Print

PrintThe following post comes to us from Jonathan C. Dickey, partner and Co-Chair of the National Securities Litigation Practice Group at Gibson, Dunn & Crutcher LLP, and is based on a Gibson Dunn publication.

It almost goes without saying that the first half of 2014 brought with it the most significant development in securities litigation in decades: the U.S. Supreme Court decided Halliburton Co. v. Erica P. John Fund, Inc.—Halliburton II. In Halliburton II, the Court declined to revisit its earlier decision in Basic v. Levinson, Inc.; plaintiffs may therefore continue to avail themselves of the legal presumption of reliance, a presumption necessary for many class action plaintiffs to achieve class certification. But the Court also reiterated what it said 20 years ago in Basic: the presumption of reliance is rebuttable. And the Court clarified that defendants may now rebut the presumption at the class certification stage with evidence that the alleged misrepresentation did not affect the security’s price, making “price impact” evidence essential to class certification.

The first half of the year brought other notable developments as well, including the Court’s grant of certiorari in two important cases: Omnicare, Inc. v. Laborers District Council Construction Industry Pension Fund, No. 13-435, and Public Employees’ Retirement System of Mississippi v. IndyMac MBS, Inc., No. 13-640. In Omnicare, the Court is expected to resolve an important circuit split concerning the scope of liability for so-called “false opinions” under Section 11 of the Securities Act of 1933. And in IndyMac, the Court will decide whether the class action tolling doctrine—so-called American Pipe tolling—can be applied to save otherwise barred claims filed by individual investors after a class is denied certification.

Early 2014 also proved a notable period for Delaware law. In a decision welcomed by the defense bar and its clients, the Supreme Court of Delaware held that directors of a non-stock corporation may adopt bylaws shifting attorneys’ fees and costs to unsuccessful plaintiffs in intra-corporate litigation. The Delaware legislature, however, is actively considering whether to undo or otherwise limit that decision. We discuss these and other notable trends in derivative, merger & acquisition, and shareholder proposal disputes in detail below.

For developments related to SEC Enforcement, including a discussion of the Second Circuit’s decision in SEC v. Citigroup Global Markets Inc., please see our Mid-Year SEC Enforcement Update. We also invite you to read our 2014 Mid-Year FCPA Update.

Filing and Settlement Trends

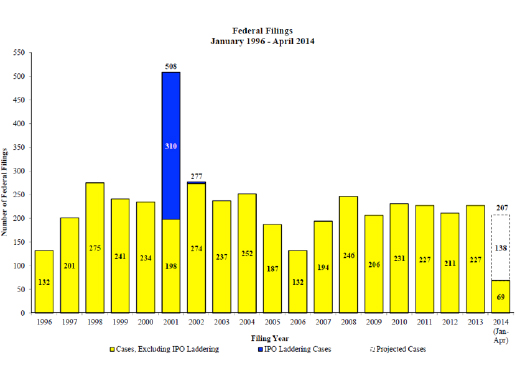

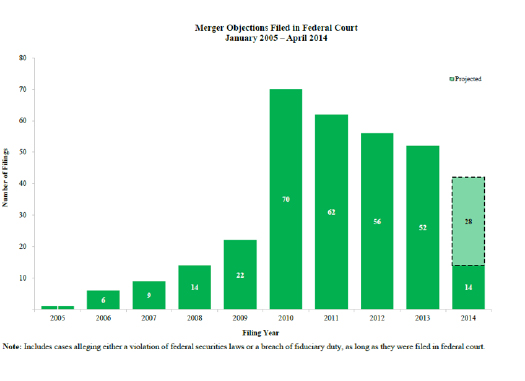

Filing and settlement trends continue to reflect a “steady state” of several hundred cases a year, notwithstanding the virtual disappearance of credit crisis class actions filed in federal court in 2013 from an all-time high of over 100 class actions in 2008. According to a recent study by NERA Economic Consulting (“NERA”), the rate of new class actions filed in the first four months of 2014 annualizes at 207 new class actions, slightly lower than the five-year average of 220 cases, but nevertheless substantial. Importantly, the mix of those cases has changed. For example, in 2013 and the first few months of 2014, there was a steep rise in class actions based on allegedly false and misleading earnings guidance, well above the number of cases alleging accounting fraud. And somewhat counter-intuitively to some commentators, the number of “merger objection” cases (including breach of fiduciary duty cases) is projected to decline in 2014. Indeed the number of such suits has declined each year since 2010. Perhaps this trend represents a flight to state courts; but the trend in federal court, at least, runs counter to the statistics indicating that M&A litigation is on the rise in general.

As well, the aggregate investor losses involved in cases filed in federal court so far in 2014 appear to have shifted to higher levels, with over $50 billion of investor losses falling into the category of cases involving investor losses of $10 billion or higher. And with respect to geography, cases filed in the 9th Circuit are projected to exceed all other Circuits.

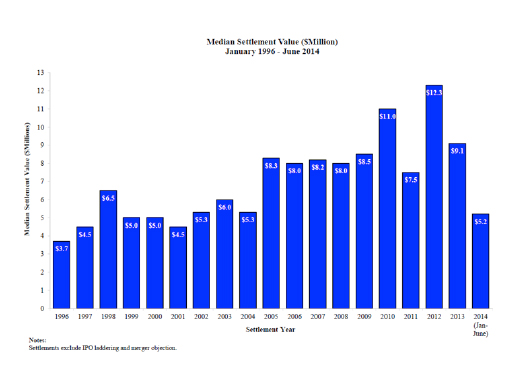

In the first six months of 2014, median settlement values have plummeted from $9.1 million in 2013 to just $5.2 million in the first half of 2014. Over half of the 2014 settlements were less than $10 million, while only 9% of all settlements in 2014 exceeded $50 million. Average settlement amounts also declined in the first six months of 2014, from $68 million in 2013 to $38 million in the first half of 2014. Excluding settlements over $1 billion, the average settlement amount in 2014 still declined, from $55 million to $44 million.

Finally, median settlement amounts as a percentage of investor losses in the first half of 2014 continued to reflect a pattern: the larger the investor losses, the lower the percentage the settlement represents. Indeed, since 1996, investor losses in excess of $400 million have settled for less than 2% of such losses, and that figure drops to below 1% when investor losses exceeded $10 billion.

As discussed in later sections of this Year-End Report, the Supreme Court’s decision in Halliburton II may affect filing and settlement trends in the future. Although Halliburton II upheld the “fraud on the market” theory, it also raised the bar on the proof required at the class certification stage to establish that allegedly misleading statements caused any “price impact.” Class certification rulings in the next year will shed light on whether this “price impact” test will have a material effect on class action filings or settlements.

Class Action Case Filing Trends

Overall filing rates are reflected in Figure 1 below (all charts courtesy of NERA). Sixty-nine cases were filed in the period January through April 2014, which annualizes to 207 cases for the full year. This figure does not include the many such class suits filed in state courts or the increasing number of state court derivative suits, including many such suits filed in the Delaware Court of Chancery. These cases, however, represent a “force multiplier” of sorts in the dynamics of securities litigation in the United States today.

Figure 1:

Mix of Cases Filed in 2014

Credit Crisis Cases. There were almost no new federal court class actions filed against financial institutions in the first few months of 2014, reflecting the dramatic decline of “credit crisis” class actions since 2008. While a number of major credit crisis cases are still pending, the trend line is expected to continue: like stock option “backdating” cases, credit crisis class actions will soon be consigned to history. That said, while credit crisis class actions are on the wane, a new generation of cases have replaced them: single-plaintiff suits by government agencies (such as the Federal Housing Finance Agency on behalf of Fannie Mae and Freddie Mac), monoline insurers (such as MBIA), and institutional and pension fund investors. A few have already resulted in settlements in excess of $100 million.

