Print

PrintThe following post comes to us from Richard Bennett, Chairman of GovernanceMetrics International, and is based on a GMI Ratings study by Kimberly Gladman, Agnes Grunfeld and Michelle Lamb, available here.

Executive Summary

In theory, the most significant corporate governance check and balance between public company shareowners and the company is the ability to elect corporate directors. In reality, that control mechanism is complicated and often compromised for a host of reasons. Nonetheless, there has been an increased focus on director elections in the past few years. This study examines what happens when shareowners withhold a majority of votes from a director nominee.

The significance of majority withhold votes for corporate directors is the subject of some debate in the governance and business community. It is sometimes argued that majority withhold votes are of little import because they are infrequent, rarely lead to director resignations, and typically come in response not to corporate-specific failings, but to violations of perceived best practice (such as the adoption of a poison pill without shareholder approval). At the same time, however, some academic literature has suggested that high levels of withhold votes may be an indicator of generally negative market perceptions of a company. [1]

This current report contributes to this discussion through an examination of majority withhold votes for 175 director nominees at Russell 3000 companies between July 1, 2009 and June 30, 2012. On the one hand, the study confirms that withhold votes occur at a small percentage of companies, and lead to director resignations in only a small proportion of cases. However, we also find that only about half of majority withhold votes are related to best practice issues, and nearly a fifth co-occur with other serious evidence of shareholder dissatisfaction. Our study also examines corporate disclosures regarding board response to majority withhold votes. We find that companies with majority or plurality plus resignation standards for director elections are more likely to make informative disclosures than those with plurality standards. [2] An analysis of withhold votes in connection to financial performance was inconclusive, but suggests directions for further study of this relationship.

Key Findings

Most directors who receive majority withhold votes continue to serve. Only 5% of the majority withhold votes in our study led directly to director removal.

Majority or plurality plus resignation election standards increase the probability, but do not guarantee, that “unelected directors” will step down. Only 8% of the directors who received majority withhold votes at companies with plurality plus resignation standards stepped down shortly after the annual meeting, and only half of directors at companies with majority standards did so.

Majority withhold votes are not just about “best practices.” Only about half of majority withhold votes in the study period were attributable to generic violations of perceived best practice such as failed attendance, directors serving on too many boards (“overboarding”), related party transactions, or poison pill adoption without shareholder approval. The remaining votes appear to have been driven mostly by shareholder concern with issues specific to the companies in question.

Majority withhold votes are often part of a larger pattern of shareholder concern. Nearly one-fifth (18%) of majority withhold votes occurred at companies where there was evidence of shareholder dissatisfaction not only with the director in question but with the board or company as a whole (as discerned through patterns of high withhold votes for multiple directors, votes against management on proxy ballot items, and proxy contests).

Majority withhold votes are more common at smaller-cap companies. Over 80% of majority withhold votes in our sample occurred at Russell 2000 companies (which made up two-thirds of the study sample).

Most majority withhold votes occur at companies without majority election standards. Ninety-one percent of majority withhold votes in our sample occurred at companies with plurality standards for director voting. This is at least partially a reflection of the fact that smaller US companies are less likely than their larger-cap peers to have adopted either majority or plurality plus resignation election standards. Another possible explanation is that a company which has adopted a majority voting standard is likely to have better governance practices overall and/or be more attuned to its shareowners’ desires, enabling it to head off majority withhold votes.

Majority or plurality plus resignation election standards improve disclosure about companies’ processes for evaluating and responding to majority withhold votes. Almost nine out of ten (87%) companies receiving majority withhold votes made no disclosure regarding their boards’ processes for responding to them. However, all companies with majority or plurality plus resignation election standards made some disclosure about their response to the votes. Even among this group, however, 37.5% of the companies did not state what they believed the reason for the withhold votes to be.

I. Incidence of Majority Withhold Votes

i. Frequency, Company Size, and Director Election Standards

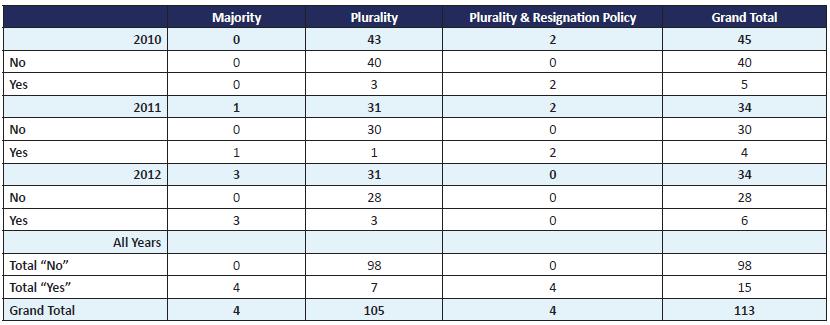

GMI Ratings’ 2010 proxy-year-end snapshot recorded majority withhold votes in uncontested elections for 79 directors at 45 companies in the Russell 3000. (Note that our methodology produces slightly different numbers than those cited by other researchers because we base our analysis on data pulled shortly before the index’s reconstitution date. For details on our process, see the Appendix.) At all but two of these companies, plurality voting standards were in place, allowing directors to be elected even with a minority of votes in their favor. Our 2011 proxy-year-end data includes majority withhold votes for 51 directors at 34 companies, all but two of which had plurality voting standards; and our 2012 proxy-year-end data includes majority withhold votes for 45 directors at 34 companies, all but three of which had plurality election standards.

The great majority of withhold votes occurred at smaller-cap companies (Russell 2000 rather than Russell 1000). In the three years combined, only 20 of the 113 (17.7%) companies concerned were members of the Russell 1000 index.

