Print

PrintHolly J. Gregory is a partner and co-global coordinator of the Corporate Governance and Executive Compensation group at Sidley Austin LLP. The following post is based on a Sidley update by Ms. Gregory, John P. Kelsh, Thomas J. Kim, Rebecca Grapsas, and Claire H. Holland. The complete publication, including footnotes, is available here. Related research from the Program on Corporate Governance about proxy access include Lucian Bebchuk’s The Case for Shareholder Access to the Ballot and The Myth of the Shareholder Franchise (discussed on the Forum here), and Private Ordering and the Proxy Access Debate by Lucian Bebchuk and Scott Hirst (discussed on the Forum here).

Efforts by shareholders to directly influence corporate decision-making are intensifying, as demonstrated by the significant increase over the past three years in financially focused shareholder activism and the more recent efforts by large institutional investors to encourage directors to “engage” with shareholders more directly.

Through the collective efforts of large institutional investors, including public and private pension funds, shareholders at a significant number of companies are likely within the next several years to gain the power to nominate a portion of the board without undertaking the expense of a proxy solicitation. By obtaining proxy access (the ability to include shareholder nominees in the company’s own proxy materials) activists and other shareholders will have an additional weapon in their arsenal to influence board decisions.

While proxy access has been the subject of shareholder proposals for several years, 2015 appears to be a turning point. This year’s proxy season has seen a significant increase in the number of shareholder proxy access proposals and shareholder support for such proposals (see highlights box below), as well as an increased frequency of negotiation and voluntary adoption of proxy access via board action or submission of a management proposal to a shareholder vote.

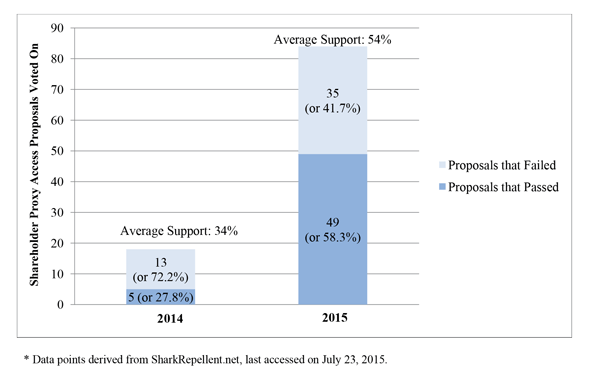

Key Highlights of Shareholder Proxy Access Proposals Voted on in 2015*

- 84 proposals were voted on, up from 18 in 2014

- 49 passed (58.3% of the total), up from 5 (27.8%) in 2014

- 35 did not pass (41.7% of the total), compared to 13 (72.2%) in 2014

- Average percentage of votes cast in favor was 54.0%, up from 33.7% in 2014

*Data points derived from SharkRepellent.net, last accessed on July 23, 2015.

Proxy access initiatives have had limited levels of success in prior years. However, shareholder support increased last year as proponents began to focus on the 3% for three years ownership requirement promoted by the Securities and Exchange Commission (SEC) in its 2010 rulemaking efforts (as described below).

This year, with a major initiative from public pension funds led by New York City Comptroller Scott M. Stringer and with encouragement from major investors, such as TIAA-CREF, and the large institutional investor industry group the Council of Institutional Investors (CII), proxy access is taking hold. Adding to the momentum is the SEC’s removal for the 2015 proxy season of a key defense in the form of no-action relief in situations in which a company intends to put forward its own competing proposal. Proxy advisory firm policies that support proxy access and discourage efforts to defend against proxy access proposals add to the momentum. Moreover, in August 2014, the CFA Institute published a report discussing the potential economic benefits of proxy access; this report has been cited by the NYC Comptroller and several other proponents in their proposals.

The broad-based shareholder campaign for proxy access on a company-by-company basis, and the apparent momentum developing among targeted companies and other leading companies to respond by taking action to adopt proxy access, is reminiscent of the campaign several years ago for companies to replace plurality voting with majority voting in the uncontested election of directors. Both issues relate to the ability of shareholders to influence the composition of the board, and both campaigns show the power of concerted efforts at private ordering.

