Print

PrintThe following post comes to us from Faten Sabry, Senior Vice President at NERA Economic Consulting, and is based on a NERA publication by Ms. Sabry, Eric Wang, and Joseph Mani; the full document, including footnotes, is available here.

It has been more than six years since the onset of the credit crisis and we have documented for the first time in the past few months a significant increase in the number and size of settlements. Meanwhile, the pace of new filings has slowed as housing markets continue to improve and delinquencies and defaults decline. However, litigation arising from the credit crisis is far from over.

In this post, we discuss the recent trends of settlement activity and review some of the major settlements in credit crisis litigation. We also discuss mortgage settlements that are related to repurchase demands mainly between mortgage sellers and Fannie Mae and Freddie Mac. We then examine the current trends in filings, including the types of claims made, the nature of defendants and plaintiffs in the litigation, and the financial products involved.

Our main findings, which are discussed in greater detail below, include the following:

Findings Related to Credit Crisis-Related Settlements:

- We have documented four categories of settlements: 1) settlements related to credit crisis securities lawsuits; 2) other proposed settlements that are yet to be finalized; 3) settlements related to the repurchase demands by Fannie Mae and Freddie Mac; and 4) settlements with regulatory agencies that are related to foreclosure proceedings and other consumer finance issues.

- Settlements of credit crisis-related litigation between 2007 and October 2013 total more than $32 billion, about 22% of which is related to settlements of securities class action lawsuits. The five largest securities litigation settlements to date total $19 billion (59% of total credit crisis litigation settlements). These are:

- the tentative $13.0 billion settlement between JPMorgan and the US Department of Justice (DOJ) resolving several civil suits and investigations regarding mortgage securitizations in October 2013;

- the $2.4 billion settlement in In re: Bank of America Corp. Securities, Derivative and ERISA Litigation in September 2012;

- the $1.7 billion settlement in MBIA v. Countrywide et al. in May 2013;

- the $1.1 billion settlement related to MBIA v. Morgan Stanley et al. and Morgan Stanley et al. v. MBIA et al. in December 2011; and

- the $885 million settlement in FHFA (as conservator for Fannie Mae and Freddie Mac) v. UBS Americas Inc. et al. in July 2013.

- There are proposed settlements that are currently before the courts for approval to resolve claims related to representations and warranties for mortgage loan collateral in RMBS trusts.

- These include a proposed $8.5 billion settlement in relation to Countrywide that is currently being reviewed by Justice Barbara Kapnick of the New York State Supreme Court in an Article 77 proceeding, and a $7.3 billion proposed settlement (with an estimated recovery value of $672 million) relating to representation and warranty claims in respect of 392 RMBS trusts issued by entities related to Residential Capital LLC (ResCap) which is currently in Chapter 11 bankruptcy.

- Settlements related to mortgage repurchase claims by Fannie Mae and Freddie Mac have exceeded $18 billion to date.

- Finally, the US government has recovered more than $34 billion in settlements of its claims against various banks in relation to allegations of improper foreclosure proceedings and other consumer finance issues such as fairness in mortgage lending.

Findings Related to Credit Crisis Litigation Filings:

- There have been a total of 927 credit crisis filings from January 2007 through the end of June 2013, but the pace at which new cases are being filed has fallen sharply: only 30 new cases were filed in the first half of 2013, less than half of the 78 cases filed during the first half of 2012.

- Consistent with the broad trend, filings of new credit crisis-related cases involving 10b-5 and ERISA allegations have declined markedly since 2007. In contrast, filings of breach of contract cases have increased since 2012.

- In lawsuits filed in 2012 and the first half of 2013, the most commonly named defendants were issuers and underwriters and the allegations were mainly related to structured products such as asset- and mortgage-backed securities (ABS and MBS, respectively).

The impact of the record-setting regulatory settlements on private litigation remains to be seen and the litigation seems to be moving to a new phase.

Credit Crisis Lawsuits: Methodology Used to Compile the Database

For the purposes of this article, we define “credit crisis lawsuits” as securities cases (i.e., cases in which the allegations relate to the purchase, ownership, or sale of securities) related to the downturn in the financial markets and mortgage markets that began in 2007. Our count of credit crisis lawsuits includes, among others, ERISA claims, shareholder derivative actions, individual state and federal cases, international cases, and state and federal shareholder class actions. We compile data from various sources including Law360, Bloomberg, Factiva, RiskMetrics Group/Securities Class Action Services, SEC filings, and case dockets from January 2007 to June 2013. If any cases are consolidated, the duplicate filings are removed and the data are adjusted.

