Print

PrintYafit Cohn is an associate at Simpson Thacher & Bartlett LLP. The following post is based on a Simpson Thacher publication authored by Ms. Cohn, Karen Hsu Kelley, and Avrohom J. Kess. Related research from the Program on Corporate Governance includes The Case for Shareholder Access to the Ballot by Lucian Bebchuk; and Private Ordering and the Proxy Access Debate by Lucian Bebchuk and Scott Hirst (discussed on the Forum here).

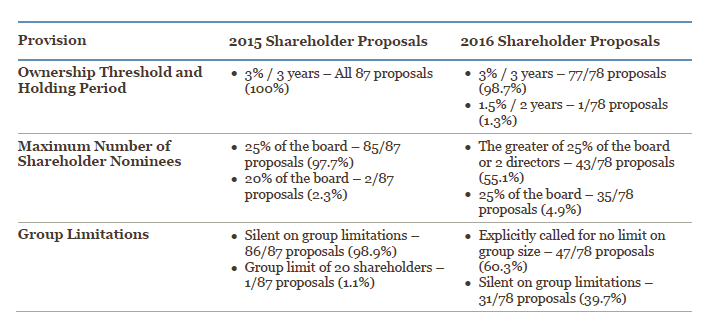

For the second year in a row, the most prevalent governance-related shareholder proposals in 2016 were those that sought to implement proxy access, a mechanism allowing shareholders to nominate directors and have those nominees listed in the company’s proxy statement and on the company’s proxy card. While the continuing momentum of proxy access proposals is due in part to the submission of 72 such proposals by New York City Comptroller Scott Stringer on behalf of the New York City pension funds he oversees, this year was marked by a meaningful increase in proxy access proposals submitted by individuals as well. Consistent with last year, the overwhelming majority of proxy access shareholder proposals called for the right of shareholders owning three percent of the company’s outstanding shares for at least three years to nominate directors in the company’s proxy materials. This year’s proposals, however, have gotten somewhat more sophisticated. More than half of the proxy access shareholder proposals reaching a vote at Russell 3000 companies capped proxy access nominees at the greater of 25 percent of the board or two directors, as opposed to simply 25 percent, which was almost universal last year. And, unlike last year, in which most shareholders proposals were silent on aggregation limits, most proxy access proposals submitted to a vote in 2016 specified that an unrestricted number of shareholders may be aggregated to reach the shareholding threshold.

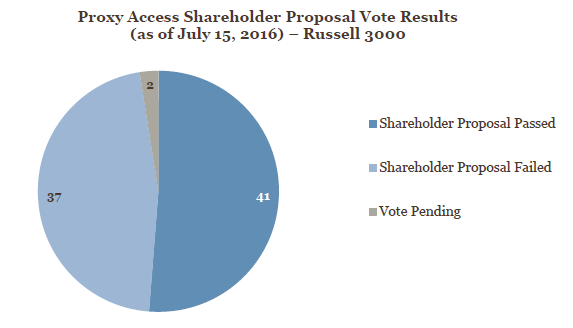

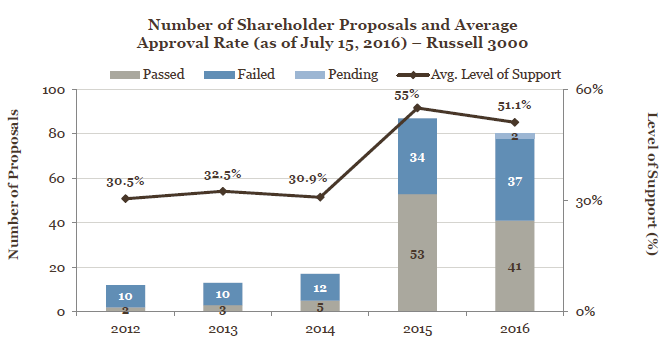

As of July 15, 2016, 78 proxy access shareholder proposals have been submitted to a vote at Russell 3000 companies during the 2016 proxy season, compared to 87 in 2015. Of the 78 proposals that have been voted on thus far this year, 41 proposals (or 52.6%) passed, while 37 proposals (or 47.4%) failed, with the primary factor determining the vote often being whether the company had previously adopted proxy access. So far this year, shareholder proposals submitted to a vote at Russell 3000 companies received average shareholder support of 51.1%, though average shareholder support rose to 64.2% among companies that had not yet adopted proxy access and dropped to 37.9% among companies that had already adopted some form of proxy access.

I. Notable Developments

A. Staff Legal Bulletin 14H

In advance of the 2016 proxy season, the Division of Corporation Finance (the “Division”) of the Securities and Exchange Commission (“SEC”) issued Staff Legal Bulletin 14H (“SLB 14H”), alleviating the uncertainty that permeated last year’s proxy season as a result of the Division’s unexpected mid-season announcement that it would not express any views that season with regard to the application of Rule 14a-8(i)(9). Rule 14a-8(i)(9) permits public companies to exclude a shareholder proposal “[i]f the proposal directly conflicts with one of the company’s own proposals to be submitted to shareholders at the same meeting.” SLB 14H clarifies the Division’s interpretation of this provision in a manner that differs significantly from that which the SEC applied before the 2015 proxy season.