Merger Cases. “Merger objection” cases represent a significant portion of new federal court securities class action filings in 2013 and 2004. NERA reports that in 2013, there were 52 merger-related cases. Filings in 2014 are projected to be 42, down from 2013, and significantly down from the 70 such cases in 2010. As discussed below in our discussion of “Merger & Acquisition and Proxy Disclosure Litigation Trends,” the exposure of corporations to M&A litigation spans a range of subject matters, with sometimes unpredictable results. Those results may become even less predictable in light of the fact that the new Chief Justice of the Delaware Supreme Court, Leo Strine, has shown a willingness to “break new ground” in his rulings in cases before him in the Chancery Court.

Figure 2:

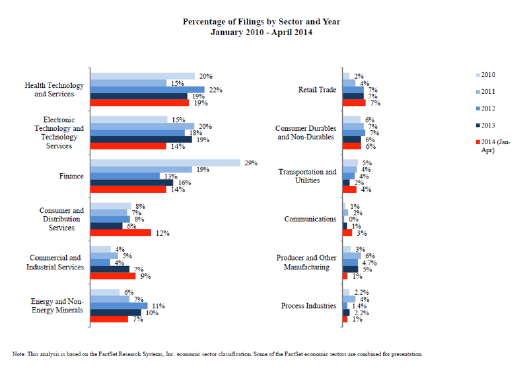

Filings By Industry Sector. The trends in new case filings against particular industry sectors reflect the decline in “credit crisis” cases, as new suits against financial institutions have dropped from record-shattering levels in 2009 to a second place tie with the technology sector in the first few months of 2014 (each with 14% of all new case filings), behind the health technology sector (19% of new case filings). The consumer products sector ranked fourth (12%). The biggest jump in new case filings on a percentage basis compared to 2013 was in the consumer sector, where new filings doubled from their 2013 levels. See Figure 3 below.

Figure 3:

Class Action Settlements

As Figure 4 shows, the median settlement amount of $5.2 million in 2014 to date—generally a better barometer of settlement trends—was hugely down compared to 2013, and the lowest figure in the last decade.

Figure 4:

One can speculate about what may account for the up-and-down fluctuation in median and average settlements over the last five years. In any given year, of course, the statistics can mask a number of important factors that contribute to settlement value, such as (i) the amount of D&O insurance; (ii) the presence of parallel proceedings, including government investigations and enforcement actions; (iii) the nature of the events that triggered the suit, such as the announcement of a major restatement; (iv) the range of provable damages in the case; and (v) whether the suit is brought under Section 10(b) of the Exchange Act or Section 11 of the Securities Act. The last few years also included the settlement of a number of the major credit crisis cases totaling several billion dollars. Whatever the variables, median and average settlement amounts over the last decade should not be viewed as a barometer of either a long-term increase or decline in settlement values.

The Supreme Court Decides Halliburton II: Fraud-On-The-Market Survives, But Defendants Have a New Tool in Defeating Class Certification

The first half of 2014 was headlined by the Supreme Court’s much-anticipated decision in Halliburton Co. v. Erica P. John Fund, Inc. (Halliburton II), 134 S. Ct. 2398 (2014). As we explained in our June 23, 2014 alert, in Halliburton II the Court held that the presumption of reliance—i.e., the “fraud on the market” theory of Basic Inc. v. Levinson, 485 U.S. 224 (1988)—will remain a part of the securities class-action landscape. [1] At the same time, however, the Court offered the defense bar a considerable tool in challenging class certification, holding that the presumption of reliance may be rebutted at the class certification stage with evidence that each challenged misrepresentation did not affect the market price of the security at issue.

While the effects of Halliburton II remain to be seen, several aspects of the opinion are particularly notable from the defense perspective.

First, securities plaintiffs bear the burden of establishing the predicates to the Basic presumption—publicity, materiality, market efficiency, and market timing—and as to all but materiality, plaintiffs must prove these prerequisites at the class certification stage. This is nothing new. But once defendants rebut the presumption with direct evidence that an alleged misrepresentation did not impact the subject security’s price, plaintiffs must produce evidence that it did. Trial courts will therefore be required to resolve the “battle of the experts” at the certification stage. This necessarily follows from the Court’s recent class action jurisprudence—including Wal-Mart Stores, Inc. v. Dukes, 131 S. Ct. 2541 (2011), and Comcast Corp. v. Behrend, 133 S. Ct. 1426 (2013)—which hold that plaintiffs must prove all the elements of class certification by a preponderance of the evidence, and district courts must make findings as to each. As the Court explained in 2013, “the ‘class determination generally involves considerations that are enmeshed in the factual and legal issues comprising the plaintiff’s cause of action.'” Comcast, 133 S. Ct. at 1432 (quoting Dukes, 131 S. Ct. at 2551). Halliburton II makes clear that the same principle extends to securities class actions. Thus, after Halliburton II, while defendants may bear the initial burden of producing price impact evidence, plaintiffs bear the ultimate burden of proving all the prerequisites of the fraud-on-the-market doctrine.

Second, a court considering the issue of price impact at class certification must evaluate the issue on a misrepresentation-by-misrepresentation basis. As the Court explained, the Basic presumption “does not require courts to ignore a defendant’s direct … evidence showing that the alleged misrepresentation did not actually affect the stock’s market price.” Halliburton II, 134 S. Ct. at 2416. The defendant may introduce event studies or other evidence regarding the effect on market prices of each alleged misrepresentation. Without a price impact, the presumption of reliance lacks an essential predicate and the plaintiffs must then prove actual reliance as to particular alleged misstatements—a significant hurdle. The result is an opportunity to narrow the potential class at a much earlier stage than was previously permitted.

Omnicare: U.S. Supreme Court to Decide Whether a Section 11 “False Opinion” Claim Requires Proof That the Speaker’s Opinion Was Not Genuinely Held

In March of this year, the Supreme Court granted certiorari in Omnicare, Inc. v. Laborers District Council Construction Industry Pension Fund, No. 13-435, a case expected to resolve an important circuit split concerning the scope of liability for so-called “false opinions” under Section 11 of the Securities Act of 1933. Section 11 gives investors a private right of action to recover damages based on an “untrue statement of a material fact” in, or the omission of a material fact from, a securities registration statement. As we explained in our 2013 Year-End Securities Litigation Update, the question in Omnicare is whether plaintiffs alleging an untrue statement of opinion—in contrast to a statement of “hard fact”—must plead and prove not just objective falsity, but also subjective falsity, i.e., that the person offering the opinion actually believed it to be false.

At issue in Omnicare is a registration statement in which the company stated a belief that it was in compliance with applicable laws. The plaintiffs allege that this belief was “untrue” under Section 11 largely because of pending lawsuits claiming that the issuer violated federal law through its contracts with business partners. The Omnicare plaintiffs’ complaint contains no allegation that the defendants did not, in fact, honestly believe that the company was complying with applicable laws when the registration statement was filed. Instead, they contend that Section 11 does not require proof of subjective falsity for statements of opinion. A panel of the Sixth Circuit agreed, parting ways with the Second, Third, and Ninth Circuits.

Notably, the Securities and Exchange Commission and Department of Justice submitted an amicus brief in support of the plaintiffs’ position. The brief argues that an opinion included in a registration statement that “lacked a basis that was reasonable under the circumstances” should give rise to Section 11 liability regardless of whether the opinion was honestly held. Br. for U.S. as Amicus Curiae at 5, Omnicare, No. 13-435 (U.S. June 12, 2014). This is so, the brief argues, because investors would expect that an issuer had undertaken “significant investigation” of an opinion in a registration statement to ensure it “has a solid foundation.” Just what constitutes such an investigation and resulting foundation is unclear. The government has argued, however, that the Sixth Circuit went a step too far and erred “in suggesting that a statement of opinion is actionable whenever it is ultimately proved incorrect.” Industry groups have filed their own amicus briefs urging reversal of the Sixth Circuit decision. Those groups argue that the Sixth Circuit’s approach will improperly expand liability under Section 11 and impose an unclear duty to investigate with respect to any opinion offered in a registration statement, and create hindsight-based liability for inherently subjective opinions that must often be included in registration statements.