Overview

- The SEC’s 2010 Proxy Access Rule

- Uptick in Shareholder Proxy Access Proposals in 2015

- Institutional Investor Support for Proxy Access

- Proxy Advisory Firm Policies on Proxy Access

- Bases for Exclusion of Shareholder Proxy Access Proposals

- Voting Results on Proxy Access Proposals

- Adoption of Proxy Access Bylaws During 2015 and Typical Provisions

- Spotlight: Limitations on the Size of the Nominating Group

- Potential Impact of Proxy Access on Corporate Governance

- International Perspectives on Proxy Access

- Practical Considerations

The SEC’s 2010 Proxy Access Rule

The SEC has unsuccessfully sought to adopt a market-wide proxy access rule for decades. Most recently, in 2010, the SEC adopted a proxy access rule (Exchange Act Rule 14a-11) that would have given shareholders the ability to nominate candidates through the company’s proxy materials if a shareholder (or a group of shareholders) held 3% of the company’s shares for at least three years. Rule 14a-11 was adopted shortly after Section 971 of the Dodd-Frank Act clarified the SEC’s authority to promulgate a proxy access rule. The SEC issued final rules mandating proxy access in August 2010 and these rules were scheduled to become effective in November 2010. In addition, the final rules amended Exchange Act Rule 14a-8(i)(8) to lift a prohibition on shareholder proposals relating to proxy access and certain other director election mechanisms.

However, in September 2010, Business Roundtable and the U.S. Chamber of Commerce challenged Rule 14a-11. In 2011, the U.S. Court of Appeals for the District of Columbia Circuit vacated Rule 14a-11 on the grounds that the SEC had acted “arbitrarily and capriciously” in promulgating the rule and failing to adequately assess its economic impact. The SEC did not appeal the court’s decision and has not re-proposed any proxy access rule since that decision; however, the amendment to Rule 14a-8 described above became effective in September 2011—thereby opening the door to shareholder proposals seeking proxy access.

Uptick in Shareholder Proxy Access Proposals in 2015

In public comments on the SEC’s proposed Rule 14a-11, several commenters expressed the view that the matter should be left to shareholders and companies to decide on a company-by-company basis through private ordering. Private ordering may take place, for example, pursuant to Section 112 of the Delaware General Corporation Law.

Approximately 13 companies adopted proxy access prior to 2015, including a few large companies, such as Hewlett-Packard Company, The Western Union Company and Verizon Communications Inc., which each adopted proxy access after receiving a shareholder proposal on the topic, as well as some companies that have since gone private. In addition, proxy access with a 5% for two years ownership threshold has been mandatory for companies incorporated in North Dakota since 2008; and we are aware of one public company that has reincorporated to North Dakota with the stated purpose of taking advantage of this and other “shareholder-friendly” provisions. To date, no shareholder has included a director nominee in the proxy materials of a United States company pursuant to a proxy access right.

The private ordering effort is now in full swing. Shareholder proposals seeking proxy access are the defining feature of the 2015 proxy season, with over 100 companies receiving proposals requesting that the board amend the bylaws to allow large, long-standing shareholders (or groups of shareholders) to nominate directors to the board and include those nominees in the company’s own proxy statement and related materials. The number of shareholder proxy access proposals submitted for the 2015 proxy season is more than four times the number submitted for the 2014 proxy season.

The New York City Pension Funds, with approximately $160 billion under management, accounted for the majority of the proxy access proposals submitted for the 2015 proxy season. In November 2014, Comptroller Stringer announced the “Boardroom Accountability Project,” targeting 75 companies with non-binding shareholder proxy access proposals.The proposals request that the board adopt a bylaw to give shareholders who meet a threshold of owning 3% of the company’s stock for three or more years the right to include their director candidates, representing up to 25% of the board, in the company’s proxy materials, with no limit on the number of shareholders that could comprise a nominating group. According to Comptroller Stringer, the targeted companies were selected due to concerns about the following three priority issues:

- Climate change (i.e., carbon-intensive coal, oil and gas and utility companies).

- Board diversity (i.e., companies with little or no gender, racial or ethnic diversity on the board).

- Excessive executive compensation (i.e., companies that received significant opposition to their 2014 say-on-pay votes).

Institutional Investor Support for Proxy Access

Proxy access is supported by many institutional investors, including the following:

- BlackRock—will review proxy access proposals on a case-by-case basis and generally support them provided that their parameters are not “overly restrictive or onerous” and “provide assurances that the mechanism will not be subject to abuse by short-term investors, investors without a substantial investment in the company, or investors seeking to take control of the board.”

- California Public Employees’ Retirement System (CalPERS)—has indicated that proxy access is one of its strategic priorities for the 2015 proxy season and that it is supporting proxy access proposals at 100 companies this year.

- California State Teachers’ Retirement System (CalSTRS)—supports proxy access at the 3% for three years threshold, capped at a minority of board seats.

- TIAA-CREF—wrote to the 100 largest companies in which it invests in February 2015 encouraging them to adopt proxy access at the 3% for three years threshold.

- T. Rowe Price—supports proxy access for owners of 3% or more of the company’s outstanding shares, with a holding period requirement of no less than two years and no more than three years.

- Vanguard—generally supports proxy access at the 5% for three years threshold, capped at 20% of board seats.

