Print

PrintAnna T. Pinedo is a partner in the New York office of Morrison & Foerster LLP. This post is based on a Morrison & Foerster publication by Ms. Pinedo, Ze’-ev Eiger, Brian Hirshberg, and David Lynn; the complete publication is available here.

Corporate governance has changed dramatically since passage of the Sarbanes-Oxley Act of 2002 and the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. The level of shareholder engagement and institutional investor expectations regarding governance practices have also changed significantly. The passage of the Jumpstart Our Business Startups Act in April 2012, which helped spur the initial public offering market, raised concerns among certain groups that new initial public offering (“IPO”) candidates would view certain of the accommodations available under the Act as a rationale to relax their governance practices and to rely on phase-in periods. [1] However, emerging growth companies, or EGCs, availing themselves of the JOBS Act’s Title I “IPO on-ramp” provisions generally have adopted rigorous governance policies and procedures.

In the complete publication, we assess the corporate governance practices adopted by EGCs. We examined the filings of (i) the approximately 580 EGCs (on an aggregated basis) that completed their IPOs in the period from January 1, 2013 through December 31, 2015 and (ii) the 157 EGCs (on a standalone basis) that completed their IPOs during the year ended December 31, 2015. Our objective is to provide data that will be useful to you in assessing whether your company’s current or proposed corporate governance practices are consisted with EGC market practice.

Under the JOBS Act, an issuer will remain an “emerging growth company” until the earliest of:

- the last day of the fiscal year during which the issuer has total annual gross revenues of $1 billion or more;

- the last day of the issuer’s fiscal year following the fifth anniversary of the date of the first sale of common equity securities of the issuer pursuant to an effective registration statement under the Securities Act (for a debt-only issuer that never sells common equity pursuant to a Securities Act registration statement, this five-year period will not run);

- any date on which the issuer has, during the prior three-year period, issued more than $1 billion in non-convertible debt; or

- the date on which the issuer becomes a “Large Accelerated Filer,” as defined in the SEC’s rules.

Period from January 1, 2013 through December 31, 2015

In this section, we present data on an aggregated basis, considering all of the EGC IPOs undertaken in the last three years. Based on these companies, here are our key findings:

- 84% of non-controlled companies had a majority of independent directors at

IPO pricing - 71% had staggered or classified boards

- 62% separated the Chief Executive Officer and Board chair positions

- 68% had all independent directors on the Audit, Compensation, and Nominating and Corporate Governance Committees upon completion of the IPO

- 93% had a “financial expert” on the Audit Committee at IPO pricing

- 40% had “exclusive forum” provisions in bylaws

- 74% had “super majority” shareholder voting provisions

- 46% allowed shareholders to take action by written consent under specified conditions

- 22% were “foreign private issuers”

Below we discuss the observed trends in more detail and provide resources intended to assist companies planning their IPOs.

The Filers

A “foreign private issuer” is any foreign issuer (other than a foreign government), unless: (i) more than 50% of the issuer’s outstanding voting securities are held directly or indirectly of record by residents of the United States; and (ii) any of the following applies: (x) the majority of the issuer’s executive officers or directors are U.S. citizens or residents; (y) more than 50% of the issuer’s assets are located in the United States; or (z) the issuer’s business is administered principally in the United States. For additional information, see our Frequently Asked Questions about Foreign Private Issuers.

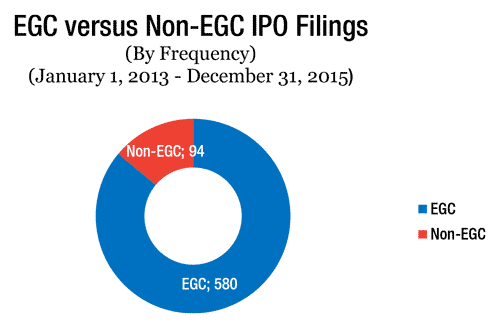

We identified the IPOs of 717 issuers in the period from January 1, 2013 through December 31, 2015, of which 94 or 13.11% were not EGCs. We reviewed the EGC IPO filings, but excluded the 42 master limited partnerships completed during the period, as well as one offering that priced but was withdrawn before closing. [2] See Appendix A of the complete publication for a list of the EGC IPOs we reviewed and Appendix B for a summary of the benefits enjoyed by EGCs under the JOBS Act. [3]

