Print

PrintMatteo Tonello is managing director of corporate leadership at The Conference Board. This post relates to an issue of The Conference Board’s Director Notes series authored by Lawrence J. Trautman; the full publication, including footnotes, is available here.

Achieving optimal board composition and succession planning requires an articulated and clearly communicated enterprise strategy. The ideal mix of director skills and experience depends on a number of company-specific factors. This report provides a matrix that nominating committees and boards can use to help define their needs and to provoke discussion about how to improve company-specific corporate governance.

How do you build the best board for your organization? What attributes and skills are required by law and what mix of experiences and talents will give you the best corporate governance? What commonly required director attributes are a must for each board and how do you customize and fine-tune your search to achieve a high-performing board? Optimal board composition—that is, achieving the best mix of director skills and experience—depends on many company-specific variables. Some of the most important of these include, but are not limited to: (1) stage of company development, (2) the extent to which international markets are mission critical to the company’s future (in which case nominees should have a detailed understanding of target culture, markets and business risk); (3) unique technology dependence; and (4) the need for access to financial and capital markets.

The discussion that follows is intended to serve as a road-map for the entrepreneur faced with recruiting a board for the first time or for the nominating committee and board in the process of recruiting and selecting new directors.

Duty of Care and Board Composition

Each board member has a legal duty to be diligently responsible to the shareholders for the governance of the corporation, including the productive functioning of the board. Corporations are created by state-granted charters, their governance dictated by state law, with corporate directors responsible for managing the affairs of the corporation. Delaware courts state the business judgment rule is a “presumption that in making a business decision the directors of a corporation acted on an informed basis, in good faith, and in the honest belief that the action taken was in the best interests of the company.” Under Delaware law, directors owe their corporation and shareholders fiduciary duties of care and loyalty.

Duty of care It is every director’s legal duty of care to exercise a careful, diligent approach to the recruitment and selection of new directors. Professors Lyman P.Q. Johnson and Mark Sides note that duty of care specifies the manner in which directors must discharge their legal responsibilities…. includ[ing] appointing members to committees and discharging committee assignments, including the important audit, compensation, and nominating committees….

Duty of good faith In order for a director to have the protection of the business judgment rule against a claim for breach of fiduciary duty, a director must be able to demonstrate that she acted in “good faith.” The board of directors of a Delaware corporation is charged with the legal responsibility to manage its business for the benefit of the corporation and its shareholders with “due care, good faith, and loyalty.”

Duty of care and committee succession planning Much as a board plan for the succession of its CEO, it must also plan for a governance and nominating committee that includes succession planning for all standing committee members and chairmanships. According to the 2012 Spencer Stuart Board Index, 71 percent of S&P 500 respondents report having succession plans. Many boards have a mandatory retirement policy based on age or length of service, in which “73 percent of all S&P 500 boards—up from 55 percent in 2002—set a mandatory retirement age for directors, yet many retain the discretion to make exceptions to the rule.” This helps provide for an orderly transition of committee duties and recruitment of talent to be groomed for eventual succession needs.

Core Personal Attributes, Qualities, and Skills Required of Every Director

Each board has the same fundamental needs for director talent The board is responsible for approving nominees for election as directors. To assist in this task, the board will designate a standing committee, usually called the nominating and governance (“N&G”) committee, which is responsible for reviewing and recommending nominees to the board. The N&G committee should consist solely of independent directors as defined by the rules of the New York Stock Exchange (NYSE) and the board’s corporate governance guidelines. A written charter for every standing committee should be adopted by the full board.

Desired personal attributes As a fundamental starting point for director recruitment and selection, directors should ask, “What human qualities are desired for every board member?” All boards should agree on a clear statement of desired personal attributes for all directors to guide to the nominating and governance committee as they search for director candidates. Each candidate should possess the following necessary core personal attributes: high standards of ethical behavior, availability, outstanding achievement in the individual’s personal and professional life, strong interpersonal and communication skills, independence, and soundness of judgment.

Board Composition: One Size Does Not Fit All

One factor that influences optimal board composition is vastly different for companies at varying stages in their lifecycle. For example, a venture stage technology company attempting to bring a single technology product to market may have profoundly different board needs than a mature, international consumer products company like Proctor & Gamble. In the case of a single-product, venture stage technology company, intimate understanding of the value proposition to the customer is paramount. Next in importance might be an understanding of appropriate marketing channels and critical access to capital markets necessary to fuel accelerated growth (production, ramp-up, etc.). These skills are vastly different from those necessary to govern global production, direct marketing, or establish financing relationships that have developed and matured over many years at companies like Proctor & Gamble, Coca Cola, General Electric, or Pfizer.

