Print

PrintJoseph Bachelder is special counsel in the Tax, Employee Benefits & Private Clients practice group at McCarter & English, LLP. This post is based on an article by Mr. Bachelder, with assistance from Andy Tsang, which first appeared in the New York Law Journal.

“Then you should say what you mean,” the March Hare went on.

“I do,” Alice hastily replied; “at least—at least I mean what I say—that’s the same thing, you know.”

“Not the same thing a bit!” said the Hatter. “You might just as well say that ‘I see what I eat’ is the same thing as ‘I eat what I see’!”

Alice in Wonderland, Lewis Carroll (1865)

The Preamble to SEC Disclosure Regulations (2006) [1] states: “We believe that plain English principles should apply to the disclosure requirements that we are adopting, so disclosure provided in response to those requirements is easier to read and understand. Clearer, more concise presentation of executive and director compensation…can facilitate more informed investing and voting decisions in the face of complex information about these important areas.”

To which the Mad Hatter might have responded: “You can assume plain English conveys clear thinking, but what happens if plain English is not fed by clear thinking?”

Long-Term Incentive Values

To understand the value of long-term incentive (LTI) awards to senior executives as reported in proxy statements of major U.S. corporations is to embark on a journey that is closer to chasing after Alice in Wonderland than providing clarity as to real values of those awards. What is the problem? What can be done about it? That is the attention of this column.

LTI awards represent, for most CEOs, the largest value in their compensation packages. These awards can be in various forms including:

- Stock Awards (including Stock Unit Awards)

- Options Awards

- Long-Term Cash Incentive Awards

Views on Valuation

One View: Summary Compensation Table Value. The Summary Compensation Table (SCT) in the executive compensation section of the proxy statement sets out values of LTI awards for each of the fiscal years being reported. These include awards to the CEO and certain other senior executives of the issuer. The SCT contains dollar amounts for each type of reportable award that has been made. Following is a brief summary of how those values are shown in the SCT.

(a) Stock Awards: [2] The dollar value shown is the market value of shares on the date of grant. [3]

(b) Option Awards: [4] The dollar value shown is based on the “Black-Scholes” or similar method for valuing options on the date of grant. [5]

(c) Long-Term Cash Incentive Awards: The amount paid out or otherwise “earned,” during the fiscal year, or years (the measurement period), being reported. For this purpose, “earned” means that the executive is entitled to receive the cash, except for timing of actual payment.

If this were the only exercise, the shareholder would add up these amounts and see what is the value of the LTI awards being reported for the CEO and other senior executives. But the story is not over.

Most of the SCT values are not the values that will be realized. Most equity awards, for example, are conditional on continued employment and/or achievement of performance targets. If termination of employment occurs before vesting, forfeiture may occur depending on the circumstances of termination. Decline in stock value may wipe out any gain in stock option awards.

Increasing numbers of issuers are presenting, in the executive compensation section of the proxy statement, a discussion (sometimes including a supplemental chart) of LTI values that are different from the values shown in the SCT. Following is a discussion of two of these alternative methods of valuation: “Realized Value” and “Realizable Value.” [6]

A Second View: “Realized Value.” This method reports LTI award values on the basis of “actual realization” of the award by the executive during the fiscal year, or years, being reported. “Actual realization” of an award occurs in the year, or years, being reported, irrespective of the year the award was granted. [7] Following is a brief summary of how this works according to type of award.

(a) Stock Awards: The dollar value shown is the market value on the date of vesting in the fiscal year, or years (measurement period), being reported. (The value of shares not yet vested at the end of the period being reported is not shown.)

(b) Option Awards: The dollar value shown is for options exercised in the fiscal year, or years (measurement period), being reported. [8]

(c) Long-Term Cash Incentive Awards: The amount shown is the amount paid out or otherwise earned for this purpose during the fiscal year, or years, being reported. As noted above in connection with SCT value, “earned” means that the executive is entitled to receive it, except for timing of actual payment.

Table 1 contains the LTI values for the CEO of The Boeing Company, first as shown in the SCT, and then as shown in a supplemental table displaying “Realized Value.” (The supplemental table contains realized values for both 2011 and 2010, but the following table in this column is limited to the year 2011.)

