Print

PrintAvrohom J. Kess is partner and head of the Public Company Advisory Practice at Simpson Thacher & Bartlett LLP. This post is based on a Simpson Thacher memorandum by Mr. Kess, Karen Hsu Kelley, and Yafit Cohn.

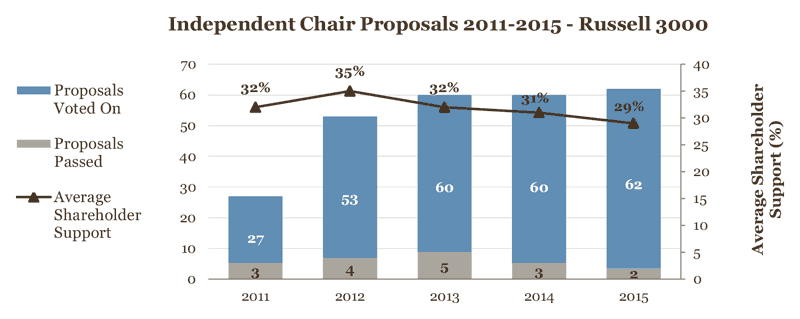

During the 2015 proxy season, 64 independent chair proposals were submitted to Russell 3000 companies, 62 of which reached a shareholder vote. This statistic is generally consistent with the number of proposals brought to a vote in 2014 and 2013, respectively. Issuers that received an independent chair proposal this year, however, may have found it more challenging to assess their chances of defeating the proposal, given that, for annual meetings occurring on or after February 1, 2015, Institutional Shareholder Services Inc. (“ISS”) changed its voting policy with regard to independent chair proposals. ISS previously applied a more objective six-factor test, which gave issuers some measure of predictability and allowed them to conform their governance features to ISS’s guidelines in an attempt to obtain an “against” recommendation. This year, however, ISS replaced this policy with a balancing test that takes a more “holistic” approach, which appears to have resulted in an increase in ISS recommendations in favor of independent chair proposals. Interestingly, ISS’s increasing support of independent chair proposals has not had a material impact on the overall outcome of the voting results: only 3.2% of independent chair proposals passed this year, as compared to 5% and 8% in 2014 and 2013, respectively.

Positions of the Proxy Advisory Firms

ISS

Prior to this proxy season, ISS applied an objective six-factor test to determine its position with regard to independent chair proposals. Under this policy, ISS generally supported independent chair proposals unless the company counterbalanced the combined chairman/CEO structure through specified governance features.

Pursuant to ISS’s newly revised policy guidelines, however, ISS generally recommends voting for independent chair proposals, taking into consideration the following factors, which it looks at “in a holistic manner”: (1) the scope of the proposal; (2) the company’s current board leadership structure; (3) the company’s governance structure and practices; (4) the company’s performance; and (5) any other relevant factors that may be applicable. [1]

This updated policy adds “new governance, board leadership, and performance factors to the analytical framework” for evaluating proposals. These include “the absence/presence of an executive chair, recent board and executive leadership transitions at the company, director/CEO tenure, and longer (five-year) TSR performance period.”

ISS has made clear that under its new “holistic” approach, any single factor that previously may have been determinative of a “for” or “against” recommendation may now be counterbalanced by other features of the company’s corporate governance. Consequently, under this holistic approach, companies have found it difficult to predict whether ISS will make a “for” or “against” recommendation.

Glass Lewis

Glass Lewis’s 2015 proxy voting guidelines on independent chair proposals remain unchanged from last year’s guidelines. As the proxy advisory firm takes the position that an independent chair is in the long-term best interests of shareholders and the company, Glass Lewis usually supports reasonably crafted shareholder proposals that seek to separate the roles of CEO and chair. That being said, Glass Lewis will not support proposals that contain “overly prescriptive” independence definitions and “may consider recommending against proposals where the company makes a compelling case for combining the two roles, has a clearly defined lead independent director role, has indicated that it intends to separate the two roles, and has strong performance and governance provisions.” [2]

Positions of Large Institutional Shareholders

The major institutional shareholders tend to be interested in a company’s governance structure, but vary in their positions on independent chair proposals. For example, Fidelity Management & Research Company generally votes against shareholder proposals calling for an independent chair unless it will further the interests of shareholders and promote effective oversight of management. [3] Other investors, such as State Street Global Advisors, analyze the proposals on a case-by-case basis, considering the presence of a lead director, the company’s performance and the general governance structure of the company. [4] Accordingly, when evaluating potential responses to a shareholder proposal to separate the chair and CEO positions, it is important to understand the positions of the company’s largest shareholders.

Independent Chair Proposal Trends

Overall Trends

- Independent chair proposals were second in popularity among corporate governance-related proposals, though their number remains relatively steady. From 2012 through 2014, independent chair proposals were the most popular among the corporate governance-related shareholder proposals submitted to Russell 3000 companies. In 2015, independent chair proposals were the second-most prevalent type of governance-related proposal, after proxy access proposals. [5] Independent chair proposals have not always been so prevalent, however. Their popularity increased sharply in 2012, when the number of proposals submitted to a vote at Russell 3000 companies doubled from the previous year. For each of 2013 and 2014, the number of independent chair proposals voted upon at Russell 3000 companies has hovered around 60, with this proxy season yielding 62 proposals—the most submitted to a vote in the last five years.

