Print

PrintJames Barrall is a partner at Latham & Watkins LLP, and Matteo Tonello is Director of Corporate Governance for The Conference Board, Inc. This post is based on a Conference Board Director Note by Mr. Barrall and his colleague Alice M. Chung.

With the 2011 proxy season coming to a close, this report reviews the results of the inaugural season of shareholder advisory votes under the Dodd-Frank Wall Street Reform and Consumer Protection Act through June 23, 2011. It further offers recommendations for companies to consider in making their compensation and governance decisions to help position them for future say-on-pay (SOP) votes. [1]

The 2011 proxy season—the first in which all but small public companies in the United States were required to allow shareholders to vote on an advisory basis to approve or disapprove the compensation of their named executive officers—is almost over. Companies with non-calendar fiscal years or delayed meetings will continue to hold SOP votes throughout 2011, but a majority of U.S. companies that are now subject to the vote requirements (and most S&P 500 and Russell 3000 companies with calendar fiscal years) have already had their 2011 shareholder meetings. [2]

There have been many twists and turns this proxy season, but some clear trends and bottom lines have emerged. Now, while experience and memories are fresh, is a good time to review the results of the inaugural SOP season, identify trends and issues, and assess the landscape for future regulations and other developments. Most importantly, companies need to take all of this into account as they make the compensation and governance decisions in 2011 that will best position them for the 2012 proxy season and SOP votes to come.

Background and overview on say on pay When the Dodd- Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) [3] was signed into law almost one year ago, few were surprised by the two pages (of about 850) that made up Section 951 of the act. Section 951 provided that shareholders of U.S. public companies would have the right to cast three types of votes on executive compensation: (i) an advisory vote to approve the compensation paid to named executive officers in the prior fiscal year (the “say-on-pay vote” or “SOP vote”); (ii) a vote on how often this vote should be held (the “frequency vote,” sometimes referred to as the “say-when-on-pay vote”) and (iii) a vote to approve so-called “golden parachute payments” made in connection with an acquisition, merger, or other specified corporate transaction (the “golden parachute vote”). Early attention of companies and executive compensation professionals was on the frequency vote and what frequency companies would recommend and shareholders would support. However, in the last several months, the focus has been on SOP votes, proxy adviser recommendations, company responses, and meeting results.

The SEC’s Final Rules In January of this year, the Securities and Exchange Commission (SEC) issued its final rules (final rules), [4] implementing Section 951 of Dodd-Frank, set forth detailed requirements for these advisory votes, and temporarily exempted smaller reporting companies (i.e., generally, those with less than $75 million in public equity float) from the SOP and frequency vote requirements until 2013. Accordingly, other than smaller reporting companies, all U.S. listed public companies were required to hold an SOP vote and frequency vote at their first shareholder meeting held on or after January 21, 2011 and a golden parachute vote for proxies seeking shareholder approval of mergers and other corporate transactions filed on or after April 25, 2011.

The SOP vote The SOP vote is a vote to approve the compensation paid by a company to its “named executive officers” (those who are named in the company’s proxy compensation tables), as such compensation is disclosed in the proxy, in general, and not with respect to individual elements of compensation or a company’s compensation philosophy or practices. The vote is purely advisory to the companies, and companies are not required to change their pay or policies based on the shareholder vote. It is evident, however, that if a substantial number of shareholders disapproves the named executive officer compensation, companies will respond. The final rules require that the vote be offered in the first annual or other meeting of shareholders on or after January 21, 2011 (January 21, 2013 for smaller reporting companies), and no less frequently than every three years thereafter. The voting results for all matters submitted to shareholder vote, including the results on the SOP vote, are required to be disclosed on a Form 8-K within four business days following the shareholder meeting. Companies are also required to discuss in the Compensation Discussion and Analysis (CD&A) section of their subsequent proxy statements whether they considered the results of the most recent SOP vote and if so, how such consideration affected their executive compensation decisions and policies. In light of this year’s votes, this will make for very interesting disclosure in years to come.