Our data confirms several conclusions that have been discussed by other governance commentators regarding the incidence of majority withhold votes for directors. First of all, these votes occur quite infrequently, affecting less than 2% of the Russell 3000 companies. Second, most majority withhold votes occur at companies with smaller market capitalization, perhaps in part because those firms are less sophisticated than larger ones about avoiding actions that will result in withhold votes under many institutional investors’ proxy voting guidelines. Third, a disproportionate majority of these votes occur at companies with plurality voting standards (this observation is related to the preceding one, since majority voting has been more widely adopted among larger firms than smaller ones). As a result, most directors receiving majority withhold votes are nevertheless re-elected to their boards.

ii. Reasons for Majority Withhold Votes

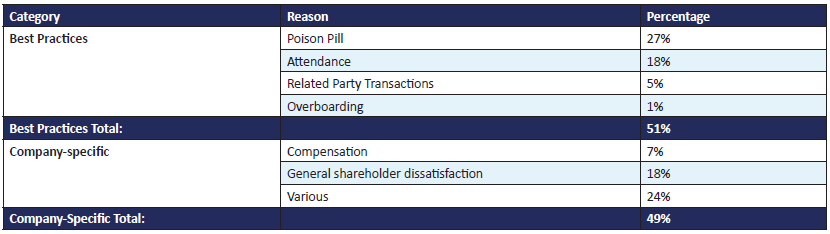

While is not always possible to determine the reasons for majority withhold votes, over seventy-five percent of the votes in our sample can be attributed to six main factors. About half the votes can be attributed to violations of what are considered to be best practices in governance, including poison pill approval without shareholder approval, failed attendance, related party transactions (RPTs), and overboarding. The other half of the votes appear to be expressions of shareholder discontent about director performance on the oversight of more particular, company-specific issues. Indeed, the current study’s methodology may overstate somewhat the number of votes that are related to perceived best practice. This is because if a director in our sample had failed attendance, approved a poison pill without shareholder approval, or had major RPTs or overboarding concerns, we put the director in the best practice category, regardless of whether there were also signs of broad-based shareholder dissatisfaction with the board as a whole.

a. Best Practice Reasons

Poison pill adoption: The adoption or extension of a poison pill without shareholder approval triggers withhold vote recommendations for the entire board from some proxy advisors and investors, and was the largest single cause of majority withhold votes in our sample. This issue appears to have been the reason for the votes withheld from about 48 directors’ elections in the time period under study, or about 27% of the group of 175 director votes.

Attendance: In all years, failed attendance appears to have been a common reason for majority withhold votes. Thirty-one of the 175 majority withhold votes, or about 18%, were for directors who had attended less than 75% of their board and committee meetings in the preceding year.

Related party transactions and overboarding: For eleven other majority withhold votes, the primary factor appears to have been related party transactions with the company or service on a high number of boards. This represents about 6% of the sample.

Taken together, these best practice reasons represent 51% of the majority withhold votes for individual directors in the sample.

b. Company-Specific Concerns

Compensation: At a few companies, withhold votes directed at the chair (or occasionally all the members) of the compensation committee suggest that shareholder concerns with compensation policy appear to be driving the withhold votes. This accounts for 13 votes, or about 7% of the total.

General shareholder dissatisfaction: Finally, at another group of companies, the withhold votes seem to be more than a judgment on one director or one aspect of company policy. Instead, they appear to be part of a much broader story of shareholder dissatisfaction with the company, which can be discerned through patterns of votes against management on proxy ballot items, proxy contests, and/or of high (but not necessarily majority) withhold votes for other directors. (As a basis for comparison, it is helpful to know that the average level of withhold votes for all directors at companies in the sample was about 5%.) This “general shareholder dissatisfaction” group accounts for 32 directors receiving majority withhold votes, or about 18% of the total.

In some cases, the companies in this category were undergoing changes in leadership and strategic direction. For example:

- Advanced Analogic, which saw a majority of votes withheld from its chair in 2010, also saw withhold votes above 30% for all its directors in 2009 and 2010, faced a proxy contest in 2011, and was acquired by Skyworks Solutions in 2012.

- At clothing retailer Christopher & Banks, which had a majority withhold vote for one of its directors in 2011, three other directors received withhold votes of about 20% that year, and over 20% of shareholders voted no on Say on Pay. After the 2011 meeting, the company announced the closure of 100 stores and reduced its field workforce by 14%. In 2012, the company changed its CEO and CFO and added several new directors to the board. Although its Say on Pay results improved in 2012 (with over 95% support), five of the company’s directors received over 30% withhold votes, and in July 2012, the company announced it had received a takeover offer.

- Chesapeake Energy, which saw two directors receive majority withhold votes in 2012 following a high-profile scandal involving loans to its CEO, underwent extensive governance restructuring following its annual meeting. The company separated its chair and CEO roles, appointed four new independent directors representing major shareholders, and is taking the necessary steps to declassify the board.

Other companies in this group appear to have ongoing governance difficulties that have not yet been resolved as of this writing (in July 2012). In some cases, shareholders appear to be expressing broad-based discontent with the entire board. For example:

- At Barnes Group, where two directors received majority withhold votes in 2012, the two other directors up for election that year received about 45% withhold votes; the directors elected to the classified board in 2011 had all received more than a quarter of votes withheld; and a 2012 shareholder proposal requesting the appointment of an independent chair received over 45% support.

- Ferro Corporation had its entire 2011 director slate receive above 15% withholds (with two receiving majority withholds and another receiving 49%). The 2012 nominees fared no better, garnering withholds of 16%, 46%, and 56%.

- At Healthcare Services Group, where there were two majority withholds each in 2010 and 2011, all directors standing for election in 2010, 2011, and 2012 received at least 25% of votes withheld (with the single exception in 2012 of one newly appointed director).

- At Hospitality Properties Trust, all directors currently on the board received at least 35% withhold votes at their last election to the company’s classified board (with one receiving a majority withhold in 2012).

- At Swift Energy, all nominees to the classified board received at least 30% withhold votes in 2009, 2010, and 2011, with three of the seven directors receiving majority withholds.

- At Taser International, which saw one majority withhold vote in each of 2011 and 2012, all board nominees in both of those years have received at least 40% votes withheld.