A Third View: “Realizable Value.” This method reports what might be described as a reasonable expectation of value to be realized by the executive in the future from awards granted during the measurement period (that is, the fiscal year, or years, being reported). Following is a brief summary of how the “Realizable Value” method works according to type of award.

(a) Stock Awards: For awards vesting during the measurement period (the fiscal year, or years, being reported), the value shown is as of the date of vesting. For awards not yet vested as of the end of the measurement period, the value shown is the value as of the end of the period. [9]

(b) Option Awards: The dollar value shown is based on the applicable option valuation method (for some of the issuers displaying “Realizable Value,” this is the Black-Scholes or similar method; others use the intrinsic value method (that is, option “spread” on the applicable date)). [10] In the case of options still unvested at the end of the year, or years (measurement period), being reported, this would mean the value on the last day of such period. For those vesting during the year, it would mean the value determined as of the date of vesting. [11]

(c) Long-Term Cash Incentive Awards. Under the “Realizable Value” method the value of long-term cash incentive awards made during the measurement period (fiscal year, or years, being reported) is determined as follows: the value for awards not yet vested at the end of the measurement period is their target value. For awards earned during the measurement period, the amount actually paid out is used. The target value of long-term cash incentive awards not yet earned out at the end of the period being reported may be subject to adjustment based on the probability of attaining target.

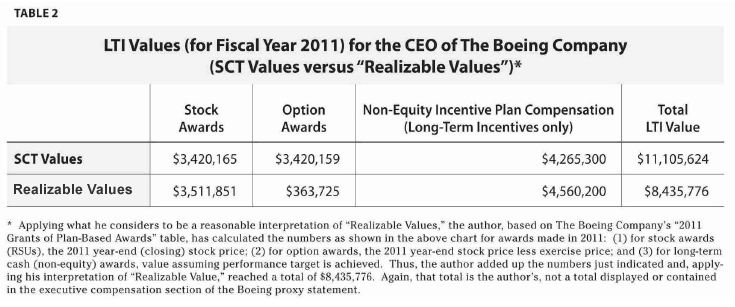

The second chart, Table 2, compares the SCT values (already set out in the chart shown earlier in the column) for the fiscal year 2011 for The Boeing Company and the “Realizable Values” for the fiscal year 2011, based on the author’s own interpretation of “Realizable Value.” It must be emphasized that Boeing does not present either “Realizable Value” for individual awards or a “Total Realizable Value” for its LTIs in its proxy statement; this is the author’s own calculation, in an effort to show the difference between the SCT value method and the “Realizable Value” method, the third of the three methods discussed in this column.

Confusing Exchange

The say-on-pay rules pursuant to Dodd-Frank Section 951, enacted in 2010, [12] and conclusions of proxy advisors such as Institutional Shareholder Services Inc. (ISS) in advising shareholders on how to cast their say-on-pay votes have been catalysts in a “warfare” over long-term award values. Whether one considers this to be a benefit to shareholders is not the point for discussion here. The point is that a noisy, confusing exchange of valuations between issuers, on the one hand, and proxy advisors like ISS, on the other hand, is going on.

ISS bases its quantitative analysis of each issuer’s pay programs and practices, to a significant degree, on the SCT value method for LTIs. It uses this method for the issuer it is analyzing and for the peer companies to which it is comparing that issuer. In contrast, issuers with competing perspectives on the value of the awards they are making use methodologies such as the “Realized Value” method and the “Realizable Value” method to respond to ISS and other proxy advisors in supplementary charts and/or narratives in proxy statements. This exercise falls far short of producing clarity for the reader.

Expecting Clarity?

Is it realistic to expect clarity in this Alice in Wonderland world of LTI values? Three points:

- As long as the battles for say-on-pay votes rage, including the pronouncements of proxy advisors expressing their own views on, and calculations of, appropriate LTI values and issuers justifying the LTI actions they are taking, there is likely to be more “sturm und drang” than illumination.

- Apart from the battles on say-on-pay votes and issuers contesting proxy advisors’ points of view on values, is it a mistake to expect that the disclosure and discussion of LTI pay can occur in an arena of clear thinking and plain English? Perhaps the real purpose of discussion is not clarity of communication but, simply, to hold issuers’ feet to the fire, making sure that they make a real effort to justify what they do. Illumination of, and understanding by, shareholders of what is going on becomes secondary.