The frequency vote On the frequency vote, the final rules require a vote in the first annual or other meeting of shareholders on or after January 21, 2011 (January 21, 2013 for smaller reporting companies), and thereafter at a shareholder meeting no later than in the sixth calendar year thereafter, as to whether the SOP vote should occur every one, two, or three years. Like the SOP vote, the frequency vote is purely advisory; however, most companies are expected to adopt the frequency selected by a plurality of their shareholders. The final rules also require companies to disclose what decision they had made on how often they would hold their SOP votes in amendments to the Form 8-K filings that initially reported the result of their annual shareholder meetings. [5] However, many companies elected to disclose this decision in the initial Form 8-K reporting their vote results rather than waiting to make the decision and filing their disclosure later.

The golden parachute vote The golden parachute vote applies to any SEC initial proxy filings on or after April 25, 2011 that seek shareholder approval for certain transactions, such as acquisitions, mergers, asset sales, and similar transactions for which SEC filings are required, and requires that shareholders be provided with a separate advisory vote on the golden parachute compensation arrangements covering named executive officers. The final rules also require specific disclosures (in both tabular and narrative formats) of golden parachute payments in the transactional proxy statements of the golden parachute compensation of the named executive officers of both the target and acquirer companies, but only the payments to the soliciting company’s officers must be subjected to the golden parachute vote. In addition, the final rules further require these specific disclosures of golden parachute payments in other filings for transactions that do not require a shareholder vote, such as tender offers and going-private transactions. Like the SOP and frequency votes, the golden parachute vote is also advisory, and does not affect the shareholder vote on the transaction itself.

Under the final rules, companies may avoid a separate golden parachute vote in their transactional proxy statements if the golden parachute arrangements were subjected to a prior SOP vote. However, if any golden parachute payments are adopted or enhanced after the prior SOP vote, the new or enhanced golden parachute arrangements would need to be subjected to a vote in the transactional proxy statement. In that case, the transactional proxy statement would need to provide two separate tabular disclosures, one table showing all golden parachute payments and the second table showing only the new or enhanced payments that are subject to the golden parachute advisory vote.

2011 Frequency Vote Results

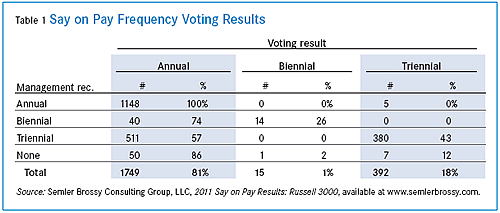

Early in the 2011 proxy season, public companies and their advisors spent much time and effort considering whether companies should recommend annual, biennial, or triennial SOP votes to their shareholders. On one hand, Institutional Shareholder Services (ISS), the most influential U.S. proxy adviser, published its 2011 voting policies and supported an annual SOP vote for all companies, without regard to individual company facts and circumstances, on the grounds that annual votes provided the most consistent and clear communications channel for shareholder concerns about executive pay. On the other hand, many executive compensation and governance experts recommended less frequent votes, arguing that annual votes would only exacerbate the tendency of shareholders to focus on short-term performance, and less frequent votes would allow companies more time to thoughtfully prepare for and react to their shareholders’ advisory votes. In the early months of the proxy season, approximately 60 percent of boards recommended triennial say on pay votes to shareholders. However, early shareholder meeting results made it clear by early March that shareholders were supporting annual votes and more boards began to recommend annual votes. It is now well settled that the annual SOP advisory recommendations and votes have prevailed in the 2011 proxy season.