Although the Omnicare case concerns only a Section 11 claim, as discussed in our 2013 Year-End Securities Litigation Update, the question of what a plaintiff must plead and prove to establish liability for an alleged false opinion also arises in other securities law claims. For example, the Second Circuit has applied the subjective falsity requirement to claims brought under Section 10 of the Securities Exchange Act and Rule 10b-5 (which in contrast to Section 11 claims, do require a pleading of scienter). See, e.g., City of Omaha, Neb. Civilian Employees’ Ret. Sys. v. CBS Corp., 679 F.3d 64, 68-69 (2d Cir. 2012) (applying the subjective falsity requirement to statements regarding goodwill valuation); see also Freeman Grp. v. Royal Bank of Scot. Grp., 540 F. App’x 33, 38 (2d Cir. 2013) (summary order) (applying the subjective falsity requirement to statements regarding capital adequacy, risk management procedures, and expected benefits of an acquisition). As one district court recently put it, regardless of whether a claim is brought under Section 11 or Rule 10b-5, “[o]ne legal proposition governs both sets of claims: statements that are matters of opinion must be ‘both objectively and subjectively false’ at the time that they were made in order to be actionable.” In re Puda Coal Sec. Inc. Litig., No. 11-cv-2598 (KBF), 2014 WL 2915880, at *11 (S.D.N.Y. June 26, 2014) (quoting Fait v. Regions Fin. Corp., 655 F.3d 105, 111 (2d. Cir. 2011))

Therefore, the Supreme Court’s opinion in Omnicare could have wide-ranging consequences. A decision siding with the Sixth Circuit could effectively loosen pleading requirements, expand liability for statements of opinion, and leave issuers with little guidance as to what constitutes an adequate basis for a statement of opinion. On the other hand, a decision adopting the view held by the majority of circuits would provide some assurance that officers, directors, underwriters, accountants, and others cannot be subject to liability for opinions and professional judgments that were offered in good faith but later prove to be inaccurate. We expect the Supreme Court to resolve this important circuit split when it hears and decides Omnicare during the upcoming October 2014 term.

Supreme Court to Decide Reach of American Pipe Tolling in Indymac

In another important securities case to be heard in the upcoming term, the Supreme Court will have the opportunity to decide whether the class action tolling doctrine of American Pipe & Construction Co. v. Utah, 414 U.S. 538 (1974), applies to the three-year statute of repose for claims under the Securities Act of 1933. “American Pipe tolling” provides that “the commencement of a class action suspends the applicable statute of limitations as to all asserted members of the class who would have been parties had the suit been permitted to continue as a class action.” Id. at 554. As noted in our 2013 Mid-Year Securities Litigation Update, the Second Circuit last year held that tolling does not apply to the three-year statute of repose in Section 13 of the Securities Act. The Supreme Court granted certiorari in that case, see Pub. Emps.’ Ret. Sys. of Miss. v. IndyMac MBS, Inc., No. 13-640, teeing up for resolution a question with significant consequences for both plaintiffs and defendants. [2]

Section 13 provides two separate limitations periods applicable to actions based on misstatements or omissions in connection with the public offering of securities. The first is a one-year period running from the date by which a misstatement or omission was discovered or should have been discovered through reasonable diligence. The second is a three-year period running from the effective date of a registration statement for Section 11 claims or from the sale of a security in an initial offering for a Section 12(a)(2) claim: after that time, “[i]n no event shall any such action be brought to enforce a liability created under [this title].” 15 U.S.C. § 77m. The Second Circuit held that this three-year limitation period is an absolute bar to liability and is therefore not subject to tolling. That outcome was in line with past Supreme Court precedent, which holds that the three-year bar is “inconsistent with tolling.” See Lampf, Pleva, Lipkind, Prupis & Petigrow v. Gilbertson, 501 U.S. 350, 363 (1991).

The question now before the Supreme Court is whether the principle from American Pipe—a doctrine of tolling that applies specifically to statutes of limitations in class action lawsuits—would similarly apply to Section 13’s statute of repose. The petitioner argues that the Second Circuit’s ruling undermines the main purpose of American Pipe and class actions generally—to put the defendant on notice of potential plaintiffs and their claims and to avoid duplicative suits. But, as the Second Circuit held and the respondent argues, the purposes behind Section 13’s repose provision are nuanced, and American Pipe does not clearly apply.

The Second Circuit left open the question of whether American Pipe tolling is an “equitable” rule or, instead, a “legal” rule stemming from Federal Rule of Civil Procedure 23. In either scenario, American Pipe may not apply to Section 13’s statute of repose. If the American Pipe tolling rule is equitable, Lampf would explicitly bar its application. If legal, the Rules Enabling Act forbids expanding substantive rights under Rule 23. The petitioners and various amici disagree, arguing that tolling Section 13 under American Pipe is consistent with the Rules Enabling Act because a statute of repose is no different from a statute of limitations.

Whatever the outcome, the Supreme Court’s decision will have a significant impact on both securities issuers and potential claimants. In the coming year, we will monitor IndyMac and its consequences and report any significant developments.

Comcast: Another Hurdle for Plaintiffs in Securities Class Actions

In our 2013 Year-End Securities Litigation Update, we reported that lower courts had begun to scrutinize securities class actions, and particularly allegations of class-wide damages, based on the Supreme Court’s decision in Comcast Corp. v. Behrend. That trend continued in the first half of 2014, with more courts expressly requiring putative class plaintiffs to satisfy what Comcast described as the “rigorous” and “demanding” predominance requirement of Rule 23(b)(3). Even setting aside Halliburton II and the likelihood of “mini-trials” on price impact, class certification proceedings are increasingly becoming more fact-intensive, prompting savvy defendants to oppose certification by presenting their own evidence—often through expert witnesses—to show that “[q]uestions of individual damage calculations will inevitably overwhelm questions common to the class.” Comcast, 133 S. Ct. at 1433. Comcast-based challenges do not always succeed, but defendants in securities cases are finding an increasingly receptive audience in the courts.

Three recent decisions illustrate these developments. In the first, In re Kosmos Energy Ltd. Securities Litigation, No. 3:12-CV-373-B, 2014 WL 1293834 (N.D. Tex. Mar. 19, 2014), the court explicitly recognized that although Comcast was an antitrust case, its lessons apply equally in the securities context. According to the court, “[g]oing forward, the clear directive to plaintiffs seeking class certification—in any type of case—is that they will face a rigorous analysis by the federal courts.” Id. at *4. Comcast, the court said, signaled a move “away from a presumptively pro-plaintiff view” of class actions. Id. at *15. As a result, plaintiffs now “must be prepared to prove with facts—and by a preponderance of the evidence—their compliance with the requirements of Rule 23.” Id. (emphasis in original).

Applying these standards, the court rejected the proposed class. Critical to the court’s decision was the defendant’s detailed evidence opposing certification, including a “107-page Expert Report demonstrating the need for individual inquiries into investor knowledge.” Id. at *18. The plaintiffs, in contrast, offered little evidence of their own, instead urging the court to “presume that the proposed class is certifiable simply because of the securities law provisions pursuant to which this case was filed.” Id. at *15 (emphasis in original). This showing was “simply not enough.” Id. at *16. Under Comcast, “plaintiffs seeking certification must produce quality evidence for each Rule 23 element—period.” Id. at *15.

In another case, a different court again emphasized the evidence-intensive nature of the predominance inquiry. In Dodona I, LLC v. Goldman, Sachs & Co., 296 F.R.D. 261 (2014), after submission of substantial evidence on both sides, the court ultimately credited the plaintiffs’ expert report “demonstrat[ing] that calculation of individual class members’ damages will rely on common methodology.” Id. at 270. The court further found that because all members of the proposed class purchased securities “pursuant to the same set of Offering Circulars containing the same alleged omissions, … common issues of generalized proof will predominate.” Id.

A final decision, In re BP p.l.c. Securities Litigation, No. 10-md-2185, 2014 WL 2112823 (S.D. Tex. May 20, 2014), revisited a prior ruling discussed in our 2013 Year-End Securities Litigation Update. Although, as we reported, the court had previously rejected certification, plaintiffs re-urged their motion, splitting their claims into two subclasses: one three-year subclass that included the lion’s share of the allegations, and a smaller subclass spanning only a single month. After conducting an in-depth examination of the parties’ evidentiary submissions, the court rejected the larger subclass. The calculation of damages for that subclass required proof of whether and when individual class members might have chosen to divest. According to the court, this “proposed measurement of damages cannot be deployed without an individualized inquiry into each investor’s subjective motivation,” making “[c]lasswide treatment … patently inappropriate.” Id. at *12.

