure of their portfolio composition. At most the SEC should facilitate the creation of a number of “standard form” IMMFs that vary in particular portfolio features to economize on disclosure and search costs. Opting into one of these forms upon establishing an IMMF should be voluntary. The expectation is that NAV may fluctuate, but not very much, and probably much less than the package of money market instruments that IMMF purchasers would have assembled if acting independently. This avoids the need to provide a resolution process for IMMFs that “bust the buck,” which is likely to be cumbersome, costly, and slow, if only because of the presumed infrequency of its use.

The result of these IMMF reforms should be to reduce systemic risk. IMMFs will not face special pressure to retain a fixed NAV. The end of mandatory portfolio restrictions should reduce supply side distortions in short term credit markets.

A minimum reform strategy for retail MMFs would impose deposit insurance on RMMFs as a condition for maintaining a fixed NAV. This would both reduce systemic risk (by reducing the likelihood than individual RMMF investors will “run”) and eliminate supply side distortions in money markets by making RMMF purchasers internalize the cost of systemic risk reduction. Banks and RMMFs will compete for deposits on more level ground. Deposit insurance necessarily entails some regulation of portfolio composition to avoid moral hazard. One approach might be a risk-adjusted insurance fee rather than direct regulation of portfolio composition. Unlike in the case of banks, the short-term, market-traded nature of many RMMF-held instruments should make the assessment of a risk-adjusted fee relatively easy. Setting the fee, which should be assessed ex ante so as to avoid a search for a funding source at a time of systemic stress, will be a challenge in light of the infrequency with which MMFs have “busted the buck.” One could imagine setting a cap on a fund that would accrue over time, scaled to the size of the industry, with a risk-adjusted “recycling” procedure that would rebate excess funding to lower risk funds while still collecting fees from higher risk funds. As with any guaranteed deposit system, the SEC would need to establish a resolution procedure that presumably it would administer.

This reforms should be adopted in lieu of the SEC proposals, which do not address the implicit deposit guarantee subsidy nor the supply-side distortions in money markets of the present regulatory structure.

The broader question is whether RMMFs should continue to receive regulatory sanction, or whether, following the proposal of the Group of 30, RMMFs should become limited purpose banks. Assuming that RMMFs paid appropriate risk-adjusted levels of deposit insurance, the remaining advantage of such a far-reaching proposal is to eliminate a regulatory structure that artificially shifts maturity transformation towards short term securities markets, principally with the objective of reducing systemic risk. (Presumably the convenience of RMMFs as part of a package of services offered by a mutual funds provider could be preserved by permitting establishment of a limited purpose bank within the fund family structure.) In this regard the history of the RMMF is important: It was invented as a work-around of interest-rate ceilings imposed by regulation and it has flourished under a regulatory umbrella that has provided implicit, subsidized deposit insurance. The money market distortions created by its portfolio structure contributed to the systemic break of fall 2008, a very serious cost.

What is the continuing value of the RMMF, a peculiar form of non-bank bank? In the spirit of the Treasury’s white paper on financial regulatory reform, it seems to me that’s the inquiry that the SEC’s MMF reform proposal should now undertake.

Footnotes:

[1] Group of Thirty, Financial Reform: A Framework of Financial Stability 29 (Feb. 2009).

(go back)

[2] In some cases regular commercial paper issuers were able to turn to back-up lines of credit at banks but this in turn took funds that banks might have otherwise provided to other borrowers at a time of credit rationing.

(go back)