- At Ultratech, two directors received majority withholds in 2010, and the entire board received at least 20% withholds in 2011.

- At Vornado, all directors standing for election in both 2011 and 2012 received majority withholds; also in 2012, a shareholder proposal requesting the adoption of a majority voting standard received majority support (for the sixth consecutive year), as did a proposal on board declassification (for the third consecutive year).

At a number of other companies where shareholder discontent appears to be ongoing, multiple directors received high withhold votes, even if the entire board did not. For example:

- At Anaren, Inc., where one director received a majority withhold vote at the company’s most recent election (in November 2011), three others, including the chair/CEO, also received about 45% of votes withheld.

- CIBER, Inc., which had a majority withhold vote in 2010, also had withhold votes above 15% for other directors in earlier and later years, went through a CEO transition in 2010, and had relatively low levels of support in its first two years of Say on Pay votes (83% in 2011 and 75% in 2012).

- At CIRCOR, the compensation committee chair received a majority withhold vote in 2010; the CEO (who also served as chair) received over 30% withhold votes in 2011; and the company’s lead director (who is a partner at a law firm used by the company) received over 15% withhold votes in 2012 (after receiving a majority withhold vote at his last election in 2009).

- At Morgan’s Hotel Group, which saw a majority withhold vote for its compensation chair in 2011, the 2012 pay plan and advisory vote passed only narrowly; three directors (none of whom served on the compensation committee) also received over 30% withhold votes in 2012.

- Three of Interline’s eight directors received majority withhold votes at their most recent elections to the company’s staggered board, in 2009 or 2010.

c. Other Reasons for Majority Withhold Votes

Finally, the remaining 24% of majority withhold votes may be attributable to unusual circumstances, such as the opposition of dominant owners to particular directors; the presence of former CEOs on the board or key committees; or the performance of a committee on which the director serves (e.g., a withhold vote for an audit committee member at a company reporting ineffective internal controls under section 404 of the Sarbanes Oxley Act). In other cases, it was not possible to speculate as to the reason for the vote on the basis of available data.

II. Director Departures Following Majority Withhold Votes

As has been discussed by other researchers, most of the directors receiving majority withhold votes in 2010-2012 continued to serve in their positions. As noted above, this is largely (but not only) because most of them were elected under their firms’ plurality vote standards.

i. 2010 Departures

Of the 79 directors receiving majority withhold votes in 2010, only six (7.6%) had stepped down from their positions by the time of the company’s 2011 annual meeting (a seventh director had died). Two of those who resigned their posts did so shortly after the 2010 vote, while four others remained on their boards for much longer, resigning only around the time of the next annual meeting. All but one of the resigning directors (Edward Walker of Herley Industries) served at companies with plurality voting standards, and two of the six had failed attendance standards. In addition, there were two directors who, after receiving majority withhold votes in 2010, submitted resignations which were rejected. One was Peter Davis at Nabi Pharmaceuticals, which had a plurality plus resignation election standard; the other was Sven Wehrwein at Vital Images, Inc., which had a plurality standard.

ii. 2011 Departures

Of the 51 directors who received majority withhold votes in 2011, seven (13.7%) had left their positions by the time of the company’s next annual meeting. Three directors who failed attendance standards stepped down within a few months of the vote, despite their companies’ plurality voting standards. One other director also left shortly after the vote (this was Roger Laverty, then-CEO of Farmer Bros., who may have lost the support of the family which controls 40% of the company’s voting power). Three other directors (two at IRIS International, which has a plurality plus resignation standard, and one at Cardinal Financial, which has a plurality standard) served until the next annual meeting, but did not stand for re-election. Interestingly, the one company with a majority election standard that saw a majority withhold vote in 2011, Annaly Capital Management, decided to retain the director who had failed attendance standards on the grounds that the absences were justifiable.

iii. 2012 Departures

Of the 45 directors who received majority withhold votes in our 2012 sample, only three (6.7%) resigned shortly after the annual meeting. Two of these were at companies with majority standards; Marc E. Kalton at Isramco and Ricardo Salgado at NYSE Euronext. The third director was Richard K. Davidson at Chesapeake Energy, which had a plurality standard prior to the vote; the company adopted majority voting via a management proposal at the 2012 annual meeting but the new standard will not be effective until January 1, 2013. (The second majority-withhold vote director at Chesapeake, V. Burns Hargis, remained on the board pending his completion of a review of the company’s loans to the CEO, but the company but the company stated it would revisit his resignation at the conclusion of that project.) A fourth director in the 2012 data set, David Wilemon (who received a majority withhold vote at plurality-standard Anaren), resigned several months after the meeting in accordance with the company’s mandatory retirement policy. (Mr.Wilemon’s resignation brings the departure total for 2012 to 8.9%. This statistic is not directly comparable to the 2010 and 2011 departure data, as those measured departures until the following annual meeting. Obviously, that information will not be available until mid-2013.) All of the other directors in the 2012 sample remained in place as of July 2012, including Bruce Gans at Hospitality Properties Trust, which has a majority election standard.

iv. Summary

In sum, only nine directors in our study, or about 5%, stepped down shortly after the annual meetings at which they received a majority of withhold votes, apparently in response to the message from shareholders. Another seven directors who received majority withhold votes in 2010 and 2011 continued to serve until the company’s next annual meeting, but did not stand for re-election at that point.

III. Disclosures of Board Processes Regarding Director Retention or Removal

i. Overview

In general, companies have made fairly minimal disclosures regarding their processes for responding to majority withhold votes and deciding whether to seat directors receiving them. As might be expected, the level of disclosure varies with the companies’ director election standards. As shown in the table below, the great majority of companies with plurality standards merely disclosed the votes as required in 8-K filings and stated that the directors were elected. Sometimes they also reiterated that their director election standards required a plurality, but they did not comment on the fact that a majority of votes were withheld for one or more directors. A handful of plurality-standard companies (just under 7%) did make substantive comments in their 8-K filings regarding the majority withhold votes. As one might expect, all of the companies with plurality-plus or majority standards commented on the majority withhold votes in these filings.