The court then certified the smaller subclass—but with reservations. The court expressed “concern[] regarding the apparent disconnect between some corrective events and the [alleged] fraud.” Id. at *13. But because, at the class certification stage, plaintiffs were required only to “present a legally viable, internally consistent, and truly classwide approach to calculating damages,” the court reserved “for a different day” the question “[w]hether Plaintiffs have properly executed” their chosen approach. Id. (emphasis in original).

Comcast will no doubt remain an important tool for defendants opposing class certification. As these cases illustrate, the best defense is often a strong offense: a robust evidentiary presentation showing class certification to be inappropriate.

Chadbourne & Parke LLP v. Troice: Did the Floodgates Really Open?

In our February 28, 2014 alert, we discussed the Supreme Court’s decision in Chadbourne & Parke LLP v. Troice, 134 S. Ct. 1058 (2014), which interpreted an important provision of the Securities Litigation Uniform Standards Act (“SLUSA”). SLUSA bars state law claims based on “a misrepresentation or omission of a material fact in connection with the purchase or sale of a covered security.” 15 U.S.C. § 78bb(f)(1) (emphasis added). In Troice, the Court defined the phrase “in connection with” to require that the misrepresentation or omission must be “material to a decision by one or more individuals (other than the fraudster) to buy or sell a ‘covered security.'” 134 S. Ct. at 1066. There has been debate about whether this opinion will open the floodgates to plaintiffs asserting state law claims. Over the first half of 2014, however, it appears that Troice has had less of an impact on the securities litigation landscape than some may have predicted.

Very few cases have interpreted and applied Troice‘s reasoning. In cases based upon the Madoff feeder fund Ponzi scheme reconciliation, the court applied the holding from Troice to reconsider—but ultimately reaffirm—the SLUSA bar on potential state-law claims. In In re Herald, Nos. 12-156-cv (L), 12-162, 2014 WL 2199774 (2d Cir. May 28, 2014) (per curiam), the court denied the plaintiffs’ petition for rehearing, which was predicated on Troice, and affirmed the application of SLUSA to forbid plaintiff’s state-law claims. The key difference from Troice, the court held, was that in the Madoff scheme, the victims were seeking to purchase “covered securities,” while the Troice victims believed they were purchasing Certificates of Deposit, which are specifically excluded from SLUSA.

In at least one Madoff-related case, however, Troice‘s definition of “in connection with” revived previously banned state-law claims. In In re Tremont Securities Law, State Law, & Insurance Litigation, Nos. 08 Civ. 11117, et al., 2014 WL 1465713 (S.D.N.Y. Apr. 14, 2014), the plaintiffs believed they had purchased a limited partnership interest in certain funds, not an ownership interest in “covered securities” under SLUSA. The court followed Troice in allowing state-law claims to proceed based on the type of interest the victims believed they were buying.

The few courts that have applied Troice have consistently held that the controlling factor is the victim’s perception of what type of security is involved. Early concerns that Troice would cause a significant increase in state-law claims have yet to be borne out; for now, the claims appear to be more of a trickle.

Foreign Purchasers: Courts Continue To Restrict Extraterritorial Suits under Morrison

Second Circuit Delivers a Blow to the Cross-Listing Theory

In the seminal case Morrison v. National Australia Bank Ltd., 561 U.S. 247 (2010), the Supreme Court held that the anti-fraud provisions of the Exchange Act apply only to “transactions in securities listed on domestic exchanges” (prong one) and “domestic transactions in other securities” (prong two). Id. at 249. Lower courts continue to grapple with that holding, and over the first half of this year, many lower courts issued decisions interpreting the types of securities transactions that satisfy (or fail to satisfy) the two-pronged Morrison test. In particular, the Second Circuit issued an opinion in City of Pontiac Policemen’s and Firemen’s Retirement System v. UBS AG (UBS), 752 F.3d 173 (2d Cir. 2014), which may have important implications for securities actions across the country.

In UBS, a case we previewed in our 2013 Mid-Year Securities Litigation Update, the Second Circuit affirmed the dismissal of various securities fraud claims for failing to satisfy Morrison. The plaintiffs contended that the securities transactions in which they had engaged fell within the “express terms” of the first Morrison prong—even though the plaintiffs had purchased their securities on a foreign exchange—because the securities at issue were cross-listed on a U.S. exchange. The Second Circuit rejected the plaintiffs’ “cross-listing” theory and its literal application of the Morrison holding. The court found instead that Morrison, “read as a whole,” focused on the “location of the securities transaction” itself and not the “location of the exchange where the security may be dually listed.” Id. at 180 (second emphasis added). The UBS court further found that the first Morrison prong was intended to serve “as a proxy for a domestic transaction,” and therefore held that Section 10(b) does not apply to “claims by a foreign purchaser of foreign-issued shares on a foreign exchange simply because those shares are also listed on a domestic exchange.” Id. at 180-81.

In addition, the UBS court held that the transactions at issue did not fall within the second Morrison prong because they were not “domestic” transactions. In the Second Circuit, a plaintiff may plead the existence of a “domestic” transaction by alleging facts sufficient to suggest “that irrevocable liability was incurred or title was transferred within the United States.” Absolute Activist Value Master Fund Ltd. v. Ficeto, 677 F.3d 60, 68 (2d Cir. 2012). In UBS, the court held that a plaintiff does not satisfy this test by alleging that the plaintiff placed “buy orders” in the United States. UBS, 752 F.3d at 181; cf. United States v. Mandell, 752 F.3d 544, 549 (2d Cir. 2014) (finding that there was sufficient evidence of a domestic transaction where investors “were required to submit purchase applications and payments to the company in the United States”).

Consistent with UBS, lower courts have emphasized that the placement of a purchase order in the United States may permit a finding of irrevocable liability sufficient to satisfy the second Morrison prong, but only when this fact is combined with other factors not present in UBS. See Atlantica Holdings, Inc. v. Sovereign Wealth Fund Samruk-Kazyna JSC, No. 12 Civ. 8852 (JMF), 2014 WL 917055, at *8-9 (S.D.N.Y. Mar. 10, 2014) (finding that plaintiffs pleaded irrevocable liability by alleging that plaintiffs had placed orders with brokers in the United States and that orders were transmitted to broker-dealers in the United States); Butler v. United States, No. 13-CV-4639, 2014 WL 216476, *10-11 (E.D.N.Y. Jan. 17, 2014) (finding irrevocable liability, in part, because defendant “made the[] purchases and sales on behalf of his clients, pursuant to instructions made to him in New York”); cf. SEC v. Amerindo Inv. Advisors, Inc., No. 05 Civ. 5231(RJS), 2014 WL 405339, at *5-8 (S.D.N.Y. Feb. 3, 2014) (finding that the location of the purchaser determined the location of the transaction at issue).

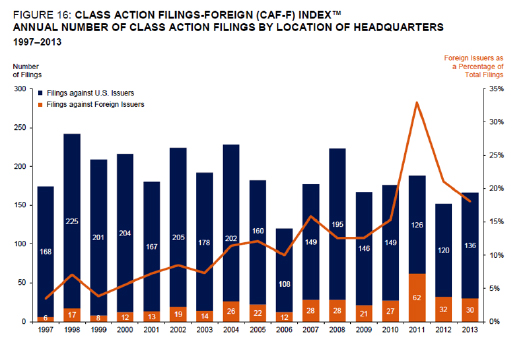

Trends in Suits Against Foreign Issuers

In light of this trend towards a more restrictive extraterritorial application of the anti-corruption provisions of the Exchange Act, it is perhaps no surprise that the number of new federal securities class action filings against foreign issuers (i.e., companies headquartered outside of the United States) has decreased in recent years. According to Cornerstone Research, the number of federal securities class action filings against foreign issuers decreased to 18 percent of all new federal securities class action filings in 2013, down from 21 percent in 2012 and 33 percent in 2011 (chart courtesy of Cornerstone Research).

