Print

PrintMatteo Tonello is managing director of corporate leadership at The Conference Board. This post relates to an issue of The Conference Board’s Director Notes series authored by Arthur H. Kohn and Julie L. Yip-Williams; the complete publication, including footnotes, is available here.

The increase in institutional ownership of corporate stock has led to questions about the role of financial intermediaries in the corporate governance process. This post focuses on the issues associated with the so-called “separation of ownership from ownership,” arising from the growth of three types of institutional investors, pensions, mutual funds, and hedge funds.

To a great extent, individuals no longer buy and hold shares directly in a corporation. Instead, they invest, or become invested, in any variety of institutions, and those institutions, whether directly or through the services of one or more investment advisers, then invest in the shares of America’s corporations. This lengthening of the investment chain, or “intermediation” between individual investor and the corporation, translates into additional agency costs for the individual investor and the system, as control over investment decisions becomes increasingly distanced from those who bear the economic benefits and risks of owners as principals. The rapid growth in intermediated investments has led to concerns about the consequences of intermediation and the role of institutional investors and other financial intermediaries in the corporate governance process. These concerns are particularly relevant against a background of increasing demands for shareholder engagement and involvement in the governance of America’s corporations.

The Rise of the Intermediaries

Business ownership before the Industrial Revolution was marked by the simplicity of sole proprietorships and businesses owned and managed by a handful of individuals. These simple forms gave way to the more complicated corporate form that called for investments by an ever-growing number of individuals into a single corporate pool to be managed by corporate managers chosen by those individuals. The success of the corporate form in terms of its ability to generate lucrative return on investment and to efficiently deliver goods and services sought by its customers resulted in the demand by corporations for, and a willingness by individuals to provide, more capital. This brought even more complexity to evolving investment practices, as it invited professional investment managers to oversee the deployment of large amounts of capital. The actual suppliers of capital were willing or, in some cases, required to abdicate their right to decide in which corporations they would invest, and, in turn, relinquish all of the related decisions associated with that right to trusted and experienced third parties. These third parties would pool the capital and deploy it in any number of funds characterized by different investment time horizons, objectives, and strategies. In return, the fund manager generally would receive a fee for these management services from the suppliers of capital.

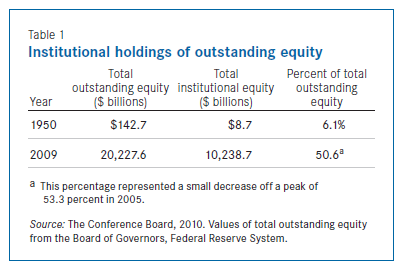

The last 60 years have seen a remarkable increase in the use of these intermediaries to invest the savings of Americans (Table 1).

Notably, the concentration of institutional ownership in the top 1,000 companies in the United States was significantly higher than the 50.6 percent cited in Table 1. As of the end of 2009, institutions owned 73 percent of such companies.

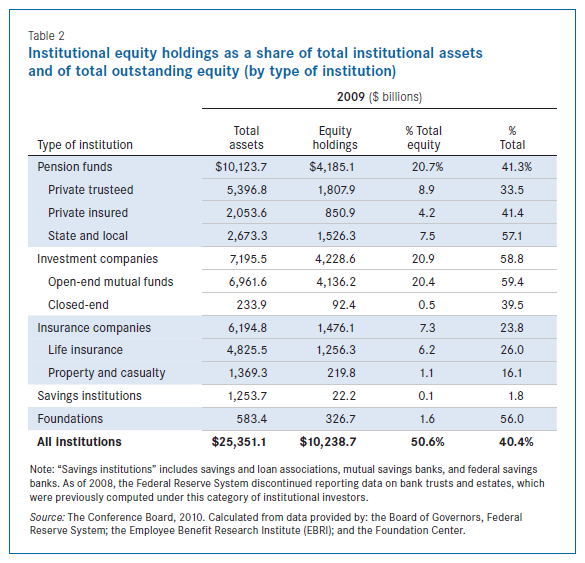

It is important to note that these figures take into account the holdings of private and public pension funds, mutual funds, insurance companies, savings institutions (e.g., savings and loan institutions, mutual savings banks, etc.) and foundations. They do not take into account the holdings of a major category of institutional investor: hedge funds. Hedge funds manage capital invested in domestic equities that amounts to only a few hundreds of billions of dollars (that is, a few percentage points out of the outstanding equity).Yet they have become well-known for their shareholder activism, frequently advocating for significant changes to a corporation’s strategic direction. As shown in Table 2, among institutional investors holding U.S. equities, pension and mutual funds own the most significant amounts by a substantial margin.