The Settlements

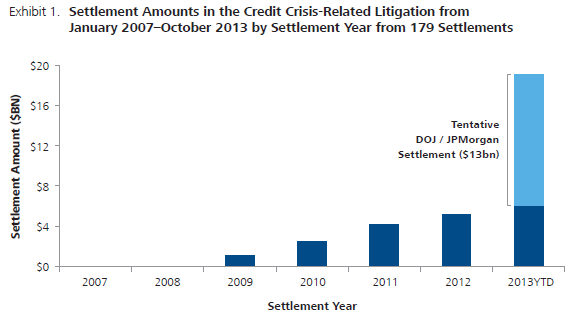

Credit Crisis-Related Litigation Settlements: Record Activity with $19 Billion in Settlements for 2013, through October

Credit crisis-related litigation settlements from 2007 through October 2013 have exceeded $32 billion, of which 22% is related to securities class actions. In 2013, we have observed a significant acceleration in credit crisis-related litigation settlements with about $19 billion in settlements through the first 10 months (January to October). Of the $19 billion in settlements, $13 billion reflects the tentative settlement between JP Morgan and the DOJ. In 2013 through October, total settlements have increased 267% from total settlements in 2012 (17% when not including the JP Morgan/DOJ settlement). Exhibit 1 below presents the total dollar value of settlements, recorded by year of settlement.

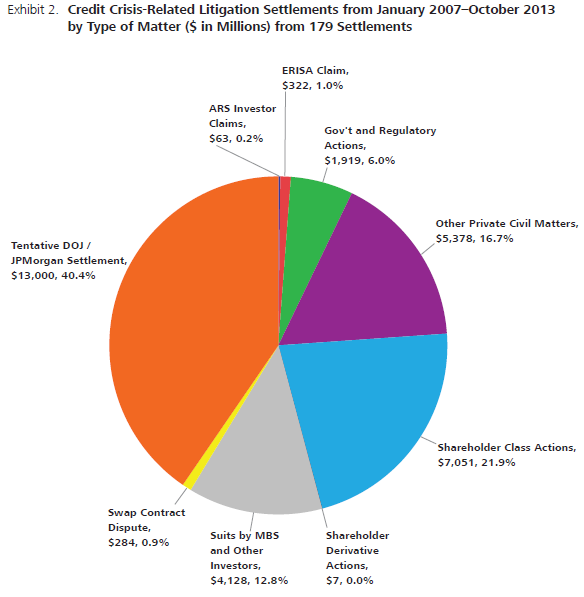

Exhibit 2 shows the breakdown of settlements by type of litigation. The tentative $13 billion settlement between the US DOJ and JPMorgan makes up 40% of the $32 billion in total settlements and is by far the largest settlement to date.

There have been 547 decisions and settlements in 409 credit crisis cases from January 2007 through October 2013, which account for 44% of the credit crisis filings to date. NERA’s database documents decisions and settlements associated with the credit crisis filings, but the decisions do not necessarily indicate the final status of these lawsuits. We have recorded 179 settlements, 159 dismissals granted, 72 dismissals denied, 92 partial dismissals, 35 voluntary dismissals, and 10 other miscellaneous decisions.