As of June 23, 2011, shareholder meeting results show that shareholder votes in approximately 81 percent of Russell 3000 reporting companies received more votes for the annual option than for the other two options (i.e., biennial, at 1 percent, and triennial, at 18 percent). [6]

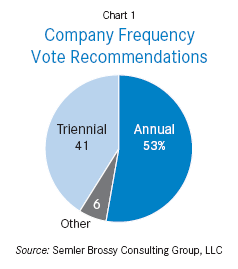

Likely as a result of the early shareholder meeting vote results and the continuing trend, boards with later proxy statement filings have largely acquiesced to ISS and shareholder sentiment and recommended annual SOP votes. As of June 23, 2011, the tally of recommendations for Russell 3000 companies stands at 53 percent annual and 41 percent triennial, with the rest recommending biennial or not recommending anything at all. [7]

Likely as a result of the early shareholder meeting vote results and the continuing trend, boards with later proxy statement filings have largely acquiesced to ISS and shareholder sentiment and recommended annual SOP votes. As of June 23, 2011, the tally of recommendations for Russell 3000 companies stands at 53 percent annual and 41 percent triennial, with the rest recommending biennial or not recommending anything at all. [7]

Not surprisingly, small to mid-sized companies were more likely to receive shareholder votes favoring biennial or triennial frequency votes. [8] Large companies were more likely to receive shareholder votes favoring annual frequency votes. [9]

2011 Golden Parachute Vote Results

Due to the limited benefits of proactively subjecting golden parachute arrangements to an SOP vote, it is not surprising that to date, we have seen only a handful of companies voluntarily subject their golden parachute arrangements to such a vote prior to a transactional proxy statement. Since the golden parachute vote became effective on April 25, 2011, 16 companies had filed transaction proxies soliciting votes for the golden parachute vote as of June 23, 2011. [10] As of June 23, 2011, none of the 16 companies had held their transactional shareholder meetings.

2011 Say on Pay Vote Results

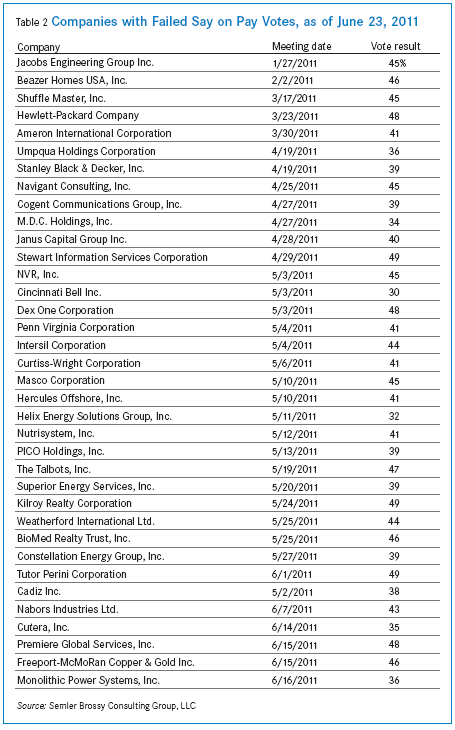

Since March, when companies began to hold their shareholder meetings and it started to become clear that annual SOP votes would win the frequency vote derby, attention has shifted to the SOP vote, focusing on proxy filings, proxy adviser recommendations, company responses, and voting results. As of June 23, 2011, of the 2,193 Russell 3000 companies that filed their SOP vote results with the SEC following shareholder meetings, at least 36 companies (or 2 percent) failed to receive at least majority approval of their SOP proposals. [11]

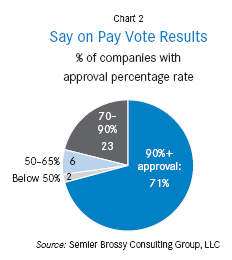

As of June 23, 2011, approximately 71 percent of Russell 3000 companies had sailed through their SOP votes with a shareholder approval rate of at least 90 percent; 92 percent of the companies passed with an approval rate of at least 70 percent. [12]

Impact of proxy adviser recommendations In the 2011 proxy season, ISS has recommended “against” company advisory votes on approximately 13 percent of the proxies it reviewed as of June 23, 2011. Its recommendations have had a meaningful impact on shareholder votes and company responses. As of June 23, 2011, approximately 300 companies had received negative recommendations from ISS on their SOP votes. Every single company that failed to receive at least majority approval of its SOP vote received an “against” recommendation on the vote from ISS. [13] Even where companies passed their votes with majority support in the face of negative ISS recommendations, on average, support from their shareholders was 25 percent lower than for companies that received favorable ISS recommendations. [14]