Venture capital-sponsored enterprises Venture-stage enterprises with institutional investor backing typically have a board composed entirely of representatives from its major investors, plus the entrepreneur. Venture capitalists often bring more than just money. Seasoned and skilled venture capitalists might bring valuable relationships and enlightened early-stage corporate governance, a combination that can help create substantial value. An entity preparing for public ownership may need to recruit seasoned directors to populate standing committees (sometimes venture capital investors who are directors want to stay, sometimes not).

Company size Microcap public companies (roughly $300 million weighted average market capitalization) often find it difficult to attract experienced director talent to meet committee structure needs. Nanocap entities (market capitalization of $50 million or less) may have even more limited resources making it difficult to attract experienced director talent. Small cap companies ($1.2 billion weighted average market cap) generally have sufficient financial resources available to attract skilled directors. Mid cap and large cap issuers (more than $1.2 billion in weighted average market cap) often fill directorship positions with those who have met the challenges of running a large, complex enterprise elsewhere, typically former or sitting CEOs of major corporations.

Board Committee Structure: the Basics

Corporate boards usually consist of the following minimal standing committees: (1) audit, (2) compensation, (3) executive, and (4) governance and nominating. Sometimes, committee names might differ slightly (i.e., the compensation committee may be known as the compensation and benefits committee or the governance and nominating committee may be referred to as the nominating committee). Other standing committees reported in The Korn/Ferry Market Cap 100 (KFMC 100) report include: charitable contributions, compliance, corporate development, credit, dividend, energy delivery, equity, finance, generation oversight, human resources, infrastructure, public issues and contributions, real estate, reserves, risk management, science/ technology, special programs, and strategy. Businesses with unique governance issues may have additional committees to address specific concerns. For example, utility NRG has a nuclear oversight committee and subcommittee, and oil and gas producers may have a reserve committee.

The duties and responsibilities of each of these core committees are specified in the charters drafted and adopted for each standing committee. Typical responsibilities for each of these standing committees and a discussion of relevant nominee considerations are discussed below.

The audit committee The board’s audit committee will be a standing committee established to comply with the requirements of Section 3(a)(58)(A) of the Securities Exchange Act of 1934, as amended. All members of the audit committee must be independent under the rules of the NYSE and the board’s corporate governance guidelines. The audit committee of any public corporation is generally responsible for:

- Appointing, compensating, retaining, and overseeing the company’s independent certified public accounting firm (CPAs);

- Creating and periodically reviewing the company’s whistleblower policy;

- Discussing the company’s audited financial statements with management and the independent public accounting firm, including a discussion with the firm regarding the matters required to be reviewed under applicable legal or regulatory requirements;

- Reviewing:

- compliance of management and operating personnel with the company’s code of business conduct, including the company’s conflict of interest policy

- adequacy of the company’s internal accounting controls and other factors affecting the integrity of its financial reports with management and with the independent certified public accounting firm

- news releases regarding annual and interim financial results and discussing with management any related earnings guidance that may be provided to analysts and rating agencies before they are released

- changes, if any, in major accounting policies of the company

- the annual report of the company’s CPAs related to quality control

- policy regarding investments and financial derivative products

- annual reports to the Securities and Exchange Commission, including the financial statements and the “Management’s Discussion and Analysis” portion of those reports, and recommending appropriate action to the board

- audit plans

- compliance and ethics program

- nonemployee-related insurance programs

- relationships with the independent public accounting firm

- risk assessment and risk management policies

- trends in accounting policy changes that are relevant to the company and

- policy regarding investment and financial derivative products.

The board must determine that all members of the audit committee are financially literate and have financial management expertise, to the extent the board has interpreted such qualifications are necessary in its business judgment. In addition, the board must designate an individual as the “financial expert” for the audit committee as defined in the Securities Exchange Act of 1934, as amended.

