Print

PrintYafit Cohn is an associate at Simpson Thacher & Bartlett LLP. The following post is based on a Simpson Thacher publication authored by Ms. Cohn, Karen Hsu Kelley, and Avrohom J. Kess. Related research from the Program on Corporate Governance includes Shining Light on Corporate Political Spending and Corporate Political Speech: Who Decides?, both by Lucian Bebchuk and Robert Jackson (discussed on the Forum here and here.)

Following the U.S. Supreme Court’s 2010 decision in Citizens United v. Federal Election Commission, the Securities and Exchange Commission (“SEC”) has been facing mounting pressure from certain members of Congress, interest groups and investors to require companies to disclose their political spending. Last year, for example, 44 Democratic Senators wrote a letter to SEC Chair Mary Jo White, urging the SEC to promulgate a rule requiring issuers to disclose how they use corporate resources for political activities. As part of its Disclosure Effectiveness Initiative, the SEC is currently soliciting public comment on whether to require disclosure of public policy issues, including political spending, though it has previously declined to require such disclosure, concluding that, absent a congressional mandate, “it generally is not authorized to consider the promotion of goals unrelated to the objectives of the federal securities laws when promulgating disclosure requirements.” Given comments made by Chair White during her tenure, suggesting that disclosure of political contributions does not appear to be in furtherance of the SEC’s mission, and in light of the fact that Congress recently prohibited the SEC from promulgating a rule requiring political spending disclosure for the rest of the fiscal year, it is unlikely the SEC will issue such a rule in the near future. In the absence of an SEC rule, investors seeking disclosure of issuers’ political contributions and/or lobbying payments and policies have continued to try to affect change through private ordering, submitting shareholder proposals on the issue.

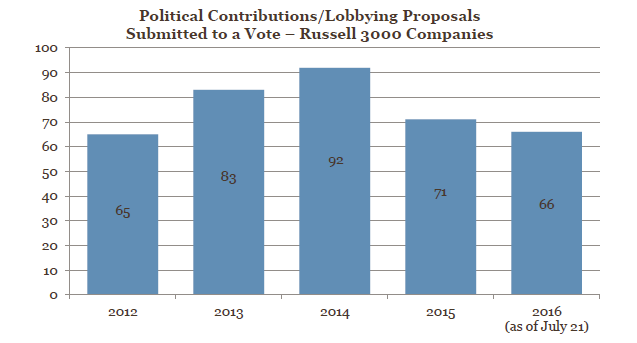

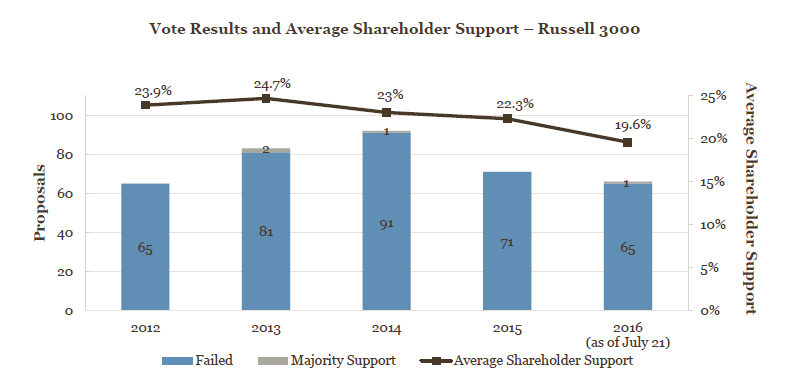

Each year from 2012 through 2015, between 65 and 92 political contributions/lobbying proposals were submitted to a vote at Russell 3000 companies. During the 2016 proxy season, 66 such proposals were submitted to a vote thus far. While roughly consistent with the 71 proposals that reached a vote in 2015, this number is significantly lower than the 92 proposals that reached a vote in 2014. Despite the relatively high number of political contributions/lobbying proposals submitted each year, the vast majority (98.9%) of these proposals have failed since 2012. Consistent with historic results, the vast majority of political contributions/lobbying proposals failed during 2016, with only one such proposal—submitted to Fluor Corporation—garnering majority support.

