Print

PrintThe following post comes to us from Dan Ryan, Leader of the Financial Services Advisory Practice at PricewaterhouseCoopers LLP, and is based on a PwC publication. The complete publication, including appendix and footnotes, is available here.

Regulatory delay is now the established norm, which continues to leave banks unsure about how to prepare for pending rulemakings and execute on strategic initiatives. With the “Too Big To Fail” (TBTF) debate about to hit the headlines again when the Government Accountability Office releases its long-awaited TBTF report, the rhetoric calling for the completion of these outstanding rules will once more sharpen.

This rhetoric should not be confused with reality, however. At about this time last summer, Treasury Secretary Lew stated that TBTF would be addressed by the end of 2013—a goal that resulted in heightened stress testing expectations and a vague final Volcker Rule in December, but little more. Since then, the slow progress has continued, with only two key rulemakings completed so far this year: the finalization of Enhanced Prudential Standards for large bank holding companies (BHCs) and a heightened supplementary leverage ratio for the eight largest BHCs (i.e., US G-SIBs).

In sum, four years since Dodd-Frank’s passage, there are more regulations to come as we pass the midpoint of the evolving regulatory framework. The Federal Reserve (Fed) during Janet Yellen’s first year as Chair continues to indicate the need for more regulation, and now seems eager to fully involve the entire Fed Board with its kick-off of a series of staff briefings to Fed governors on supervisory issues this past May.

When the dust settles and the rules are finally known, the cumulative impact of all these siloed regulatory actions will have to be determined and strategically addressed. Until then, this post provides our view of which regulations will be issued next and what they will look like.

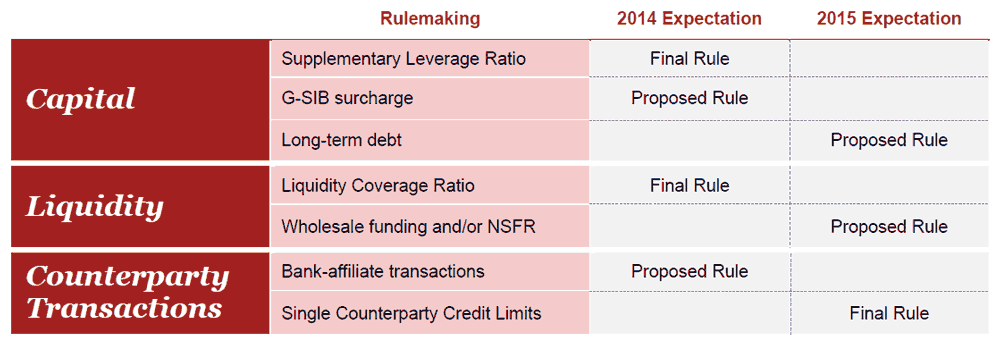

It is well known that the SEC will soon finalize its money market rule; however, we believe there will be other regulatory action this year in the following four major areas:

- Finalization of the Liquidity Coverage Ratio (LCR)

- Finalization of the US Supplementary Leverage Ratio

- Proposed rulemaking of a risk-based capital surcharge of 1% to 2.5% for US G-SIBs

- Proposed rulemaking regarding bank-affiliate transactions (23A)

We do not expect regulatory action on key items beyond these this year. The following table depicts our expectations for 2014 and of rulemaking delays to 2015. (More details are presented in the Appendix of the complete publication.)

What will the regulations look like?

Capital

Supplementary Leverage Ratio

In April 2014, US regulators released a proposed rule to modify the leverage exposure calculation of the SLR (i.e., the denominator) in order to make the measure more commensurate with the version finalized by the Basel Committee on Banking Supervision (Basel) earlier in the year.

Under the US proposed rule, banks will have to calculate written credit derivatives exposure at their notional amount instead of the previous US version’s more lenient calculation of “current exposure” plus “potential future exposure.” This change was a primary driver of the Fed’s projected industry wide capital shortfall for meeting the latest proposal in April.

At the same time, the April proposed rule made the SLR more palatable by applying credit conversion factors to off-balance sheet exposures (except for derivatives and repo-type transactions) to harmonize the US’s SLR with Basel’s ratio. These credit conversion factors reduce exposure by up to 90%, which is a large improvement from the earlier version that did not allow for any reduction and therefore disadvantaged US banks vis-a-vis foreign firms.

We expect the regulators to finalize the SLR this year, since it must be disclosed by Advanced Approaches firms (i.e., those with over $250 billion in assets) as part of the EPS beginning on January 1, 2015. Furthermore, the heightened SLR (which adds a 2% buffer to the SLR for the US’s eight G-SIBs) depends on the SLR being finalized as is an important regulatory priority for addressing TBTF.