While no-action responses issued prior to 2015 on the basis of Rule 14a-8(i)(9) focused on the potential for inconsistent and ambiguous results and shareholder confusion, the Division’s new approach centers “more specifically on the nature of the conflict between a management and shareholder proposal.” In particular, under the Division’s new approach, any assessment of whether a proposal is excludable under Rule 14a-8(i)(9) assesses “whether there is a direct conflict between the management and shareholder proposals.” As explained by the Division, “a direct conflict would exist if a reasonable shareholder could not logically vote in favor of both proposals, i.e., a vote for one proposal is tantamount to a vote against the other proposal.” Thus, if the two proposals are “in essence, mutually exclusive,” the shareholder proposal is excludable; if, however, a reasonable shareholder could logically vote in favor of both proposals—although possibly preferring one proposal over the other—the shareholder proposal is required to be included in the company’s proxy statement.

Illustrating the application of its new guidance, the Division specifically noted that a shareholder and management proposal, each of which seeks the adoption of proxy access but with different eligibility thresholds, are not “directly conflicting.”

B. Expansion of the Comptroller’s Proxy Access Initiative

Last year’s influx of proxy access shareholder proposals was due, in large part, to New York City Comptroller Scott Stringer’s “2015 Boardroom Accountability Project”—an initiative in which the Comptroller submitted 75 precatory shareholder proposals on proxy access to companies in diverse industries and with various market capitalizations on behalf of the New York City pension funds he oversees. In January of 2016, the Comptroller’s office issued a press release announcing the expansion of the Comptroller’s proxy access initiative, pursuant to which it submitted 72 proposals to public companies this proxy season calling for the adoption of “meaningful proxy access bylaws.”

Like last year, the Comptroller’s 2016 proposal seeks the right for shareholders owning three percent of the company’s outstanding shares for at least three years to nominate up to 25 percent of the board in the company’s proxy materials. And like last year, the vast majority of the issuers targeted by the Comptroller’s office in 2016 were companies with purportedly weak track records on the issues of board diversity, climate change or say-on-pay.

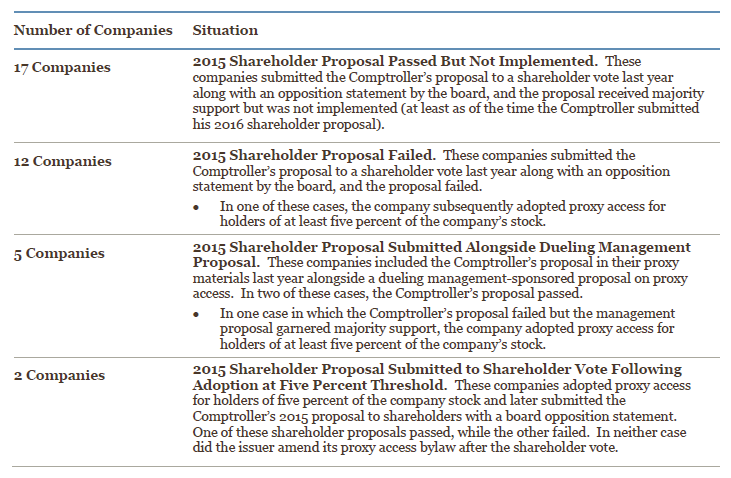

Interestingly, half of the 72 companies that received the Comptroller’s proxy access proposal this year had also received his proposal last year, but, according to the Comptroller, had “not yet enacted, or agreed to enact, a 3% bylaw with viable terms” as of the time he submitted his 2016 proposal. Notably, this group of issuers includes companies that had enacted so-called “unworkable bylaws requiring 5% ownership, some of which received binding proposals to amend their bylaw.”

The 36 companies that received the Comptroller’s proposal for the second year in a row can be broken down as follows:

Of the 72 shareholder proposals that the Comptroller’s office submitted to public companies this year, 50 (or 69.4%) were withdrawn pursuant to negotiations with the proponent. The high rate at which companies have been willing to implement proxy access at the 3% / three-year thresholds in response to the Comptroller’s proposal seems to reflect a recognition that, in its sustained pursuit of a global standard of proxy access across public companies, the Comptroller’s office is likely to continue to target these companies in subsequent years if they do not adopt proxy access at the Comptroller’s preferred thresholds. It also may indicate an acknowledgment that, at companies that have not yet adopted proxy access, a shareholder proposal on the issue is significantly more likely to garner majority support.

II. SEC No-Action Letters

Thus far this year, the staff of the SEC’s Division of Corporation Finance issued responses to 51 no-action requests pertaining to proxy access shareholder proposals, 42 of them on substantive grounds. Of those, 40 responses were based on Rule 14a-8(i)(10), which permits the exclusion of a shareholder proposal where “the company has already substantially implemented the proposal.”

A. Substantial Implementation Under Rule 14a-8(i)(10)

With its suggestion in SLB 14H that Rule 14a-8(i)(9) will no longer be available in most cases to issuers seeking to exclude proxy access shareholder proposals from their proxy materials, more companies turned to Rule 14a-8(i)(10) as a basis for exclusion this proxy season. Rule 14a-8(i)(10) was particularly ripe for use in the proxy access context this year, as an unprecedented number of companies adopted proxy access in 2015 and 2016. This exclusionary rule, however, had seldom been applied to proxy access prior to this proxy season, given the relatively new phenomenon of proxy access proposals and adoptions.

During the 2016 proxy season, the SEC Staff concurred with 36 companies that the proxy access shareholder proposals they had received may be excluded from their proxy materials pursuant to Rule 14a-8(i)(10). The Staff denied relief, however, in three instances where the company’s proxy access bylaw provisions contained a higher eligibility threshold than that requested in the shareholder proposal, as well as one case in which the shareholder proposal explicitly requested specific revisions to the company’s proxy access bylaw.