- Fewer proposals passed, as compared with previous years. During the 2011 through 2014 proxy seasons, between five and 11 percent of independent chair proposals submitted to a vote passed each year. This year, passage rates dropped, as only 3.2% of independent chair proposals passed. [6]

- Average shareholder support remains relatively constant. From 2011 through 2014, independent chair proposals received average shareholder support of 31-35%. This proxy season, independent chair proposals received average support of 29%.

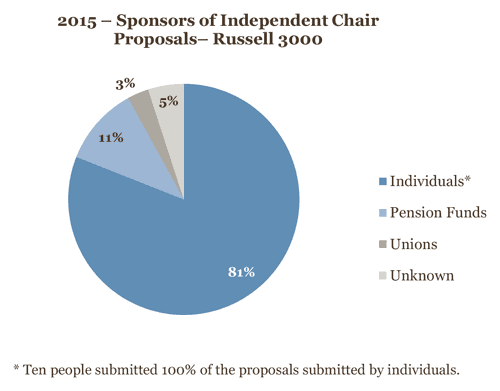

- The vast majority of proponents of independent chair proposals were individuals. Activist investor John Chevedden, for example, was responsible for 24 of the 62 independent chair proposals (or 39%) put to a vote at Russell 3000 companies this proxy season.

Impact of ISS Recommendations on Vote Results

ISS’s policy change likely impacted the proxy advisory firm’s rate of support for independent proposals this year. In contrast to 2013 and 2014, during which ISS supported 50% and 48% of independent chair proposals, respectively, ISS supported 63% of these proposals among Russell 3000 companies during the 2015 proxy season.

In 2015, the proposals supported by ISS received average shareholder support of 35%, as opposed to 19% average shareholder support for those proposals that received a negative ISS recommendation. Nonetheless—and despite the higher levels of ISS support noted above—the average voting results for independent chair proposals overall this proxy season generally paralleled those of recent years.

SEC No-Action Letters

Of the 35 no-action requests submitted to the Securities and Exchange Commission (“SEC”) this proxy season with regard to independent chair proposals, three were granted on substantive grounds, 23 were denied on substantive grounds, and one was withdrawn by the company. The remaining no-action requests were based on procedural grounds. This proxy season, issuers made two successful arguments for no-action relief pursuant to Rule 14a-8’s substantive bases for exclusion:

- The proposal’s language is inherently vague, so as to render the proxy statement misleading under Rule 14a-8(i)(3).

- The corporation lacks the authority to implement the proposal under Rule 14a-8(i)(6).

The no-action requests that were denied on substantive grounds similarly made arguments based on Rule 14a-8(i)(3) and Rule 14a-8(i)(6). Several of these requests also included the argument that the proposal was already substantially implemented and could, therefore, be properly excluded under Rule 14a-8(i)(10).

Vagueness under Rule 14a-8(i)(3)

Pfizer

The no-action letter issued to Pfizer was among the most unusual this season in that, after issuing the letter to Pfizer, the SEC staff reversed course in responding to similar no-action requests submitted by other companies, thereby generating uncertainty in the corporate community. [7]

The main argument presented by Pfizer in its initial no-action request and accepted by the staff was that the proposal was vague and indefinite such that it rendered the proxy statement misleading under Rule 14a-8. Specifically, Pfizer argued that the proposal failed to define the term “independent director.” The proposal purported to define an independent director as one “whose only nontrivial professional, familial or financial connection to the company or its CEO is the directorship.” Because Pfizer’s non-employee board members are subject to stock ownership guidelines requiring them to own a certain amount of stock (worth $687,000 as of the date Pfizer drafted its request), the company maintained that it was unclear whether the proposal would disqualify all of its non-employee directors from serving as the independent chairman of the board. Accordingly, Pfizer argued, neither Pfizer nor its shareholders would be able to determine with any reasonable certainty exactly what actions or measures the proposal requires. Pfizer relied on a no-action letter issued in early 2014 to Abbott Laboratories, permitting the company to exclude a shareholder proposal calling for an independent lead director and defining independence as “a person whose directorship constitutes his or her only connection to our company.” [8] The SEC concurred that the proposal submitted to Pfizer was similarly excludable from the company’s proxy materials pursuant to Rule 14a-8(i)(3).