We expect little change to the April proposal since it now largely aligns with Basel’s approach.

G-SIB risk-based capital surcharge

Basel issued its heightened risk-based capital requirements for G-SIBs in 2011 and updated them in 2013. Under Basel’s standard, G-SIBs must hold a capital buffer of Common Equity Tier 1 (CET1) on top of Basel III capital requirements. Basel’s approach assigns a particular buffer of between 1% and 2.5% to each G-SIB, depending on the firm’s systemic risk (determined by the firm’s size, interconnectedness, complexity, lack of substitutability, and scope of global activities).

Although Basel’s standard has not been formally promulgated in the US, US G-SIBs have already been required to account for the buffer as part of their annual stress testing process (using Basel’s approach), limiting the surprise factor of the upcoming proposal. We expect the US rule to be proposed in the fall and to ultimately be finalized will little change a few months later.

Long-term debt

The Fed’s long-term debt proposal has been anticipated since last year. It is closely intertwined with the FDIC’s proposed single point of entry (SPOE) resolution strategy, as the success of the SPOE strategy hinges on the existence of sufficient equity and unsecured longterm debt at the BHC-level. Therefore, many observers expected a long-term debt proposal to be issued concurrently with the FDIC’s SPOE proposal last December.

However, while the Fed and FDIC likely agree on the basic framework, they have not reached common ground on the all-important reference metric (e.g., risk-weighted assets, total assets, or on- and off-balance sheet exposures) and are likely still debating the percentage of long-term debt to be held against the metric. For the metric, we believe the SLR’s approach to measuring leverage exposure is a logical outcome because it neatly captures both on- and off-balance sheet exposures.

On the global stage, the long-term debt proposal has also been delayed by discord among supervisors. Although a global long-term debt proposed standard is expected from the Financial Stability Board (FSB) this November, we believe it will lack detail due to continuing disagreements within the FSB. For example, regulators from some jurisdictions (e.g., Japan) oppose bail-in debt requirements that are seen as unduly costly to their universal banks that are largely deposit-funded.

Accordingly, we expect the FSB’s proposal to inform the US’s, but we do not expect alignment in the near term. Furthermore, it is unclear whether the two proposals will be consistent with the EU’s approach, recently finalized in the Bank Recovery and Resolution Directive (BRRD). Under the BRRD, financial institutions must bail-in an amount equal to at least 8% of “total liabilities plus Tier 1 and Tier 2 capital” before other forms of assistance could be provided during the resolution process.

Regardless of the degree to which the US and global standards align, we expect US regulators to treat the FSB proposal as an opportunity to receive feedback from the industry and other stakeholders before issuing their proposal, which we expect no earlier than mid-2015.

Liquidity

Liquidity Coverage Ratio

Last October, the US regulators proposed their version of Basel’s Liquidity Coverage Ratio (LCR). The US proposal came out significantly tougher than Basel’s then-proposed ratio, and continues to be tougher than Basel’s ratio finalized in January 2014 in three key ways. Namely the US proposal:

- Excluded key items from the definition of high quality liquidity assets (HQLA) such as municipal debt and private label mortgage debt (impacting the LCR’s numerator).

- Rendered GSE-issued debt as “Level 2A” HQLA rather than “Level 1,” despite its deep and liquid market, thus subjecting GSE debt to a 15% haircut and to the Level 2 asset cap of 40% of HQLA.

- Introduced a stricter methodology for calculating daily net cash outflows for BHCs with over $250 billion in assets (impacting the LCR’s denominator), by calculating it based on the “peak” net cumulative amount and applying a daily limit to the amount of outflows that can be offset by inflows.

Unlike the SLR and the G-SIB capital surcharge, we do not expect US regulators to defer to Basel’s LCR approach. However, we do believe the proposal will change in several respects and view the following as the most likely candidates for improvement:

- Including municipal bonds in the definition of HQLA.

- Treating GSE debt more favorably by excluding it from the Level 2 asset cap of 40% of HQLA, but retaining the 15% haircut.

- Providing up to one year of relief from the daily net cash outflow calculation for most firms (but likely not for US G-SIBs).

- Capping the outflow rate of secured public deposits at a much lower level, since the proposed outflow rate of these deposits is a punitive 100%.