Recent Credit Crisis-Related Litigation Settlements: A Review

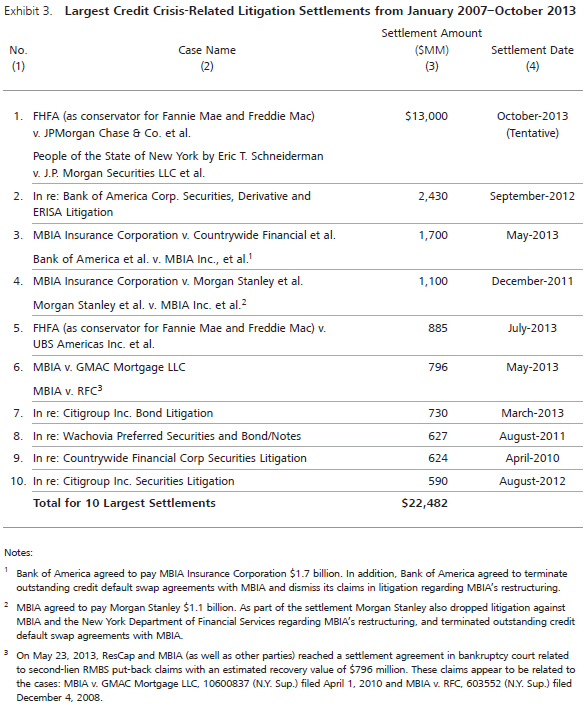

Some of the largest settlements to date involve claims that were brought by the monoline insurers, investors in ABS or MBS securities, and shareholders. See Exhibit 3 for a list of the 10 largest settlements arising from credit crisis-related litigation.

The largest credit crisis-related litigation settlement occurred in October 2013, when JPMorgan reached a tentative settlement with the US DOJ regarding civil suits and investigations into JPMorgan’s mortgage securitization business. The settlement includes $4.0 billion to settle claims brought by the Federal Housing Finance Agency regarding alleged misrepresentations about collateral underlying MBS notes purchased by Fannie Mae and Freddie Mac. The remainder will represent additional penalties as well as an allocation for consumer mortgage relief. The settlement, if approved by the court, will also resolve a case brought by New York Attorney Eric Schneiderman over mortgage securitization practices at Bear Stearns and EMC Mortgage.

The second largest settlement is in In re: Bank of America Corp. Securities, Derivatives, and ERISA Litigation, with a value of $2.4 billion, announced in September 2012. The settlement was approved in April 2013. Bank of America shareholders alleged that Bank of America and its directors and officers made misleading statements about the financial health of Bank of America and Merrill Lynch at the time of its acquisition. According to a press release from Bank of America, the company “denie[d] the allegations and [entered] into this settlement to eliminate the uncertainties, burden and expense of further protracted litigation.”

The third largest settlement is the $1.7 billion paid by Bank of America to MBIA Insurance Corporation in the MBIA v. Countrywide et al. case, announced on May 6, 2013–nearly five years after it was originally filed. In that case, MBIA alleged misrepresentations and breaches of contract in connection with financial guarantees on fifteen RMBS sponsored by Countrywide. Specifically, MBIA alleged that Countrywide falsely represented the underlying mortgages and its underwriting standards to MBIA and that Countrywide refused to repurchase non-compliant mortgage loans. The $1.7 billion settlement consisted of approximately $1.6 billion in cash and the remittance of MBIA’s senior notes (due 2034) with a principal amount totaling $137 million that Bank of America had previously held. In addition, Bank of America received five-year warrants to purchase shares of MBIA common stock and MBIA entered into a $500 million three-year secured revolving credit agreement with Bank of America. Bank of America also agreed to terminate outstanding credit default swap (CDS) agreements with MBIA and dismiss its claims in litigation regarding MBIA’s restructuring. Based on a press release from MBIA, the settlement eliminated $7.4 billion of insured exposure.

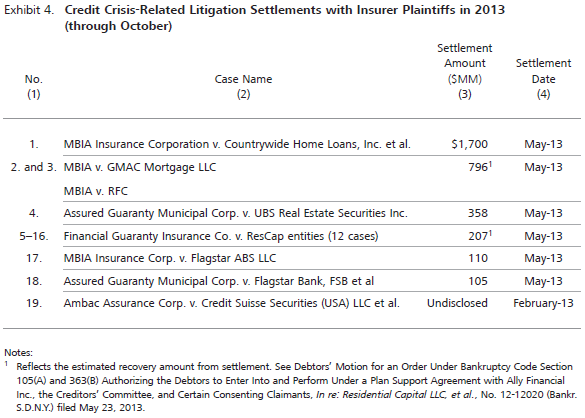

Cases brought by MBS and ABS investors have been very active, with 8 such cases settling in 2012, and 17 settling in 2013 through October for a total value of $6.6 billion. While the allegations in these cases vary, a large majority of the cases involved claims under Sections 11 and 12 of the Securities Act of 1933. Much of the recent settlement activity in 2013 has also occurred in cases where the plaintiffs are monoline insurers of MBS and ABS securities. In addition to the $1.7 billion settlement between MBIA and Countrywide, 18 similar cases with monoline insurers settled in 2013 through October. See Exhibit 4 for a list of these cases.