For this reason, in addressing concerns surrounding the lengthening of the investment chain, the attention of this post is focused on pension and mutual funds—also known as “traditional” institutional investors—and hedge funds because of their activist tendencies and reputation.

The proliferation of institutional investors is undoubtedly attributable in large part to the widespread acceptance of modern portfolio theory, which promotes diversification as the optimal investment strategy, where returns are maximized in a manner consistent with overall market performance and economic conditions, all at relatively low risk and low cost to the individual investor. Institutional investors are able to diversify to an extent that the individual investor is not, as a practical matter, able to do. They also offer a more attractive investment alternative for individual investors, since their returns are certainly higher than the negligible amounts that the investor would receive in a bank savings account.

Legal Safeguards against Agency Concerns

The insertion of intermediaries introduces additional agency relationships into the investment chain. As is the case with the establishment of any agency relationship, there are always concerns about whether the agent is acting in the best interests of the principal. The following briefly describes the legal framework governing certain institutional asset managers, which, to a significant extent, address and thereby serve to identify and highlight agency concerns.

Mutual funds. Mutual funds, formed as corporations or, sometimes, business trusts, are a type of investment company regulated by the Investment Company Act of 1940. In certain respects, they very much resemble the conventional corporation—they are formed by a sponsor, managed by a board of directors, who are subject to the same fiduciary duties of loyalty and care under state law as a director of any other corporation, and have shareholders whose liability is limited to their equity investment. Mutual fund directors are also charged with oversight responsibilities, principally overseeing the fund’s performance. Like publicly traded corporations, mutual fund directors are required to engage in certain practices to promote good governance, including conducting annual self-evaluations and quarterly executive session meetings. Under the Investment Company Act, at least 40 percent of a board’s members must be independent (although, in practice, most mutual funds have boards that are 75 percent independent), which generally means that those directors do not have any material relationships with the investment adviser retained by the fund. Mutual funds, as incorporated entities, must afford their shareholders the same general rights as shareholders of conventional corporations (e.g., election of directors (although only two-thirds of directors need to be elected by shareholders), attendance at shareholder meetings (although such meetings are much less common), and binding votes on certain fundamental transactions. Because mutual funds are registered under the Securities Act of 1933, current and prospective fund shareholders benefit from extensive information rights under federal securities laws. Regularly updated prospectuses disclose a fund’s investment policies and objectives, potential risks, fees and expenses, historic performance, and information about the fund’s directors, investment adviser, and other third-party service providers (although there are no disclosure obligations as to their or their investment advisers’ voting policies or other information as to their positions on corporate governance matters).

However, a mutual fund is entirely distinct in its operations and structure from a conventional corporation in that it does not have employees or other staff to manage its pool of contributed capital. Rather, all operations are outsourced to investment advisers, distributors, custodians, transfer agents, and other third parties who are frequently considered for purposes of the Investment Company Act as “affiliated” with the mutual fund and its sponsor. Because of the potential for conflicts of interest inherent in such relationships, one of the primary responsibilities of the board of directors is to evaluate and approve those arrangements on a periodic basis.

The investment adviser is the most critical of the mutual fund’s service providers, empowered with the authority to manage the mutual fund’s capital and make all day-to-day investment decisions. Therefore, the investment adviser is a vital player within the intermediation process, representing the existence of another principal–agent relationship within the investment chain. Legal safeguards exist to protect the principal (i.e., in this instance, the mutual fund). It is the mutual fund’s prerogative to terminate an existing relationship with an investment adviser by either terminating or declining to renew the advisory agreement. However, this rarely happens, largely because the investment advisers are affiliated with the mutual funds and their sponsor. Unless there are extreme circumstances, such as fraud, a change of advisers would also be costly, disruptive, and potentially contrary to shareholders’ express intention to invest with a particular mutual fund. Instead, to effect change, directors typically would urge action by the investment adviser, such as a change in portfolio management, increased investment research capability, or retaining a sub-adviser.

As a legal matter, an investment adviser owes fiduciary duties to its client, the mutual fund, including duties of care (e.g., by exercising prudence and reasonableness in making investment decisions), loyalty (e.g., by placing the client’s interests first, acting in the client’s best interests and avoiding conflicts of interests) and good faith (e.g., by being truthful and accurate in all communications and disclosures). These fiduciary duties are rooted in a combination of common law (principally, in the laws of agency and trust) and federal statutory law (principally, the Investment Company Actand the Investment Advisers Act of 1940 (the Advisers Act)).