In all 36 cases in which the Staff granted no-action relief, the shareholder proposal requested, in relevant part, that the company adopt proxy access with the following provisions:

- Ownership threshold and holding period. The proposal requested proxy access for holders of three percent of the company’s outstanding common stock for at least three consecutive years. The proposal specifically noted that “recallable loaned stock” should be counted toward the three-percent ownership.

- No Aggregation Limit. The proposal provided that an “unrestricted number of shareholders” should be permitted to form a group for purposes of satisfying the ownership threshold.

- Cap on Shareholder Nominees. The proposal requested that the number of shareholder-nominated candidates appearing in the company’s proxy materials not exceed the greater of two directors or 25 percent of the board.

- Information Requirements. The proposal sought to require the nominating shareholder (or group of shareholders) to provide the company with information required by the company’s bylaws and any SEC rules regarding “(i) the nominee, including consent to being named in proxy materials and to serving as director if elected; and (ii) the Nominator, including proof it owns the required shares.”

- Required Shareholder Certifications. The proposal sought to require the nominating shareholder (or group of shareholders) to certify that “(i) it will assume liability stemming from any legal or regulatory violation arising out of the Nominator’s communications with the Company shareholders … (ii) it will comply with all applicable laws and regulations if it uses soliciting material other than the Company’s proxy materials; and (iii) to the best of its knowledge, the required shares were acquired in the ordinary course of business, not to change or influence control at the Company.”

- “No Additional Restrictions.” The proposal added: “No additional restrictions that do not apply to other board nominees should be placed on these nominations or re-nominations.”

In all 36 cases, the proxy access bylaw adopted by the company granted proxy access for holders of three percent of the company’s outstanding stock for at least three years and explicitly included loaned shares in the ownership calculation, provided that the lending shareholder has the power to recall the shares within a specified period (and, in some cases, that the shareholder does indeed recall them). Most of the companies’ bylaws, however, differed from the proposal in one or more of the following respects:

- Aggregation Limit. In 33 cases, the company’s bylaws limited the number of shareholders who could be aggregated for purposes of reaching the ownership threshold. (In all but one of these cases, the group limit was set at 20 shareholders; in the remaining case, the group limit was set at 25 shareholders).

- Cap on Shareholder Nominees. The bylaws of 30 companies included a lower cap on the number of candidates who may be nominated pursuant to proxy access. These bylaws limited the number of shareholder nominees to either:

- the greater of the two directors or 20 percent of the board, or

- 20 percent of the board (rounded down to the nearest whole number).

- Whether or not a company’s bylaws contained a lower cap on shareholder nominees than that requested by the proposal, the bylaws sometimes specified additional categories of individuals who would be deemed shareholder nominees for purposes of calculating the cap (e.g., individuals nominated pursuant to the company’s advance bylaw provision, incumbent director candidates previously nominated through the proxy access mechanism until they have served a specified number of terms, any shareholder nominee whose nomination is subsequently withdrawn or who becomes ineligible).

- Information and Certification Requirements. While the bylaws of each of the companies that obtained no-action relief required all of the disclosures and certifications outlined in the proposal, they also often required additional disclosures and/or certifications from the nominating shareholder (e.g., a representation that the nominating shareholder intends to continue to own the requisite shares through the date of the annual meeting and/or for at least one year following the date of the annual meeting (subject to limited exceptions), a representation that the nominating shareholder will not distribute any form of proxy for the annual meeting other than the form distributed by the company, a representation that the nominating shareholder will indemnify the company and its directors and officers against specified losses arising from nominations submitted by the shareholder).

- Additional Restrictions. While noting that it is not entirely clear what “additional restrictions” the proposal referred to, many of the no-action request letters acknowledged that the company’s bylaws impose certain requirements on shareholder-nominated candidates that do not expressly apply to the board’s nominees. Examples include requirements that:

- the shareholder-nominated candidate be independent according to applicable listing standards and/or the company’s governance guidelines;

- the election of the shareholder-nominated candidate not cause the company to violate its governing documents, applicable listing rules or other applicable laws, rules or regulations;

- the shareholder-nominated candidate not be an officer or director of a competitor; and

- the shareholder-nominated candidate not be the subject of certain criminal proceedings or be a “bad actor” under SEC rules.

Many companies took the position that the practical effect of imposing such “additional restrictions on proxy access nominees is to place proxy access candidates and [b]oard nominated candidates on an equal footing,” because the board “does not have the opportunity to follow the same vetting process for shareholder-nominated proxy access candidates.”

Despite these differences, the Staff granted no-action relief to these companies, specifically noting in each case the company’s “representation that the board has adopted a proxy access bylaw that addresses the proposal’s essential objective.”

Three companies, however, which had received a substantially similar shareholder proposal as those companies that received no-action relief, were unsuccessful in obtaining relief in reliance on Rule 14a-8(i)(10). These companies had each adopted proxy access for owners of at least five percent of the company’s outstanding common stock, while the shareholder proposals they received called for proxy access at a three-percent ownership threshold. In each of these cases, the Staff concluded that, based on the information presented by the company in its no-action request, “it appears that [the company’s] policies, practices and procedures do not compare favorably with the guidelines of the proposal and that [the company] has not, therefore, substantially implemented the proposal.” (In one of these cases, the company’s board later amended the company’s proxy access bylaw to reduce the minimum ownership requirement from five percent to three percent of the company’s outstanding common stock and was able to obtain no-action relief from the Staff pursuant to Rule 14a-8(i)(10).)