I. Positions of the Proxy Advisory Firms

A. Institutional Shareholder Services Inc. (“ISS”)

1. Lobbying

ISS recommends voting on a case-by-case basis with respect to proposals requesting information on a company’s lobbying policies and practices, taking into account the following factors:

- “The company’s current disclosure of relevant lobbying policies, and management and board oversight;

- The company’s disclosure regarding trade associations or other groups that it supports or is a member of, that engage in lobbying activities; and

- Recent significant controversies, fines, or litigation regarding the company’s lobbying-related activities.”

In practice, ISS recommended voting for 33 shareholder proposals related solely to lobbying and against seven such proposals that were submitted to a vote at Russell 3000 companies this year.

2. Political Contributions

ISS generally recommends voting in favor of proposals that request greater disclosure of political and trade association spending policies and activities, considering the following factors:

- “The company’s policies, and management and board oversight related to its direct political contributions and payments to trade associations or other groups that may be used for political purposes;

- The company’s disclosure regarding its support of, and participation in, trade associations or other groups that may make political contributions; and

- Recent significant controversies, fines, or litigation related to the company’s political contributions or political activities.”

As a general matter, ISS recommends voting against proposals that bar a company from making political contributions, as well as proposals requesting the publication of a company’s political contributions in news media outlets.

In practice, ISS supported 17 proposals and opposed four proposals related solely to political contributions in 2016.

B. Glass Lewis

Glass Lewis generally believes that day-to-day management and policy decisions, including those related to political issues, “are best left to management and the board as they in almost all cases have more and better information about company strategy and risk.” In cases where Glass Lewis believes there is a clear link between the subject of a shareholder proposal and value enhancement or risk mitigation, however, the proxy advisory firm will support “a reasonable, well-crafted shareholder proposal where the company has failed to or inadequately addressed the issue.”

Glass Lewis considers political contributions/lobbying proposals on a case-by-case basis, asking the following questions:

- “What is the risk to shareholders from the company’s political activities?

- Is the company’s disclosure comprehensive and readily accessible?

- How does the company’s political expenditure policy and disclosure compare to its peers?

- What is the company’s current level of oversight?

- Would adoption of this proposal lead to an increase in shareholder value?”

Glass Lewis will consider supporting a proposal requesting increased disclosure of corporate lobbying or political contributions where it determines that the company’s current disclosure is insufficient or falls behind the company’s peers or where it believes the company’s political activities put it at risk.

Additionally, Glass Lewis “will typically recommend voting for proposals requesting reports on lobbying or political contributions or expenditures when there is no explicit board oversight or there is evidence of inadequate board oversight of such contributions.” Glass Lewis may also support these proposals where there is “evidence, or credible allegations, that the company is mismanaging corporate funds through political donations or lobbying activities.”

While Glass Lewis assesses proposals requesting reports on political contributions and lobbying activities on a case-by-case basis, it generally recommends voting against proposals requesting that companies adopt an advisory vote on electioneering expenditures, as well as proposals asking companies either to prohibit corporate political spending or to provide a study on prohibiting corporate political spending. Finally, Glass Lewis takes a case-by-case approach to proposals that request that companies “construct policies that ensure that their values are aligned with their political spending.”

II. Positions of Institutional Shareholders

Not all large institutional shareholders disclose official positions on political contributions/lobbying proposals. Fidelity and State Street Global Advisors, for example, do not expressly discuss such proposals in their proxy voting guidelines. On the other hand, Blackrock’s voting guidelines specifically address shareholder proposals seeking increased disclosure on corporate political activities, indicating BlackRock’s general belief that “it is the duty of boards and management to determine the appropriate level of disclosure of all types of corporate activity” and reflecting its general reluctance to support shareholder proposals that are overly prescriptive. Nonetheless, Blackrock may support proposals requesting additional reporting of corporate political activities where there appears to be “a significant potential threat or actual harm to shareholders’ interests” and where BlackRock believes the company’s current disclosure is insufficient for shareholders to assess the company’s management of the risk. Blackrock generally does not support proposals requesting a shareholder vote on the company’s political activities or expenditures.

