Print

PrintDan Ryan is Leader of the Financial Services Advisory Practice at PricewaterhouseCoopers LLP. This post is based on a PwC publication by Mr. Ryan, Mike Alix, Adam Gilbert, and Armen Meyer.

The Fed issued its Comprehensive Capital Analysis and Review (CCAR) instructions and accompanying supervisory scenarios on January 28th. These documents apply to capital plans due in April for the CCAR 2016 cycle. The following are our early takeaways:

Integration of CCAR assessments into year-round supervision begins. The CCAR 2016 instructions make clear that the Fed will be looking for integrated, business-as-usual capital planning processes that meet or exceed supervisory expectations. As a result, we expect supervisory teams’ year-round reviews of risk management, internal controls, audit, and governance (and any areas where weaknesses have been identified previously) to play a more significant role in informing the overall qualitative CCAR assessment this year. This ongoing interaction enables the Fed to form a view of capabilities ahead of the formal submission and provide strong and early feedback where practices fall short of expectations. The approach is also consistent with the Fed’s effort to bring more transparency to its qualitative assessment of capital plans and to reduce surprises in final qualitative objection decisions.

Baseline earnings projections must be reasonable. Historically, the Fed has focused its assessment of stress-test results on the severely adverse scenarios. This year, we expect the Fed to carefully assess the quality of baseline projections and to closely monitor actual results for deviations from projections. This additional scrutiny is needed not just to assess forecasting effectiveness but also to assess the reasonableness of implied dividend payout ratios, [1] and to test for changes that might prompt required revisions of the capital plan. This focus should discourage bank holding companies (BHCs) from projecting their baseline earnings too optimistically, which would lead to implied payout ratios that appear low and, potentially, to resubmissions. This approach is consistent with the Fed’s preference for quantitative projections that are derived from a rigorous bottom-up budgeting process rather than driven by aggressive top-down management directives.

The Fed expects consistency with respect to capital distributions. CCAR 2016 instructions also make clear that the Fed expects BHCs’ capital actions to be consistent with the firms’ historical experience and capital policies. This will discourage BHCs from gaining capital flexibility, for example, by projecting significant drops in planned capital distributions in the “out-quarters” of the planning horizon. [2]

Similarly, BHCs are unlikely to be allowed to address the breach of a minimum capital ratio in one quarter by lowering capital distributions in that quarter only. Rather, the Fed will expect to see consistent capital distribution adjustments across all quarters. [3] Therefore, in the event that a BHC may have to “take the mulligan” [4] this year, it should consider revising its planned capital actions across the CCAR horizon. Adjusting only one quarter is likely to lead to a regulatory finding of weaknesses in capital planning practices.

Global market shock’s January 4th as-of date provides a rare opportunity for the six largest BHCs. Stress losses on trading book positions are double-counted because the underlying positions are stressed twice, once as part of PPNR stress and once under the global market shock (GMS). The Fed allows BHCs to use the higher of the two losses, rather than double counting them, but only under the condition that a BHC can demonstrate that the stressed position is “identical” under PPNR and GMS. This condition however poses a significant operational challenge, because trading book positions change between PPNR and GMS as-of dates. But this year the GMS’s January 4th as-of date coincides with the first trading day of the year, leading to little variance in positions between that date and CCAR’s December 31st PPNR as-of date. This provides an opportunity for banks to show the significant impact of the double-count, provided they can project trading PPNR at a position or portfolio level.

This year’s January 4th GMS as-of date also has the added benefit of dampening the effect of the severely adverse scenario, which is more punitive this year (e.g., in terms of credit and basis spread widening and devaluation of illiquid assets) if, as is typical, risk positions are reduced over year-end.

Negative Treasury yields in the severely adverse scenario may lead to projected negative deposit rates. This year, three-month Treasury yields in the severely adverse scenario go to negative 50bps and remain there for the duration of the scenario. This would likely squeeze interest margins. In response, banks may be tempted to forecast negative deposit rates to increase projected net interest margin. However, before making this assumption, banks should be able to explain how they can attract, maintain, and operationally manage deposits at negative rates under severely adverse market conditions and consider the resultant strategic implications for their business model.

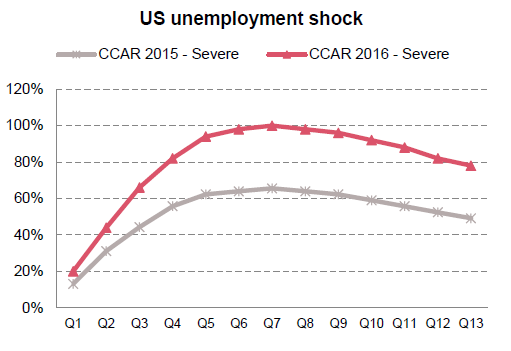

The severely adverse scenario’s unemployment reaches 10% again, but at a faster pace than last year. As a result, this year’s severely adverse stress scenario is more severe, as a sharper increase of unemployment (depicted below) could lead to increased credit defaults. This change also serves as a reminder for BHCs to avoid underestimating credit losses; they should focus their attention on the rate of change in macroeconomic indicators rather than only on absolute levels (e.g., the 10% unemployment rate).

