Print

PrintIra Millstein is a senior partner at Weil, Gotshal & Manges LLP and co-chair of the Millstein Center for Global Markets and Corporate Ownership at Columbia Law School.

The recent shareholder “campaign” by a coalition of large institutional investors – AFSCME Employees Pension Plan, Hermes Fund Managers, the New York City Pension Funds, and the Connecticut Retirement Plans and Trust Funds – sought on its face to pressure the JPMorgan Chase & Co. board of directors to amend the bylaws to require that the role of chair be held by an independent director. It became a referendum on two additional issues: Mr. Dimon’s competence as a manager, and the competence of the board’s oversight of risk management. Unfortunately for “good governance,” the three issues become conflated and lead to harangues, heat, and polar positions by all sides, leading to little that’s instructive. It’s worth separating the issues to seek guidelines for the future.

Thoughtful advocates recognize that the board should have flexibility to determine leadership based on the company’s circumstances and rather than seeking to mandate the practice of independent chairmanship, view it as the appropriate default standard – or presumptive model. Even so, very few advocates of the independent chair model favor stripping an extant CEO/chair of the chair title; rather, they urge boards to consider separation upon CEO succession, unless there is an urgent need.

In theory, placing board leadership in the hands of an independent director acknowledges the oversight role of the board vis-a-vis the CEO and management team. Giving the role of chair to an independent director is a practice that is steadily gaining traction in the US, although few companies require such an approach in their bylaws. A Conference Board report found that only 19% of incoming CEOs in 2012 were also jointly appointed as board chairs. Additionally, 43% of the S&P 500 split the roles of CEO and chair and 23% of such boards have a truly independent chair. Eighteen such companies have a formal policy mandating the separation of the CEO and chair roles. These are new levels. (See 2012 Spencer Stuart Board Index)

But at JP Morgan Chase, separating board leadership from the CEO role became conflated with a debate about Mr. Dimon’s record in leading the company through perilous times. While there have been challenges, to be sure, they have been largely related to the generic problems inherent in managing “big bank” structures rather than Mr. Dimon’s managerial competence. His personal management record is significantly positive.

The vote on the shareholder proposal seeking an independent chair was clearly impacted by investor support for Dimon’s leadership of the company and the vigorous campaign by management to prevail. Nearly one third of investors backed a split, but this proved a drop from the 40% registered in support of a similar resolution in 2012. The outcome should not be viewed as a dip in shareholder support for independent board leadership. Many shareholders clearly did not want to send a message of a lack of confidence in Mr. Dimon and, according to news reports, some significant shareholders were concerned that a high vote in favor of the proposal could prompt Mr. Dimon to leave. In addition, some shareholders appear to have found comfort in JPMorgan Chase’s assertion that it has a strong and well-defined lead independent director role. For those who believe, as I do, that governance flexibility is beneficial – even critical – and that “one size does not fit all,” the role of a lead independent director may be a viable alternative to an independent chair, but only if the position is defined and duties performed with real power, judgment and authority. In order for a lead independent director to provide a reasonable substitute for an independent chair, the job description of the lead director must be substantially similar to an independent chair’s responsibilities. At the moment, this is not generally the case.

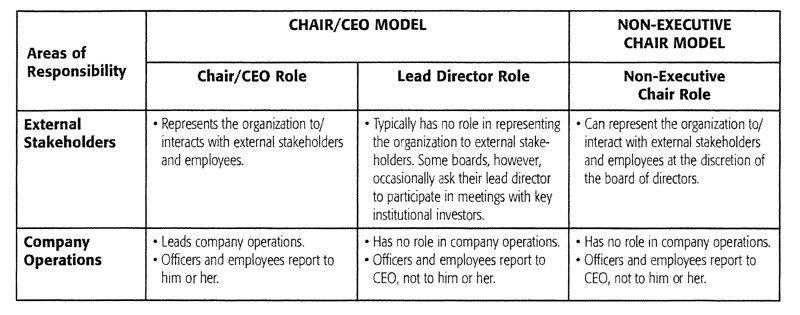

Substantial work was done on this issue by the National Association of Corporate Directors (NACD), in its Blue Ribbon Commission Report “The Effective Lead Director.” The role of the lead director as viewed in that report is not as strong a position as the independent chair, as indicated in a comparison chart included as Appendix A (below). In comparing the key duties of a typical independent chair to a lead director, the powers and duties of a lead director fall short in the following areas:

- Power to call a board meeting: Unlike the chair, the lead director typically does not have convening power but only suggests to the chair/CEO that a meeting be called.

- Control of the board agenda and board information: Unlike the chair who bears responsibility and authority for determining both the board agenda and the information that will be provided, the lead director collaborates with the chair/CEO and other directors on these issues.

- Authority to represent the board in shareholder and stakeholder communications: Typically the chair/CEO represents the board with shareholders and external stakeholders; the lead director plays a role only if specifically asked by the chair/CEO or the board directly.

These are key distinctions, and they build on other subtle differences in the role and authority of the chair and lead director with respect to the board’s efforts in management oversight: CEO succession; strategic development; board and director assessment; board relations with the CEO and C-suite; board diversity and succession; and, board oversight of risk. The Chairmen’s Forum, a body of independent chairs in North America, has found that the chair title itself often carries subtle authority compared to lead director, and those who hold the Chair are often compensated more to reflect that.

Those boards that opt for a lead director rather than an independent chair should define the role with significant authority to lead the board in areas where management has clear conflicts, including the matters outlined above.

Thus, separating the issues and thinking of the future, the instructive result, I believe, is: The campaign to strip Mr. Dimon of his existing titles was not timely. The board, if anything, should have been asked by shareholder proponents to split the roles on his succession. Indeed, for a big conglomerated bank it is especially necessary to have the board separately led to truly monitor management. A proposal could equally ask that, if the board seeks to stay with a lead director, that position should explicitly be the functional equivalent of a separate chair, or the board should explain, in some detail, as to “why not.”

As to Director elections and “risks,” the Board will presumably react to the vote, one way or another.

Appendix A

Comparison of the Non-Executive Chair and the Chair/CEO Models