Most notably in the context of investor engagement with public companies, the proper exercise of an investment adviser’s fiduciary duties today includes diligently exercising its right to vote on behalf of its institutional clients.

In the more distant past, advisers often did not vote on behalf of their clients, believing that the task was too costly and time-consuming and that their clients’ small holdings were unlikely to make a difference in the outcome. However, at the beginning of this century and coinciding with an era of greater shareholder activism, advisers and their institutional clients were increasingly criticized for not voting, given their enormous collective voting power and ability, in some cases, to affect the outcome of the shareholder votes and influence corporate governance. In 2003, the U.S. Securities and Exchange Commission (SEC) promulgated Rule 206(4)-6 under the Advisers Act, which made it fraudulent for an adviser to exercise proxy voting authority without having procedures reasonably designed to ensure that the adviser votes in the best interest of its clients. In the rule’s adopting release, the SEC confirmed that an adviser owes fiduciary duties of care and loyalty to its clients with respect to all services undertaken on its client’s behalf, including proxy voting. The adopting release further stated, “The duty of care requires an adviser with proxy voting authority to monitor corporate events and to vote the proxies. To satisfy its duty of loyalty, the adviser must cast the proxy votes in a manner consistent with the best interest of its client and must not subrogate client interests for its own.”

Pension funds. The governance of retirement savings vehicles—that is, the processes by which their investment decisions are made—as a threshold matter, depends on the type of pension arrangement concerned. Generally, pension vehicles are classified into one of three categories for this purpose.

- 1. Private-sector defined benefit pension plans are subject to the federal Employee Retirement Income Security Act of 1974 (ERISA). ERISA requires employers to set aside assets to satisfy their future pension payment obligations and imposes a governance structure pursuant to which those assets are invested. Generally, each plan must designate a “named fiduciary,” which has ultimate investment control. The named fiduciary of corporate pension plans is typically a committee of senior executives of the corporate plan sponsor. While some named fiduciaries directly make individual investment decisions (that is, decisions about investing in particular stock or other assets), most only keep responsibility for asset allocation and management selection decisions, with individual investment decisions being made by investment advisers hired for this purpose. The investment advisers may manage plan assets either through separate accounts or through collective investment vehicles they maintain.

- 2. Public-sector defined benefit plans are not governed by federal pension law, but rather are subject to distinct state or local laws. Generally, ultimate investment authority for those plans rests with a board or investment committee that is composed of state or local politicians or their appointees. Generally, those committees may either make individual investment decisions or delegate such decisions to investment advisers hired for that purpose.

- 3. 401(k) and other similar defined contribution plansare subject to the governance structure mandated by ERISA, if they are sponsored by private-sector companies, or by state or local law, if they are government-sponsored plans. What these plans have in common, however, is that they generally pass investment decisions to individual plan participants, whose ultimate retirement savings under the plans depend on their investment choices. The large majority of such assets are invested among a limited menu of mutual funds or other commingled investment vehicles that each plan’s named fiduciaries designate as available under the plan. While many such plans also permit participants to make individual investment decisions through so-called “open brokerage windows,” only a very small portion of the aggregate assets of such plans are so invested.

Persons who make decisions related to the investment of ERISA plan assets are subject to strict fiduciary duties, as are, generally, persons who have discretion over the investment of governmental plan assets. Under ERISA, the duties of plan fiduciaries include a duty of care, skill, diligence and prudence (under a so-called “reasonable expert standard”), diversification, and exclusive attention to the interests of plan participants and their beneficiaries. In addition, ERISA fiduciaries are subject to a strict and complex framework of detailed conflict-of-interest rules. Fiduciaries of public-sector plans are typically subject to similar conflict-of-interest rules, which have been expanded recently to include, in some jurisdictions, so-called “pay-to-play” rules that were enacted in response to concerns about inappropriate influence on investment decisions of public-sector plans by pension investment consultants. The disclosure requirements ERISA imposes for the benefit of plan participants with respect to individual investment decisions made with plan assets are relatively limited.

Interestingly, the ERISA conflict-of-interest rules have been applied to impose limits on the types of incentive fee arrangements that may be implemented for investment advisers who manage ERISA plan assets, based on a concern that such fees may incentivize advisers to make investment decisions with their own interests in mind (i.e., earning an incentive fee) and take inappropriate risks with plan assets.