Other Major Credit Crisis Settlements

In addition to settlements directly related to securities litigation (i.e., those that resolved a pre-existing securities lawsuit), there have been other major credit-crisis related settlements. We discuss these settlements below.

Proposed Settlements for Countrywide MBS and ResCap MBS

In addition to the settlements arising from credit crisis securities litigation, there is the proposed $8.5 billion Countrywide settlement currently being reviewed by Justice Barbara Kapnick of the New York State Supreme Court in an Article 77 proceeding. In June 2011, institutional investors that held certificates in these trusts requested that Bank of New York Mellon (BNYM) enter into a settlement with Countrywide and Bank of America. BNYM subsequently filed a petition in the Supreme Court of the State of New York to begin a proceeding under Article 77 of the Civil Practice Law and Rules (CPLR) to request judicial approval of the proposed settlement. The proposed settlement, if approved by the Court, would resolve repurchase exposure, among other issues, for 530 Countrywide-issued first-lien RMBS trusts with an original principal balance of $424 billion.

Another similar proposed settlement regarding representation and warranty claims is the $7.3 billion settlement for over 392 RMBS trusts issued by entities related to Residential Capital LLC (ResCap). In June 2012, ResCap submitted a motion in its bankruptcy proceeding to approve an $8.7 billion settlement, which it had negotiated with a group of institutional investors. In a May 2013 motion submitted by ResCap to enter into a plan support agreement, the claim amount was revised to $7.3 billion, with an estimated recovery value of $672 million.

Strong Settlement Activity for Repurchase Demands by Fannie Mae and Freddie Mac

In addition to the settlements described above, Fannie Mae and Freddie Mac have recovered more than $18 billion from several financial institutions to resolve mortgage repurchase claims. These recoveries include the following:

- A $1.1 billion settlement agreement reached in October 2013 between JPMorgan and Fannie Mae and Freddie Mac regarding mortgage repurchase claims.

- A $438 million settlement agreement reached in October 2013 between SunTrust and Fannie Mae and Freddie Mac regarding mortgage repurchase claims.

- An $869 million settlement reached in September 2013 between Wells Fargo and Freddie Mac, resolving nearly all repurchase claims related to loans sold to Freddie Mac through 2008.

- A $395 million settlement reached in September 2013 between Citigroup and Freddie Mac, regarding repurchase claims for about 3.7 million loans sold to Freddie Mac from 2000 to 2012.

- A $968 million settlement reached in July 2013 between Citigroup and Fannie Mae resolving repurchase claims related to 3.7 million residential first-lien mortgages.

- An $11.6 billion settlement reached in January 2013 between Bank of America and Fannie Mae, resolving Fannie Mae’s repurchase claims related to mortgages sold to Fannie Mae between 2000 and 2008. The settlement also included the payment of fees related to foreclosure delays by Bank of America.

- A $2.8 billion settlement reached in January 2011 between Bank of America and Fannie Mae and Freddie Mac ($1.5 billion to Fannie Mae and $1.3 billion to Freddie Mac), relating to mortgage repurchase demands.

Settlements Related to Mortgage Lending and Servicing

In addition to the settlements in the securities litigation and repurchase demands discussed above, there have been over $34 billion of settlements between the US government and various financial institutions, related to foreclosure procedures and consumer finance issues such as fairness in mortgage lending. On January 7, 2013, the Office of the Comptroller of the Currency and the Federal Reserve Board announced an $8.5 billion agreement with various banks such as Bank of America and Citibank regarding foreclosure practices and mortgage loan servicing deficiencies. The agreement was subsequently increased to $9.3 billion in February 2013, with $3.6 in cash payments and $5.7 in homeowner assistance, including loan modifications and forgiveness of deficiency judgments. In February 2012, Bank of America, Citigroup, JPMorgan, Wells Fargo, and Ally Financial had agreed to a $25 billion settlement with 49 state attorneys general and federal agencies such as the US Department of Justice regarding mortgage loan servicing and foreclosure problems. The settlement included approximately $5 billion in cash penalties, with the remaining $20 billion to be provided as relief to homeowners. In December 2011, the US Department of Justice also settled with Bank of America and Countrywide over alleged mortgage lending discrimination from 2004 to 2008, providing $335 million in compensation.