- Including more items in the definition of operational deposits (which enjoy a relatively low 25% outflow rate), since the proposal’s definition excludes any deposits associated with the provision of services to a range of entities (including investment companies and investment advisors) thereby subjecting firms to higher projected outflows by carving out more deposits than warranted from the definition of operational deposits (Basel’s definition only excludes deposits arising from the provision of prime brokerage services).

We believe US regulators will finalize the LCR proposal in early Fall to give firms some time to implement the measure by the January 1, 2015 proposed effective date. We do not expect US regulators to defer to the Basel’s prolonged implementation time frame, as some in the industry have called for.

Wholesale funding and/or Net Stable Funding Ratio

Fed officials for some time have raised concerns around the systemic risk posed by firms’ reliance on short-term wholesale funding markets and continue to discuss the issue (most recently at the Financial Stability Oversight Council’s June meeting). Governor Tarullo has outlined requirements to address these concerns, including (a) capital surcharges for firms that are heavily reliant on wholesale funding, and (b) increased liquidity or capital requirements imposed on securities financing transactions (SFTs) matched books.

Chair Yellen recently suggested that the Fed’s forthcoming proposal might include elements of both requirements, depending on the type of institution—i.e., capital or liquidity surcharges for the largest banks, and industry-wide SFT margin requirements (including nonbanks). Governor Tarullo has similarly suggested that margin requirements should reach beyond Fed-regulated institutions to include “shadow banks.”

Internationally, the issue of wholesale funding is being addressed by Basel’s proposed Net Stable Funding Ratio (NSFR) proposal, issued in 2010 and modified in January 2014. The Basel proposal requires that a bank’s “available stable funding” (generally, the sum of regulatory capital and weighted liabilities) be equal to or greater than its “required stable funding” (generally, the sum of weighted assets and off-balance sheet exposures) on an on-going basis. This approach is similar to the increased liquidity requirements suggested by Fed governors as part of their wholesale funding discussion, thus making it unclear whether the Fed will implement Basel’s NSFR separately or as part of a larger wholesale funding proposed rule.

We expect the Fed to issue its wholesale funding proposal in 2015. A separate NSFR proposal, if issued, is similarly unlikely before 2015 and will depend on Basel’s finalized approach.

Counterparty Transactions

Affiliate transactions

The long-awaited affiliate transactions proposed rule saw renewed attention earlier this year when the Fed sent a questionnaire to several large BHCs seeking data on derivative and securities financing transactions between the lead bank and their top ten affiliates. The Fed’s questionnaire asked BHCs how they would alter their derivatives booking practices if exposure limits included a potential future exposure (PFE) component, implying that the Fed is considering the business impact of its upcoming proposed rule.

That impact may influence where on the continuum of current guidance the Fed lands when proposing its rule. Existing approaches for measuring credit exposure (non CDS) include the 2012 OCC Lending Limits Rule (which excludes affiliate transactions and incorporates a PFE component in each of the allowable methods and restricts netting), and state banking rules that range from mirroring the OCC rule (Maryland) to calculating exposure as the current positive mark-to-market and allowing for netting and collateral offsets (New York).

Regardless of the approach taken by the Fed, we expect the rule to be proposed this year and to trigger significant changes in booking models as organizations seek to reduce the historically high level of back-to-back affiliate derivative transactions in light of potentially increased collateral requirements or reconfiguration of operational processes.

Single Counterparty Credit Limits

The US’s Single Counterparty Credit Limit (SCCL) provision was initially included as part of the Fed’s EPS proposal issued in 2011. However, the SCCL was not included in the final EPS rule issued in February 2014 as the Fed continues to struggle with two issues: how to measure exposure and where to draw the line on exposure limits without harming financial markets (similar to the Fed’s affiliate transactions proposal).

Basel released its final version of its similar large exposures framework on April 15, 2014. The framework is generally more lenient than the proposed US SCCL. Namely, the Basel framework sets the G-SIB to G-SIB exposure limit at 15% of Tier 1 Capital (T1C) versus the SCCL proposal’s 10%. Basel also uses T1C as the denominator for the limit’s ratio versus the SCCL proposal’s use of the more stringent CET1 or “capital stock and surplus.” Basel also only requires aggregation of exposures to additional counterparties where one controls 50% of the other’s voting rights, compared with a more stringent 25% threshold under the SCCL.

Given the trend toward harmonization between US and global standards (as we have most recently seen with the SLR and the LCR), US regulators are likely to adopt some of the Basel framework’s measures. We expected the US’s final SCCL rule in 2015, which we believe will use T1C as the denominator of the limit’s ratio.

The complete publication is available here.