As with mutual funds, as discussed above, regulators were required to step in to encourage managers of ERISA plan assets to actually vote the shares in which they have invested. In 1988, the U.S. Department of Labor issued an advisory opinion, concluding that the right to vote shares was a “plan asset” to which the fiduciary rules referred to above apply.

Hedge funds. Hedge funds are yet another type of pooled investment vehicle. Their organizational structure enables them to avoid certain legal and regulatory requirements that apply to other investment companies. Hedge funds domiciled in the United States are generally formed as limited partnerships or other limited liability entities and are managed by the partnership’s general partner (or equivalent entity), who may also serve as the hedge fund’s investment adviser. Investors contribute capital to the partnership (or other equivalent entity), which executes a partnership or other operating agreement that frequently entitles them to certain rights that are generally limited to information and reports and redemption of all or a portion their interest at specified periods. There is often limited visibility into the general partner’s investment practices and other activities. Because U.S.-domiciled hedge funds are not formed and operated as corporations, there is no board of directors; therefore, director independence requirements and the extensive body of law governing a director’s duties to a corporation’s investors do not apply. Investors also do not have a right to attend shareholder meetings or otherwise vote in certain fundamental decisions (i.e., sales and mergers). Furthermore, the private nature of hedge fund offerings (their interests are not sold through registered public offerings) and the limits on the number and types of investors admitted into their partnerships, ensure that their interests are exempt from the registration requirements of the Securities Act of 1933 and the fund itself is exempt from being classified as an investment company under the Investment Company Act. As a “private fund” exempt from the registration requirements of the Investment Company Act, hedge funds are not bound by the disclosure and other requirements and investment limitations that it sets. For example, registered investment companies, including mutual funds, are prohibited from trading on margin or engaging in short sales and must secure shareholder approval to take on significant debt or invest in certain types of assets, such as real estate or commodities. These types of transactions are often core elements of hedge fund trading strategies. Hedge funds trade in all sorts of assets, from traditional stocks, bonds, and currencies to more exotic financial derivatives and even nonfinancial assets, and often use leverage to increase their returns.

As a result of recent regulatory changes, most investment advisers of hedge funds are now required to register as such under the Advisers Act, thereby making them subject to its requirements. These requirements include disclosure obligations about gross and net asset values, investor concentration, borrowing and liquidity, performance, investment strategies, credit risk and trading, and clearing practices. Large advisers must also disclose information regarding exposures to asset class, geographical concentration and the monthly value of portfolio turnover by asset class. Investment advisers are also now required to have written policies reasonably designed to prevent violations of the Advisers Act, regular review of those policies, and a chief compliance officer, who is responsible for administering those policies. As with investment advisers to traditional institutional investors, hedge fund investment advisers are also subject to fiduciary duties (both at common law and based on the antifraud provisions of Section 206 of the Advisers Act) that obligate them, among other things, to allocate their fees and expenses fairly between themselves and their clients, disclose conflicts of interest, and properly oversee the management of risk.

The Downside of Intermediation

Some advocates for stewardship place the blame for events at Enron, WorldCom, and other corporate scandals of the last decade, as well as the financial crisis, in part on intermediation and, more specifically, on the many intermediaries who stand between the ultimate beneficial owners and the corporation. Intermediation creates multiple layers of agency costs that cannot be entirely mitigated by legal safeguards. According to this line of thought, the potential for misaligned interests is exacerbated by the growing divide between ownership and control, where institutional investors and their advisers lack any real incentive to actually “own” the companies in which they invest but seek merely to manage their portfolios to maximize their own returns. In other words, institutional investors deserve blame because they failed to act as owners or “stewards” to adequately monitor and hold accountable corporate managers, and in so doing, failed in protecting the interests of their investors, the ultimate beneficial owners. The idea of stewardship is most popular in the United Kingdom and the European Union.

Because institutional investors own large blocks of stock, they have the unique ability to play a far more active role in corporate governance than dispersed individual investors traditionally have. Stewardship advocates assert that short-termism by corporate managers is partly attributable to the institutional investors’ singular focus on short-term returns, which are an inevitable result of their focus on extreme diversification and their compensation and incentive structures.