CII, an industry group for large institutional investors, has long supported proxy access, favoring a broad-based SEC rule imposing proxy access. Absent such a rule, Section 3.2 of CII’s Corporate Governance Policies states that a company should provide access to management proxy materials for an investor or a group of investors that have held in the aggregate at least 3% of the company’s voting stock for at least two years, to nominate less than a majority of the directors up for election.

On the other hand, Fidelity generally votes against proposals to adopt proxy access.

Some institutional investors that favor proxy access coordinated their efforts during the 2015 proxy season in an attempt to increase investor support for the proxy access proposals they sponsored. Specifically, the New York City Pension Funds, CalPERS and other large labor-affiliated pension funds each filed Form PX14A6Gs with the SEC enabling them to communicate in support of their proxy access proposals (but not collect actual proxies) without such communications being subject to the proxy solicitation rules.

Proxy Advisory Firm Policies on Proxy Access

Both Institutional Shareholder Services (ISS) and Glass, Lewis & Co. generally favor proxy access for significant, long-term shareholders.

ISS

In prior years, ISS analyzed proxy access proposals on a case-by-case basis. Beginning with the 2015 proxy season, ISS will generally recommend in favor of shareholder and management proxy access proposals with all of the following features:

- An ownership threshold of not more than 3% of the voting power.

- A holding period of no longer than three years of continuous ownership for each member of the nominating group.

- Minimal or no limits on the number of shareholders that may form a nominating group.

- A cap on the number of available proxy access seats of generally 25% of the board.

ISS will review any additional restrictions for reasonableness. Where a company includes both a management proposal along with a shareholder proposal, ISS will compare them in relation to the guidance above. ISS will generally recommend a vote against proposals that are more restrictive than the ISS guidelines.

ISS will also generally recommend a vote against one or more directors if a company omits from its ballot a properly submitted shareholder proxy access proposal, if the company has not obtained any of the following:

- The proponent’s voluntary withdrawal of the proposal.

- A grant of SEC no-action relief.

- A U.S. district court ruling that exclusion is appropriate.

Glass Lewis

Glass Lewis’ proxy voting policies for 2015 provide that it will review on a case-by-case basis shareholder proxy access proposals and the company’s response, including whether the company offers its own proposal in place of, or in addition to, the shareholder proposal. Glass Lewis will consider:

- Company size.

- Board independence and diversity of skills, experience, background and tenure.

- The shareholder proponent and the rationale for the proposal.

- The percentage of ownership requested and the holding period requirement; although note that Glass Lewis policy does not specify a preferred percentage.

- The shareholder base in both percentage of ownership and type of shareholder (such as a hedge fund, activist investor, mutual fund or pension fund).

- Board and management responsiveness to shareholders, as evidenced by progressive shareholder rights policies (such as majority voting or board declassification) and reaction to shareholder proposals.

- Company performance and steps taken to improve poor performance (such as appointing new executives or directors or engaging in a spin-off).

- Existence of anti-takeover protections or other entrenchment devices.

- Opportunities for shareholder action (such as the ability to act by written consent or the right to call a special meeting).

Bases for Exclusion of Shareholder Proxy Access Proposals

Under the SEC’s proxy rules, a company may exclude a shareholder proxy access proposal from its proxy materials if the proposal fails to meet any of the technical and substantive requirements ofExchange Act Rule 14a-8. A company may seek no-action relief from the SEC Staff, pursuant to which the company can exclude the proposal from its proxy materials. Two substantive grounds that have been relied on by companies seeking to exclude a shareholder proxy access proposal are that the proposal directly conflicts with a management proposal (Exchange Act Rule 14a-8(i)(9)) or has already been substantially implemented by the company (Exchange Act Rule 14a-8(i)(10)).

However, as discussed below, the SEC Staff is currently reviewing the Rule 14a-8(i)(9) basis for exclusion and, effective for the 2015 proxy season, will not grant no-action relief on the grounds that a shareholder proposal directly conflicts with a management proposal.

Directly Conflicting Proposals

In early December 2014, the SEC’s Division of Corporation Finance granted no-action relief to Whole Foods Market, Inc. on the basis that a 3% for three years shareholder proxy access proposal directly conflicted with a 9% for five years management proposal. When Whole Foods filed its preliminary proxy statement with the SEC after this relief was granted, the ownership threshold in the management proposal was reduced from 9% to 5%.

In the wake of the no-action relief granted to Whole Foods, it was broadly expected that companies would counter shareholder proxy access proposals by putting forward management proxy access proposals with higher minimum ownership thresholds, and obtain no-action relief on the basis that the proposals were conflicting and therefore excludable. However, following the grant of no-action relief to Whole Foods, James McRitchie, the proponent of the Whole Foods proposal, appealed the grant to the full SEC and a letter-writing campaign by incensed shareholders followed.