The compensation committee Spencer Stuart’s discussion of the top governance issues for 2012 notes that “executive compensation continues to be the top issue, ranked first by 72 percent of survey respondents.” The following list, adapted from Amgen’s Compensation and Management Development Committee Charter, provides an example of typical responsibilities of compensation committees:

- Reviewing and approving company goals and objectives relevant to CEO compensation;

- Evaluating the CEO’s performance in light of those goals and objectives;

- Setting the compensation of the CEO and other executive officers;

- Overseeing administration of employee benefit plans; and

- Taking action as appropriate regarding the institution and termination of, revisions in and actions under employee benefit plans that are not required to be approved by the board.

The compensation committee might make recommendations to the board regarding:

- Institution and termination of, revisions in and actions under employee benefit plans that (i) increase benefits only for officers of the company or disproportionately increase benefits for officers of the company more than other employees of the company, (ii) require or permit the issuance of the company’s stock or (iii) the board must approve;

- Reservation of company stock for use as awards of grants under plans or as contributions or sales to any trustee of any employee benefit plan; and

- Purchase of company stock in connection with employee benefit plans.

In performing its functions, the committee is supported by the company’s human resources organization. The compensation committee needs the authority to retain any advisors it deems appropriate to carry out its responsibilities. The committee might ask the compensation consultant to advise it directly on executive compensation philosophy, strategies, pay levels, decision-making processes, and other matters within the scope of the committee’s charter. The compensation committee might instruct the consultant to assist the company’s human resources organization in its support of the committee in these matters with such items as peer-group assessment, analysis of the executive compensation market, and compensation recommendations. The comp committee usually considers it important that its compensation consultant’s objectivity not be compromised by other business engagements with the company or its management. Usually, the compensation committee considers executive compensation in a multistep process that involves the review of market information, performance data, and possible compensation levels over several meetings, leading to the annual determinations. Before setting executive compensation, the committee reviews the total compensation and benefits of the executive officers and considers the impact that their retirement, or termination under various other scenarios, would have on their compensation and benefits.

The executive committee The principal function of an executive committee is typically to perform and exercise the powers of the board to direct the business and affairs of the company between meetings of the board. In some organizations, composition of this committee might consist of the chairman of the board and chairpersons of all standing committees. The ability for members to be available on short notice (physical proximity/availability) is an important consideration for membership on this committee.

The governance and nominating committee The governance and nominating committee is generally responsible for making recommendations to the board regarding:

- Development and revision of corporate governance principles;

- Size, composition and functioning of the board and board committees;

- Candidates to fill board positions;

- Nominees to be designated for election as directors;

- Compensation of board members;

- Organization and responsibilities of board committees;

- Succession planning by the company;

- Potential conflicts of interest involving a board member raised under the conflict of interest policy;

- Election of executive officers of the company;

- Topics affecting the relationship between the company and stockholders;

- Public issues likely to affect the company; and

- Responses to proposals submitted by stockholders.

In addition, the governance and nominating committee is usually responsible for reviewing:

- Contribution policies of the company

- Revisions to the company’s code of ethics

- Electing officers of the company other than the executive officers and

- Oversight of the annual evaluation of the board and the committee.

Corporate Governance Demographics

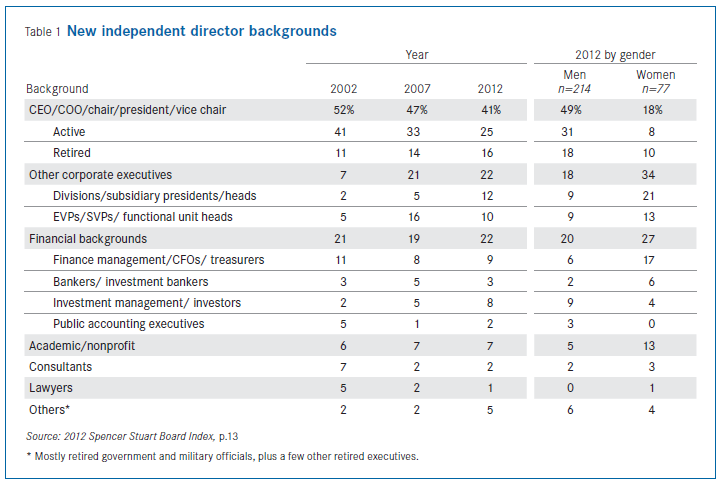

Spencer Stuart’s 2012 Board Index provides a snapshot of the backgrounds of new independent directors, based upon responses from directors of S&P 500 companies. According to the report, in the 2012 proxy year, 291 new independent directors joined boards, down from 443 in 2004, representing the smallest number of new directors to join boards in any year since 2001. One-quarter of new S&P 500 directors during 2012 were active CEOs, COOs, chairmen, presidents and vice chairmen, compared with 41 percent during 2002. This trend is due to a number of factors. There are fewer directorships overall, as boards are smaller and there are fewer listed companies due to consolidation. Fewer CEOs are serving on other boards due to the increased time considerations associated with serving as a director and pressure from their boards to limit external activities.

