Print

PrintCarsten Gerner-Beuerle is an Associate Professor of Law at the London School of Economics and Political Science. This post is based on an article authored by Professor Gerner-Beuerle and Tom Kirchmaier, Researcher at the London School of Economics and Political Science.

In our paper, Say on Pay: Do Shareholders Care?, which was recently made publicly available on SSRN, we examine the impact of enhanced executive remuneration disclosure rules on the voting pattern of shareholders under UK regulations. The key findings are that shareholders guide their vote by top line salary only, and appear to disregard the remaining—substantial—body of information provided to them.

Our paper can be seen against a backdrop of numerous policy initiatives that seek to reform executive remuneration in response to the continued attention and controversy that compensation packages of directors of listed companies generate. In the United Kingdom, executive pay has been regulated increasingly stringently since the early 2000s. The first steps were taken in 2002 with the introduction of the requirement that directors of quoted companies prepare a directors’ remuneration report for each financial year and lay the report before the general meeting for shareholder approval. [1] The shareholder vote was designed as an advisory vote and produced a number of high-profile shareholder revolts, but it was generally seen as largely ineffective because votes rejecting the remuneration report remained rare and the regulations failed to halt the exponential rise in executive pay. [2] In 2013, the British government therefore amplified the regulatory regime, which now requires the remuneration report to consist of two parts, the “annual report on remuneration,” which sets out the payments and benefits received by the directors in the relevant financial year, and the “directors’ remuneration policy,” which describes the operation of the individual components of the directors’ remuneration package for future years.

The content of the remuneration policy is laid down in considerable detail in a statutory instrument. [3] According to the regulations, the policy report has to contain, inter alia, a description in tabular form of the components of the executive and non-executive directors’ remuneration package, arrangements for the reduction or recovery of payments (malus and clawback), the maximum that may be paid in respect of each component, how the remuneration opportunity available under incentive plans compares to the director’s fixed salary, the type of performance targets used by the company, vesting and retention periods, and the percentage of the total award vesting and having to be retained by the director. The CEO’s remuneration opportunity in future years must be depicted graphically in bar charts indicating the level of remuneration that will be received by the CEO if the relevant performance targets are met or exceeded.

Under the 2013 regulations, the disclosure obligations are supplemented by two shareholder votes. The advisory vote has been retained for the annual report on remuneration and complemented by a binding vote on the forward-looking remuneration policy every three years. In the 2014 cycle of annual general meetings, shareholders of listed UK companies were, for the first time, required to vote on these two resolutions and decide on the approval of the annual report on remuneration and the directors’ remuneration policy.

Given that the two parts of the directors’ remuneration report have to contain clearly specified, distinct sets of information, in an efficient market, we would expect the vote on the annual report on remuneration to be responsive to the information contained in that part of the remuneration report, in particular the amount of remuneration received by executives in the past financial year, and the vote on the remuneration policy report to be responsive to differences in how the compensation package is structured and the policy intended to apply in future years. In other words, we would expect shareholders to penalize excessively high remuneration packages with the first (advisory) vote, and badly structured compensation packages, for example because they do not rein in reward for failure, with the second (binding) vote. In an efficient market, we would also expect shareholders to be able to distinguish between compensation arrangements not only based on top-line salary figures, but also based on narrative information that requires an interpretive assessment of the item of disclosure, similar to the evaluation of governance rules.

We test this hypothesis based on a hand-collected dataset comprising the pay information disclosed by FTSE 100 companies in the financial year 2013/14. We define 22 legal variables that capture different aspects of the CEO’s remuneration package and the company’s remuneration policy for future years, as well as 39 financial and ownership variables, which allow us to control comprehensively for a large number of confounding factors.