Summary of Settlement Activity

From 2007 through October 2013, defendants have agreed to pay a total of $32 billion to settle various credit crisis-related lawsuits. This total does not include the proposed $8.5 billion settlement of Countrywide MBS litigation and the $7.3 billion proposed settlement ($672 million estimated recovery value) in the ResCap bankruptcy. In addition, financial institutions have settled repurchase demands by Fannie and Freddie for a total of $18 billion. Settlements and agreements between the US government and various banks and servicers related to mortgage lending and loan servicing issues arising from the credit crisis have exceeded $34 billion.

New Filings: New Filings Have Declined as Housing Markets Show Signs of Recovery

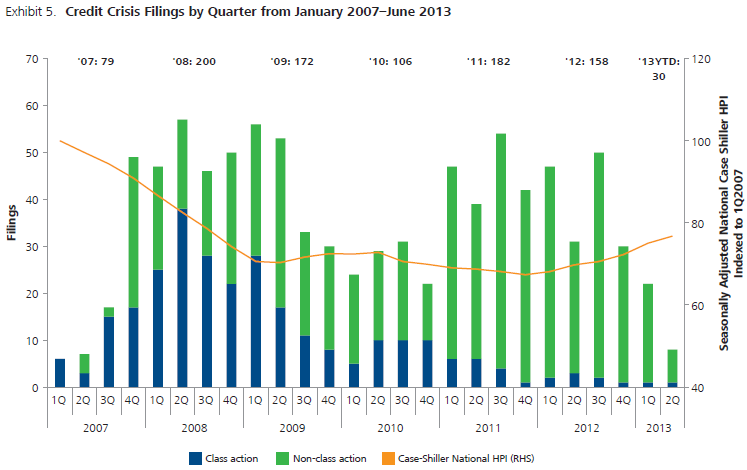

There have been a total of 927 credit crisis-related filings over the period January 2007 through the end of June 2013, with 158 filings in 2012 and 30 filings in the first half of 2013 (60 annualized). In terms of class action matters, there were eight filings in 2012 and two filings in 2013 through June (four annualized). For non-class action matters, there were 150 filings in 2012 and 28 filings in 2013 through June (56 annualized). As the housing markets have started to show signs of improvement, leading to fewer delinquencies and defaults, the pace of new filings has fallen to a fraction of that seen in prior years. This trend is illustrated in Exhibit 5 which presents credit crisis filings by quarter, divided into securities class action lawsuits and other types of lawsuits, along with the seasonally adjusted Case-Shiller national home price index indexed to 1Q2007.

Credit Crisis-Related Breach of Contract Lawsuits Increased Sharply Since 2012

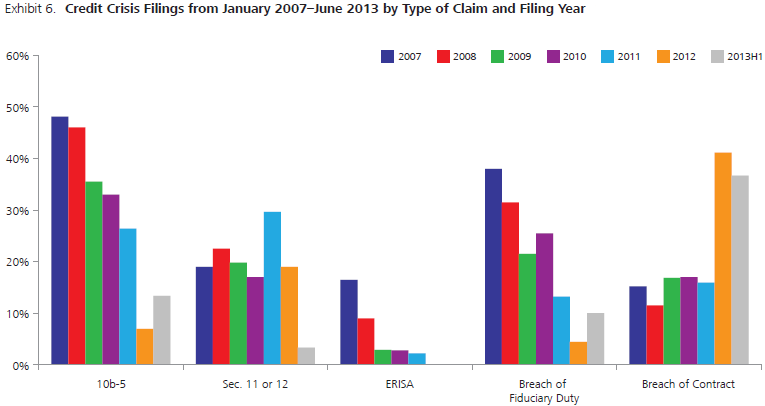

We classify filings by the type of claims. Categories include cases involving claims pursuant to: Rule 10b-5, Sections 11 and 12 from the Securities Act of 1933, the Employee Retirement Income Security Act of 1974 (ERISA), breaches of fiduciary duty, and breaches of contract. Many cases involve allegations under more than one of these statutes. Exhibit 6 below presents the share of annual filings by type of claims from 2007 through the first half of 2013.