In January 2015, the SEC reversed course. In a relatively unusual development, SEC Chair Mary Jo White directed the SEC Staff to review Rule 14a-8(i)(9) as a basis for exclusion. As discussed in our previous update, following Chair White’s direction, the Division of Corporation Finance announced that it would express no view on the application of Rule 14a-8(i)(9) for the remainder of the 2015 proxy season in connection with all shareholder proposals—not just those seeking proxy access—and withdrew the no-action relief previously granted to Whole Foods. Prior to its annual meeting (which it postponed to September 2015), effective June 26, 2015, Whole Foods’ Board of Directors approved bylaw amendments giving an eligible shareholder, or group of up to 20 shareholders, owning 3% or more of the company’s stock for at least three years the right to nominate and include in the company’s proxy materials directors constituting up to 20% of the board seats. Mr. McRitchie withdrew his proposal, even though he had sought a 25% cap on the number of board seats and no limit on the number of participants comprising a nominating group.

Business Roundtable and other commentators have expressed concern that the SEC’s approach forces companies faced with a shareholder proxy access proposal that are considering a management proposal to either include the shareholder proposal in the proxy materials, even though it will compete with the similar management proposal and possibly lead to confusion, or omit the shareholder proposal, creating a heightened risk of litigation and negative targeting by certain pension funds and proxy advisory firms. As described below, seven companies have included competing shareholder and management proxy access proposals on the ballot. We are not aware of any company omitting a shareholder proxy access proposal without first obtaining no-action relief or withdrawal.

In June 2015, five large law firms that together handle a significant volume of shareholder proposal work on behalf of corporate clients, including Sidley Austin LLP, sent a joint letter to the SEC urging it to continue its long-standing practice of permitting companies to exclude shareholder proposals that directly conflict with management proposals on the basis of Rule 14a-8(i)(9). The firms argued that any meaningful deviation from the SEC Staff’s historical approach to administering that rule (1) has the potential to cause confusion for both companies and shareholders and (2) would require the SEC to propose the new approach as a rule amendment subject to public comment (rather than merely interpretive guidance) pursuant to the Administrative Procedures Act. Finally, the firms asked that the Staff complete its review and publicly announce its results sufficiently in advance of the 2016 proxy season to give companies and shareholders adequate time to prepare.

In a speech in late June 2015, SEC Chair White noted that, notwithstanding concerns that shareholders would be confused by two competing proposals, “shareholders were able to sort it all out and express their views.” She also expressed her hope that the Staff’s review of Rule 14a-8(i)(9) will be completed prior to the 2016 proxy season.

Substantially Implemented Proposals

A tactic that remains available to companies is to adopt proxy access and then seek to omit a shareholder proxy access proposal on the grounds that it has been “substantially implemented” by the company.

In March 2015, the SEC granted General Electric Company no-action relief allowing it to exclude a shareholder proxy access proposal on these grounds. The shareholder proposal had sought an ownership threshold of 3% for three years, for up to 20% of the board’s seats and with no limit on the number of shareholders that could comprise a nominating group. General Electric adopted a proposal with the same 3% for three years threshold for up to 20% of board seats, but limited to 20 the number of shareholders that could compromise a nominating group.

Voting Results on Proxy Access Proposals

Proxy access proposals with a 3% for three years ownership threshold have a fair likelihood of receiving majority shareholder support.

Shareholder Proposals

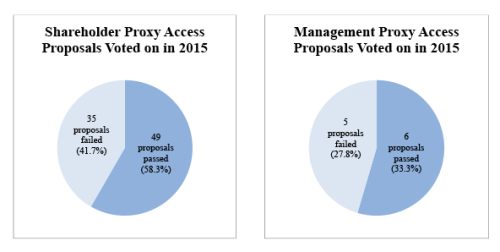

Eighty-four shareholder proxy access proposals have been voted on in 2015, averaging support of approximately 54% of votes cast; 49 proposals (58.3%) have received majority support while 35 (41.7%) did not pass. Management opposed all but three of the proposals; it supported two of the proposals and provided no recommendation with respect to one proposal. ISS supported all shareholder proposals, most of which included a 3% for three years ownership threshold (such as Comptroller Stringer’s proposals).

Voting results on shareholder proxy access proposals in 2015 appear to be influenced by the following factors:

| Factors Increasing Shareholder Support | Factors Decreasing Shareholder Support |

|---|---|

| No competing management proxy access proposal on the ballot | Competing management proxy access proposal on the ballot |

| Company has not adopted proxy access prior to the meeting | Company has adopted proxy access prior to the meeting; significantly lower support if previously adopted at 3 percent ownership threshold |

| Less insider ownership | Greater degree of insider ownership |

| Combative tone of corporate disclosure around proxy access concept | More conciliatory/open tone of corporate disclosure around proxy access concept |

| Concerns relating to corporate performance | No concerns relating to corporate performance |

| Shareholder proposal voted on later in the proxy season, as momentum towards proxy access has accelerated | Shareholder proposal voted on earlier in the proxy season |

In 2014, 18 shareholder proxy access proposals were voted on and averaged support of approximately 34% of votes cast. Five proposals passed, each of which included a 3% for three years ownership requirement. The eight proposals that deviated from that formulation received average support of only 9% of votes cast. Thirteen proposals did not pass.