Impact of proxy adviser recommendations In the 2011 proxy season, ISS has recommended “against” company advisory votes on approximately 13 percent of the proxies it reviewed as of June 23, 2011. Its recommendations have had a meaningful impact on shareholder votes and company responses. As of June 23, 2011, approximately 300 companies had received negative recommendations from ISS on their SOP votes. Every single company that failed to receive at least majority approval of its SOP vote received an “against” recommendation on the vote from ISS. [13] Even where companies passed their votes with majority support in the face of negative ISS recommendations, on average, support from their shareholders was 25 percent lower than for companies that received favorable ISS recommendations. [14]

Other proxy advisers, most notably Glass Lewis, the second most influential U.S. proxy adviser, have issued their fair share of negative SOP vote recommendations, but are not nearly as visible and transparent as ISS in reporting their recommendations. However, based on a review of Glass Lewis proxy reports and of company SEC filings contesting proxy adviser recommendations, as well as statements made by institutional shareholders, it appears that Glass Lewis’s negative recommendation rate has been comparable to ISS’s 13 percent rate, and possibly higher.

Reasons for proxy adviser negative recommendations and the importance of “pay-for-performance” Negative proxy adviser recommendations in the 2011 proxy have been triggered by a variety of pay policies and practices that the proxy advisers have labeled as “problematic” or “egregious,” notably, Internal Revenue Code Section 280G tax gross-up payments on golden parachute payments, [15] single-trigger change-in-control payments or broad (so-called “liberal”) change-in-control definitions, [16] “excessive” severance pay [17] and “excessive relocation payments,” particularly including those with home-loss make-whole payments and related income tax gross-ups. [18] But by far the single most prevalent and important basis for proxy adviser negative recommendations has been “pay-for-performance” voting policies and the advisers’ conclusions that there were “disconnects” between the company’s financial performance and its pay to its executive officers—most importantly, to its CEO.

At the beginning of the proxy season, ISS issued its 2011 voting guidelines, which included its 2011 pay-for-performance policy. [19] The guidelines state ISS’s general intention to examine the alignment of a CEO’s pay with company performance over time, from the shareholders’ perspective, with special focus on companies with continued underperformance when compared to their peers. In furtherance of this general policy, the ISS policy sets forth a two-pronged test. The first prong of the test evaluates a company’s financial performance based on its total shareholder return (TSR) in different periods relative to that of the other companies in its four-digit Global Industry Classification Standard (GICS) group. On this prong, ISS generally has found a performance problem that triggers application of the second prong if the company’s TSR was in the bottom half of its GICS category for both the one-year and three-year periods ended in the prior fiscal year (2010 for most companies). [20] The second prong of the test evaluates whether the total compensation paid to the company’s CEO (but only if he or she had served at least two consecutive years as the CEO) was aligned with the company’s TSR, with non-alignment (or a so-called “pay-for-performance disconnect”) if the CEO’s total direct compensation either increased, stayed the same, or was not significantly reduced from 2009 to 2010. As of June 23, 2011, of the 36 companies that failed to receive at least majority approval of their say on pay votes, 25 (or 69 percent) had ISS pay–for-performance disconnects. [21]

Glass Lewis’s pay-for-performance voting policy and its application are far from transparent and very difficult to assess. In the reports on company proxies we reviewed, Glass Lewis uniformly made a boilerplate statement that its assessments of pay for performance were based on a proprietary pay-for-performance model with 36 measurement points, with no further explanation of the 36 points or the criteria for how the points were selected or applied in any particular case. Glass Lewis followed this statement with a letter grade (often a C-minus or D) to reflect its conclusion as to whether the company’s pay was aligned with its performance. Interestingly, ISS and Glass Lewis have disagreed on pay-for-performance alignments and made contrary SOP vote recommendations. [22]