In future Securities Litigation Updates, we will continue to monitor and report trends relating to the application of the Exchange Act’s anti-fraud provisions to extraterritorial securities transactions and defendants’ efforts to rebut the “fraud-on-the-market” presumption for dually-listed securities.

Shareholder Derivative and Intra-Corporation Litigation Trends

Fee-Shifting Bylaws

A recent decision of the Supreme Court of Delaware may give Delaware corporations an important tool to discourage meritless shareholder litigation, but Delaware lawmakers are actively considering whether to enact legislation to limit the effects of the decision. In ATP Tour, Inc. v. Deutscher Tennis Bund, 91 A.3d 554 (Del. 2014), the Supreme Court of Delaware held that the directors of a non-stock corporation may adopt bylaws that shift attorneys’ fees and costs to unsuccessful plaintiffs in intra-corporate litigation.

Answering questions certified to it by a federal district court, the Supreme Court of Delaware ruled that fee-shifting bylaw provisions are not invalid per se and may be enforceable against members of a non-stock corporation who joined the corporation before the bylaw provision was adopted. The court reasoned that a “bylaw that allocates risk among parties in intra-corporate litigation” is within the permissible scope of bylaws in general because it relates to “the business of the corporation, the conduct of its affairs, and its rights or powers or the rights or powers of its stockholders, directors, officers, or employees.” Id. at 558. Additionally, bylaws operate as a contract among a corporation’s shareholders and are generally enforceable against members who joined the corporation before the bylaws were adopted. Id. at 558-59.

The court cautioned that fee-shifting bylaw provisions could be unenforceable if they were “adopted for an improper purpose.” Id. at 559. For example, the court noted that it had declined to enforce bylaws that were adopted for the purpose of entrenching directors or obstructing the rights of shareholders to undertake a proxy contest against management. Significantly, however, the court held that “[t]he intent to deter litigation … is not invariably an improper purpose.” Id.

Despite this significant ruling, the future of fee-shifting bylaws remains uncertain in Delaware. First, it is unclear whether ATP‘s rule applies to stock corporations as well as non-stock corporations, though the court’s reasoning strongly suggests that it does. More significantly, the Delaware legislature is considering amending Delaware law to limit the impact of the decision. Within weeks of the decision, the Corporation Law Section of the Delaware State Bar Association proposed legislation that would prohibit stock corporations from adopting fee-shifting provisions in either a certificate of incorporation or bylaws. See S.B. 236, 147th Gen. Assemb., Reg. Sess. (Del. 2014), available at http://tinyurl.com/ltdx2e3. On June 18, 2014, the Delaware Senate withdrew the proposed legislation to allow for continued examination of the issues, including whether adoption of similar amendments would be appropriate during the Delaware General Assembly’s next session in early 2015. The Delaware Senate resolution calling for continued examination of the amendments, however, suggests that the Delaware Senate supports the proposed law and is likely to adopt legislation limiting fee-shifting provisions. The preamble of that resolution states that Delaware “strongly support[s] a level playing field” and “a proliferation of broad fee-shifting bylaws for stock corporations will upset the careful balance that [Delaware] has strived to maintain.” S.J. Res. 12, 147th Gen. Assemb., Reg. Sess. (Del. 2014), available at http://tinyurl.com/lh3jt2n.

Forum-selection Bylaw Cases

As discussed in our 2013 Year-End Securities Litigation Update, last year courts across the country issued decisions upholding the facial validity of corporate bylaws that select the Delaware Court of Chancery as the exclusive forum for litigation relating to the company’s internal affairs, including shareholder derivative suits. See Boilermakers Local 154 Ret. Fund v. Chevron Corp., 73 A.3d 934 (Del. Ch. 2013); see also Hemg Inc. v. Aspen Univ., No. 650457/13, 2013 WL 5958388 (N.Y. Sup. Ct. Nov. 4, 2013); In re MetroPCS Commc’ns, Inc., 391 S.W.3d 329 (Tex. App. 2013).

The trend of upholding forum-selection bylaws continued in the first half of 2014. In an Illinois state court action, the court granted a motion to dismiss as a result of a forum-selection provision, holding that “the [forum] selection bylaw passed by the Board of directors is enforceable and … properly precludes litigation of Plaintiff’s claims in Illinois.” Report of Proceedings Held Before the Honorable Jean Prendergast Rooney at 38, Miller v. Beam Inc., No. 2014 CH 00932 (Ill. Cir. Ct. March 5, 2014). A California state court also dismissed a derivative action because the company’s forum-selection clause “contractually obligated [plaintiffs] to bring their claims … only in the Delaware Court of Chancery.” Groen v. Safeway Inc., No. RG14716641 (Cal. Super. Ct. Alameda County May 14, 2014). Plaintiffs had brought a derivative action on behalf of Safeway Inc. alleging directors and officers breached their fiduciary duties in connection with Cerberus’s acquisition of Safeway. Safeway’s bylaws contained a forum-selection clause that designated the Delaware Court of Chancery as the “sole and exclusive forum” for “any action asserting a claim for breach of fiduciary duty owed by, or other wrongdoing by, any director or officer of the corporation … to the corporation’s shareholders.” Id. In dismissing the case, the California court applied Boilermakers and held that plaintiffs had failed to demonstrate that application of the forum-selection bylaws would be unreasonable under the facts. Id.

More decisions concerning forum-selection bylaws are expected in the months ahead. For example, the Delaware Court of Chancery may soon decide whether a Delaware corporation may designate a non-Delaware forum as its exclusive forum. See Verified Stockholder Class Action Compl. at 12-13, City of Providence v. First Citizens BancShares, Inc., No. 9795, 2014 WL 2799011 (Del. Ch. June 19, 2014). The City of Providence, Rhode Island—acting as a shareholder—recently filed the action challenging the validity of a bylaw provision designating North Carolina as the exclusive forum for any derivative lawsuit, claim of breach of fiduciary duty, or any action arising under Delaware corporate law. The defendant, a Delaware corporation, adopted the forum-selection provision before announcing a merger. Providence claims that the bylaw improperly forecloses Delaware courts’ ability to oversee the corporation, including litigation related to the merger and matters over which the Chancery Court has exclusive jurisdiction, such as shareholder books and records actions.

Recent Demand Futility Decisions: Defendants Prevail in Most Cases

In the first half of 2014, several shareholder derivative plaintiffs claimed demand was excused because the board of directors was interested in the compensation plan being challenged in the litigation. Courts dismissed most of these cases, holding that demand was not excused because the claims related to executive compensation under the plan and, in any event, the plaintiffs had not adequately alleged that the compensation was material to the directors.

For example, in New Jersey Building Laborers Pension Fund v. Ball, No. 11-1153-LPS-SRF, 2014 WL 1018210 (D. Del. Mar. 13, 2014), the plaintiffs challenged an incentive compensation plan approved by shareholders, alleging that the related proxy solicitation was misleading. Id. at *2. The report and recommendation of the magistrate judge, which the plaintiffs did not challenge, concluded that demand was not excused even though the directors received compensation under the plan. Id. at *3-5. As the magistrate’s report explained, “[a]n allegation that directors are compensated for their services as directors is not necessarily enough to establish director interest under Delaware law,” and there was no allegation that the director compensation in the plan exceeded compensation for directors at peer corporations. Id. at *4. Other cases produced similar results. See In re Caterpillar Inc. Derivative Litig., No. 12-1076-LPS-CJB, 2014 WL 2587479 (D. Del. June 10, 2014) (report and recommendation of mag. j.); Kaufman v. Alexander, No. 11-00217-RGA, 2014 WL 1623824 (D. Del. Apr. 23, 2014); Freedman v. Mulva, No. 11-686-LPS-SRF, 2014 WL 975308 (D. Del. Mar. 12, 2014).