Rule 10b-5, promulgated under Section 10b of the Securities Exchange Act of 1934, governs investors who purchased or sold securities of a company which allegedly made “untrue statements of a material fact” or “omit[ted] to state a material fact necessary in order to make the statements… not misleading.” Credit crisis-related 10b-5 lawsuits have decreased from 38 cases in 2007 (or 48% of the credit crisis cases filed in that year) to 11 cases (or 7% of cases) in 2012 and 4 cases (or 13% of cases) in the first half of 2013.

Sections 11 and 12 claims are brought pursuant to the Securities Act of 1933 for alleged material misstatements or omissions in a registration statement or prospectus, respectively. Many of the cases involving claims under Sections 11 and 12 relate to registration statements or prospectuses for mortgage pass-through securities, mutual fund shares, and secondary public stock offerings. Such claims were made in 15 cases (or 19% of cases) filed in 2007 and 30 cases (or 19% of cases) in 2012, but were made in only one of the 30 cases (or 3% of cases) filed so far in the first half of 2013.

The Employee Retirement Income Security Act of 1974 (ERISA) is a federal statute that governs the benefits of pension plans and employee benefit rights. The majority of ERISA cases involve suits brought by plan participants against asset managers, or cases against a company and its executives for offering the company’s stock to plan participants. Credit crisis-related claims alleging a violation of ERISA peaked in 2008 with 18 filings, or 9% of cases filed in that year. None of the credit crisis-related claims filed in 2012 or the first half of 2013 involve ERISA claims.

There were 30 cases involving allegations of breaches of fiduciary duty (or 38% of cases) filed in 2007, 7 cases (or 4%) filed in 2012, and 3 cases (or 10%) filed in the first half of 2013. Allegations of breaches of contract surged from 12 cases (or 15%) filed in 2007 to 65 cases (or 41%) filed in 2012 and 11 cases (or 37%) filed in the first half of 2013, in large part due to filing activity related to investors and insurers of ABS and MBS securities alleging contract claims.

Issuers and Underwriters Continue to Be the Most Frequently Named Defendants in Recent Filings

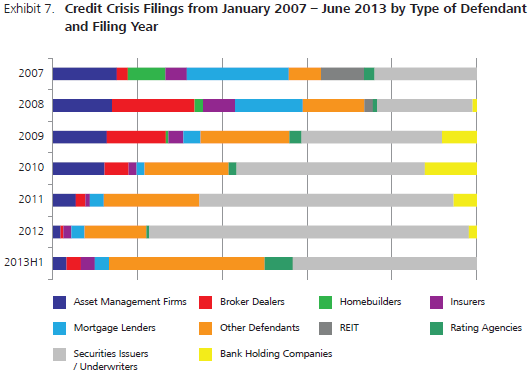

We classify the primary defendants in the credit crisis filings by reviewing complaints and other legal documents. Our classification of the defendants is based on the allegations and the role of the defendants in each case. For example, one firm may be categorized as an issuer/underwriter in a particular lawsuit for packaging and selling mortgage-backed securities. The same firm may then be categorized as a broker/dealer for marketing and selling auction-rate securities (“ARS”) to an investor. Asset management firm defendants may include hedge funds, private equity firms, and investment advisors, among others. Insurers include mortgage and bond insurers. We classify the defendants as securities issuers/underwriters, asset management firms, mortgage lenders, insurers, home builders, broker/dealers, rating agencies, REITs, or others. A breakdown of defendant types by filing year is presented in Exhibit 7.

There has been a noticeable shift in the type of defendants as credit crisis-related litigation has progressed. In 2007, mortgage lenders, home builders, and REITs were named as defendants in 43% of filings. In 2008, mortgage lenders, home builders, and REITs were named in only 20% of filings. Such businesses were named as defendants in just 3% of filings in 2012 and 2013 through June.

Although securities issuers/underwriters were defendants in only 24% and 23% of filings in 2007 and 2008, respectively, filings against these types of defendants increased in both 2009 and 2010. In 2009, securities issuers/underwriters were named in 33% of the filings. In 2010, 44% of filings targeted securities issuers/underwriters, in part due to the wave of litigation against Goldman Sachs and its involvement in synthetic CDOs. By 2011 and 2012, the percentage of credit crisis litigation filed against securities issuers/underwriters rose to 60% and 75%, respectively. In the first half of 2013, 43% of filings were against securities issuers/underwriters.