Taken together, the disclosures from all of these companies provide some information about the processes by which boards make their decisions about whether to retain a director. However, since most withhold votes occurred at plurality standard companies, for almost nine-tenths (88%) of the companies in the full sample, we have no disclosure about how they viewed the withhold votes.

The table below breaks down the sample of companies that saw at least one majority withhold vote into categories, indicating how many with each director election standard provided substantive disclosure regarding the company’s response to the vote.

ii. 2010 Disclosures

In 2010, two companies in our sample had plurality plus resignation standards, and the remainder had plurality standards; the two plurality & resignation companies provided disclosure regarding their response to withhold votes, as did three of the plurality companies. At one of the plurality plus resignation companies, Herley Industries, an 8-K filing issued by the company indicates that the affected director, Edward K. Walker, submitted his resignation after the March 23, 2010 vote. The remaining directors met on March 31st and:

in light of the results of the shareholders vote at the Annual Meeting, the Board, following the deliberation process provided for in the By-Laws, determined unanimously to accept Admiral Walker’s resignation and to terminate the consulting arrangement between the Company and Admiral Walker.

The relevant section of the company’s by-laws provides that after the resignation of a director who has received less than a majority of support, “the remaining directors shall, upon a process managed by the Nominating, Governance and Ethics Committee and excluding the director nominee in question, within 45 days of receiving such resignation letter, determine whether to accept such resignation.” Presumably, when the board met in this case, they were of the opinion that the director’s consulting arrangement—according to the 2010 proxy, a $75,000 payment for “services relating to corporate governance and ethics”—was the reason for the high withhold votes.

The second company, Nabi Biopharmaceuticals, came to a different conclusion when one of its directors, Peter B. Davis, received a majority withhold vote. As the filing states:

Promptly following the Annual Meeting, Mr. Davis tendered his resignation as required by the Company’s Corporate Governance Principles. In accordance with those Principles, the Nominating and Governance Committee promptly met in person to consider whether to recommend acceptance or rejection of Mr. Davis’ tendered resignation to the full Board of Directors, which is charged under the Principles with making that determination. The Nominating and Governance Committee recommended to the Board of Directors that it reject Mr. Davis’ tendered resignation. The Board of Directors met in person promptly after the meeting of the Nominating and Governance Committee to consider its recommendation, and review the facts and circumstances relevant to the stockholder vote. Considering the best interests of the Company and its stockholders and other factors, the Board of Directors rejected Mr. Davis’ resignation, noting Mr. Davis’ significant contributions to the Company, the Board of Directors, the Audit Committee, and various committees of the Board in connection with the Company’s strategic alternative as well as his financial background and expertise. Mr. Davis did not take part in either the Nominating and Governance Committee or the Board’s deliberations.

This disclosure provides no information regarding what the Board believes to have been the reason for the majority withhold vote. (One possibility is the board’s July 2009 decision to extend the term of the company’s poison pill, which was likely a factor in the entire board’s receipt of over 27% withhold votes. However, it is unclear why Mr. Davis should have received an even lower level of support than his fellow directors.)

Three companies that received majority withhold votes in 2010 and had plurality election standards commented on the withhold votes in the 8-Ks where the votes were reported. One company, Michael Baker, noted that it believed the large number of withhold votes received for all of its nominees was a result of RiskMetrics’ withhold-vote recommendations, issued in response to the company’s extension of its poison pill without shareholder approval. The company did not go beyond this explanation of the votes to discuss the company’s view of the poison pill extension. Another firm, First Merchants, did discuss both a possible reason for the votes and the company’s reason for disagreeing with it. As the 8-K states:

ISS/RiskMetrics, a proxy advisory firm, recommended withholding votes for Mr. Schalliol because, under their policies, they conclude he is an “affiliated outside director” by virtue of his being “of counsel” to the law firm of Baker & Daniels, which does legal work for the Company. However, the Company concludes he is an “independent” director under the Rules of both NASDAQ and the SEC.

Finally, a third plurality-standard company, Vital Images, described in great detail the reasons it believed its Audit Committee chair received a majority withhold vote, but should nonetheless remain in his position. The company’s disclosure shows an unusual level of transparency regarding board process, as well as thoughtful consideration of voting results. Shortly after the annual meeting, the filing states:

[The board] held a special meeting on May 12, 2010, to review the voting. Even though all directors were duly elected under the Company’s plurality voting rules, the Board discussed the results for each individual director. After the discussion, Mr. Wehrwein offered to submit his resignation to the Board in recognition of the fact that, of the votes he received from shareholders voting at the Annual Meeting, 49.68% were “for” votes and 50.32% were “withhold” votes. The offering of such a resignation is not required by any applicable statute or rule, nor by the Company’s bylaws or any Board or Company policies. After a full discussion during which the Board determined that the resignation of Mr. Wehrwein would be detrimental to the best interests of the Company and its shareholders, the Board, with Mr. Wehrwein abstaining, unanimously voted not to accept Mr. Wehrwein’s offer of resignation. Mr. Wehrwein withdrew his offer and agreed to continue his service on the Board for this term. In addition, Mr. Wehrwein asked the Governance Committee, and the full Board agreed, to look into the reasons for the large number of withhold votes, share their findings with the Board and make any appropriate recommendations.

Vital Images’ board did then conduct this investigation into the reason for the votes, and concluded:

[The number of withhold votes] were substantially due to an analysis by a third party corporate governance firm that the time commitment required by his service on multiple public company audit committees may preclude Mr. Wehrwein from dedicating the time and attention necessary to fulfill his duties as the Chair of the Board’s Audit Committee despite his experience and training. The Board respectfully disagrees with this view and maintains that, instead of being a detriment, Mr. Wehrwein’s service on the audit committees of several other emerging and small capitalization medical and technology companies provides him with rich experiences and perspectives regarding accounting and securities law matters.