One additional company—H&R Block, Inc.—was unsuccessful in its substantial implementation argument, though with regard to a proxy access shareholder proposal that was phrased as a request that the company’s board adopt and present for shareholder approval specific revisions to the company’s existing proxy access bylaw. H&R Block’s proxy access bylaw, which it had adopted last year, permits a shareholder or a group of up to 20 shareholders owning three percent or more of the company’s outstanding common stock continuously for at least three years to nominate and include in the company’s proxy materials director nominees constituting up to 20 percent of the board. The shareholder proposal submitted to H&R Block requested that the company’s bylaws be revised to “ensure the following:

- The number of shareholder-nominated candidates eligible to appear in proxy materials should be one quarter of the directors then serving or two, whichever is greater.

- Loaned securities should be counted toward the ownership threshold if the nominating shareholder or group represents that it has the legal right to recall those securities for voting purposes, will vote the securities at the annual meeting, and will hold those securities through the date of that meeting.

- There should be no limitations on the number of shareholders that can aggregate their shares to achieve the required 3% ownership to be an ‘Eligible Shareholder.’

- There should be no limitation on the renomination of shareholder nominees based on the number of percentage votes received in any election.”

Citing the group of no-action letters issued earlier this year with regard to proxy access proposals under Rule 14a-8(i)(10), H&R Block asserted that “[t]he Staff has concluded that proposals calling for a shareholder proxy access bylaw could be excluded as substantially implemented where the company had adopted a bylaw with the same stock ownership amount and length of ownership called for by the proposal, even though the company’s bylaw included certain procedural limitations or restrictions that were inconsistent with or not contemplated by the proposal.” The company took the position that, under this standard, it too has substantially implemented the proposal. The proponent, on the other hand, argued, among other things, that the no-action letters issued by the Staff earlier this year with regard to proxy access proposals under Rule 14a-8(i)(10) “provide no evidence why 3% of shares is considered an essential element to proxy access but having no cap on the number allowed to form a group is not. There is a world of difference between a group of twenty … and an unlimited group.” Perhaps more importantly, the proponent drew a distinction between proposals seeking the adoption of proxy access bylaws and those seeking “revisions to existing proxy access bylaws,” arguing that “once bylaws have been adopted, shareholders must be able to recommend substantive changes.” The Staff ultimately denied H&R Block no-action relief, noting that the Staff was “unable to conclude that H&R Block’s proxy access bylaw compares favorably with the guidelines of the proposal.”

B. Violation of Proxy Rules Under Rule 14a-8(i)(3)

While the vast majority of substantive no-action requests regarding proxy access proposals were based on Rule 14a-8(i)(10), two letters sought no-action relief pursuant to Rule 14a-8(i)(3). Rule 14a-8(i)(3) permits the exclusion of a shareholder proposal “[i]f the proposal or supporting statement is contrary to the Commission’s proxy rules, including Rule 14a-9, which prohibits materially false or misleading statements in [a company’s] proxy soliciting materials.” Both The Interpublic Group of Companies, Inc. and Amphenol Corporation took the position that the proxy access proposals they received—which were substantially identical to those at issue in the no-action requests premised on Rule 14a-8(i)(10)—were “impermissibly vague and indefinite so as to be inherently misleading.”

The Interpublic Group asserted that the shareholder proposal was “vague, indefinite and misleading in at least the following respects”:

- The provision in the proposal that provides that “[n]o additional restrictions that do not apply to other board nominees should be placed on these nominations or re-nominations” is susceptible to multiple interpretations, and “neither the shareholders when voting on the Proposal nor the Board when fashioning the requested bylaw would know what terms or provisions of the requested bylaw would constitute ‘additional restrictions.’”

- The term “beneficial ownership” has many definitions, such as those “found in the securities laws and a vast variety of commercial and governance settings,” and yet this term is undefined in the proposal, rendering the proposal vague, indefinite and misleading. Additionally, the board “is called upon by the Proposal to provide a useful and workable definition [of ‘beneficial ownership’], but in light of the No Additional Restrictions Provision it is not clear” how the board would know that its definition does not violate the “no additional restrictions” provision.

- The proposal’s request that to cap shareholder nominees at “one-quarter of the directors then serving or two, whichever is greater” is vague, because the proposal does not clarify how the board must treat a circumstance in which 25 percent of the board results in a fractional number, and any resolution devised by the board may contravene the “no additional restrictions” provision.

- The meaning and scope of the proposal’s provision that the nominating shareholder certify that it will “assume liability stemming from any legal or regulatory violation arising out of the Nominator’s communications with the Company shareholders” is ambiguous, “nor is it clear how the Board can clarify this language without violating the No Additional Restrictions Provision.”

- The proposal’s language regarding continuous ownership of the requisite amount of stock for three years “is open to multiple definitions and interpretations,” since it “specifies a continuous holding period of three years ‘before’ submitting the nomination, which would potentially allow any prior three-year period of continuous ownership to enable a Nominator to submit a nominee, not just the three years leading up to and including the day of submission.” If the board were to clarify, when adopting its bylaw, that the shares must have been held continuously for at least three years as of the date of submission, the board would not know whether it had violated the “no additional restrictions” provision.

Amphenol Corporation similarly took the position that there were “multiple ways” in which the company and its shareholders could interpret the proposal, but focused on the fact that the proposal did not “provide any clarity as to what steps the Proponent expects the Company and its stockholders to take in order to implement the Proposal.” Specifically, Amphenol Corporation noted that it was unclear whether, upon passage of the shareholder proposal, the shareholder proponent expected the board to:

- “adopt a resolution setting forth the amendment proposed, declaring its advisability, and either calling a special meeting for consideration of the amendment or directing that the amendment be considered at the next annual meeting of shareholders”;

- approve the proposed bylaw and call on the shareholders to approve the proposal at the next annual meeting, though the bylaw would remain effective regardless of the outcome of the shareholder vote;

- approve the proposed bylaw and call on the shareholders to approve the proposal at the next annual meeting, and if the shareholders reject the bylaw, it would be repealed; or

- “present the proposed bylaw for approval by stockholders in the manner set forth in the Company’s bylaws, without any special actions by the Board prior to such vote.”