Interestingly, however, after several other companies with similar stock ownership guidelines as Pfizer requested no-action relief on the same ground as a result of identical language in the proposal, the SEC backpedaled. Approximately two months after issuing the Pfizer letter, the SEC declined to provide relief to Union Pacific Corporation, stating that “[a]lthough the staff has previously agreed that there is some basis for your view, upon further reflection, we are unable to conclude that the proposal, taken as a whole, is so vague or indefinite that it is rendered materially misleading.” [9] The SEC issued nearly identical letters to another 16 companies that requested no-action relief on the basis of Rule 14a-8(i)(3) due to substantially the same language as that at issue in the Pfizer proposal. In the case of Pfizer, however, the SEC denied the proponent’s request for reconsideration, allowing the initial no-action letter to stand, since the company had already sent its proxy statement to the printer.

General Electric

The independent chair proposal submitted to General Electric (“GE”) asked the Board to separate the roles of CEO and Chair. Among other things, the proposal stated that the board could cure a violation of independence by “follow[ing] SEC Staff Legal Bulletin 14C.” [10] In its request for no-action relief, GE argued that this sentence refers to an external standard that cannot reasonably be understood by shareholders reading the proposal and its supporting statement. Accordingly, GE, citing Staff Legal Bulletin No. 14B (Sept. 15, 2004), maintained that “neither the stockholders voting on the proposal, nor the company in implementing the proposal (if adopted), would be able to determine with any reasonable certainty exactly what actions or measures the proposal requires.” The SEC agreed with GE that the proposal was vague and indefinite and could be properly excluded from GE’s proxy statement pursuant to Rule 14a-8(i)(3).

Lack of Authority to Implement the Proposal under Rule 14a-8(i)(6)

The Goldman Sachs Group

Goldman Sachs received an independent chair proposal that requested “that the Chairman of our board of directors shall be an independent director. For the purpose of this proposal, an independent director is defined as at page 23 of the firm’s Proxy Statement for the 2014 Annual Meeting of Shareholders.” [11]

In support of its no-action request to exclude this proposal, Goldman Sachs argued that the company lacks the power or authority to implement the proposal under Rule 14a-8(i)(6) because it could not “guarantee that an independent director would (1) be elected to the Board by the Company’s shareholders, (2) be elected as Chairman by the members of the board, (3) be willing to serve as Chairman, and (4) remain independent at all times while serving as Chairman.” Goldman Sachs also argued that the proposal did not “provide the Board with an opportunity or mechanism to cure a situation where the Chairman … fails to maintain his or her independence.” The SEC concurred with the company that the board does not have the power to ensure that its chairman remain independent at all times, and the proposal did not provide the board with an opportunity or mechanism to cure any violation of the independence standard proposed. Accordingly, the SEC agreed that Goldman Sachs could omit the shareholder proposal from its proxy materials.

Takeaways

Though independent chair proposals continue to be among the most prevalent governance-related proposals, they seldom garner majority support, regardless of proxy advisory firm support. Boards should be prepared to receive independent chair proposals, but should keep in mind that, absent systemic governance or performance failures at the company, these proposals are unlikely to pass. Boards should take a firm stance against an independent chair proposal if they believe combining the positions of chair and CEO is in the best interest of the company at the time the proposal is received. As is the case with all shareholder proposals, however, a board’s failure to implement a successful independent chair proposal puts the directors at risk of receiving an “against” recommendation from ISS.

Appendix A

Companies At Which Independent Chair Shareholder Proposals Have Passed

| 2011 | 2012 | 2013 | 2014 | 2015 |

|---|---|---|---|---|

| Aetna Inc. | KeyCorp | Freeport-McMoRan Inc. | Healthcare Services Group, Inc. | Omnicom Group Inc. |

| Moody’s Corporation | Kindred Healthcare, Inc. | Healthcare Services Group, Inc. | Staples, Inc. | Vornado Realty Trust |

| Vornado Realty Trust | McKesson Corporation | Kohl’s Corporation | Vornado Realty Trust | |

| Sempra Energy | Netflix, Inc. | |||

| Vornado Realty Trust |

Endnotes:

[1] ISS, United States Proxy Voting Guideline Updates: 2015 Benchmark Policy Recommendations (Nov. 6, 2014).

(go back)

[2] Glass Lewis, Proxy Paper Guidelines, 2015 Proxy Season: An Overview of the Glass Lewis Approach to Proxy Advice, Shareholder Initiatives.

(go back)

[3] See Fidelity Investments, Corporate Governance and Proxy Guidelines (Nov. 2014).

(go back)

[4] See State Street Global Advisors, Proxy Voting and Engagement Guidelines: United States (Mar. 2015).

(go back)

[5] See Veritas Executive Compensation Consultants, U.S. Proxy Season Halftime Report—Governance Trends (May 26, 2015).

(go back)

[6] See Appendix A for the list of companies at which an independent chair proposal passed.

(go back)

[7] See Pfizer Inc. (avail. Dec. 22, 2014; recon. denied Mar. 10, 2015).

(go back)

[8] Abbott Laboratories (avail. Jan. 13, 2014).

(go back)

[9] Union Pacific Corp. (avail. Feb. 26, 2015).

(go back)

[10] General Electric Co. (avail. Jan. 15, 2015).

(go back)

[11] The Goldman Sachs Group, Inc. (avail. Jan. 28, 2015).

(go back)