Spencer Stuart’s 2012 Board Index also provides a snapshot of the backgrounds of new independent directors, based upon responses from directors of S&P 500 companies (below).

Director demographics for S&P 500 2012

- Average board size is 10.7, down from 10.9 in 2002

- The number of new independent directors has decreased from 401 in 2002 to 291 in 2012

- Women comprise 26 percent of all S&P 500 directorships, up from 16 percent in 2002

- 18 women CEOs serve as directors of other companies, up from 7 in 2002

- Nine percent of S&P 500 boards still have no women

- The average age of directors is 62.6, up from 60.1 a decade ago

- 73 percent of boards have a mandatory retirement age, up from 55 percent in 2002 and

- Eighty-five percent of boards have a mandatory retirement age of 72 or older; 36 percent had such a requirement in 2002.

Source: Spencer Stuart, 2012 Spencer Stuart Board Index

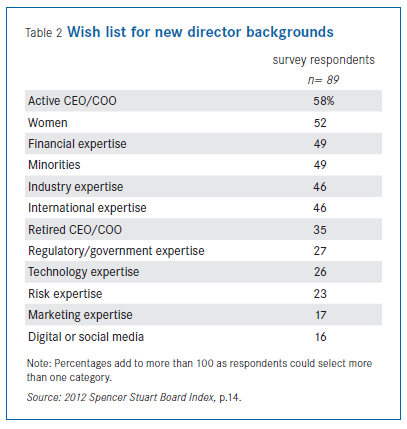

Director Recruitment Wish List

Retired and active “CEOs and COOs are at the top of boards’ wish lists. More than half of those surveyed (58 percent) said they sought current top executives, while 35 percent said they look for retirees from those roles.

Houston-based energy search specialist David E. Preng, founder and president of Preng & Associates, believes that boards today are doing a good job of determining the skills required to meet their fiduciary duty. According to Preng, the primary characteristics currently desired in director candidates are independence, conviction, the ability to act as a team player, and financial and business acumen. “Most boards look to recruit someone who understands their business, and former CEOs are preferable,” says Preng. Boards also look for candidates who have skills and expertise in strategy and risk management. Boards often require that a new director bring particular expertise such as international experience or accounting skills so that the person can serve on the audit committee. “It’s much easier to teach someone from your industry corporate governance skills than to start from scratch and try to teach them your business,” Preng continues. “Expertise in compensation is also valuable, given the considerable increase in the board’s proxy responsibilities—tying achievement of the articulated strategies to the compensation schematic is an important role for the board,” Preng observes. With particular reference to the energy business, “if someone presently sits on the board of an exploration and production company, they can’t serve on a competing board due to conflicts of interest. This tends to create a supply and demand dynamic for my industry,” he continues. Robert L. Pearson, founder and CEO of Dallas-based Pearson Partners International, Inc., says “skills most in demand is a sitting CEO with technology savvy hard to find is diversity at the C[-suite] level.”

“One third of our board searches are for audit committee financial experts,” says Theodore L. Dysart, vice chairman of Chicago-based executive search firm Heidrick & Struggles. “Those who technically qualify are relatively easy to find: every public company CEO, retired major accounting firm senior executives, and most chief financial officers and controllers meet the technical requirements.” He continues:

The challenge is to find those qualified candidates who will make a great board member, those with industry experience at the proper level and also bring the right perspective, stature, and presence—and will be able to meaningfully contribute to the future strategy of the enterprise. Following Sarbanes-Oxley, best practice seems to call for the new financial expert director to serve on the audit committee for a year or two in order to provide for orderly succession planning…

I would characterize the next general category of director searches as focusing on those candidates having industry operating experience. Finally, probably one-quarter of our current searches are for diversity candidates.