The Staff denied both of the requests for no-action relief under Rule 14a-8(i)(3), noting: “We are unable to conclude that the proposal is so inherently vague or indefinite that neither the shareholders voting on the proposal, nor the company in implementing the proposal, would be able to determine with any reasonable certainty exactly what actions or measures the proposal requires.”

Shortly after receiving the denial of no-action relief, Amphenol Corporation revised its bylaws to adopt proxy access at the 3% / 3-year thresholds and returned to the SEC with a request for no-action relief on the basis of substantial implementation, which the Staff granted.

III. Positions of the Proxy Advisory Firms

A. Institutional Shareholder Services, Inc. (“ISS”)

1. Policy

ISS’s voting policy with regard to proxy access proposals remains unchanged from last year.

Unlike the case-by-case approach it used in evaluating these proposals prior to 2015, ISS’s current policy provides that it will generally recommend a vote in favor of management and shareholder proxy access proposals with the following features:

- A maximum ownership threshold of three percent of the voting power;

- A maximum duration requirement of three years of continuous ownership for each member of the nominating group;

- “[M]inimal or no limits on the number of shareholders permitted to form a nominating group”;

and

- A cap on shareholder nominees generally set at 25% of the board.

ISS will also “[r]eview for reasonableness any other restrictions on the right of proxy access” and will “[g]enerally recommend a vote against proposals that are more restrictive than these guidelines.”

This proxy season, ISS also issued a new Frequently Asked Question (“FAQ”) regarding proxy access, which delved into how ISS will evaluate a board’s implementation of proxy access in response to a majority supported shareholder proposal. The FAQ provides that, in assessing a board’s response to a majority supported shareholder proposal seeking proxy access, ISS will examine “whether the major points of the shareholder proposal are being implemented” and whether additional provisions that were not included in the shareholder proposal “unnecessarily restrict the use of a proxy access right.” ISS’s assessment will inform its vote recommendation with regard to individual directors, nominating/governance committee members or the entire board, as appropriate.

The FAQ further specifies that ISS may issue adverse vote recommendations “if a proxy access policy implemented or proposed by management contains material restrictions more stringent than those included” in the shareholder proposal with respect to the following features, “at a minimum”:

- An ownership threshold above three percent;

- Ownership duration longer than three years;

- A limit on the number of shareholders who may be aggregated to form a group set at below 20 shareholders; and

- A cap on proxy access nominees below 20 percent of the board.

According to ISS, where an aggregation limit or cap differs from that provided in the shareholder proposal, “lack of disclosure by the company regarding shareholder outreach efforts and engagement may also warrant negative vote recommendations.”

Turning to the addition of provisions in the company’s proxy access policy or management proposal beyond those included in the shareholder proposal, ISS indicated that it will review “restrictions or conditions on proxy access nominees” on a case-by-case basis. The restrictions ISS deems problematic, “especially when used in combination include, but are not limited to:

- Prohibitions on resubmissions of failed nominees in subsequent years;

- Restrictions on third-party compensation of proxy access nominees;

- Restrictions on the use of proxy access and proxy contest procedures for the same meeting;

- How long and under what terms an elected shareholder nominee will count toward the maximum number of proxy access nominees; and

- When the right will be fully implemented and accessible to qualifying shareholders.” In addition, the two types of restrictions that ISS considers “especially problematic” are:

- “Counting individual funds within a mutual fund family as separate shareholders for purposes of an aggregation limit; and

- The imposition of post-meeting shareholding requirements for nominating shareholders.”

2. Practice

This proxy season:

- ISS recommended a vote “For” all but one of the 83 proxy access shareholder proposals submitted to Russell 3000 companies for which it has published a report (including those proposals that were subsequently withdrawn). The sole shareholder proposal to receive a negative ISS vote recommendation this proxy season was submitted to Peoples Financial Services Corp. and, unlike every other shareholder proposal submitted this year, sought proxy access for those owning 1.5% of the company’s outstanding stock for at least two years.

- ISS recommended a vote “For” 18 of the 21 proxy access proposals submitted by management for which it published a report. In the three cases in which ISS recommended a vote “Against” a management-sponsored proposal on proxy access, ISS voiced concerns about various provisions it deemed “overly restrictive”—most notably, a five-percent ownership threshold and/or an aggregation limit of 10 shareholders.

B. Glass Lewis

1. Policy

Glass Lewis’s policy, which remains unchanged from last year, provides that the proxy advisory firm “will consider supporting reasonable proposals requesting shareholders’ ability to nominate director candidates to management’s proxy” and will review such proposals on a case-by-case basis, considering the following factors:

- company size;

- board independence and diversity of skills, experience, background and tenure;

- the shareholder proponent and its rationale for submitting the proposal;

- the proposal’s ownership threshold and holding period requirement;

- shareholder base in both percentage of ownership and type of shareholder;

- responsiveness of board and management to shareholders evidenced by progressive shareholder rights policies (e.g., majority voting, declassified boards) and reaction to shareholder proposals;

- company performance and steps taken to improve poor performance;

- existence of anti-takeover protections; and

- opportunities for shareholder action (e.g., ability to act by written consent, right to call a special meeting).