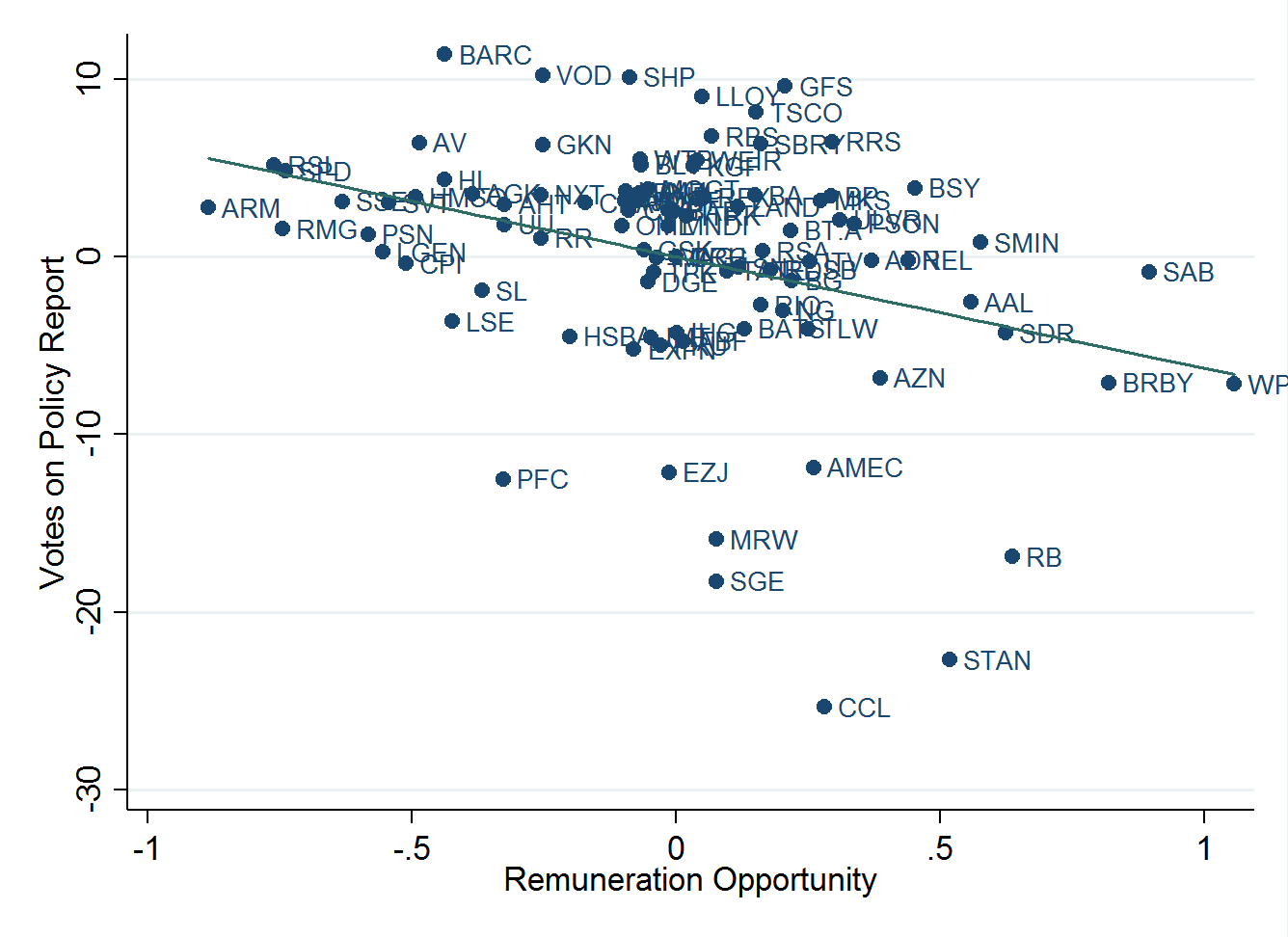

To give an intuition of our paper, we reproduce in Graph 1 an added variable plot of the correlation between the CEO’s total remuneration opportunity in future years under the company’s pay policy and the outcome of the binding shareholder vote approving the policy. We control for financial performance, ownership structure, and legal variables capturing different aspects of the remuneration policy and find that the CEO’s remuneration opportunity under maximum performance level assumptions is negatively associated with a positive vote on the policy report. The correlation is statistically significant at the 1 percent level and robust to the inclusion of different sets of controls. None of the other legal variables, measuring, for example, vesting and retention conditions or contractual provisions to avoid reward for failure, are statistically significantly associated with the voting outcome.

Graph 1: Maximum Total Remuneration Opportunity vs. Votes on Policy Report

Graph 1: Maximum Total Remuneration Opportunity vs. Votes on Policy Report

The main message of these findings is that shareholders seem to focus on an easily accessible top-line remuneration figure when deciding how to vote at the annual general meeting and disregard the wealth of information that is provided to them under the newly adopted “say-on-pay” regulations.

We also investigate which factors influence the likelihood that the vote on the policy report is significantly higher than the vote on the annual remuneration report (and vice versa). We find that in about a quarter of all cases the two votes diverge fundamentally. However, in contrast to the rationale of the legislation that introduced the two votes, differentiating voting behavior is not driven by the characteristics of the executive’s remuneration policy, but mainly by exceptionally positive future performance expectations.

The full paper is available for download here.

Endnotes:

[1] Directors’ Remuneration Report Regulations 2002, Directors’ Remuneration Report Regulations 2002.

(go back)

[2] The Department for Business, Innovation & Skills, Shareholder votes on directors’ remuneration: Impact assessment, BIS/12/967 (2012), p. 11, report a number of cases where opposition in excess of 30 percent did not lead to any adjustment of the remuneration packages but was rather dismissed without serious discussion by management.

(go back)

[3] The Large and Medium-sized Companies and Groups (Accounts and Reports) (Amendment) Regulations, Statutory Instrument 2013 No. 1981, Part 4.

(go back)