However, the Delaware Court of Chancery recently held that where a derivative action challenged board action granting compensation to directors, the directors were interested for purposes of demand futility regardless of whether the compensation was material. In Cambridge Retirement System v. Bosnjak, No. 9178-CB, 2014 WL 2930869 (Del. Ch. June 26, 2014), a shareholder derivative plaintiff claimed that directors breached their fiduciary duties and wasted corporate assets by awarding themselves two forms of compensation: (1) equity awards that were approved by shareholders, and (2) cash compensation that was not. The Chancery Court held that demand was excused because the directors were interested in the transaction. The court explained, “where self-dealing is present, a plaintiff need not plead that a director’s interest in a challenged transaction is material to him to establish that the director has a disabling interest.” Id. at *4. The court, however, dismissed plaintiff’s claims related to the equity awards under Rule 12(b)(6) because plaintiff failed to plead facts to legitimately call into question the validity of the stockholders’ approval of the equity awards or to rebut the presumption of the business judgment rule. Id. at *7.

Plaintiffs also argued in numerous cases in the first half of 2014 that demand was excused because the directors faced a substantial likelihood of personal liability. Courts repeatedly rejected these arguments, holding that plaintiffs failed to allege the substantial likelihood with sufficient particularity. See, e.g., Morello v. McGee, No. 3:13cv586 (JBA), 2014 WL 2196406 (D. Conn. May 27, 2014); Canty v. Day, Nos. 13 Civ. 5629 (KBF), 13 Civ. 5977 (KBF), 2014 WL 1388676 (S.D.N.Y. Apr. 9, 2014); La. Mun. Police Emps. Ret. Sys. v. Wynn, No. 2:12-CV-509 JCM (GWF), 2014 WL 994616 (D. Nev. Mar. 13, 2014). These cases routinely reaffirmed that the directors’ membership on an audit committee (or other committee) alone was not enough to imply the directors’ knowledge of or participation in corporate wrongdoing. See, e.g., Bryceland v. Minogue, 557 F. App’x 1 (1st Cir. 2014); Campbell v. Yu, No. 12 Civ. 3169 (LAK), 2014 WL 2599856 (S.D.N.Y. June 10, 2014); Montini v. Lawler, Nos. 12-11296-DJC, 12-11399-DJC, 2014 WL 1271696 (D. Mass. Mar. 26, 2014); Kuberski v. O’Rourke, No. 12 C 7993, 2014 WL 1227630 (N.D. Ill. Mar. 25, 2014); Seni v. Peterschmidt, No. 12-cv-00320-REB-CBS, 2014 WL 561618 (D. Colo. Feb 12, 2014).

Recent decisions also reaffirmed a long line of precedent holding that Caremark claims, which challenge an alleged failure to monitor a company through inaction, are “possibly the most difficult theory in corporation law upon which a plaintiff might hope to win a judgment.” See Seni, 2014 WL 561618, at *7 (quoting In re Caremark Int’l, Inc. Derivative Litig., 698 A.2d 959, 967 (Del. Ch. 1996)). For example, in Welch v. Havenstein, 553 F. App’x 54 (2d Cir. 2014), the Second Circuit Court of Appeals affirmed a district court’s holding that demand was not excused where the derivative plaintiff asserted Caremark claims against corporate directors. The plaintiff vaguely asserted that the directors had ignored signs that a former employee was perpetrating a kickback scheme related to one of the company’s contracts. In affirming dismissal, the Second Circuit reasoned that the complaint failed to plead particularized allegations that the board took action to approve the alleged misconduct and the “so-called ‘red flags’ alleged in the complaint did not support an inference of actual or constructive knowledge on the part of the board.” Id. at 55; see also In re JPMorgan Chase & Co. Derivative Litig., No. 12 Civ. 03878(GBD), 2014 WL 1297824 (S.D.N.Y. Mar. 31, 2014); Brautigam v. Blankfein, No. 13 Civ. 0760, 2014 WL 1244701 (S.D.N.Y. Mar. 26, 2014); In re Hecla Mining Co. Derivative Shareholder Litig., No. 2:12-CV-00097, 2014 WL 689036 (D. Idaho Feb. 20, 2014).

Finally, courts rejected plaintiffs’ attempts to evade the demand requirement by asserting that director action violated the business judgment rule. See, e.g., Freedman v. Redstone, No. 13-3372, 2014 WL 2219173, at *7-9 (3d Cir. May 30, 2014) (holding that the plaintiff failed to plead particularized allegations that directors violated a stockholder-approved compensation plan); In re Maxwell Techs., Inc. Derivative Litig., No. 13-CV-966-BEN (RBB), 2014 WL 2212155, at *10-13 (S.D. Cal. May 27, 2014) (holding that conclusory allegations that directors knew or should have known about problems with the company’s revenue recognition did not excuse demand; directors were entitled to rely on honesty and integrity of employees).

Trends in Merger & Acquisition Litigation and the Delaware Courts

Filing and Settlement Trends

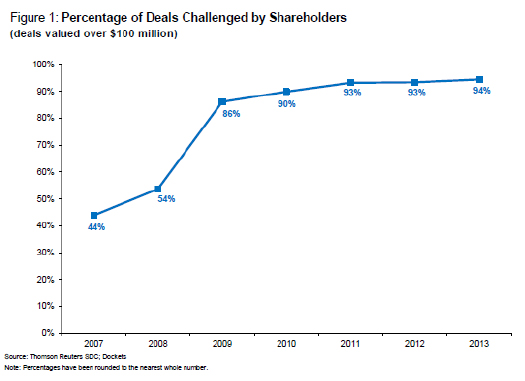

As we noted in our last update, from 2009 to 2012, virtually every significant M&A transaction was challenged by stockholder litigation. That trend continued in 2013. According to Cornerstone Research, 94 percent of deals valued over $100 million resulted in litigation in 2013. This is the fourth straight year topping 90 percent.

Cornerstone Research, Shareholder Litigation Involving Mergers and Acquisitions (2014). As noted above, however, the filing trends in 2014 point to a slight decline, at least in federal court filings.

Deals valued over $100 million attracted an average of more than five lawsuits, and more than 62 percent were litigated in more than one court. As in previous years, the vast majority of these suits were settled. However, monetary settlements were less common in 2013, and average fee requests for plaintiffs’ attorneys were down to $1.1 million in 2013, compared to $1.4 million in the two previous years. Fee requests for disclosure-only settlements were also down for the sixth consecutive year, averaging $500,000 in 2013.

Delaware Chancery Court Finds Two-Tiered Poison Pill Reasonable

The Delaware Court of Chancery’s recent decision in Third Point LLC v. Ruprechet, Nos. 9469-VCP, 9497-VCP, 9508-VCP, 2014 WL 1922029 (Del. Ch. May 2, 2014), is significant for companies and activist investors keen on influencing corporate strategy. Vice Chancellor Parsons found that Sotheby’s two-tiered poison pill—which limited activist investors to 10% stakes while permitting passive stockholders to hold as much as 20%—was a permissible response to rapid acquisitions of its stock by hedge funds. This decision may lead to more companies adopting forms of a two-tiered pill that differentiate between types of stockholders.

In the summer of 2013, Third Point and several other investors filed with the SEC notices of their holdings in Sotheby’s and their intent to effect corporate change. By August 2013, hedge funds controlled over 15% of Sotheby’s outstanding shares, with options to increase that figure to over 20%. On October 2, 2013, Third Point disclosed that it had increased its stake to 9.4% and attached a letter setting forth its concerns about Sotheby’s, including its board and management team. The next day, Sotheby’s board adopted a poison pill. The pill had a two-tiered structure under which Schedule 13G filers—those without any purpose to change or influence the company—were permitted to acquire up to a 20% interest in Sotheby’s. Schedule 13D filers—those, like Third Point, who intended to change or influence the company—were limited to a 10% stake. Shortly thereafter, Third Point filed suit, alleging that Sotheby’s directors breached their fiduciary duties by adopting the pill and refusing Third Point’s request for a waiver.