This assertion of a director’s valuable experience and knowledge is a fairly standard company response to concerns about overboarding. Vital Images’ board goes on, however, to make two other points to substantiate the claim that this concern is, in this particular case, unfounded. First, they note that Mr. Wehrwein is a full-time director, which suggests that the directorship limits recommended for active executives may not be applicable to him. Mr. Wehrwein, the filing notes, has:

only one professional obligation—his service on various boards of directors. As a result of devoting 100% of his time and attention to his board responsibilities, he has a broad exposure to auditing, public accounting, and corporate governance issues, and routinely brings best practices from one company to another.

Furthermore, the filing notes that the director:

lives in the Twin Cities, the home of all of the companies where he is a board member. This close proximity facilitates regular informal meetings with members of management and all but eliminates scheduling issues for him—the result of which is that he has missed only one formal meeting, board or committee or otherwise, across all his various board positions, in the last five years, belying the concern expressed about his ability to devote the time and attention necessary to fulfill his duties as the Chair of the Board’s Audit Committee.

iii. 2011 Disclosures

In 2011, one company in our sample had a majority standard, two had plurality plus resignation, and the remainder had plurality election standards. All three companies with either majority or plurality plus resignation standards provided disclosure about their response to the votes, as did one of the plurality-standard companies.

The one company with a majority standard, Annaly Capital, decided to retain a director who had received a majority of withhold votes due to failed attendance standards. The company explains in an amended 8-K filing (issued after the first report of the voting results) that the director in question had a generally good attendance record over many years; that his absences in 2010 were unusual, justifiable, and unlikely to be repeated; and that he was a valuable board member the company wished to retain. As the filing states:

[T]he Board considered a number of factors to determine if requesting Mr. Green’s resignation was in the best interests of the Company and its shareholders. Among other things, the Board considered Mr. Green’s unique qualifications, including, among other things, his significant experience as a chief executive of a real estate company, his diverse and significant background in the real estate industry and his legal expertise; his past and expected future contributions to the Company; his significant exposure to the Company’s business and industry through length of service on the Board; his historical participation and contributions at Board meetings and communications and commitment regarding future attendance and scheduling; his commitment to the success of the Company; the overall composition of the Board; and the likely reason why Mr. Green received more “Against” votes than “For” votes. Additionally, the Board considered that prior to 2010, in each and every year since his election to the Board at the Company’s inception in January 1997, Mr. Green attended at least 75% of the regularly scheduled Board meetings and Committee meetings for each Committee on which he served. The Board also determined that there were reasonable justifications for Mr. Green’s absences from the meetings in 2010. Ultimately, after consideration of all of these factors, the members of the Board determined that Mr. Green has and continues to participate actively as a director, that he has made and continues to make substantial contributions to the Company and that it would not be in the best interests of the Company and its shareholders to request Mr. Green’s resignation. Since Mr. Green’s resignation was not requested, Mr. Green will continue to serve on the Company’s Board until our next annual meeting of shareholders, at which time the Board expects he will be re-nominated for reelection as director.

While this decision may sound reasonable, it may also seem, on its face, to conflict with a majority director election standard. However, the common-sense notion of majority voting—if a director does not receive a majority of votes, he or she is removed—is not necessarily what is reflected in some companies’ bylaws. For example, Annaly’s bylaws provide that directors will be elected by a majority, but state that if a director fails to get majority support:

and no successor has been elected … such director shall hold over and continue to manage the business and affairs of the corporation until his or her successor is elected and qualified unless such director resigns and such resignation is accepted by the Board of Directors. The Board of Directors shall and [sic] publicly disclose (by a press release, a filing with the Securities and Exchange Commission or other broadly disseminated means of communication) whether it has requested and accepted the resignation of a director who shall have failed to receive the required vote to be elected in accordance with the terms of this Section 7 and, if applicable, its decision regarding any tendered resignation and the rationale behind the decision.

In other words, although Annaly has a majority standard, it is a quite weak one: directors need not resign if they do not receive a majority, and even if they do submit a resignation, the board may not accept it.

IRIS International was one of two companies with a plurality plus resignation standard that had directors who received majority withhold votes in our 2011 sample. At IRIS, an 8-K filed shortly after the vote stated that all the directors had received majority withhold votes and tendered their resignations, but that the company believed the reason for this to be that ISS had recommended withhold votes because the board adopted a poison pill without shareholder approval. The company noted that:

ISS did not disclose any other basis for its recommendation of a “withhold” vote for all directors, nor did ISS recommend against any other proposal submitted to our stockholders for a vote at the annual meeting, including with respect to the advisory vote on approval of the compensation of our executive officers. This is the first time that ISS has recommended a “withhold” vote for any of our director nominees, and this is the first time that any of our director nominees has received a greater number of votes “withheld” from his or her election than votes “for” such election. The Board concluded from this information that the ISS recommendation was the primary reason for the vote results. The Board does not believe that the entire Board should be removed from office for exercising its authority to adopt a shareholder rights plan without obtaining or agreeing to seek shareholder approval of the plan, and the Board therefore rejected the resignation offers tendered by all directors.

The IRIS bylaws, interestingly, actually have a fairly detailed process for consideration of such resignations by directors receiving majority withheld votes. As the bylaws explain:

The Corporate Governance and Nominating Committee of the Board shall consider the resignation offer and recommend to the Board whether to accept the resignation. The Board will act on the Corporate Governance and Nominating Committee’s recommendation within 90 days following certification of the stockholder vote. Thereafter, the Board will promptly disclose its decision whether to accept the director’s resignation offer (and the reasons for rejecting the resignation offer, if applicable) on a Current Report on Form 8-K. Any director who tenders his or her resignation pursuant to this provision shall not participate in the Corporate Governance and Nominating Committee’s recommendation or the Board’s action regarding whether to accept the resignation offer. However, if each member of the Corporate Governance and Nominating Committee received a Majority Withheld Vote at the same election, then the independent directors who did not receive a Majority Withheld Vote shall appoint a committee amongst themselves to consider the resignation offers and recommend to the Board whether to accept them. However, if the only directors who did not receive a Majority Withheld Vote in the same election constitute three or fewer directors, all directors may participate in the action regarding whether to accept the resignation offers.