Role of the Lead Director

Among S&P 500 boards, there is a pronounced trend toward independent board leadership: 43 percent of these boards split the CEO and chair roles in 2012, up from 35 percent in 2007, and 23 percent of chairmen are truly independent, compared with 13 percent in 2007. Moreover, 53 percent of boards—a new high—had only one nonindependent director (the CEO) in 2012, compared with 22 percent in 2000 and 39 percent in 2005.”

According to Bonnie G. Hill, lead director of Home Depot, Inc., “The prescience of the board and the CEO to separate governance and operational responsibilities—so that the CEO could focus on running the business—is now widely considered a best practice.” Korn/Ferry notes that “The role of the non-executive board leader is growing. The non-executive board leader position began as a means of meeting an independence requirement, but today the role increasingly is being leveraged to create efficiency and additional value in the boardroom.”

As a result of the 2008 global financial crisis, political and media attention directed at corporate boards has surged. Warranted or not, the focus on board performance—especially on risk mitigation, CEO pay, and succession—has fueled major regulatory changes intended to foster greater independence and board oversight. In particular, the Dodd-Frank Act of 2010 requires companies to disclose in their annual proxy statements, whether the CEO and board chairman roles are combined or split and why the company has determined that its leadership structure is appropriate. Each company has a unique culture, so the exact shape the non-executive leadership takes should remain the board’s decision. Today’s non-executive board leader—often referred as the lead director—plays a key role in determining not only the board’s focus, but also the fulfillment of its oversight responsibilities. The lead director may be thought of as the “conscience” of the board. Central to success is the relationship between this individual and the CEO. Communications between the two should be candid, with the non-executive board leader operating as the CEO’s thought partner, providing insights into the board’s thinking, and conveying good news as well as bad. The board, too, must view the non-executive board leader as an honest broker. With those building blocks in place, the non-executive board leader represents a potentially powerful vehicle for enhanced board performance.

SEC rules require listed companies to disclose their board leadership structure and explain why they determined that such a leadership structure is appropriate for the company, given their specific characteristics or circumstances. If a board determines a lead director is desired, it must consider the skills and experience, as well as the time commitment required.

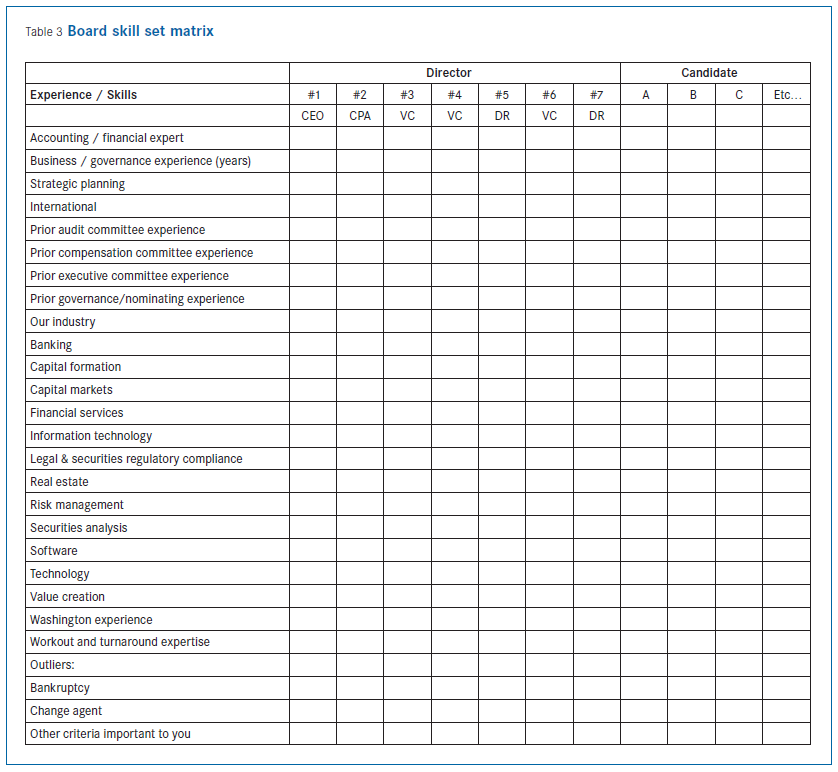

Director Optimization Template: The Matrix

Table 3 provides one example of how a governance and nominating committee might assess their current inventory of director skill sets to “fine tune” their thinking about future director needs. Procedurally, it might prove helpful to place the must-have skill sets first, followed by those deemed critically important for the future. Accordingly, the governance and nominating committee might first prioritize the skill sets and experience required for the future, the skills or experience lacking in the current board, and/or the skills needed in the near-term due to director succession. Conducting a board self-assessment may help in assessing the board’s strengths and weaknesses.