III. The Shareholder Proposals

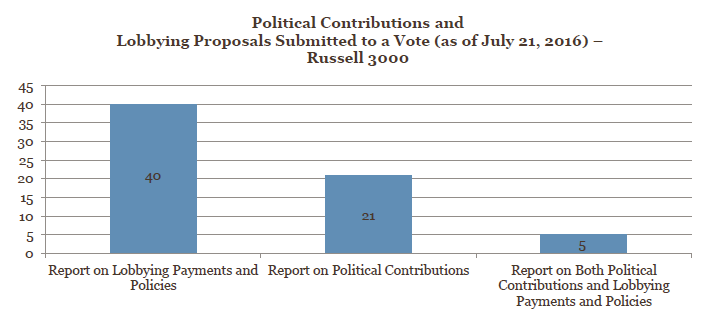

In 2016, 66 political contributions/lobbying proposals were submitted to Russell 3000 companies. Of these proposals, 40 (or 60.6%) requested a report on the company’s lobbying payments and policies, 21 (or 31.8%) requested a report on political contributions and five (or 7.6%) requested a report on both political contributions and lobbying payments and policies.

A. Requests for Reports on Lobbying Payments and Policies

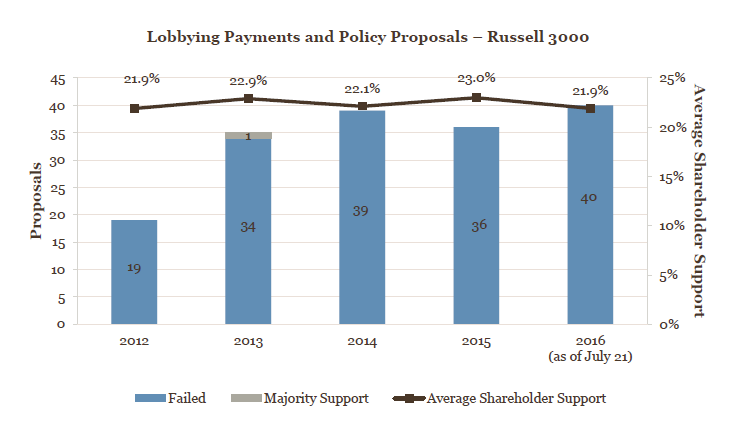

As noted above, in 2016, there were 40 shareholder proposals pertaining solely to corporate lobbying payments and policies that were submitted to a vote at Russell 3000 companies.

- General Report on Corporate Lobbying Payments and Policies. Using nearly identical language, 38 of the 40 shareholder proposals (or 95.0%) requested that the company prepare and disclose an annual report containing:

- “Company policy and procedures governing lobbying, both direct and indirect, and grassroots lobbying communications.

- Payments by [the company] used for (a) direct or indirect lobbying or (b) grassroots lobbying communications, in each case including the amount of the payment and the recipient.

- [The company]’s membership in and payments to any tax-exempt organization that writes and endorses model legislation.

- Description of management’s and the Board’s decision making process and oversight for making payments described in sections 2 and 3 above.”

- Report on Payments and Policies Tied to Environmental Lobbying. Two of the 40 lobbying proposals (or 5.0%)—submitted to Devon Energy Corporation (which also received the more prevalent lobbying proposal described above) and Occidental Petroleum Corporation—specifically targeted environmental lobbying efforts. Both requested an analysis and report of the company’s environmental lobbying activities and payments similar to the more frequently submitted lobbying proposal described above.