Management Proposals

Eleven management proxy access proposals have been voted on in 2015, averaging support of approximately 59% of votes cast; six proposals (54.5%) passed while five (45.5%) did not pass (including one that received majority support but fell short of the company’s supermajority vote requirement). ISS recommended votes in favor of four of these proposals (which followed the 3% for three years formulation) and against seven of these proposals (six of which included a 5% for three years ownership threshold; one included a 3% for three years threshold).

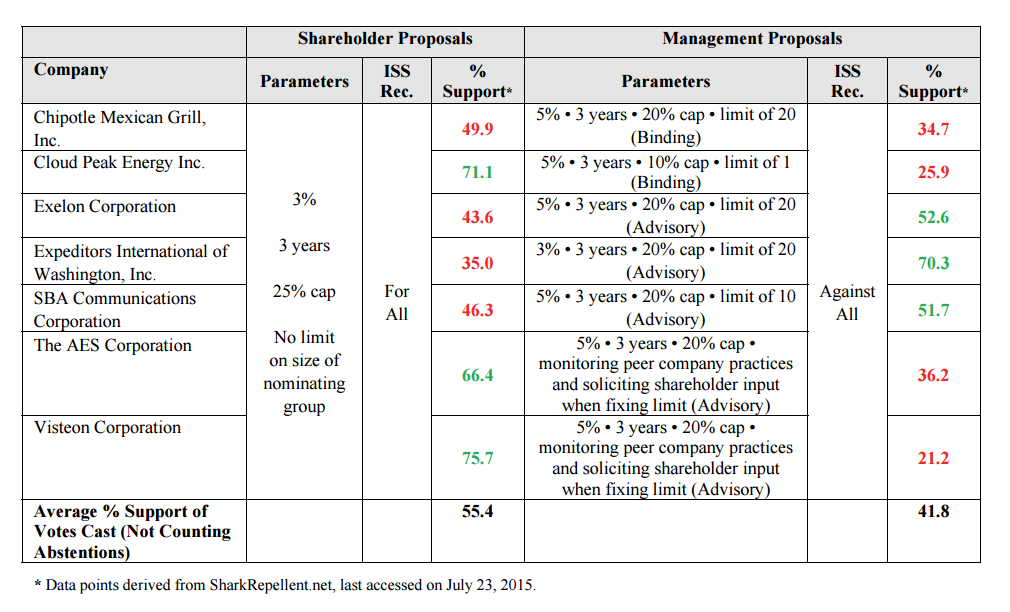

Competing Shareholder and Management Proposals

At seven companies shareholders voted on two proxy access proposals at the 2015 annual meeting—a shareholder proposal at a 3% ownership threshold and a management proposal at a 5% ownership threshold (other than one management proposal at a 3% threshold). ISS recommended for all seven shareholder proposals. ISS recommended against all seven management proposals, including at the one company which proposed a 3% for three years threshold but imposed more restrictive terms than the shareholder proposal. Specifically, the management proposal at that company included a cap of 20% of board seats (compared with a 25% cap in the shareholder proposal) and a limit of 20 shareholders in the nominating group (compared with no limit in the shareholder proposal).

As shown in the table below, the management proposal passed at three companies, the shareholder proposal passed at three companies, neither proposal passed at one company and there were no instances where both proposals passed. As noted above, SEC Chair White recently stated that, despite the concerns of some commentators, there did not appear to be shareholder confusion with respect to competing proposals.

Adoption of Proxy Access Bylaws During 2015 and Typical Provisions

Twenty-three companies have adopted proxy access during 2015, and they have done so in a range of circumstances:

- All companies except two had received a shareholder proxy access proposal.

- Four companies adopted proxy access in response to a majority-supported shareholder proposal.

- Four companies adopted proxy access prior to a vote on a shareholder proxy access proposal, and the shareholder proposal passed.

- Four companies adopted proxy access prior to a vote on a shareholder proxy access proposal, and the shareholder proposal failed.

- Eight companies adopted proxy access and a shareholder proxy access proposal was either withdrawn (at seven companies) or excluded (at one company).

- One company adopted proxy access in connection with its spin-off after a shareholder proxy access proposal was approved at its parent company’s 2015 annual meeting.

The table below highlights the key parameters of the proxy access provisions adopted so far this year, including the minimum ownership thresholds and holding periods, the maximum percentage of board seats open to proxy access candidates and the maximum number of shareholders that can comprise a nominating group.