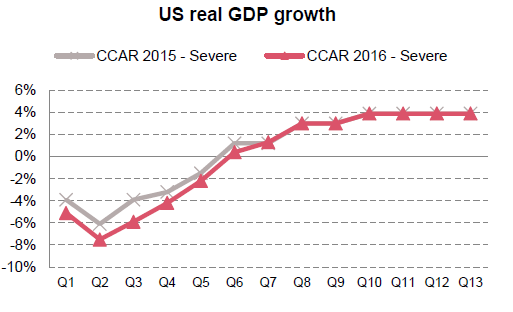

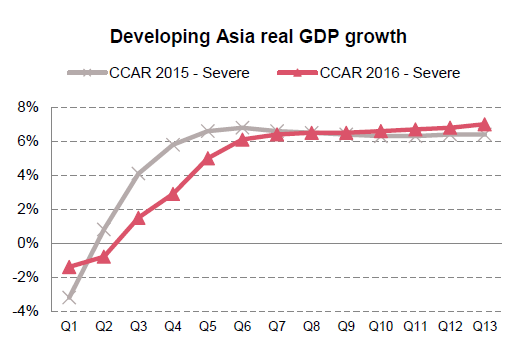

Deep recession and deflation should lead to higher default rates. As depicted in the below graphs, the 2016 severely adverse scenario includes a deeper real GDP contraction in the US, and a slower recovery in both the US and in developing Asia. Coupled with a deflationary economy and risk aversion, these trends lead to wider credit spreads and lower corporate income and cash-flow, and should result in higher defaults in BHCs’ models.

Real estate stress factors are generally similar to 2015, but prices should be stressed at a more granular level. This year’s CCAR instructions re-emphasize the regulatory expectation for more granular (e.g., regional and local) stressing of residential and commercial real estate prices. While this expectation is not new, the re-emphasis indicates lower regulatory tolerance for models that are insufficiently granular to apply greater stress to assets in areas that have experienced the most pronounced real estate price increases.

The adverse scenario is once again a test of model sensitivity to inflation and interest rates. The 2016 adverse scenario is characterized by a moderate recession and deflationary period coupled with declining Treasury yields and higher real effective rates, contrasting with last year’s adverse scenario that was a stagflation scenario with a moderate recession and sharply rising inflation and interest rates. Thus, the adverse scenario seems to have become a regulatory tool to test BHCs’ ability to forecast the impact of changes in inflation and rates. For example, the scenario description explicitly states that higher real effective interest rates should contribute to increased defaults, implying that credit loss models should incorporate the effect of the higher cost of debt servicing, a feature that many BHC credit models currently lack.

Foreign banks: Welcome to the machine. There are two new CCAR banks in 2016, [5] as a result of last year’s expiration of an exemption (SR 01-01) utilized by these two foreign-owned US BHCs. In addition, foreign firms that are repurposing their US BHC as an intermediate holding company (IHC) should include their non-BHC US subsidiaries in their CCAR projections this year. [6] These firms have much work to do in 2016, as they will also need to meet their enhanced prudential standards (EPS) requirements (including establishing risk management frameworks and risk-based capital processes). [7] Other foreign firms that are forming de-novo IHCs by July 1, 2016, will file their first CCAR submission in the 2017 cycle.

Endnotes:

[1] The Fed will give “particularly close scrutiny” to plans with implied common dividend payout ratios above 30 percent.

(go back)

[2] “Out-quarters” are the three last quarters in each year CCAR’s projections (e.g., 3Q17 through 1Q18 for CCAR 2016). Capital actions in the out quarters influence post-stress capital ratios—higher distributions will reduce the calculated pro forma ratio – but are not directly subject to the Fed’s object/non-object decision. Capital actions in the CCAR 2016 out quarters will be decided as part of CCAR 2017.

(go back)

[3] The Fed is also likely to compare BHC proposed capital actions from one year to the next and seek explanations for sharp divergences.

(go back)

[4] Since CCAR 2013 the Fed has offered BHCs an opportunity to revise downward their planned capital distributions and resubmit their capital plans after receiving the Fed’s preliminary quantitative results. See PwC’s First take, CCAR stress testing (March 2015).

(go back)

[5] TD Bank and BancWest are new for CCAR 2016.

(go back)

[6] See PwC’s First take: CCAR Guidance and final Capital Plan amendments (October 2014).

(go back)

[7] See PwC’s Regulatory brief, Foreign banks: US admission price rising (July 2014).

(go back)