In 2011, the last-mentioned situation occurred—the entire board received majority withholds, and all directors were therefore permitted to participate in the decision not to accept one another’s resignations. However, later in 2011, the directors chose to accelerate the expiration of the poison pill whose adoption had caused the withhold votes, effectively terminating it by December.

The other plurality & resignation company in the 2011 sample is HSN, where the company disclosed that the director in question tendered his resignation but the board unanimously rejected it, after considering both his contributions to the board and “the reasons why Mr. Blatt received more ‘withheld’ votes than ‘for’ votes.” However, the company does not state what it believed those reasons to be.

Finally, one company in the 2011 sample provided disclosure regarding its response to a majority-withhold vote despite having a plurality election standard. That company, Synovis, stated that it believed its former CEO received a majority of votes withheld from her election to the board as a “result of her having joined the compensation and governance committees of the board of directors effective November 1, 2010, after having served as our Chief Executive Officer from July 1997 to January 2007.” The filing goes on to state:

After considering the vote of our shareholders at the Annual Meeting, Ms. Larson voluntarily offered to step down from our compensation and governance committees. Our board of directors intends to honor Ms. Larson’s request, but has asked Ms. Larson to remain a member of our compensation and governance committees until the board names a replacement. Replacements are expected to be named before the next meetings of either committee are held.

iv. 2012 Disclosures

In the 2012 sample, all three majority-standard companies commented on the majority withhold votes received by their directors. One company, Isramco, stated simply that it had “determined to reduce the size of the board to six members rather than to add a director to replace [Marc Kalton,] a director who was not re-elected at the Annual Meeting of Shareholders.” Another, NYSE Euronext, stated that the director in question had resigned and that the board had accepted his resignation. A press release attached to the 8-K in which this information was disclosed implied that the vote was due to the director’s having failed attendance standards, noting that “we completely understand the business priorities and his leadership role in the Portuguese financial community which require his full attention.”

The final company with a majority standard to receive a majority withhold vote in 2012, Hospitality Properties Trust, took a different approach. Its filing notes that director Bruce Gans did not receive sufficient support to be elected, and consequently resigned. The filing goes on to state that the company’s board had:

determined that the insufficient vote for Dr. Gans appeared not be directed at any personal failings of Dr. Gans, but rather to be the result of a policy position taken by the Board of Trustees in opposition to the shareholder proposal by the California Public Employee Pension Plan, or CalPERS.

The CalPERS shareholder proposal (requesting board declassification) had been submitted and received majority support every year since 2009, and it is indeed possible that the company’s lack of responsiveness to it provoked shareholders to vote against the board. All of the company’s directors received at least 35% withhold votes at their last election to the company’s classified board in 2010, 2011, or 2012, with Adam D. Portnoy (the only director other than Dr. Gans up for election in 2012) receiving close to a majority of withhold votes (47%).

However, after having understood the vote in this fashion, Hospitality Properties’ board “requested that Dr. Gans accept appointment to the vacancy created by his resignation,” and he promptly did so. Thus, the company was able to violate the spirit of the majority voting policy by retaining the director, while honoring the letter of it (since the director did indeed resign, before his reappointment).

Three plurality-standard companies made some disclosure regarding the majority withhold votes received by their directors in 2012. One, Costar Group, noted in the 8-K disclosing the votes simply that “[t]he Board notes and is taking into consideration the votes withheld” from the director in question. The other, United Stationers, attributed the majority vote against one of their directors to his having attended only 63% of meetings in the previous year, which triggered a withhold vote recommendation from some proxy voting firms. The company stated, however, that the director in question joined the board midyear, had made his fellow directors aware of previous commitments that would limit his availability that year, and was not expected to have continuing attendance problems in the future.

Chesapeake Energy, where two directors received majority withhold votes in the midst of a broader governance scandal, conducted a major board restructuring following its annual meeting. In the same filing that announced its appointment of new directors representing activist shareholders Southern Asset Management (SAM) and Carl Icahn, the company explained that:

Mr. Davidson and V. Burns Hargis submitted their resignations when they did not receive support of a majority of the shares voted. The Board accepted Mr. Davidson’s resignation, but given Mr. Hargis’ current role as Chairman of the Audit Committee, and reflecting input from SAM and Mr. Icahn, the Board has declined to accept his resignation, at this time, to permit completion of the previously announced review of the financing arrangements between Mr. McClendon (and the entities through which he participates in the Founder Well Participation Program) and any third party that has had or may have a relationship with the company in any capacity. Mr. Hargis will continue to lead the review, but is not expected to remain Chairman of the Audit Committee. Upon completion of the review, the Board will revisit his resignation.

IV. Governance Changes Following Majority Withhold Votes

Moving beyond the question of director removal or retention, companies have shown mixed levels of responsiveness to the policy and governance concerns expressed in director withhold votes.

i. Poison Pills

As noted above, IRIS International chose to terminate the poison pill whose adoption without shareholder approval had led to its entire board receiving majority withhold votes in 2011. Other companies that had experienced majority withholds for this same reason did not, however, take similar steps to accelerate their pills.

ii. Compensation

Most companies where majority withhold votes were related to compensation policy did make changes to their compensation policies in the following year. (Note that all of the companies where compensation appears to have been a major factor had plurality standards, so the votes did not affect the election of directors.) In some cases, the changes were significant. One good example is The Pantry, which after high withhold votes in 2010 increased the percentage of its equity grants that are performance-vesting, lengthened the evaluation period for its long-term performance award, and made its annual incentive plan more challenging. The company also updated its peer group, increased its ownership and stock retention guidelines, implemented a clawback policy, and instituted a formal review process for compensation-related risk. Shareholders responded with radically reduced withhold-vote levels in 2011, as well as strongly favorable Say on Pay results.