Given the SEC’s recent release of SLB 14H, which leaves open the option for issuers to submit a shareholder proposal alongside a management proposal on the same issue, Glass Lewis added a policy to its proxy voting guidelines this year that articulates its approach to analyzing dueling proposals. In reviewing dueling proposals, Glass Lewis will consider the following factors:

- “The nature of the underlying issue;

- The benefit to shareholders from implementation of the proposal;

- The materiality of the differences between the terms of the shareholder proposal and management proposal;

- The appropriateness of the provisions in the context of a company’s shareholder base, corporate structure and other relevant circumstances; and

- A company’s overall governance profile and, specifically, its responsiveness to shareholders as evidenced by a company’s response to previous shareholder proposals and its adoption of progressive shareholder rights provisions.”

2. Practice

Glass Lewis generally recommends voting “For” proxy access shareholder proposals. Notably, in the three instances this year in which a company submitted competing shareholder and management proposals to a vote, each of which included a three-percent shareholding threshold, Glass Lewis recommended voting “Against” the shareholder proposal while supporting the management proposal.

Glass Lewis recommended a vote “For” 19 of the 21 proxy access proposals submitted by management this year. In the two cases in which Glass Lewis recommended a vote “Against” the management-sponsored proposal, the proposal included a five-percent shareholding threshold.

IV. Positions of Large Institutional Shareholders

At present, there is no consensus among the major institutional shareholders on the issue of proxy access. BlackRock and State Street Global Advisors, for example, currently consider proxy access proposals on a case-by-case basis. BlackRock’s present policy, which remains unchanged from last year, reflects its belief that “long-term shareholders should have the opportunity, when necessary and under reasonable conditions, to nominate individuals to stand for election to the boards of the companies they own and to have those nominees included on the company’s proxy card,” provided that the proxy access mechanism will “provide assurances that the mechanism will not be subject to abuse by short-term investors, investors without a substantial investment in the company, or investors seeking to take control of the board.” State Street Global Advisors supports shareholder proposals on proxy access “that set parameters to empower long-term shareholders while providing management the flexibility to design a process that is appropriate for the company’s circumstances.” In deciding how to vote, State Street will take into account considerations such as “the ownership thresholds and holding duration proposed in the resolution, the binding nature of the proposal, the number of directors that shareholders may be able to nominate each year, company governance structure, shareholder rights, and board performance.”

The Vanguard Group also currently considers proxy access proposals on a case-by-case basis, but generally supports proxy access provisions that provide a shareholder (or group of shareholders) holding three percent of a company’s outstanding shares for at least three years with the right to nominate up to 20% of the board’s directors. The Vanguard Group may, however, “support different thresholds based on a company’s other governance provisions, as well as other relevant factors.” This policy represents a change from last year, in which Vanguard supported provisions that sought proxy access for holders of five percent of the company’s outstanding shares.

Finally, Fidelity Management & Research is currently opposed to proxy access, generally voting against management and shareholder proposals seeking to implement proxy access.

V. Proxy Access Proposal Trends

A. Overall Trends

- For the second year in a row, proxy access shareholder proposals were the most popular of the governance-related proposals. A total of 78 shareholder proposals have gone to a vote thus far among Russell 3000 companies (with two proposals pending as of July 15, 2016), as compared to 87 proposals that have gone to a vote in 2015. In contrast, between 12 and 17 proxy access shareholder proposals were submitted to a vote in each of the previous three years.

- Shareholder proponents continue to converge on the 3% / 3-year thresholds. All but one proposal submitted to a vote at Russell 3000 companies called for proxy access at the thresholds of three percent and three years. As noted earlier, only one proposal broke with this trend, seeking proxy access for holders of 1.5% of the company’s outstanding stock for at least two consecutive years. This continues the trend observed last year, in which all 87 proposals submitted to a vote at Russell 3000 companies called for proxy access at the 3% / three-year thresholds. In contrast, of the 17 shareholder proposals submitted to a vote in 2014, only ten contained the 3% / three-year thresholds.

- More than half of this year’s shareholder proposals capped proxy access nominees at the greater of 25% of the board or 2 directors. Forty-three of the 78 proposals that were submitted to a vote (or 55%) capped proxy access nominees at the greater of 25% of the board or 2 directors, while the remaining 35 proposals (or 45%) sought a cap of 25% of the board. This reflects the somewhat increased sophistication of shareholder proposals this proxy season as compared with last year’s proposals, 98% of which capped proxy access nominees at 25% of the board (while the remaining two percent capped shareholder nominees at 20% of the board).

- Most of this year’s shareholder proposals explicitly provided that an unrestricted number of shareholders may be aggregated to reach the shareholding threshold. Forty-seven of the 78 proposals that reached a vote at Russell 3000 companies this year (or 60%) requested that there be no group limit for purposes of reaching the requisite ownership threshold, while the remaining 31 proposals (or 40%) were silent on the issue of group size limitations. This represents a meaningful change from last year, in which the overwhelming majority of shareholder proposals were silent with respect to limits on the number of shareholders that can be aggregated to form a group.