Filing of Shareholder Suits Has Decreased Since 2008; Lawsuits by MBS/ABS Investors Maintain Strong Share of Activity in 2012 and 2013YTD

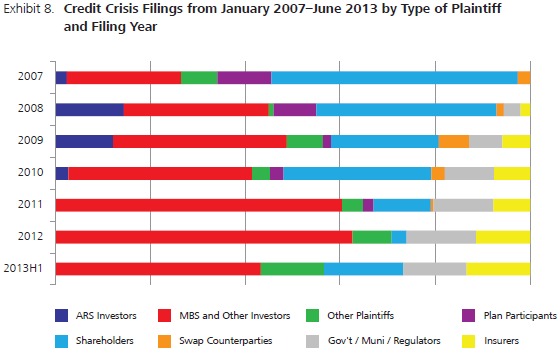

We also classify the types of plaintiffs in the credit crisis filings as shareholders, ARS investors, MBS/other investors, trustees on behalf of investors, plan participants, insurers, swap contract claimants, government/regulators, and other plaintiffs. A breakdown of filings by type of plaintiff by filing year is shown in Exhibit 8.

We define shareholders as common stock owners. ARS investors are those who invested in long-term variable-rate instruments (usually municipal or corporate bonds) whose interest rates are reset through auctions. MBS/other investors are those who invested in MBS, ABS, preferred securities, corporate bonds, mutual funds, and money market funds. Plan participants are generally employees that file ERISA claims. Swap contract claimants are most commonly parties that bring suits regarding disputes over CDS. The government/regulator claims include cases brought by the SEC, state attorneys’ general, cities, and municipalities.

Similar to the trends in the types of defendants named in credit crisis-related cases, the plaintiffs involved in cases have shifted towards investors in MBS and other mortgage-related securities. The share of cases involving MBS/other investors has increased over time, with 39% of cases in 2010, 60% of cases in 2011, 63% of cases in 2012, and 43% of cases in the first half of 2013. Insurers, in particular those who insured MBS and ABS, have also increased filing activity, from 8% of cases in 2010 to 13% of cases in the first half of 2013. See Exhibit 8.

Most Recent Filings Relate to ABS and MBS

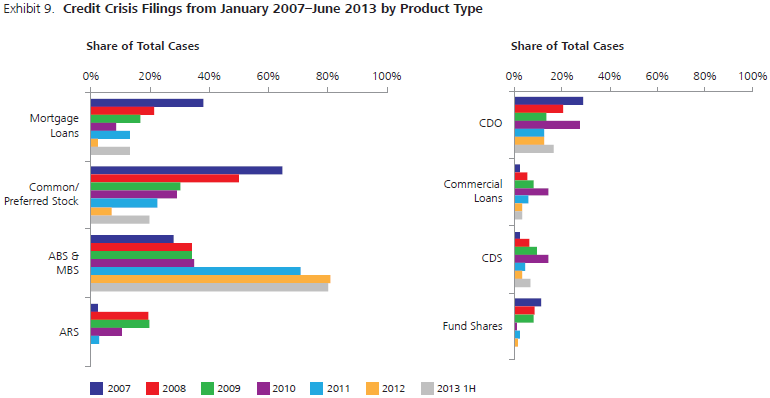

We also classify credit crisis filings according to the type of product or security at issue in the case. These categories are not mutually exclusive and, in many instances, multiple types of securities are involved in each filing. Cases filed in 2007, which tended to involve lenders, originators, and home builders, largely involved claims related to increased accounting provisions (i.e., increases in reserves) for mortgage loans and mortgage loan charge-offs due to impairment. In fact, in 2007, 38% of credit crisis claims involved allegations relating to mortgage loans. By comparison, in 2012, only 3% of claims involved mortgage loans. In the first half of 2013, 13% of claims involved mortgage loans. The majority of recent credit crisis securities lawsuits involve products such as ABS/MBS. In 2012 and the first half of 2013, 81% and 80% of claims involved ABS/MBS, respectively. See Exhibit 9.

Conclusion

We have documented a significant increase in settlement activity related to the credit crisis litigation as well as settlements of Fannie Mae and Freddie Mac’s repurchase demands in recent months. Notwithstanding, many cases remain active and continue to be litigated. Given the recent surge in regulatory settlements and investigations against financial institutions on various issues related to the credit crisis, it is not clear that we have seen the end of this litigation.