Stewart Information Services, too, began a significant overhaul of its compensation program following the majority withholds received by its entire compensation committee in 2010 and by the retired chair of its compensation committee in 2011. It hired a new compensation consultant, engaged with shareholders and proxy advisory firms on pay issues, and adjusted pay targets to the median of peer group total compensation. (In addition, Stewart also replaced its CEO and separated its chair and CEO roles.) Another positive example is CIRCOR, which like The Pantry made more of its equity awards dependent on performance after its compensation committee chair received a majority withhold vote in 2010. CIRCOR also eliminated tax gross-ups and some other perks such as home buyouts, and implemented clawback provisions. (However, it retained high change-in-control severance payments for the CEO, at a level worth 19 times his salary.)

At other companies, the changes made to compensation practices following majority withhold votes for compensation committee chairs were more structural. For example, at Gibraltar Industries, where the compensation chair received only minority support in 2010, the company has reformed change-in-control agreements to include double trigger payment provisions; somewhat strengthened stock ownership policies; and a commitment to avoid future employment agreements including tax gross-ups. Perhaps reflecting shareholders’ view that pay policy has continued to raise concerns, Say on Pay support at the company fell by about 25% from 2011 to 2012, from an initially strong showing of 95% to just over 70%.

Another company that has made primarily structural changes to its compensation program is Premiere Global, where two compensation committee directors (including the committee chair) garnered majority withhold votes in 2010. At Premiere, tax gross-ups were eliminated and clawbacks and share ownership guidelines were adopted; the company also hired a new compensation consultant. However, only one-third of a recent mega-grant of stock options to the CEO was contingent on performance, salary and bonus remain high for the company’s size, and past time-vesting equity grants have continued to benefit executives despite poor current performance. The company received a majority-against vote on Say on Pay in 2011, and withhold votes above 20% for all directors at its 2011 election. However, as financial performance improved in 2012, so did approval rates for directors and Say on Pay.

Finally, another firm where compensation concerns appear to continue is United Online, Inc. At this company, which has a staggered board, two of its compensation committee members received majority withholds in 2010; in 2012, the third member of its compensation committee received nearly a quarter of votes withheld, and a majority of shareholders voted no on Say on Pay (in 2011, Say on Pay had passed with a relatively low 79% of votes).

iii. Other Governance Changes

As noted in Section III iii above, Synovis removed a former CEO from her seats on two key committees after it determined that these positions were the likely reason for her lack of support from shareholders.

In addition, the companies discussed above in Section I ii b (those whose majority withhold votes we attributed to “general shareholder dissatisfaction”) went through a number of governance and strategic changes following the votes. In those cases, the majority withhold votes were one of several expressions of shareholder concern about the company’s direction, and these changes were likely made not solely in response to the votes, but also out of the board’s perception of the larger problems facing the firm.

Moreover, five companies changed their director election standards (but did not specify whether this decision bore any relationship to the withhold votes). Hersha Hospitality Trust, HMS Holdings Corp, Gibraltar Industries, and Navigant Consulting all adopted a majority voting standard within a year of receiving the majority withhold votes, and Stanley Black & Decker changed its standard to plurality plus resignation in the same time frame.

Finally, many companies where one or more directors received majority withhold votes do not appear to have made any significant governance changes in response to them.

V. Investment Performance and Withhold Votes

The current study also examined the relationship between majority withhold votes and investment performance. Any analysis of this kind must come with several caveats. As is well known, many complex factors influence equity returns. In addition, the number of companies receiving majority withhold votes is not large, and caution is always advised when drawing conclusions on the basis of a small sample. Furthermore, for a variety of reasons, complete performance data could not be obtained for all of the companies in the sample; our findings are therefore best viewed as provisional, and as the possible basis for further study. However, we do note that of the companies for which we have data, more companies underperformed than outperformed their peer group in the year following the majority withhold votes. We conducted our performance study by comparing each company’s total shareholder return to the median return for a group of peer companies of similar size and industry characteristics, both one year prior to the majority withhold vote and (except for companies in the 2012 sample) in the following year. (For more details on our methodology, see the Appendix.)

i. Entire Sample Analysis

In the year preceding the majority withhold votes, just over half of the subject companies for which we had data underperformed the average return for their peer group, and just under half outperformed. Moreover, the companies’ median relative underperformance in the prior year (calculated as a company’s return minus the median return) was a mere -0.6%. It would not be surprising to find that companies that receive majority withhold votes have underperformed their peers, since poor financial performance may be one factor leading shareholders to withhold their votes from directors. However, the empirical evidence on this point does not support a conclusion that poor stock market performance leads to withhold votes.

Findings for the year following the votes are somewhat more robust. Of the 66 companies for which we have data, 58% underperformed their peer-group medians, and the median relative performance (calculated in the same fashion described above) was -5.5%. If borne out by an analysis with a larger sample size, this finding would suggest that majority withhold votes can be a leading indicator of worsening relative performance.

ii. Subcategories of Vote Reason

a. General Shareholder Dissatisfaction

We analyzed separately the companies whose majority withhold votes we identified as being related to broad-based general shareholder dissatisfaction (as evidenced by patterns of high withhold votes for other directors, votes against management on proxy ballot items, and proxy contests) or being clearly related to compensation concerns. The results were consistent with what was found for the entire universe. In the year preceding the votes, exactly half of the companies in this category for which we have data underperformed their peer group medians, and the median relative performance in that period was -1.1%. In the year following the votes, 12 of the 19 companies for which we have data (63%) underperformed the peer group, with median relative performance of -12.3%.

b. Best Practices

We also analyzed separately the companies whose withhold votes were clearly attributable to the best practice issues of poison pill approval, attendance, related party transactions, and overboarding. Fifty-seven percent of these companies underperformed the peer group median in the year preceding the votes, and the median relative performance was -4.3%. In the year following the votes, 51% of the companies underperformed, with a median relative return of -0.4%.