Several additional companies have publicly committed to adopt proxy access in 2015 or 2016, including companies which made such commitments in exchange for the withdrawal of a shareholder proxy access proposal, and companies where non-binding management proxy access proposals received majority support

in 2015.

While market practice continues to develop, the proxy access provisions adopted by companies during 2015 include several elements that are beginning to emerge as typical. In addition to the key parameters described in the table below, the provisions delineate various procedural and informational requirements, proxy access nominee eligibility conditions and circumstances in which a company will not be required to include a proxy access nominee in its proxy materials.

Typical Provisions

Nomination Deadline

Requests to include proxy access nominees in the company’s proxy materials typically must be received no earlier than 120 or 150 days, and no later than 90 or 120 days, before the anniversary of the previous year’s annual meeting or the anniversary of the date on which the company released its proxy statement for the previous year’s annual meeting. Some companies have aligned their advance notice and proxy access deadlines.

Net Long Beneficial Ownership of 3% or 5%

A nominating shareholder is typically deemed to own only those outstanding common shares of the company as to which the shareholder possesses both the full voting and investment rights pertaining to the shares, and the full economic interest in such shares. For example, shares subject to any derivative arrangement entered into by the shareholder or any of its affiliates would not qualify as eligible ownership for proxy access purposes. As indicated in the table above, 3% for three years is emerging as the most common ownership threshold, although several companies have adopted a 5% for three years threshold.

Holding Period

A nominating shareholder is typically required to own the requisite amount of shares for a period of three years until the nomination date and the record date, and may be required to represent that it will continue to own the requisite shares for at least one year after the annual meeting.

Nominee Limit and Procedure for Selecting Candidates if Nominee Limit is Exceeded

Most companies have limited the number of board seats available to proxy access nominees to 20% of the board, although several have adopted a 25% cap. If the calculation of the maximum number of proxy access nominees does not result in a whole number, the maximum number of proxy access nominees that the company would be required to include in its proxy materials would be the closest whole number below the applicable percentage (e.g., 20% or 25%). Several of the proxy access bylaws provide that, if a vacancy occurs on the board after the nomination deadline but before the date of the annual meeting, and the board decides to reduce the size of the board in connection with the vacancy, the nominee limit would be calculated based on the reduced number of directors. Any proxy access nominee who is either subsequently withdrawn or included by the board in the proxy materials as a board-nominated candidate would count against the nominee limit (including in future years).

Any nominating shareholder that submits more than one nominee would be required to provide a ranking of its proposed nominees. If the number of proxy access nominees from all nominating shareholders exceeds the nominee limit, the highest ranking qualified person from the list proposed by each nominating shareholder, beginning with the nominating shareholder with the largest qualifying ownership and proceeding through the list of nominating shareholders in descending order of qualifying ownership, would be selected for inclusion in the proxy materials, with the process repeating until the nominee limit is reached.

Limitation on the Size of the Nominating Group

All but one company that has adopted proxy access during 2015 has limited the number of shareholders that are permitted to comprise a nominating group. A nominating group size limit of 20 is the most common; however, a small number of companies have set a lower limit (e.g., 1, 5, 10 or 15). A proxy access bylaw may also provide that a shareholder cannot be a member of more than one nominating group. Many companies require that one group member be designated as authorized to act on behalf of all other group members.

Information Required of All Nominating Shareholders

Each nominating shareholder is typically required to provide certain information to the company, including:

- Verification of, and information regarding, the stock ownership of the shareholder as of the date of the submission and the record date for the annual meeting (including in relation to derivative positions).

- The Schedule 14N filed by the shareholder with the SEC.

- Information regarding each proxy access nominee, including biographical and stock ownership information.

- The written consent of each proxy access nominee to (1) be named in the proxy statement, (2) serve as a director if elected and (3) the public disclosure of the information provided by the shareholder regarding the proxy access nominee.

- A description of any arrangement with respect to the nomination between the shareholder and any other person.

- Any other information relating to the shareholder that is required to be disclosed pursuant to Section 14 of the Exchange Act, and the rules and regulations promulgated thereunder.

- The written consent of the shareholder to the public disclosure of the information provided to the company.

Nominating shareholders are permitted to include in the proxy statement a 500-word statement in support of their nominees. The company may omit any information or statement that it, in good faith, believes would violate any applicable law or regulation.

Nominating shareholders are also typically required to make certain written representations to and agreements with the company, including in relation to:

- Lack of intent to change or influence control of the company.

- Intent to maintain qualifying ownership through the annual meeting date and, in many cases, for one year beyond the meeting date.

- Refraining from nominating any person for election to the board other than its proxy access nominees.

- Intent to be present in person or by proxy to present its nominees at the meeting.