The first few skills listed in Table 3 seem germane to most well-composed boards: audit and financial expertise, broad business and corporate governance experience, understanding of a board’s legal duties and responsibilities, industry experience, strategic planning, and capital markets expertise. Beyond these core skills are a list of possible attributes that may assist in the stratification and prioritization of any given board’s particular needs. These secondary considerations are not exhaustive and are presented in alphabetical order, not ranked by importance. There is no single answer to the question, “What is the best board composition?” Indeed, boards will need to continually reassess their needs as the business environment changes.

The “must-have:” the audit committee “qualified financial expert” Certain skills and experience are absolute “must-haves:” (1) independent directors to populate the audit, compensation, and nominating and governance committees, and (2) qualified individuals who meet the definition of “financial expert” to serve on the audit committee. NYSE and SEC rules require that audit committees consist of independent directors, with at least one as chair deemed to be a qualified financial expert. Ideally, a board will have three individuals who qualify as financial experts: one to serve as chairman of the audit committee, a backup designated as vice chairman for succession planning purposes, and if possible, a third qualified financial expert to serve while gaining in-service experience about the company’s pressing audit issues.

Just as the fulfillment of each director’s duty of care requires that a succession plan be in place to assure that the enterprise will be able to adapt with minimal disruption if a CEO unexpectedly dies or is incapacitated, it makes sense that audit committees should strive to have more than one experienced, qualified financial expert replacement waiting in the wings in the event that the audit committee chair position is vacated unexpectedly. Information technology plays an increasingly critical role for almost every enterprise. Accordingly, in the absence of a risk committee, the board’s responsibility to govern information technology should also dictate that one or more audit committee members have relevant information technology skills and experience.

Prior business/corporate governance experience Corporate governance is a legally intensive endeavor. Directors must understand and comply with numerous rules and regulations, including state law and evolving case law, as well as grapple with the increasing trend toward federalization of corporate governance (in the form of the 33 Act, 34 Act, Foreign Corrupt Practices Act (FCPA), Sarbanes-Oxley, and more recently Dodd-Frank.) Previous public board service can help provide an indication of a candidate’s existing directorship skills. This assumes that the director served previously at a company where he benefited from skilled legal counsel, and so, without formal legal training, acquired an understanding of director duties and responsibilities.

Strategic Planning

Strategic planning seems fundamental to the success of any enterprise and yet is universally acknowledged to receive inadequate attention by many boards. Spencer Stuart’s 2012 survey of S&P 500 directors finds that “the board’s role in corporate strategy” was rated second as the issue most deserving of board focus by directors (after executive compensation). Identifying and recruiting strategic planning experience and expertise may be the most difficult and controversial matrix component.

Many directors believe that strategy originates from management and should be overseen by it. Having the board actively engaged in strategy development and monitoring is a threat to many CEOs. Others believe that strategy is an important function, best handled by the entire board, often at an annual strategy retreat. Management theorist Peter Drucker states:

But tomorrow always arrives. It is always different. And then even the mightiest company is in trouble if it has not worked on the future. It will have lost distinction and leadership—all that will remain is big-company overhead. It will neither control nor understand what is happening. Not having dared to take the risk of making the new happen, it perforce took the much greater risk of being surprised by what did happen. And this is a risk that even the largest and richest company cannot afford and that even the smallest business need not run.

Conclusion

Optimal board composition—that is, the best mix of director skills and experience—will depend on many company-specific variables. As a starting point for director recruitment and selection, boards should ask, “What human qualities are desired of every board member?” Every board should agree on a clear statement of desired personal attributes for all board members to guide the nominating and governance committee as they search for director candidates.

In addition, boards should adopt a clear definition of director independence. At the fifty-thousand-foot level, the question that must be asked and answered by every board nominating committee is, “What does our company do to create value, and do board members understand this value creation process so that they can govern effectively?”

Using the matrix methodology to assess the skills and experience needed and desired in potential directors may help evoke thoughtful discussions by the board, leading to better decisions by the nominating and governance committee.