c. Other

Finally, we looked at the companies whose votes we could not attribute to one of the six categories above. (Because no obvious best practice reasons could be identified for these votes, however, we assume they relate to shareholder concerns regarding an issue specific to the company.) Only a third of the 21 companies for which we had data in this category underperformed the median in the year preceding the votes, and the median relative return was 9.3%; however, 8 of the 13 (61%) companies in this category for which we had following-year data underperformed, with a median relative return of -4.9%.

d. Summary

In sum, for all categories of votes, more companies for which we had data underperformed than outperformed peers in the year following the votes. On the face of it, this would suggest that majority withhold votes may be a leading indicator of worsening investment performance relative to industry and market-cap peers. However, the small number of companies included in our calculations precludes a strong conclusion on this point. More thorough research should be conducted on this question, examining a larger number of withhold votes over a longer period of time, and accounting in some way for companies which are acquired or otherwise cease to exist in the period following the votes.

VI. Conclusion

The findings in this report have implications for companies, investors, and researchers. First, companies and their boards should recognize that majority withhold votes are not necessarily the result of “check the box” standard governance practices or proxy advisors’ recommendations, and may well be part of a pattern of shareholder communication expressing serious concerns about the company’s direction. Indeed, even withhold votes that fall short of a majority, but are significantly above the universe average (which has been about 5% in recent history), may warrant reflection on the part of boards of directors. Secondly, investors who wish to make boards more responsive to shareholder voting would do well to continue advocating the adoption of majority voting, even for smaller firms, since companies with majority standards are more likely than others to remove directors who receive minority support. Companies with anything other than a plurality election standard are also far more likely to provide disclosure regarding their response to majority withhold votes. Therefore, investor pressure to move away from plurality voting may also improve transparency on this topic. Finally, researchers may wish to explore in greater depth the initial findings presented here regarding withhold votes as a potential leading indicator of peer group-relative underperformance. One way to do this could be to expand the time frame of the study, and to include companies with high levels of withhold votes that fall short of a majority.

VII. Appendix: Methodology

The historical data snapshots used in this report were created each July, after the end of the US proxy season, and include director voting results for annual meetings held since June of the previous year. Because they reflect Russell 3000 membership shortly before the midsummer reconstitution of that index, these snapshots may omit some majority withhold votes (for example, if the votes occurred at a Russell 3000 company that held its annual meeting in March and was removed from the index in May). In addition, the snapshot omits companies which, for a variety of reasons, filed more than one proxy statement during the relevant June-July period, or for which a proxy statement covering that period was not available.

The sample includes 113 instances in which a company received majority withhold votes for at least one of its directors between June 2009 and July 2012. As fourteen companies appear in the data set in at least two years, it includes only 98 individual companies. Because some companies received majority withhold votes for more than one director in a given year, the sample includes 175 majority withhold votes.

Our performance study measured peer-relative total shareholder returns, including dividends, for each company over a one-year period preceding the proxy season in which at least one of its directors received a majority withhold vote. Performance was also measured in this way for the one-year period following the proxy season for votes occurring in the 2010 and 2011 proxy years. For companies with proxies issued in March through May of each year (the majority of the sample), the measurement period was from April 30th to April 30th. For 11 companies with fall annual meeting dates, the measurement period was from November 30th to November 30th. Calculations were not made for companies for which share-price information in a given period was unavailable from our data provider, FactSet. As a result of this constraint, our performance study for the 45 companies in the 2010 proxy year sample included previous-year and following-year calculations for 38 companies. For the 34 companies in the 2011 proxy year data set, we were able to include previous-year calculations for 31 companies but following-year calculations for only 28 companies. Finally, we were able to make previous-year calculations for all of the 34 companies in our 2012 proxy year sample, but no calculations were made for the forward-year period.

Peer group median performance was calculated for the peer group excluding the subject company. In a few cases, peer companies for which performance data was lacking in a given period were also excluded from calculations for that period. However, company peer groups for all calculations included at least eight peers. The peer groups were created by first consulting the list of peers named by the company in the Compensation Discussion and Analysis section of its most recent proxy statement. Only companies on the list which were in the same industry as the company, and with a roughly similar market cap (typically ranging from approximately one half to double the company’s market capitalization), were included in the peer groups for our calculations. In cases where the resulting list of companies was smaller than eight, additional companies meeting these industry and market capitalization criteria were added. In one case (Fred’s, Inc.) sufficient peer group data could not be obtained, and the company was omitted from the performance study.

Performance relative to peer group was calculated by subtracting the peer group median return from the return of the subject company. This method was chosen because it provides the most precise information about investor wealth. If company A’s annual relative return calculated by this method is -1%, a holding in that company is 1% less valuable at the end of the year than a holding in a company with the median peer-group return. However, readers should note that this method does not explain the scale of a company’s under- or outperformance, which can vary depending on the peer group median return. (For example, many investors would view 1% underperformance with much less concern if it occurred during a strong market rally, as opposed to a time when returns are flat).

Endnotes

[1] See, for example, Fischer, Paul E., Gramlich, Jeffrey D., Miller, Brian P. and White, Hal D. Investor Perceptions of Board Performance: Evidence from Uncontested Director Elections (May 12, 2009). Available at SSRN: http://ssrn.com/abstract=928843 or http://dx.doi.org/10.2139/ssrn.928843

[2] US companies adopt one of three standards for director elections: plurality, plurality plus resignation, and majority.

- 1. Under a plurality election standard, the director receiving the highest number of votes for a given seat is elected. At companies with this standard, a director who ran unopposed (as most do) could theoretically be elected with a single vote, since he or she would still have received more votes for the seat than anyone else.

- 2. Under a plurality plus resignation standard, directors in uncontested elections are also elected by a plurality of votes. However, directors who do not receive a majority of votes must submit their resignations for the board’s consideration.

- 3. Under a majority standard, directors running unopposed must receive the support of a majority of votes cast in order to be elected.