B. Requests for Reports on Political Contributions

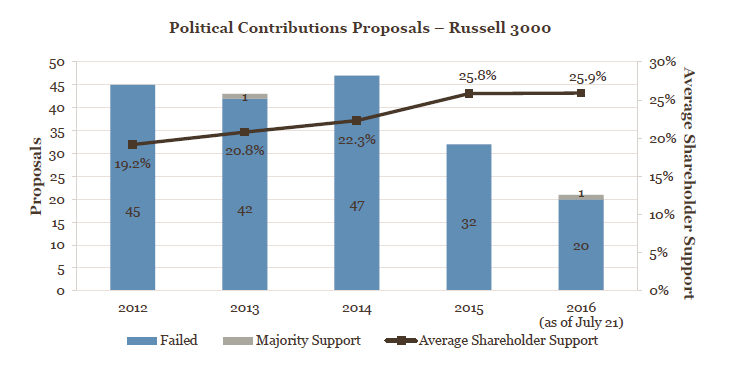

This year, a total of 21 shareholder proposals relating exclusively to political contributions reached a vote at Russell 3000 companies.

- Report on Corporate Political Spending. Of the 21 proposals on political contributions, 19 (or 90.5%) used similar language to request from the company semi-annual reports on:

- “Policies and procedures for making, with corporate funds or assets, contributions and expenditures (direct or indirect) to—(a) participate or intervene in any political campaign on behalf of (or in opposition to) any candidate for public office, or (b) influence the general public, or any segment thereof, with respect to an election or referendum.

- Monetary and non-monetary contributions and expenditures (direct and indirect) used in the manner described in section (1) above, including

- The identity of the recipient as well as the amount paid to each; and,

- The title(s) of the person(s) in the Company responsible for decision-making.”

- Congruency Analysis Comparing Company Values and Political Contributions. Two shareholder proposals, submitted to CVS Health Corporation and McDonald’s Corporation, requested an annual congruency analysis between corporate values, as defined by the company’s stated policies, and any political contributions. The proposal submitted to McDonald’s also requested that the congruency analysis include any fees paid to trade associations.

C. Requests for Reports on Both Political Contributions and Lobbying Payments and Policies

There were five hybrid proposals this year that requested reports on both political contributions and lobbying payments and policies, which can be broken down as follows:

- General Report on Political Contributions and Lobbying. Four of the five hybrid proposals (or 80.0%) used similar language to request a report on monetary and non-monetary expenditures including:

- “expenditures that [the company] cannot deduct as an ‘ordinary and necessary’ business expense under section 162(e) of the Internal Revenue Code (the ‘Code’) because they are incurred in connection with influencing legislation; (b) participating or intervening in any political campaign on behalf of (or in opposition to) any candidate for public office; and (c) attempting to influence the general public, or segments thereof, with respect to elections, legislative matters, or referenda;

- contributions to or expenditures in support of or opposition to political candidates, political parties, and political committees;

- dues, contributions or other payments made to tax-exempt ‘social welfare’ organizations and ‘political committees’ operating under sections 501(c)(4) and 527 of the Code, respectively, and to tax-exempt entities that write model legislation and operate under section 501(c)(3) of the Code; and

- the portion of dues or other payments made to a tax-exempt entity such as a trade association that is used for an expenditure or contribution and that would not be deductible under section 162(e) of the Code if made directly by the Company.”

- Report on Spending with a “Political Purpose.” One of the five hybrid proposals, submitted to Aetna Inc., requested annual disclosure of all payments to tax-exempt organizations “that were used, or that Aetna had reasonable grounds to believe were used, for a political purpose.” The proposal defined a “political purpose” as lobbying at all levels of government, participation in any political campaign, communication with the public regarding an election or referendum, and drafting and endorsing model legislation.