Unprecedented company responses to proxy adviser recommendations In the 2011 proxy season, many companies took unprecedented steps to challenge ISS and Glass Lewis negative vote recommendations by filing additional proxy materials prior to their shareholder meetings. Companies disputed ISS and/or Glass Lewis conclusions and analysis on a range of issues including their director elections [23] and equity plan recommendations; [24] however, most company disputes were on their pay-for-performance judgments. [25] Of the companies that have publicly responded to an ISS adverse recommendation, approximately 47 percent disputed ISS’s pay-for-performance assessment model. In addition, at least a handful of companies responded to negative recommendations by amending existing employment and equity agreements to induce ISS to change its negative recommendations. [26] Other companies, rather than amend outstanding agreements, made prospective pay-for-performance commitments to subject a certain percentage of shares underlying named executive officers’ equity awards in future years to performance vesting. [27]

Many of these public challenges have focused well-deserved attention on the factual errors and problems with some of the analytical methods used by ISS and Glass Lewis. These responses, and likely resulting questions and concerns from institutional investors who have been bombarded by criticisms of the proxy adviser methods and recommendations, appear to be having an impact. During a June 16, 2011 webcast, ISS executive director Patrick McGurn disclosed that ISS is currently reviewing its stock option valuation model due to the number of companies disputing the use of the model to derive more value to stock option grants; on June 20, ISS disclosed that it is rolling out a new compensation database for evaluating and benchmarking compensation, which, while aimed at a new corporate advisory service, could also foreshadow changes to its proxy voting policies. [28]

Shareholder derivative litigation Further adding to the adverse consequences of failing a SOP vote, law firms are filing shareholder derivative suits against directors and executive officers of companies with failed votes, and in some cases, against the compensation consulting firms that advised them. [29] There is no reason to believe that other companies with failed votes will not suffer the same consequences. These shareholder derivative suits face substantial hurdles, such as overcoming motions to dismiss based on the plaintiffs’ failure to make a demand on the company to bring the action or to prove that such a demand would be futile, or the requirement to prove that an independent compensation committee violated the business judgment rule in making its compensation decisions. However, these suits are distractions and generally will cause companies and their insurers to make settlement payments to the lawyers at relatively early stages in the proceedings to avoid the time and expense of trying them on the merits. Like the settlements in the derivative actions brought against boards of directors in the wave of stock option misdating cases several years ago, these settlements likely will also contain agreements by the companies to revise their compensation programs.

Lessons Learned

Here are our bottom-line assessments of the U.S. SOP experience in the 2011 proxy season, the lessons learned, and observations on their implications for future SOP votes.

Reflections on the 2011 Proxy Season

- Those who expected the 2011 U.S. SOP proxy season to be a non-event (like past seasons in the United Kingdom and other jurisdictions with histories of required SOP votes or recent seasons for companies subjected to mandatory SOP votes under the Troubled Asset Relief Program, or TARP) have been sorely disappointed. [30]

- While as of June 23, 2011, only approximately 2 percent of the season’s SOP votes have failed to obtain majority shareholder approval, ISS and Glass Lewis have been very active in recommending negative votes (e.g., for ISS, in approximately 13 percent of proxies reviewed and likely more for Glass Lewis), and many companies have had to struggle mightily to convince shareholders not to follow these negative recommendations, or have made concessions to the proxy advisers to change their recommendations.

- The biggest SOP story of the 2011 proxy season has been the importance of ISS and Glass Lewis recommendations and the vocal and compelling company responses they have engendered, especially on pay-for-performance issues.

- The 2011 proxy season has exposed fundamental problems with proxy advisers’ pay-for-performance policies and their application. Glass Lewis’ opaque pay-for-performance determinations are not helpful in providing companies or shareholders with guidance. ISS’s methods for determining poor performance (based on TSRs measured against GICS categories) and for determining CEO compensation (based on a one-year snapshot using grant date fair valuation methods for possible future grants) have substantial problems that should be fixed.