Vice Chancellor Parsons reviewed the board’s conduct under “well-known Unocal standard,” which requires a board to have reasonable grounds for perceiving a threat to the company, and to demonstrate that the board’s response to that threat was reasonable in relation to the threat. Third Point, 2014 WL 1922029, at *16-17. Third Point argued that the court should apply the more demanding Blasius standard, which requires directors to provide a “compelling justification” for actions that have “the primary purpose of interfering with the effectiveness of a stockholder vote.” Id. at *15. In rejecting the argument, Vice Chancellor Parsons noted that Third Point did not cite “any case in which this Court or the Supreme Court has invoked Blasius to examine a rights plan.” Id. at *16.

In assessing the two-tiered pill under Unocal, the court found that there was a sufficient support to show that Sotheby’s board reasonably perceived a threat to the company. The company was facing the possibility of “creeping control” gained by several hedge funds acquiring its stock simultaneously, and that it was not uncommon for hedge funds to form a “wolfpack” to coordinate their acquisition of a company’s stock. Id. at *17. In other words, the threat was similar to threats faced by boards implementing single-tier pills. However, the court also found that Sotheby’s could show that its two-tiered poison pill fell within the range of reasonableness required by Unocal. According to the court, while the two-tiered pill is “discriminatory … it also arguably is a ‘closer fit’ to addressing the Company’s needs to prevent an activist or activists from gaining control than a ‘garden variety’ [single-tier] rights plan.” Id. at *20-21.

The Third Point decision reaffirms the primacy of board decision-making under Delaware law in the context of perceived “threats” to the corporation, including a board’s decision to implement unique pills in response to an activist “threat.”

Delaware Chancery Court Holds Financial Advisor Liable for Aiding and Abetting Breach of Board’s Fiduciary Duties

On March 7, 2014, Vice Chancellor Laster issued a post-trial opinion in In re Rural Metro Corp. Stockholders Litigation, 88 A.3d 54 (Del. Ch. 2014), in which he found a financial advisor liable for aiding and abetting breaches of fiduciary duty by the board of Rural/Metro Corporation (“Rural”) in connection with a going-private transaction. The decision highlights Delaware courts’ increasing focus on the role of a financial advisor in the sales process, and the potential conflicts that can arise from a financial advisor’s working with both the target and acquiring companies. The decision reaffirms that boards should be attuned to potential conflicts involving their financial advisors at all stages of a transaction.

In 2010, Rural formed a special committee to assess a possible acquisition of its lone national competitor. After being rebuffed, Rural considered a going-private transaction, and a special committee of the Rural board retained RBC Capital Markets LLC (“RBC”) as its financial advisor. Later in 2010, the competitor’s parent was rumored to be in play, and a possible related acquisition of Rural was also rumored. During this time, RBC spoke with private equity firms about buy-side financing roles in connection with the acquisitions of both the competitor and Rural, but did not disclose this fact to Rural’s board.

In early 2011, Rural received six preliminary bids to take the company private. But according to Warburg Pincus LLC, a private equity bidder, a concurrent bidding process involving Rural’s competitor had “sideline[d]” many of the larger private equity firms due to confidentiality problems with bidding for both companies. Indeed, several of the “sidelined” bidders raised concerns about their inability to pursue both companies. In March 2011, Rural solicited final bids for the Rural going-private transaction, and Warburg was the only firm to make an offer. RBC did not ultimately provide meaningful buy-side financing to Warburg.

To maintain an aiding and abetting claim against RBC, Vice Chancellor Laster held that plaintiffs needed to show that RBC acted with an improper motive and misled Rural’s directors into breaching their duty of care. The court found that plaintiffs had met this burden. Even though RBC did not ultimately provide financing to Warburg, the court found that RBC should have disclosed to Rural its attempt to provide financing to Warburg as part of Rural’s going-private transaction. With respect to Rural’s board’s fiduciary duties, Vice Chancellor Laster singled out three aspects of the sales process as unreasonable. First, the court criticized the Rural board’s decision to initiate a sales process at the same time its competitor was for sale, because this limited the pool of potential bidders. Second, the court found it unreasonable that Rural continued the sales process despite negative feedback from prospective buyers about their inability to bid for both Rural and the competitor. Third, the court found that Rural’s board accepted Warburg’s bid without a reasonable informational basis, including the Board’s lack of knowledge concerning RBC’s effort to solicit a financing role from Warburg.

The decision serves as an important reminder that boards must be vigilant in assessing all possible conflicts (especially financial advisor conflicts) throughout the life of a transaction, especially when a transaction changes course and new potential conflicts may emerge.

Delaware Supreme Court Affirms that Business Judgment Rule Can Apply to Squeeze-Out Mergers with Appropriate Protections

In our 2013 Mid-Year Securities Update, we reported then-Chancellor Strine’s decision in In re MFW Shareholders Litigation, 67 A.3d 496 (Del. Ch. 2013). Chancellor Strine considered whether a going-private merger transaction involving a controlling stockholder is entitled to the protections of the business judgment rule when the merger is conditioned on approval of both a committee of independent directors and a majority of the minority stockholders. Chancellor Strine concluded that this “potent combination of procedural protections” was a “transactional structure that is most likely to protect” the interests of minority stockholders, and thus applied the business judgment rule rather than the more exacting entire fairness standard.

On March 14, 2014, the Delaware Supreme Court affirmed the decision in Kahn v. M & F Worldwide Corp., 88 A.3d 635 (Del. 2014). The Supreme Court found that the business judgment rule applies to going-private transactions with controlling stockholders “where the merger is conditioned ab initio upon both the approval of an independent, adequately-empowered Special Committee that fulfills its duty of care; and the uncoerced, informed vote of a majority of the minority stockholders.” Id. at 644. Notably, however, the court also found that a plaintiff could still challenge as a factual matter whether both of these protections were present, which the appellants in Kahn did, albeit unsuccessfully. Accordingly, while the standard affirmed by the Supreme Court will be useful for companies and their advisors in structuring controlling stockholder transactions to pass muster in Delaware courts, this structure will not necessarily immunize deals from litigation brought by enterprising dissenting stockholders who may challenge whether the required prophylactic measures—a truly independent board, for example—were present.

Shareholder Proposal/Proxy Disclosure Case Trends

Executive Compensation Litigation

Since the Dodd-Frank Wall Street Reform and Consumer Protection Act’s “Say-on-Pay” proxy disclosure rules were enacted—requiring companies to conduct a separate shareholder advisory vote to approve the compensation of executives—plaintiffs’ lawyers have filed dozens of complaints challenging companies’ disclosures relating to executive compensation and, more generally, equity compensation plans.

In a first wave of lawsuits filed shortly after the say-on-pay regulation went into effect, plaintiffs’ lawyers asserted that companies and their directors breached their fiduciary duties by either (1) failing to disclose material information in the company’s proxy before the non-binding advisory vote, or (2) adopting a proposed executive compensation plan despite a negative, albeit nonbinding, advisory vote. Although Dodd-Frank itself expressly states that it does not impose new fiduciary duties on issuers or their boards of directors, plaintiffs’ lawyers asked courts to extend state-law-based fiduciary duties to include additional say-on-pay disclosure requirements. When litigated (rather than settled), courts uniformly rejected these suits, recognizing that the say-on-pay vote is non-binding and cannot be construed to create or imply any change or addition to a company’s or board’s fiduciary duties. See, e.g., Charter Township of Clinton Police & Fire Ret. Sys. v Martin, 219 Cal. App. 4th 924 (2013).

In a second wave of cases, plaintiffs’ lawyers have focused on equity compensation plans submitted to stockholders for approval and executive compensation packages submitted to stockholders for approval under Section 162(m) of the Internal Revenue Code. In these cases, plaintiffs’ lawyers follow the litigation model they frequently pursue in M&A litigation: alleging that companies and their directors breached their fiduciary duty of candor by publishing false or misleading proxy materials; threatening to seek an injunction delaying the company’s annual meeting pending publication of certain supplementary information; and, when a company agrees to supplement its proxy materials to avoid even a remote chance of a delay in its annual meeting, demanding a large fee for the purported benefit obtained for the stockholders.