IV. Political Contributions/Lobbying Proposal Trends

- The total number of political contributions/lobbying proposals that have reached a vote thus far is slightly lower than last year but meaningfully lower than the high observed in 2014. Between 2012 and 2015, the number of political contributions/lobbying proposals submitted to a vote at Russell 3000 companies fluctuated between 65 and 92. This year, 66 such proposals were submitted to a vote as of July 21, 2016; in comparison, 71 such proposals were submitted to a vote in 2015, and 92 reached a vote in 2014.

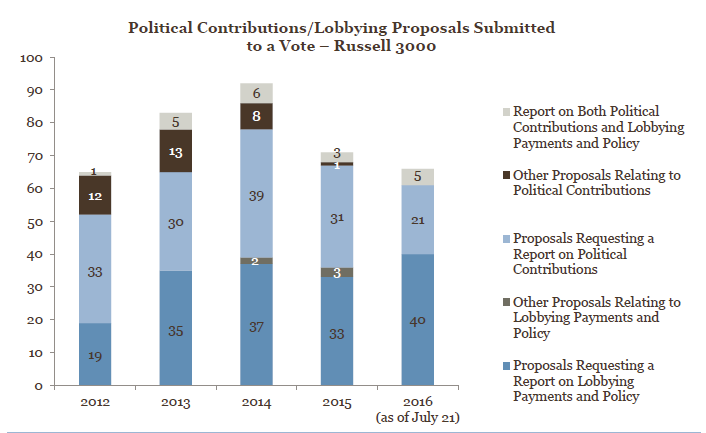

- The number of lobbying payment and policies proposals are increasing relative to political contribution proposals. In 2012, there were more than twice as many proposals relating to political contributions than those relating to lobbying. In 2016, however, the opposite was true. This year, there were 40 shareholder proposals pertaining to solely lobbying payments and policies, compared to 21 shareholder proposals concerned only with political contributions. Consistent with recent years, five shareholder proposals pertained to both political contributions and lobbying. While only one hybrid proposal was submitted to a vote at a Russell 3000 company in 2012, in each year since then between three and six such proposals have been submitted to a vote.

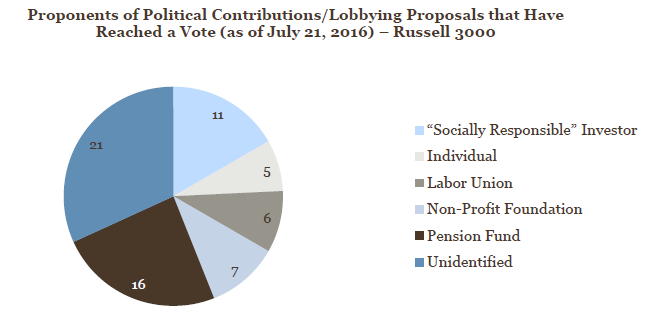

- Most proponents of political contributions/lobbying proposals were institutions, rather than individuals. This year, at least 40 of the 66 proposals (or 60.6%) that reached a vote at Russell 3000 companies were submitted by institutions, including pension funds, “socially responsible” investors and labor unions. Five proposals (or 7.6%) were submitted by individuals, and 21 proposals (or 31.8%) were submitted by a proponent that was unidentified in the company’s proxy statement.

- Consistent with previous years, 98.5% of shareholder proposals regarding political or lobbying activities and expenditures failed this year. Only one proposal passed thus far this year, receiving 52.5% support. This result is in line with each of the last four years, during which zero to two political contributions/lobbying proposals passed. The proposal that passed this year, submitted to Fluor Corporation, requested that the company prepare and disclose a semi-annual report regarding its political contributions and its policies and procedures for making political contributions. Last year, Fluor received an identical shareholder proposal, which garnered 30.7% approval, slightly more than the 25.8% average approval that similar proposals received in 2015.

- Average shareholder support for political contributions/lobbying proposals is somewhat lower than it has been in recent years. Average shareholder support for political contributions/lobbying shareholder proposals has decreased slightly each year since 2013, reaching a five-year low of 20.0% this year.