- More fundamentally, can we really imagine clear presentation of LTI pay values given the inherent complexities of the subject matter? Can we really expect to find a simple, concise explanation of value where there are so many different ways of looking at such value? Perhaps, like Alice, we are trapped inside our own “creativity” in designing and valuing LTI pay.

Reducing the Confusion

Following are two suggestions as to how greater clarity (albeit, not less “noise”) might be achieved.

- The SEC might adopt specific definitions of what it considers to be the appropriate meanings of “Realized Value” and “Realizable Value,” which would become approved methodologies for alternative reporting by issuers in the narrative part of the executive compensation disclosure section of the proxy statement.

- Proxy advisors should coordinate with the SEC in reaching common definitions of “Realized Value” and “Realizable Value.” In its most recent report, ISS does recognize the possible use of the “Realizable Value” method, but limits its use to its own qualitative (secondary) level of analysis and further limits its use to large cap companies (that is, at present, the S&P 500 companies). [13] Broader and more basic use of such alternative methods of valuation should be recognized by ISS.

If the above suggestions were implemented, shareholders would be able to decide which valuation method for a particular issuer made the most sense to them and be better able to reach a judgment on whether the values of LTI awards at that issuer are appropriate.

Endnotes

[1] The quoted language appears in the preamble to the Executive Compensation and Related Person Disclosure Regulations as published in 71 Fed. Reg. 53158, 53208 (Sept. 8, 2006).

(go back)

[2] Item 402(a)(6)(i) of Reg. S-K provides that “[t]he term stock means instruments such as common stock, restricted stock, restricted stock units, phantom stock, phantom stock units, common stock equivalent units or any similar instruments that do not have option-like features, and the term option means instruments such as stock options, stock appreciation rights and similar instruments with option-like features.”

(go back)

[3] The value shown for stock awards that are subject to adjustment based on achievement of performance targets should be adjusted to reflect the possibility of achieving the targets. Also, if an amount greater than target value may be achieved based on exceeding targets then that too should be taken into account in setting value under the regulations.

(go back)

[4] Item 402(a)(6)(i) of Reg. S-K, quoted in footnote 2 above, contains a definition of “option” as used in the Summary Compensation Table. Also, it should be noted that value adjustments as noted in footnote 3 in connection with stock awards should also be taken into account with regard to option awards.

(go back)

[5] For discussion of the “Black-Scholes” method, including modifications permitted, see FASB ASC Topic 718. See also Item 402(c)(2)(vi) of Reg. S-K.

(go back)

[6] In presenting the discussion of the two methods of valuation, the author has reviewed statements by issuers in proxy statements and numerous commentaries. There is not complete agreement on the meanings to be given these terms, and the meaning given to each in this column is the author’s best effort to reflect a consensus among issuers and others on such meaning.

(go back)

[7] “Realized Value” differs from “Realizable Value,” among other things, in that “Realized Value,” as noted in the text, includes the value of grants realized even if made prior to the fiscal year, or years (measurement period), being reported. “Realizable Value” only includes grants made during the fiscal year, or years (measurement period), being reported.

(go back)

[8] The author is aware of one company, Hewlett-Packard Company, that defines “Realized Value” for option awards as the spread on the vesting date of all options vesting during the fiscal period being reported. Hewlett-Packard bases “Realized Value” for options on vesting and not on exercise.

(go back)

[9] As noted above in the discussion of SCT value, value of performance shares and performancebased options that are based on targets to be achieved after the end of the measurement period should be adjusted based on probability of the attainment of (or, if applicable, exceeding) such targets.

(go back)

[10] For adjustments to value in the case of performance-based options, see discussions in footnotes 4 and 9 above.

(go back)

[11] In determining “Realizable Value,” some proxy advisors and issuers consider that options not exercised during the year, or years, being reported, should be valued as of the last day of such measurement period. For those exercised during such period, the value would be determined as of the date of exercise.

(go back)

[12] Dodd-Frank Wall Street Reform and Consumer Protection Act, Pub. L. No. 111-203, §951, 124 Stat. 1376, 1899 (2010).

(go back)

[13] See “U.S. Corporate Governance Policy—2013 Updates” (ISS, Nov. 16, 2012, at pp. 13-15).

(go back)