Diversification is the principal means by which institutional investors manage risk—not merely through investing in multiple companies and other classes of assets, but also through a manager diversification, in which management of a pool of capital is divided among separate investment advisers who employ different investment strategies. This contributes to extreme diversification, with one institutional investor holding fragmented positions sometimes in hundreds or even thousands of companies. Extreme diversification is also fostered by modern portfolio theory, which shifts the focus away from the specifics of a particular company to “mathematical insights into the relative performance of shares and investment funds in relation to selected benchmarks or indices.” Investment decisions are made on the basis of mathematical calculations where an investor must ensure that its portfolio is an adequate reflection of the market or otherwise increase risk to the portfolio. Selling and buying of shares is therefore based on their weight in an index.

Compensation for investment advisers of traditional institutional investors is almost always determined based on assets under management and not upon investment return (except in the case of hedge fund advisers, who are compensated based on a combination of both factors). Therefore, there is incentive for investment advisers to attract as much investment as possible. Additionally, the security of an investment adviser’s continued position, particularly those who manage pension funds, is also based on its performance, typically with a short-term focus measured quarterly, semiannually, or annually, but too often not in terms of the multiyear time horizons that companies often need to see a return on implementing new strategies. Competition among those advisers and sub-advisers to attract more clients also places an emphasis on short-term performance and meeting short-term investment returns.

Pressures to maintain adequate levels of diversification and deliver results with respect to performance have led to increasingly short holding periods. While the information differs slightly, depending on the type of investor being surveyed and the locus of the trading, commentators generally report that holding periods, which were in the five-year range 30 years ago, have shrunk to between five and nine months today. The concern is that institutional investors who invest in companies for short periods of time have relatively little interest in the long-term performance of those companies. Furthermore, high rates of portfolio turnover, many argue, is said to increase risk and decrease investment return.

What Downside?

The view that traditional institutional investors are culpable in contributing to market failures is by no means a universally accepted one. Those on the other side of the debate see no merit in institutional investors acting as stewards or otherwise compelling them to do so, pointing to the fact that institutional investors have consistently failed to play any stewardship role, despite the urging of academics and regulators. Opponents of stewardship offer the following arguments against it:

- Given business models driven by diversification, relatively short holding periods, and, in many cases, passivity in tracking a market index, institutional investors are rationally apathetic to corporate governance decisions;

- There is little to no correlation between shareholder activism by traditional institutional investors or improved corporate governance practices and the maximization of shareholder value; and

- A fundamental assumption of stewardship advocates—the notion of the very existence of short-termism and long-termism—is flawed. Opponents of stewardship believe in the efficient market hypothesis, which holds that a company’s share price incorporates all information relevant to its value and reflects the best estimate of the stock’s future risk and return. Long term and short term run together because the company’s share price is the only accurate way to measure future risks and returns. Under this theory, short-term behavior by corporate managers is punished by the market through a lowering of share price. Rejecting the notion of long-termism or short-termism, critics maintain there is no basis for much of the criticism lodged by stewardship advocates against institutional investors.

Inconsistent views and disagreements on all of these issues among the institutional investor community is evidenced by the varying levels of interest in and capacity for engagement exhibited by institutional investors (although, interest and capacity also seem to have a practical correlation with the size of an institutional investor; larger institutional investors appear more inclined to engage and, therefore, more likely to act as stewards).

Ronald J. Gilson and Jeffrey N. Gordon propose what may be viewed as an attractive middle ground in the debate over whether institutional investors should act as stewards. They argue that mutual funds and pension funds are and should be encouraged to serve as governance intermediaries; while they can generally be expected to be passive and not initiate any important proposals, they can be called upon to consider proposals made by shareholder activists (i.e., hedge funds). Gilson and Gordon say that the effect would be “to potentiate institutional investor voice, to increase the value of the vote, and thereby to reduce the agency costs” associated with the intermediation process.

Possible Solutions to Problems Associated with Intermediation

For stewardship advocates, the solution to the problems associated with intermediation, particularly as it relates to the promotion of short-termism, is to find ways for institutional investors to act more like owners and, therefore, better represent the interests of those whose capital they invest. In certain cases, this means requiring institutional investors to revamp their business practices. Stewardship advocates recommend measures encouraging institutional investors to:

- invest in fewer companies so that scarce resources can be better allocated to understanding more deeply the business strategies and objectives of the companies in which the institutional investor is invested;

- devote more resources to corporate governance and engagement issues;

- retain more investment responsibilities rather than outsourcing them to investment advisers;

- develop policies on corporate governance and engagement;

- change the performance evaluation procedures for investment advisers so that they are evaluated on a five- to 10-year cycle;

- revamp compensation practices—for example, by including a performance fee that is paid over several years, adding an equity component to promote long-term behavior, and offering additional compensation for corporate governance-related activities; and

- limit the amount of portfolio turnover.