- Proposals relating to both political contributions and lobbying received the highest average shareholder support, followed by political contributions proposals and, lastly, lobbying proposals. In 2016, hybrid proposals garnered average shareholder support of 31.1% (though, admittedly, the sample size of these proposals was small this year, consistent with prior years). In comparison, proposals concerning political contributions received average shareholder support of 25.9%, and lobbying proposals received average support of 21.9%.

V. SEC No-Action Letters

During the 2016 proxy season, the SEC staff (the “Staff”) responded on substantive grounds to one no-action request regarding a political contributions proposal and two requests regarding lobbying-related proposals. In each of these cases, the Staff granted no-action relief.

In a no-action letter issued to CVS Health Corporation with regard to a shareholder proposal seeking an annual report from the company’s board of directors on the congruency between “corporate values as defined by CVS Health’s stated policies (including the Company’s ‘Our Public Policy Principles’) and Company political contributions and policy activities,” the Staff agreed with the company that the proposal was substantially duplicative of a previously submitted shareholder proposal to be included in the company’s 2016 proxy materials. The previously submitted shareholder proposal was virtually identical to the proposal at issue, requesting a “congruency analysis between corporate values as defined by CVS’s state policies (including [the company’s] Environmental Commitment Statement and [the company’s] employment policy on Equal Opportunity) and the Company and CVS EPAC political and electioneering contributions….” The Staff thus permitted exclusion of the proposal under Rule 14a-8(i)(11).

The Staff reached a similar result with respect to a shareholder proposal submitted to Duke Energy Corporation, which requested a review and summary report of the organizations in which the company is a member or otherwise supports that may engage in lobbying activities. In its no-action request, the company argued that the proposal was substantially duplicative of a previously submitted proposal for inclusion in the company’s proxy materials, which requested a general report on corporate lobbying payments and policies using the typical language as most proposals submitted to a vote this year. The Staff concurred and granted Duke Energy no-action relief under Rule 14a-8(i)(11).

Pfizer also sought no-action relief with respect to a lobbying-related proposal pursuant to Rule 14a- 8(i)(12)(ii), which permits the exclusion of a shareholder proposal where a proposal on substantially the same subject matter received “[l]ess than 6% of the vote on its last submission to shareholders if proposed twice previously within the preceding 5 calendar years.” Pfizer argued that the proposal it received dealt with substantially the same subject matter as items included in the company’s proxy materials in 2014 and 2015, in which they received 3.7% and 5.6% approval, respectively. The proposals submitted to a vote in 2014 and 2015 used nearly identical language as that submitted to the company in 2016 for inclusion in its proxy materials; each of the three proposals requested that the board review the lobbying organizations in which Pfizer is a member. The Staff concurred with Pfizer’s position and granted no-action relief.

VI. Takeaways

While political contributions/lobbying proposals remain prevalent, companies should be mindful that they rarely pass, regardless of whether they are supported by the proxy advisory firms. Issuers often successfully oppose political contributions/lobbying proposals, typically highlighting in their opposition statements legally mandated disclosures already in place and the additional cost of duplicating such disclosures. In determining how to respond to a shareholder proposal on political contributions and/or lobbying, companies should assess the level of disclosure, if any, that is appropriate for the company and should feel comfortable opposing the proposal if they feel it is in the best interests of the company and its shareholders.

The complete publication, including footnotes, is available here.

Appendix A

Companies at Which Political Contributions/Lobbying Shareholder Proposals Have Passed

| 2012 | [None] |

|---|---|

| 2013 |

|

| 2014 | Smith & Wesson Holding Corporation (Proposal requiring report on political contributions and lobbying expenditures received 55.8% shareholder support.) |

| 2015 | [None] |

| 2016 | Fluor Corporation (Proposal requiring report on political contributions received 52.5% shareholder support.) |