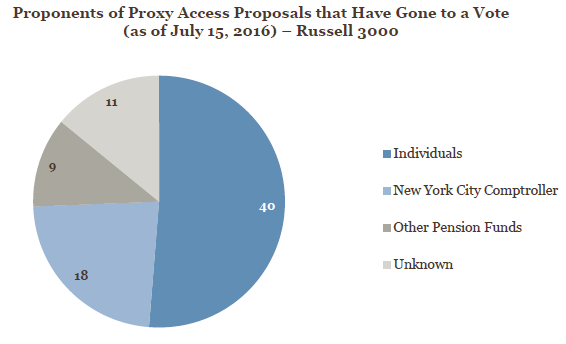

- While the New York City Comptroller’s office submitted many proxy access proposals this year, the majority of proposals that reached a vote were submitted by individuals. At least 40 of the 78 shareholder proposals that reached a vote this year at Russell 3000 companies (or 41.3%) were submitted by individuals. Only 18 of the 78 proposals that reached a vote among the Russell 3000 (or 23.1%) were submitted by the New York City Comptroller’s office, primarily due to the high rate of successful negotiations between issuers and the Comptroller’s office this year. Across all indices, 20 of the 72 shareholder proposals sponsored by the New York City Comptroller’s office (or 27.8%) reached a vote this year, in contrast to 66 of the 75 proposals (or 88%) submitted by the Comptroller’s office in 2015.

- Vote results have been decidedly mixed. Of the proposals that have been voted on at Russell 3000 companies so far this season, 41 shareholder proposals (or 52.6%) have passed, while 37 shareholder proposals (or 47.4%) have failed. Two proposals remain pending as of July 15. In contrast, in 2015, 53 of 87 shareholder proposals (or 60.9%) passed, while 34 proposals (or 39.1%) failed.

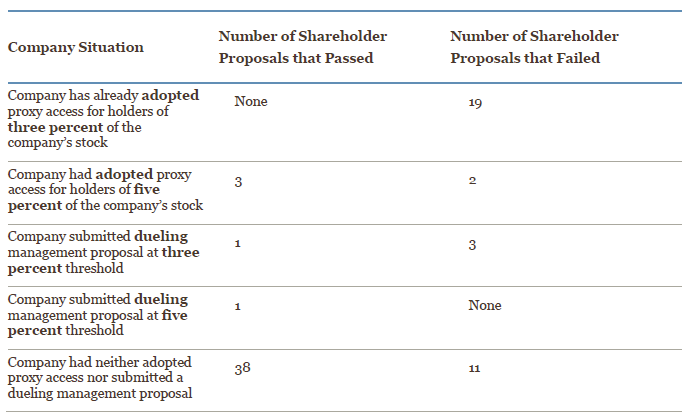

- The major factor determining the vote results this year appears to be whether the company has already adopted proxy access. There were 19 cases this year in which companies that had already adopted proxy access at the 3% / 3-year thresholds nonetheless received and submitted to a vote a shareholder proposal on proxy access. In each of these cases, the shareholder proposal failed. Shareholder proposals submitted to companies that neither adopted proxy access nor were submitting a dueling management-sponsored proposal to a vote fared significantly better. Thirty-eight of the 49 shareholders’ proposals in this category (or 77.6%) garnered majority support, while the remaining 11 proposals (or 22.4%) failed.

- Average shareholder support for proxy access shareholder proposals decreased slightly from last year, though shareholder support varied meaningfully depending on whether a company had already adopted proxy access. Proxy access shareholder proposals among Russell 3000 companies received average support of 51.1%% thus far in 2016, compared to 55% average support in 2015. While significantly higher than the 30.9% average shareholder support these proposals received in 2014, this year’s average shareholder support is roughly consistent with the 53.4% average support for proposals with 3% / three-year thresholds in 2014. Notably, at companies that had not already adopted a proxy access bylaw, average shareholder support of shareholder proposals with 3% / 3-year thresholds rose to 64.2%. Conversely, at companies that had already adopted some form of proxy access, average shareholder support was only 37.9%.

B. Management Responses to Proxy Access Shareholder Proposals

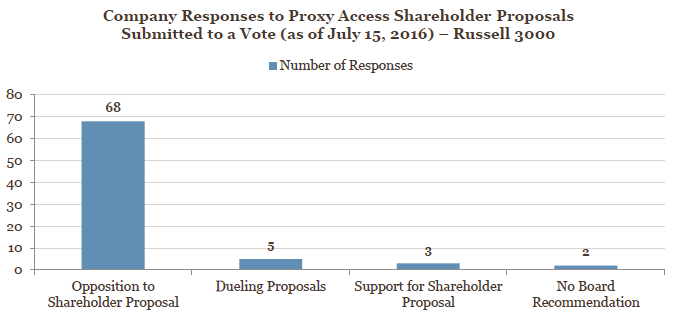

Putting aside cases in which management negotiated successfully with the shareholder proponent for exclusion of the proposal, companies chose to pursue different options in response to proxy access shareholder proposals. While the vast majority of companies submitting a proxy access shareholder proposal to a vote opposed the proposal, others determined to include the proposal alongside a competing management proposal, supported the shareholder proposal or did not provide any board recommendation with regard to the shareholder proposal.

C. Trends Among Companies Submitting Dueling Proposals

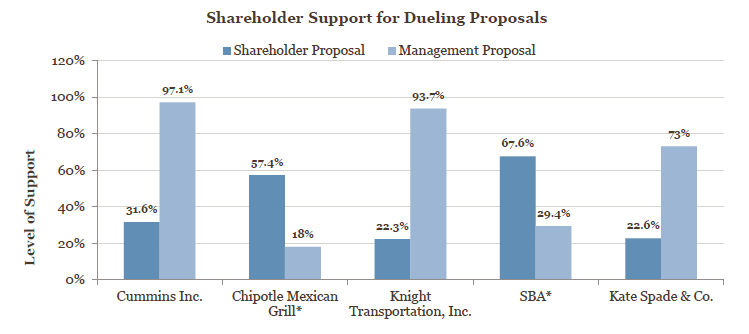

Vote results for shareholder proposals that were submitted in conjunction with a competing management proposal were mixed. In two of the five cases of dueling proposals, the shareholder proposal passed, while the management proposal failed. In both of these cases, the management proposal sought proxy access at the five percent shareholding threshold. In the three cases in which the shareholder proposal and the management proposal both sought proxy access for holders of three percent of the company’s stock, however, the shareholder proposal failed, while the competing management proposal passed by a significant margin.