Impact on Future Proxy Seasons

- The victory of annual votes in the frequency vote elections means that many companies (and the vast majority of larger companies) will face SOP vote challenges annually, for at least the foreseeable future.

- Given the large volume of SOP votes and the difficulties companies encountered in engaging with shareholders on these matters in 2011 between the time the proxy advisers issued their reports and their shareholder meetings, companies have learned that they will need to begin to engage with their important shareholders much earlier in the year.

- Given that 2011 bonus, equity, and other compensation grants were determined by many companies prior to their 2011 SOP votes, it may not be easy for companies to react to failed or close votes, or negative voting recommendations, in a way that can be meaningfully reflected in their 2012 proxies and SOP votes. Accordingly, some companies may already find it too late to avoid negative proxy adviser recommendations for 2012, especially if their 2011 TSRs are below those of their peer groups.

- Given the relatively bright line between companies receiving less than 70 percent shareholder approval and those receiving more, companies that received less than 70 percent approval are likely to be as motivated as those that lost their votes to understand proxy adviser and shareholder concerns and to address any executive compensation issues with their shareholders.

- Even companies that won their SOP vote with more than 70 percent shareholder approval cannot rest easy going into the 2012 and future proxy seasons, given the crucial role played by ISS negative recommendations based on alleged payfor- performance disconnects. One or two years of poor TSR performance may jeopardize ISS positive recommendations.

- Pay-for-performance issues will only be more important next proxy season, especially if the SEC adopts pay-versus-performance rules under Section 953(a) of Dodd-Frank this year (as it is calendared to do). These rules will require U.S. public companies to disclose annually in their proxies the relationship between the executive compensation they “actually paid” and the financial performance of the company “taking into account any change in the value of the shares of stock and dividends of the issuer.” This disclosure may require graphic representation of the information.

- Based on problems with proxy adviser models and approaches on pay-for-performance issues, we hope that the SEC’s pay versus performance rules will recognize that:

- no one size metric for measuring performance can fit all companies in different and cyclical industries;

- relative financial performance should be evaluated using peer groups determined on the basis of labor and capital market competitors (not arbitrary GICS group or other categories);

- alignment of pay with performance should be measured over time and based on compensation actually paid, not on compensation that could be earned; and

- most importantly, companies should be able to determine how it makes the most sense for them, based on their individual facts and circumstances, to measure their performance and pay and to design pay plans which align the two.

- In addition to SEC pay-versus-performance rules, in 2011 the SEC is expected to issue rules on Dodd-Frank clawback policies and additional proxy disclosures, such as with respect to pay disparity, hedging policies, and the separation of CEO and chairman positions, as well as final rules on the independence of compensation committees and their advisers and on financial institution executive compensation.

- The 2011 proxy season and a complete postmortem of the proxy advisory services’ activities, especially in their analysis of pay-for-performance and their targeting some companies and not others, are also likely to fuel the movement seeking to have the SEC recognize the rule-making role of the proxy advisers and regulate them to require greater transparency, more rigor, and fewer conflicts in the way they conduct their businesses. [31]

- Most importantly, during the balance of 2011, public companies should review what happened to their SOP votes and the reasons of the outcome, evaluate whether and how their executive compensation has been aligned with company financial performance, and think about how they should explain this alignment to shareholders, in narrative or graphic form.

Endnotes

[1] Special thanks to Semler Brossy Consulting Group, LLC for sharing its statistics and findings on SOP recommendations and votes. See “2011 Say on Pay Results: Russell 3000” report by Semler Brossy Consulting Group, LLC, at [http://www.semlerbrossy.com/pages/htindex.php].

(go back)

[2] According to the SEC, approximately 5,800 U.S. public companies are subject to SOP vote requirements in the 2011 proxy season, and as of June 23, 2011, 2,193 Russell 3000 companies had held their 2011 meetings and reported their results.

(go back)

[3] The Dodd-Frank Wall Street Reform and Consumer Protection Act is available at [http://www.gpo.gov/fdsys/pkg/PLAW-111publ203/pdf/PLAW-111publ203.pdf].