- Not participating in any solicitation other than that relating to its nominees or board nominees.

- Not distributing any form of proxy for the annual meeting other than the form distributed by the company.

- Complying with solicitation rules and assuming liability and providing indemnification relating to the nomination, if required.

- The accuracy and completeness of all information provided to the company.

Information Required of All Proxy Access Nominees

Each proxy access nominee is typically required to make certain written representations to and agreements with the company, including in relation to:

- Acting in accordance with his or her duties as a director under applicable law.

- Not being party to any voting agreements or commitments as a director that have not been disclosed to the company.

- Not being party to any compensatory arrangements with a person or entity other than the company in connection with such proxy access nominee’s candidacy or service as a director that have not been disclosed to the company.

- Complying with applicable laws and stock exchange requirements and the company’s policies and guidelines applicable to directors.

- The accuracy and completeness of all information provided to the company.

Proxy access nominees are also typically required to submit completed and signed D&O questionnaires.

Several companies have adopted a provision requiring each proxy access nominee to submit an irrevocable resignation to the company in connection with his or her nomination, which would become effective upon the board determining that certain information provided by the proxy access nominee in connection with the nomination is untrue or misleading or that the nominee or the nominating shareholder breached any obligations to the company.

Exclusion or Disqualification of Proxy Access Nominees

It is typical for proxy access bylaws to permit exclusion of proxy access nominees from the company’s proxy statement if (1) the nominating shareholder (or at some companies, any shareholder) has nominated one or more of the proxy access nominees pursuant to the company’s advance notice provisions, or (2) any shareholder has nominated any person for election to the board pursuant to the company’s advance notice provisions.

In addition, the company is typically not required to include a proxy access nominee in the company’s proxy materials if:

- The nominee withdraws, becomes ineligible or does not receive at least 25% of the votes cast at his or her election. Such person is typically ineligible to be a proxy access nominee for the two annual meetings following such vote.

- The nominating shareholder participates in the solicitation of any nominee other than its nominees or board nominees.

- The nominee is or becomes a party to a compensatory arrangement with a person or entity other than the company in connection with such nominee’s candidacy or service as a director.

- The nominee is not independent under any applicable independence standards.

- The election of the nominee would cause the company to violate its charter or bylaws, any stock exchange requirements or any laws, rules or regulations.

- The nominee has been an officer or director of a competitor (often as defined in Section 8 of the Clayton Antitrust Act of 1914) within the past three years.

- The nominee is the subject of a pending criminal proceeding or has been convicted in a criminal proceeding within the past 10 years, or is subject to any order of the type specified in Rule 506(d) of Regulation D promulgated under the Securities Act.

- The nominee or the nominating shareholder has provided false or misleading information to the company or breached any obligations under the proxy access bylaw.

At some companies, if a nominating shareholder’s nominee is elected to the board, then such nominating shareholder may not utilize proxy access for the following two annual meetings (other than with respect to the nomination of the previously elected proxy access nominee).

The board or the chairman of the annual meeting may declare a director nomination by a shareholder to be invalid, and such nomination may be disregarded, if the proxy access nominee or the nominating shareholder breaches any obligations under the proxy access bylaw or the nominating shareholder does not appear at the annual meeting in person or by proxy to present the nomination.

Spotlight: Limitations on the Size of the Nominating Group

Companies that have already adopted proxy access should bear in mind that shareholders may seek to modify the terms of such provisions in the future. For example, Mr. McRitchie, the proponent at Whole Foods and several other companies that have since adopted proxy access, has criticized many proxy access bylaws as embodying “proxy access lite” and has indicated that he may in the future propose “precatory or binding bylaw resolutions to try to eliminate the limitation on group participants and to address other possible issues to be discovered upon closer examination of adopted bylaws.”

It remains to be seen whether the SEC would grant no-action relief to a company wishing to exclude a shareholder proposal that sought to eliminate a limit on the size of a nominating group. As noted above, General Electric succeeded in arguing that its proxy access bylaw substantially implemented a shareholder proxy access proposal even though the company’s bylaw limited the size of the nominating group to 20, whereas the shareholder’s proposal included no such limit.

Potential Impact of Proxy Access on Corporate Governance

It remains to be seen what impact proxy access will have on corporate governance. At companies where proxy access has been adopted, boards and management may become more focused on the quality of shareholder relations, communications and engagement, in an effort to avoid a contested election against one or more proxy access nominees.

One of the benefits of the board self-determination that occurs absent a proxy contest or proxy access situation is the ability of the board to ensure that its composition is aligned with its view of what the company needs for effective oversight. This is not a simple matter given the mosaic of skill sets, experience and diversity that is needed on a board.