These recommendations would necessitate a fundamental shift in the business model of institutional investors and their advisers, which makes them unlikely to be implemented.

Suggested Alternatives to Stewardship

As an alternative to mandating fundamental changes to the business model of institutional investors, other proposals and initiatives have been advanced that are aimed at more closely aligning the interests of the ultimate beneficial owner and intermediary. They include:

Enhanced disclosure requirements. This includes enhancing disclosure requirements around fees and expenses, especially as to the costs associated with a fund’s high turnover rate. Some have also called for greater disclosure around complex investment strategies relating to structured and derivative arrangements that would appear to promote short-term gains at the expense of long-term value creation (e.g., an activist who becomes a formal shareholder with voting power while simultaneously shorting the same corporation’s stock, or an investor who owns shares of one company and uses that position to increase the value of its holdings in another company instead). Increased and enhanced disclosure would theoretically provide individual investors with the information needed to evaluate an institutional investor’s short-term approaches.

Changes to the taxation of transactions by institutional investors. The Aspen Institute has recommended revising capital gains tax provisions or implementing an excise tax in ways that would discourage excessive portfolio turnover and encourage longer-term share ownership. The capital gains tax rate might be set on a descending scale, based on the number of years a security is held. The Aspen Institute also recommended the elimination of limitations on capital-loss deductibility for very long-term holdings, now capped at $3,000 per year for losses related to holdings of any duration.

Clarifying fiduciary duties. This proposal includes urging fiduciaries to reevaluate, and courts and other governmental bodies to clarify or alter as necessary, the generally accepted understanding of the nature and extent of fiduciary duties owed by various intermediaries. Some argue that the understanding of fiduciary duties has evolved into a purely economic analysis that considers quantitative factors only, and that it has devolved into a practice of simply comparing fund performance and fees, without regard to qualitative factors. For example, when a fund manager is deciding whether it would be consistent with its fiduciary duties to recall a stock on loan to vote it, fund managers are obligated to compare the value of voting against the stock-lending revenues that would be sacrificed for the vote. Given the difficulty of valuing a vote quantitatively, some fund managers routinely assign it a zero value and, hence, conclude that shareholder interest is better served by not recalling the stock, even when contentious issues are to be voted. In the takeover context, the decision of whether to accept a bid is guided principally by stock price, which is highly influenced by short-term considerations, rather than a thorough assessment of a company’s long-term prospects. Reform in this area would focus on clarifying fiduciaries’ duties to include taking long-term and short-term considerations, as well as other qualitative considerations, into account. Aside from any new regulations requiring greater disclosure as described above, the Aspen Institute has also suggested that fiduciary duties should include an obligation for investment advisers to take into account, and clearly inform investors of, tax and other factors that have implications for long-term investing.

Adopting a stewardship code. In 2010, the Financial Reporting Council (FRC) released the UK Stewardship Code, which aims to enhance the quality of engagement between institutional investors and companies and describes governance practices to which institutional investors should aspire. The Stewardship Code sets out good practice on engagement with companies to which the FRC believes institutional investors should aspire and operates on a “comply or explain” basis. UK-authorized asset managers must report on whether or not they apply the Stewardship Code. The principles embrace the notion of institutional investors as stewards of the public corporation (i.e., active monitoring and engagement) and call on them to:

- publicly disclose their policy on how they will discharge their stewardship responsibilities;

- have and publicly disclose a robust policy on managing conflicts of interest in relation to stewardship;

- monitor their investee companies;

- establish clear guidelines on when and how they will escalate their stewardship activities;

- be willing to act collectively with other investors, where appropriate;

- have a clear policy on voting and disclosure of voting activity; and

- report periodically on their stewarding and voting activities

In conclusion, evidence of substantial change in the structures of corporate ownership seems clear. Changes in governance processes to reflect and counterbalance the changes in ownership structures could help to optimize corporate performance. However, changes to entrenched practices can lead to unintended consequences, and it’s unclear whether such changes would develop organically through the operation of the markets. Under the circumstances, incremental approaches to test the impact of adjustments in governance processes, such as the one suggested by Gilson and Gordon, seem attractive.