(go back)

[4] Final SEC rule, “Shareholder Approval Of Executive Compensation And Golden Parachute Compensation,” available at [http://www.sec.gov/rules/final/2011/33-9178.pdf].

(go back)

[5] The Final Rule added a new Item 5.07(d) to Form 8-K requiring that, no later than 150 calendar days after the end of the shareholder meeting at which the frequency vote was required, but in no event later than 60 calendar years prior to the deadline for submission of shareholder proposals, by amendment to the most recent Form 8-K filed disclosing the results of the shareholder votes, the company must disclose the company’s decision in light of such vote as to how frequently the company will include a shareholder vote on the compensation of executives in its proxy materials “until the next required vote on the frequency of shareholder votes on the compensation of executives.” The SEC has informally advised that its interpretive position is that it was not the intent of the SEC to bind the company to its determination of the frequency of future SOP votes in Item 5.07(d). The SEC further informally advised that if the company decides to change the frequency of future SOP votes, an amendment to the Form 8-K is required to be filed detailing the change in the frequency determination and the reasons for the change.

(go back)

[6] According to the “2011 Say on Pay Results: Russell 3000” report by Semler Brossy Consulting Group, LLC.

(go back)

[7] Ibid.

(go back)

[8] Ibid.

(go back)

[9] Ibid.

(go back)

[10] The 16 are Kirby Corporation/K-Sea; Park Sterling Corporation/Community Capital Corporation; Bronco Drilling Company; SMART Modular Technologies; Lawson Software; GS Financial Corporation; Kendle International, Inc.; Brookline Bancorp, Inc.; Varian Semiconductor Equipment Associates; Centurylink, Inc.; Warner Music Group; Cephalon, Inc.; Level 3 Communications/Global Crossing; Nobel Learning Communities, Inc.; Kratos Defense & Security Solutions, Inc./ Integral Systems; and FPIC Insurance Group.

(go back)

[11] According to the “2011 Say on Pay Results: Russell 3000” report.

(go back)

[12] Ibid.

(go back)

[13] Ibid.

(go back)

[14] Ibid.

(go back)

[15] For example, Headwaters, Inc., Dr. Pepper Snapple Group, Dean Foods Co. and Walt Disney Company received ISS “against” recommendations due to 280G excess tax gross-ups.

(go back)

[16] For example, Ion Geophysical Corporation and Amedisys Inc. received ISS “against” recommendations due to “liberal” change in control definitions or modified single-trigger severance arrangements.

(go back)

[17] For example, Hewlett-Packard Company and Superior Energy Services received ISS “against” recommendations due to excessive severance arrangements to at least their CEOs.

(go back)

[18] For example, ENSCO Plc and Equifax Inc. received ISS “against” recommendations due to excessive relocation arrangements.

(go back)

[19] See ISS 2011 U.S. Policy Summary Guidelines, [http://www.issgovernance.com/files/ISS2011USPolicySummaryGuidelines20110127.pdf].

(go back)

[20] Notwithstanding the focus of the company performance prong on being below the GICS category median for both one- and three-year TSRs, some companies with either one- or three-year TSRs above median TSRs but below median in its five-year TSR received negative SOP recommendations from ISS based on a finding of a pay-for-performance disconnect.

(go back)

[21] According to the “2011 Say on Pay Results: Russell 3000” report.

(go back)

[22] For example, see Tyco International Ltd. (in which ISS recommended “against” SOP advisory vote and Glass Lewis recommended “for,” at [http://www.sec.gov/Archives/edgar/data/833444/000110465911008794/a11-6432_1defa14a.htm]; and Harsco Corporation (in which ISS recommended “against” SOP advisory vote and both Glass Lewis and Eagan-Jones recommended “for,” at [http://www.sec.gov/Archives/edgar/data/45876/000095012311034823/w82382e8vk.htm]); Textron, Inc. (in which Glass Lewis recommended “against” SOP advisory vote and ISS recommended “for,” at [http://sec.gov/Archives/edgar/data/217346/000095012311033179/b85925defa14a.htm]).