* In these cases, the management-sponsored proposal sought proxy access at the 5% threshold. In addition, both of these companies submitted dueling proposals last year, and the vote results were significantly closer then. At Chipotle, both proposals failed last year, with the shareholder proposal garnering 49.9% support and the management proposal receiving 34.5% support. At SBA, the management proposal passed last year, receiving 51.7% support, while the shareholder proposal received 46.3% support.

VI. Proxy Access Adoption Trends

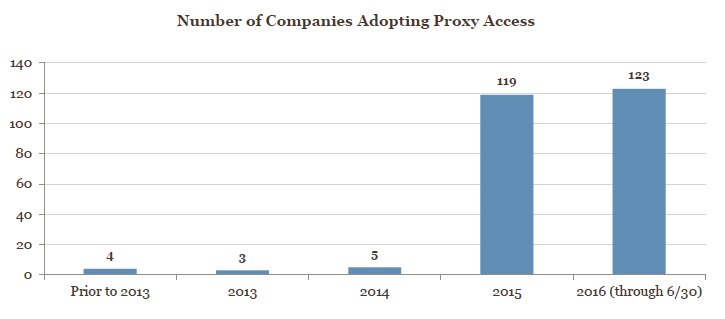

This year, there has been a steep increase in the number of companies that had adopted proxy access. Last year, 119 companies adopted proxy access, compared to a total of 12 companies that had adopted proxy access before then. This trend has accelerated in 2016, with an increasing number of companies adopting proxy access pre-emptively.

As of June 30, 2016, approximately 38% of companies in the S&P 500 index and approximately 73% of companies in the Dow 30 index have adopted proxy access thus far. In contrast, by June 30, 2015, only 3.8% of the S&P 500 and 6.7% of the Dow 30 had adopted proxy access.

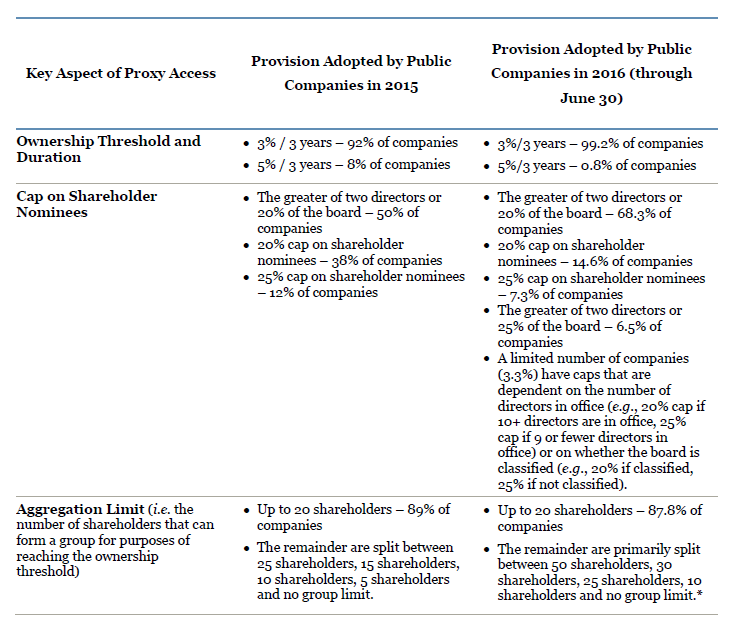

While there is variation in the proxy access bylaws adopted by public companies, their most significant provisions are generally consistent.

* An additional two companies have aggregation limits that are subject to change. In one instance, the company’s limit of 20 shareholders increases to 25 shareholders if the company’s revenues for the prior fiscal year exceeds a certain threshold. In another case, the company’s chosen limit of 10 shareholders increases to 25 shareholders if the company’s market cap for the prior fiscal year exceeds $1 billion.

VII. Takeaways

As evidenced this season, a key factor influencing the vote results is whether a particular company had already adopted proxy access. Given this observation—and in light of the SEC Staff’s clarification that the adoption of proxy access at the 3% / 3-year thresholds substantially implements a proposal with the same thresholds, despite other differences between the shareholder and management proposals—more companies have adopted proxy access in the first six months of this year than in all of 2015. This trend is likely to continue, particularly as more companies appreciate that the Comptroller’s office and other shareholder proponents are likely to continue submitting proxy access proposals and that, especially for larger companies, receiving such a proposal is a question of when, not if.

Since the “private ordering” of proxy access at the 3% / 3-year thresholds is very likely to continue, issuers that have not yet adopted proxy access should consider how they will approach proxy access in the coming months. In preparation for the 2017 proxy season, issuers that have not yet adopted proxy access and their in-house counsel should consider taking the following actions:

- Educate the Board. The board of directors should be informed of the trends that have developed during the 2016 proxy season, as well as the advantages and disadvantages of pre-emptively adopting proxy access.

- Evaluate the Company’s Shareholder Base and Engage with Shareholders. As noted above, there is no consensus among the large institutional shareholders on the issue of proxy access. Issuers considering the adoption of a proxy access bylaw should analyze their shareholder base and their shareholders’ policies on proxy access and should begin to engage their largest shareholders.

- Consider the Proxy Access Structure, If Any, Appropriate for the Company. To the extent a company is open to voluntarily adopting a proxy access bylaw, it should consider which thresholds and which “bells and whistles” it might want to include in the provision.