In 2012, courts provided plaintiffs’ lawyers with two early victories. In Knee v. Brocade Communications Systems, Inc., No. 1-12-CV-220249, 2012 WL 8881027 (Cal. Super. Ct. Santa Clara County April 10, 2012), plaintiffs brought suit in the California Superior Court for Santa Clara County seeking to enjoin Brocade’s scheduled annual shareholder vote. Plaintiffs alleged that Brocade’s proxy statement, which recommended that shareholders approve a proposal to increase the company’s equity incentive plan reserves by 35 million shares, did not fully and accurately describe the proposal or its purported dilutive impact. The court granted plaintiffs’ motion for a preliminary injunction, concluding that plaintiffs demonstrated a reasonable likelihood of prevailing on the claim that Brocade’s proxy statement, by virtue of its allegedly deficient disclosures, amounted to a breach of fiduciary duty. Brocade later settled the claim, agreeing to supplement its proxy statements and to reimburse plaintiffs’ counsel up to $625,000. In October 2012, plaintiffs’ counsel achieved a similar result in another case. St. Louis Police Ret. Sys. v. Severson (Abaxis), No. 12-CV-5086 YGR, 2012 WL 5270125 (N.D. Cal. Oct. 23, 2012). There, the board subsequently received an even more emphatic vote in favor of the plan changes, the company mooted further issues through bylaw amendments, and the defendants then moved to dismiss the complaint as moot and failing to state a claim, leading to a corporate governance measures settlement with plaintiffs

Courts that have looked at similar claims since Brocade and Severson have rejected them. In Mancuso v. The Clorox Company, No. RG12-651653 (Cal. Super. Ct. Alameda County Sept. 23, 2013), for example, plaintiff alleged that the proxy statement failed to provide sufficient information to enable shareholders to cast an informed vote on the say-on-pay proposal. Plaintiff argued, among other things, that Clorox needed to disclose a wide array of information provided to its compensation committee by an outside consultant. The court rejected the claims on summary judgment, holding that there was no duty to say more in the proxy statement and refusing to expand the concept of “material” information to information that simply “would be helpful.”

In February of this year, the United States District Court for the Central District of California in Masters v. Avanir Pharmaceuticals, Inc., No. SACV 14-00053-CJC(RNBx), 2014 WL 545138 (C.D. Cal. Feb. 12, 2014), reached a similar result in the context of a Rule 12(b)(6) motion to dismiss. In connection with its annual meeting, Avanir sought shareholder approval for a proposal to authorize an additional 17 million shares because its existing incentive plan was running out of authorized shares. Plaintiff alleged that the proxy statement omitted a laundry list of information regarding the reasons for, and effects of, the proposal—a list familiar to dozens of companies that have received stockholder demand letters this proxy season. The court rejected plaintiff’s claim, observing that “The Proxy provides a full and fair disclosure of the purpose, rationale, and effects of the proposed plan.” Id. at 1. The court explained that “[t]he fundamental flaw in Plaintiff’s argument is that he essentially deems all information reviewed by the board as material… . But just because a particular analysis was worth considering by the board does not mean that it is material to a reasonable investor.” Id. at 9.

Likely as a result of these adverse decisions, the number of lawsuits seeking to enjoin annual meetings because of alleged faulty executive and equity compensation disclosures declined in 2014. Dozens of companies, however, received demand letters from plaintiffs’ lawyers seeking a quick settlement and fee. Brocade and Abaxis, however, remain outlier decisions and companies who chose to fight such claims have largely succeeded.

Shareholder Proposal Litigation on the Rise

Over the past several years, there has been a significant rise in the number of shareholder proposals submitted for inclusion in public company proxy materials. According to Institutional Shareholder Services (“ISS”), shareholders have submitted approximately 901 proposals to date for 2014 shareholder meetings, which already surpasses the total of 840 proposals submitted for all shareholder meetings in 2013. In turn, there has been a rise in the number of lawsuits filed by both shareholders seeking inclusion of their proposals and companies seeking to exclude shareholder proposals.

The 2014 proxy season saw an increase in litigation related to shareholder proposals, primarily by companies seeking declaratory judgments to exclude proposals from John Chevedden and other shareholder activists. This increased inclination to litigate was driven by some companies’ successes in excluding proposals through litigation in recent years, though this season’s litigation has yielded mixed results.

Jurisdictional Issues. In Waste Connections, Inc. v. Chevedden, 554 F. App’x 334 (5th Cir. 2014) (per curiam), the U.S. Court of Appeals for the Fifth Circuit affirmed the district court’s denial of a motion to dismiss for lack of subject matter jurisdiction by John Chevedden, James McRitchie and Myra K. Young (collectively, the “defendants”). Waste Connections had sued for a declaratory judgment that it could exclude from its 2013 proxy materials a shareholder proposal submitted by the defendants. After receiving Waste Connections’ complaint, the defendants filed a motion to dismiss, in which they stated that they “covenant that they will not sue [Waste Connections] if it elects to exclude the proposal from its proxy materials and their decision not to sue is irrevocable.” Defs.’ Mot. to Dismiss at 1, Waste Connections, Inc. v. Chevedden, No. 4:13-cv-00176 (S.D. Tex. Feb. 1, 2013). Based on this covenant, the Defendants argued that they “have not caused any injury in fact of sufficient immediacy to confer standing upon [Waste Connections].” Id. In April 2013, the district court rejected this argument and denied the motion to dismiss, and the Fifth Circuit affirmed the district court’s decision in February 2014. In reaching its decision, the Fifth Circuit noted that despite the covenant not to sue, excluding the proposal could subject the company to an SEC enforcement action. It therefore concluded that Waste Connections had standing to seek a declaratory judgment.

However, three district courts in 2014 declined to follow Waste Connections. See Omnicom Grp., Inc. v. Chevedden, No. 14 Civ. 0386 (LLS), 2014 U.S. Dist. LEXIS 33036 (S.D.N.Y. Mar. 11, 2014); Chipotle Mexican Grill, Inc. v. Chevedden, No. 14-cv-0018-WSM-KMT, 2014 U.S. Dist. LEXIS 33378 (D. Colo. Mar. 14, 2014); EMC Corp. v. Chevedden, No. 14-10233-MLW, 2014 WL 1004111 (D. Mass. Mar. 16, 2014). In each case the shareholder proponents “irrevocably promise[d]” not to sue the companies if they omitted the shareholder proposals. Based on these promises, the courts held that the companies lacked standing. Unlike the Fifth Circuit in Waste Connections, these courts determined that the possibility of an SEC enforcement action was not certain or immediate enough to establish an “imminent injury in fact.” Accordingly, all three suits seeking declaratory judgments in favor of the companies were dismissed for lack of subject matter jurisdiction.

Company’s Statement in Opposition to a Shareholder Proposal. In Silberstein v. Aetna, Inc., No. 13 Civ. 8759 (AJN), 2014 U.S. Dist. LEXIS 49369 (S.D.N.Y. Apr. 9, 2014), plaintiff Stephen W. Silberstein brought suit against Aetna, Inc.; its Chairman, CEO, and President; and members of its board of directors in the U.S. District Court for the Southern District of New York, alleging false and misleading statements in Aetna’s 2012 and 2013 proxy statements. These proxy statements included shareholder proposals related to Aetna’s political contributions followed by statements in opposition referencing the company’s political contribution reports. Mr. Silberstein filed a motion for preliminary injunction to prohibit Aetna from distributing its 2014 proxy materials and from holding its 2014 annual meeting until it had amended its 2010-12 political contribution reports, issued its 2013 political contributions report, and informed shareholders of the alleged errors in the previous reports. The court denied this motion because Mr. Silberstein “failed to demonstrate irreparable harm.” Id. Aetna has since distributed its 2014 proxy materials, and the company held its 2014 annual meeting on May 30, 2014. The litigation is still pending in the Southern District of New York.

Endnotes:

[1] Gibson Dunn filed a brief for Vivendi S.A. as amicus curiae in support of Halliburton, arguing that the Supreme Court should abrogate the Basic presumption of reliance.

(go back)

[2] Gibson Dunn successfully represented various defendants before the Second Circuit and now represents the respondents before the Supreme Court.

(go back)