(go back)

[23] For example, see Chesapeake Energy Corp. at [http://www.sec.gov/Archives/edgar/data/895126/000119312511153383/ddefa14a.htm], Sempra Energy at [http://www.sec.gov/Archives/edgar/data/1032208/000119312511120750/ddefa14a.htm] and Bank of America Corporation at [http://www.sec.gov/ Archives/edgar/data/70858/000119312511115328/ddefa14a.htm].

(go back)

[24] For example, see The Standard Register Company at [http://www.sec.gov/Archives/edgar/data/93456/000090631811000053/defa14a041511.htm], The Gap, Inc. at [http://www.sec.gov/Archives/edgar/data/39911/000119312511106213/ddefa14a.htm] and Aon Corporation at [http://www.sec.gov/Archives/edgar/data/315293/000110465911025506/a11-11537_1defa14a.htm].

(go back)

[25] For example, see Safeway Inc. at [http://www.sec.gov/Archives/edgar/data/86144/000119312511133787/ddefa14a.htm] (disputing ISS’s pay-forperformance analysis, including stock option valuation); Masimo Corporation at [http://www.sec.gov/Archives/edgar/data/937556/000119312511147210/ddefa14a.htm] (disputing ISS’s pay-for-performance analysis, including proxy adviser peer group determinations, stock option valuation and factual errors) and Healthcare Realty Trust Inc. at [http://www.sec.gov/Archives/edgar/data/899749/000095012311044718/g27102defa14a.htm] (disputing ISS’s pay-for-performance analysis, including proxy adviser peer group determinations and factual errors) and J.C. Penney Company Inc. at [http://www.sec.gov/Archives/edgar/data/1166126/000116612611000027/defa14a050311.htm] (disputing ISS’s pay-for-performance analysis, including proxy adviser peer group determinations and stock option valuation).

(go back)

[26] For example, The Walt Disney Company at [http://sec.gov/Archives/edgar/data/1001039/000119312511070351/d8k.htm]; General Electric Company at [http://sec.gov/Archives/edgar/data/40545/000119312511101003/ddefa14a.htm]; Lockheed Martin Corporation at [http://www.sec.gov/Archives/edgar/data/936468/000119312511106383/ddefa14a.htm]; and Alcoa Inc. at [http://www.sec.gov/Archives/edgar/data/4281/000119312511117085/d8k.htm].

(go back)

[27] For example, Gannett Co., Inc. has made a prospective commitment to subject at least 50 percent of the equity awards (based on number of shares) granted annually to the company’s named executive officers will be performance-based, at [http://www.sec.gov/Archives/edgar/data/39899/000119312511091277/d8k.htm].

(go back)

[28] See BNA: Proxy Adviser’s Reports Questioned; ISS to Review Option Value Method.

(go back)

[29] Shareholder derivative lawsuits stemming from 2011 failed SOP votes have already been filed against the boards of directors and others at Jacobs Engineering Group Inc., Beazer Homes USA, Inc., Umpqua Holdings Corp., Hercules Offshore, Inc., Bank of New York Mellon Corporation, and Cincinnati Bell Inc.

(go back)

[30] None of the approximately 240 financial institution required to hold SOP votes under TARP in 2009 and/or 2010 received less than majority support for its pay and The Economist has said that the “no” votes cast in U.S. SOP votes this year may be more than the “no “votes cast in the rest of the world since Great Britain introduced SOP in 2002. [http://www.economist.com/node/18836886?frsc=dg%7Ca]

(go back)

[31] For a thorough discussion of the role of proxy advisers, the pressures on their business model and the bases for their possible regulation, see Latham & Watkins LLP’s recent Corporate Governance Commentary “Proxy Advisory Business: Apotheosis or Apogee?” at [http://www.lw.com/upload/pubContent/_pdf/pub4042_1.pdf].

(go back)