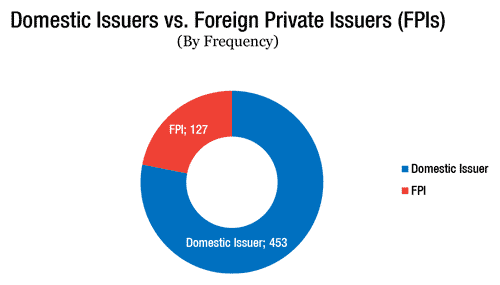

Of the remaining 580 EGCs, 127 were foreign private issuers, or FPIs.

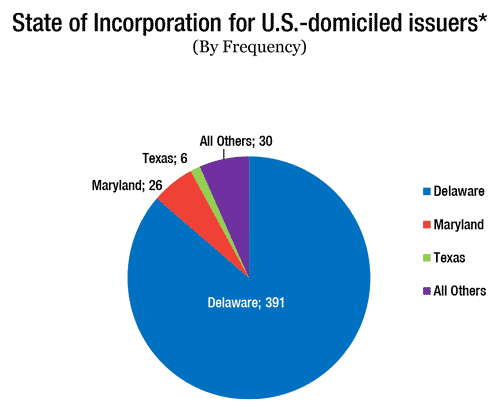

Of the 453 U.S. domestic companies, 86.9% were incorporated in Delaware, followed by Maryland (5.7%) and Texas (1.3%).

Of the 580 EGCs, all but two listed on either the Nasdaq or the NYSE. [4]

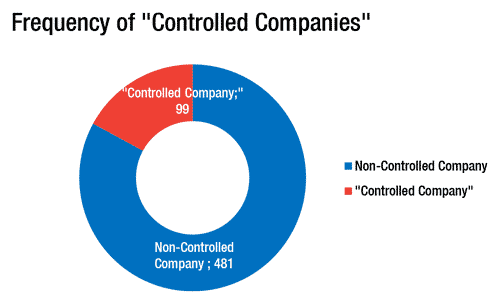

“Controlled companies” represented 17.1% of the 580 issuers. The securities exchanges exempt controlled companies from certain requirements. To the extent “control” was relevant, we

note that below.

Figure 1: N=674

Both the NYSE and the Nasdaq define a “controlled company” as one in which more than 50% of the voting power is controlled by an individual, a group, or another company. Many private equity-backed and venture capital-backed IPO issuers choose to be considered “controlled companies,” at least for a period following their IPOs while the sponsors remain significant holders.

See Appendix E of the complete publication for additional information about “controlled companies.”

Figure 2: N=580.

Figure 3: N=453.

* Excludes FPIs.

All of the Maryland-incorporated issuers were real estate investment trusts, or REITs, because Maryland’s corporate law has specific accommodations for REITs. [5]

Figure 4: N=580.

Ten of the “controlled companies” were controlled by non-U.S. parents, two of which were Chinese entities. Of the 99 “controlled companies,” four disclosed that they were controlled by venture capital funds, 52 disclosed that they were controlled by private equity funds, and two were controlled by both.

The complete publication is available here.

Endnotes:

[1] For a general overview of the JOBS Act, see our JOBS Act Quick Start: A Brief Overview of the JOBS Act (2016).

(go back)

[2] We did not review any business development company (BDC) EGCs because BDCs are subject to the additional requirements of the Investment Company Act of 1940. For additional information, see our Frequently Asked Questions about Business Development Companies.

(go back)

[3] For additional information, see our Frequently Asked Questions about Initial Public Offerings, and The Short Field Guide to IPOs.

(go back)

[4] See Appendix C of the complete publication for a summary of the NYSE and the Nasdaq quantitative listing requirements and Appendix D for a summary description of the differences between the listing requirements of these securities exchanges.

(go back)

[5] For additional information, see our Frequently Asked Questions about Real Estate Investment Trusts and our Quick Guide to REIT IPOs.

(go back)