Print

PrintMatthew C. Plosser is an Economist in the Financial Intermediation Function at the Federal Reserve Bank of New York. This post is based on a forthcoming article by Mr. Plosser, Valentin Haddad, Assistant Professor of Economics at Princeton University, and Erik Loualiche, Assistant Professor of Finance at the MIT Sloan School of Management.

Leveraged buyouts are a powerful tool to alter incentives in firms and improve their corporate governance. Despite these benefits, the use of the buyout transaction varies wildly over time. In the U.S., peak buyout years exhibit close to one hundred public-to-private transactions and trough years as few as ten. What explains this dramatic time-variation in activity? Prior literature and the popular press largely focus on how the cost of debt impacts buyout activity, as debt is a key input to the buyout transaction. Another popular explanation is a periodical form of irrational exuberance for buyouts.

In Buyout Activity: The Impact of Aggregate Discount Rates (forthcoming, Journal of Finance), we argue that these approaches miss the forest for the trees: the overall cost of capital, rather than debt alone, is the primary driver of buyout activity. We document that common changes in the cost of debt and the cost of equity—also known as the aggregate risk premium—best explain booms and busts in buyout activity. We also outline the economic mechanisms by which the risk premium influence the buyout decision.

The overall risk premium should matter for two reasons. First, buyouts are investments in the improved management of the firm. Like other investments, discounted cash flow analysis can evaluate their attractiveness. Investors discount future cash flows at a rate commensurate with their risk. Less risk results in a lower discount rate and a more attractive buyout opportunity. Hence, time-variation in the price of risk (i.e. the risk premium) varies the benefit of a buyout.

Second, a buyout transaction increases the illiquidity of target firms. Relative to public firms, it is more difficult to sell privately held firms. We demonstrate that the cost of being illiquid is also greater when the risk premium is high. Therefore, a high risk premium not only decreases the present value of cash-flow improvements, but it also increases the costs of making illiquid investments like buyouts.

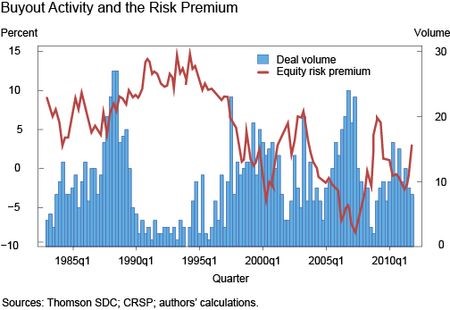

The data broadly support these implications. Figure 1 plots the quarterly number of U.S. public-to-private deals along with our measure of the equity risk premium. Three of the four sustained booms correspond with a decline in the risk premium. Likewise, the sustained drought of buyout activity in the early 1990s corresponds to a persistently high risk premium.

Figure 1: Buyout activity and the risk premium

The primary alternative hypothesis is that the cost of credit uniquely determines the attractiveness of buyout investments, rather than the overall variation in market conditions. When we compare the explanatory power of the equity risk premium to commonly cited credit market factors, like the spread on high yield bonds, we find that the equity premium explains two to three times more variation than credit factors. This does not mean the credit conditions are completely irrelevant, but rather that they are not the primary determinant of buyout activity. The most important driver is the overall attitude of markets towards risk.

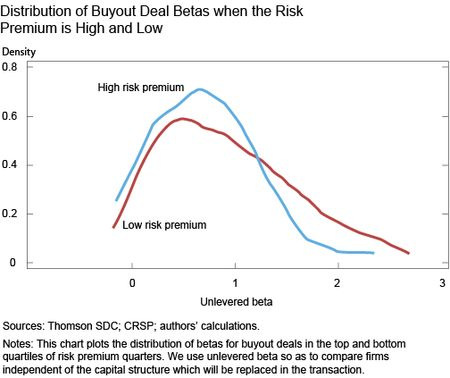

If the price of risk is a core determinant of the buyout decision, we expect the likelihood of particular firms to be buyout targets to be more sensitive to variation in the risk premium. For example, the discount rate for high beta firms is more sensitive to variation in the risk premium. By extension, the present value of a potential buyout declines more for high beta firms than low beta firms when the risk premium rises. Indeed, Figure 2 demonstrates that buyouts of higher beta firms are less common when the risk premium is high compared to when it is low.

Figure 2: Distribution of buyout target betas in high and low risk premium periods

In addition, firms with greater potential gains from a buyout have more future cash-flow that need to be discounted. As a result, they should be more sensitive to variation in discount rates. For instance, strong corporate governance should reduce the potential benefits of a buyout. By extension, such firms should be less sensitive to changes in the risk premium. In fact, we find that firms that have stronger governance are less sensitive to variation in the risk premium.

The forces we outline for the case of the buyout transaction, the present value of cash-flow improvements and illiquidity, also apply to other types of corporate finance activity. For example, mergers and acquisitions typically result in synergies that also should be subject to variation in discount rates. Also, IPOs move firms from private to public markets, influencing their liquidity. We explore these alternative types of activity in the full paper.

The dialogue around buyouts has traditionally centered on the role of credit markets. Our results challenge this view: we document that the aggregate risk premium—the overall demand for risk by all types of investors—is the primary determinant of buyout activity. Given the prominent role the risk premium plays for the buyout cycle, the risk premium’s ability to coordinate corporate finance activity more broadly represents a promising avenue for future research.

The full article can be downloaded here.