An elected proxy access director will owe the same fiduciary duties as the other directors, though some may view proxy access directors as potentially having an allegiance to the nominating shareholder’s interests. Depending on the circumstances, however, there may be a greater risk that the proxy access director is viewed by the rest of the board as an outsider or even an adversary.

Concerns about how proxy access may impact board dynamics include:

- Board fragmentation. The board may become dominated by factions that are aligned with particular segments of the shareholding body rather than the shareholding body as a whole.

- Board dysfunction. Distrust among directors may develop and lead to board dysfunction with an associated negative impact on the quality of board oversight.

Concerns about how proxy access may impact a company in general include:

- A higher risk of legal challenges. Disagreement among directors may lead to a greater risk of legal challenges, including challenges in contexts that lack business judgment rule protection, subjecting transactions to heightened standards of review.

- Joint shareholder action. Special interest shareholders could coordinate to increase their representation on the board without the shareholding body at large understanding the potential for joint action.

- Increased costs and distractions. Proxy access can lead to increased costs and distractions without delivering improvements in company or board performance.

International Perspectives on Proxy Access

In considering how proxy access may impact corporate governance in the United States, in may be helpful to consider international experience. The CFA Institute Report on Proxy Access indicates that proxy access has historically been used sparingly to elect directors in countries that have adopted proxy access, including Canada, the UK, Australia, France, Germany, the Netherlands, Norway, Switzerland and Brazil. For example, the report cites to a 2009 finding that proxy access nominations at Canadian companies are often withdrawn prior to a vote because companies are “more willing and more likely to reach agreements with investors to avoid a vote.”

The CFA Institute Report on Proxy Access also evaluates the relationship between company returns and proxy access elections in Canada, the UK and Australia, and states the “[t]o the extent that proxy access provides governance benefits from a policy perspective, a preliminary analysis suggests that adverse financial impacts are negligible.”

Practical Considerations

Notwithstanding the concerns outlined above, it appears inevitable that proxy access will soon play a larger role in corporate governance as a result of private ordering. There is no indication that the SEC will revisit a broadly applicable rule. In response to questions from US House of Representatives Democrats during a congressional hearing in March 2015, SEC Chair White testified that the SEC has no “current intention” to adopt a mandatory proxy access rule. Chair White pointed to the success of the current shareholder proposal process and indicated that the SEC is very closely monitoring the private ordering process to see the direction it takes.

Proxy access will likely follow the pattern of majority voting in uncontested director elections and become common among S&P 500 companies in the next several years, assuming that institutional investors continue to campaign through shareholder proposals and the threat of shareholder proposals.

Companies have several alternatives when considering whether and when to adopt proxy access. Companies where a proxy access proposal received majority support in 2015 should consider proxy advisor policies when implementing proxy access—specifically, the likelihood of negative vote recommendations on director elections if the board has “failed to act” on a majority-supported shareholder proposal.

We expect that many companies will follow a “wait and see” approach, particularly if they have not previously received a shareholder proxy access proposal.

If faced with a proxy access proposal, counsel should be prepared to help the board and management consider the full range of options available given the company’s circumstances. Companies may wish to consult the decision tree, attached to the complete publication as Appendix A, when responding to a shareholder proposal calling for proxy access or when considering whether to modify a proxy access bylaw that is disfavored by shareholders (e.g., because of the ownership threshold, cap on board seats and/or limitation on the number of shareholders that can compromise a nominating group).

Some companies may choose to proactively adopt a proxy access bylaw by board action or by requesting shareholder approval of a bylaw amendment at the next annual meeting, in either case with or without a prior public commitment to adopt proxy access. This may help position the company as a governance leader—particularly if no shareholder proposal has been received—and, depending on the specific provisions, may minimize the likelihood of receiving a future shareholder proxy access proposal. A company taking this approach should ensure that it can justify any proxy access bylaw with thresholds that are more onerous than 3% for three years.

As companies are considering these alternatives, they should:

- Follow developments in this area and keep the nominating and corporate governance committee and the full board generally apprised.

- Know the preferences of their shareholder base (as evidenced in proxy voting policies and voting history on proxy access proposals) and engage with shareholders with respect to proxy access.

- Stay current on proxy advisory firm policies and guidance relating to proxy access.

- Keep apprised of the terms upon which companies are adopting proxy access (such as ownership threshold, holding period, limits on the number of seats at issue, limits on the number of shareholders who can combine to meet the threshold, nominee requirements and shareholder and nominee disclosure requirements), which appear to be settling in on a market standard as discussed above.

- Review the advance notice and director qualification provisions in the bylaws and consider how such provisions may be aligned with a proxy access bylaw if implemented. In addition, companies that have cumulative voting in place may wish to consider eliminating cumulative voting or requiring cumulative voting to be suspended if a proxy access nominee is included in the company’s proxy materials.

The complete publication, including footnotes, is available here.