Print

PrintYafit Cohn is an associate at Simpson Thacher & Bartlett LLP. The following post is based on a Simpson Thacher publication authored by Ms. Cohn, Karen Hsu Kelley, and Avrohom J. Kess.

Shareholders petitioning the board for the special meeting right propose either to create the right or, in circumstances where the right already exists, lower the minimum share ownership threshold required to exercise the right. As of June 30, 2016, 295 companies in the S&P 500 already provided their shareholders with the right to call a special meeting outside of the usual annual meeting, as compared with 286 companies at this time last year. Among companies in the Russell 3000, approximately 1,300 provide their shareholders with the right to call special meetings. During the 2016 proxy season, 19 special meeting shareholder proposals went to a vote at Russell 3000 companies. Of these, five proposals sought to create the right, one of which received majority shareholder support to create the right for holders of 15% of the company’s outstanding common stock. The other 14 proposals sought to lower the ownership threshold with respect to an existing right, two of which received majority support; these proposals requested to lower the threshold of an existing right to 10% from either 25% or 50%. Overall, shareholder proposals relating to special meetings received average shareholder support of 41.5% this proxy season.

I. Positions of the Proxy Advisory Firms

A. Institutional Shareholder Services Inc. (“ISS”)

With respect to proposals related to special meetings, consistent with its position in 2015, ISS generally recommends:

- voting against proposals that restrict or prohibit a shareholder’s right to call a special meeting; and

- voting for proposals that provide shareholders with the ability to call a special meeting.

ISS prefers a 10% minimum shareholding threshold as opposed to the 20-25% threshold typically favored by management. Notwithstanding its preference, ISS recommended a vote “for” nearly all shareholder proposals in 2016, even those that proposed a threshold greater than 10%. Likewise, ISS recommended a vote “for” 11 of the 12 management proposals submitted to a vote in 2016, even though none of them proposed a threshold of 10% and one was submitted together with a competing shareholder proposal.

ISS’s recommendations suggest that its view is that some right to call a special meeting is better than no right.

Equally important is ISS’s policy on substantial implementation. If ISS determines that a proposal that received majority support was not substantially implemented by the board, ISS will recommend a vote “against” one or more directors the following year. Failure to substantially implement the proposal includes situations where the board implements the proposal at a different ownership threshold than the one proposed and/or where the board imposes significant limitations on the right. If, however, the company’s shareholder outreach efforts reveal that a different threshold is acceptable to the company’s shareholders, “and the company disclosed these results in its proxy statement, along with the board’s rationale for the threshold chosen,” ISS has indicated that it will take this into account on a case-by-case basis. ISS will similarly consider the ownership structure of the company. With regard to limitations on the right to call a special meeting, ISS finds “reasonable limitations on the timing and number per year of special meetings” to be “generally acceptable.”

ISS considers the right of shareholders to call special meetings beyond just the context of shareholder proposals. For instance, ISS takes into account the “inability of shareholders to call special meetings” as a factor in considering whether to recommend a vote against an entire board of directors where the board “lacks accountability and oversight, coupled with sustained poor performance relative to peers.”

Additionally, ISS considers the special meeting right when calculating its Governance QuickScore in both the Board Structure Pillar and the Shareholder Rights & Takeover Defenses Pillar. For the former pillar, ISS considers a unilateral board action that diminishes shareholder rights to call a special meeting to be an action that “materially reduces shareholder rights,” which could negatively impact a company’s score.

In calculating the latter pillar, ISS takes into account “whether shareholders can call a special meeting,

and, if so, the ownership threshold required.” It also considers whether there are “material restrictions” to the right, which include restrictions on timing, “restrictions that may be interpreted to preclude director elections,” and restrictions that effectively raise the ownership threshold.

B. Glass Lewis

Consistent with its position in 2015, Glass Lewis is in favor of providing shareholders with the right to call a special meeting, preferring an ownership threshold of 10-15%, depending on the size of the company, in order to “prevent abuse and waste of corporate resources by a small minority of shareholders.” In forming its recommendation, Glass Lewis also takes into account several other factors, including whether the board and management are responsive to proposals for shareholder rights policies, whether shareholders can already act by written consent and whether anti-takeover provisions exist at the company.

In addition, Glass Lewis considers the right to call special meetings an “important shareholder right” and recommends voting against members of the governance committee who hold office while management infringes upon “important shareholder rights,” such as when the board unilaterally removes such rights or when the board fails to act after a majority of shareholders has approved such rights.

II. Positions of Large Institutional Shareholders

While their current positions on special meeting proposals vary, the major institutional investors generally favor shareholders having the right to call special meetings and usually focus on a few key variables, e.g., the minimum ownership threshold associated with the right. For instance, State Street Global Advisors votes for proposals that set the threshold at 25% or less but not less than 10%, and BlackRock supports proposals that set the threshold at 25% or less but not less than 15%. Conversely, other investors, like Fidelity Management & Research Co., recommend voting for a proposal if the threshold is 25% or more. Still others, such as Vanguard, support shareholders’ right to call special meetings (for good cause and with ample representation) and will generally vote for proposals to grant the right, irrespective of the minimum ownership threshold, and against those that seek to abridge the right. Sometimes, investors’ policies take into account whether or not the company already provides for a shareholder right to act by written consent.

In addition, some investors support management proposals outright but are more wary of shareholder proposals that may support the narrow interests of one or few shareholders.

III. SEC No-Action Letters

The 2016 proxy season was marked by a meaningful decrease of no-action requests with regard to special meeting shareholder proposals, with only two requests made on procedural grounds (both of which were granted) and no requests made pursuant to Rule 14a-8’s substantive exclusions. This is a significant decrease from 2015, during which there were a total of 17 no-action requests seeking the exclusion of special meeting shareholder proposals, 14 of which were based on substantive grounds.

This decrease is, at least in large part, due to the issuance by the Securities and Exchange Commission (“SEC”) of Staff Legal Bulletin 14H (“SLB 14H”) on October 22, 2015, which clarified the SEC’s view of Rule 14a-8(i)(9)—the provision that permits the exclusion of a shareholder proposal that “directly conflicts with one of the company’s own proposals to be submitted to shareholders at the same meeting.” Alleviating the uncertainty created by the Division of Corporation Finance’s announcement in early 2015 that it would not consider no-action requests based on Rule 14a-8(i)(9) during the 2015 proxy season, SLB 14H indicated that, in considering no-action requests under Rule 14a-8(i)(9), the SEC would now focus on “whether there is a direct conflict between the management and shareholder proposals,” explaining that “a direct conflict would exist if a reasonable shareholder could not logically vote in favor of both proposals.” In essence, under the SEC’s new approach, if the proposals are “in essence, mutually exclusive,” then the shareholder proposal would be excludable; otherwise the proposal may not be excluded on the basis of Rule 14a-8(i)(9). SLB 14H further suggested that a pair of proposals on the same general subject matter but containing different eligibility thresholds would not be deemed “directly conflicting” for purposes of Rule 14a-8(i)(9).

Accordingly, unlike last year, in which 12 no-action requests pertaining to special meeting shareholder proposals were predicated on Rule 14a-8(i)(9), no company submitted a request for no-action relief to exclude a special meeting proposal on the ground that it was submitting a competing management-sponsored proposal on the issue. In fact, 2016 was the first year since 2008 that no companies submitted no-action requests to the SEC on the basis of Rule 14a-8(i)(9) with respect to special meeting shareholder proposals. More broadly, 2016 marked the first year in which there were zero no-action requests regarding special meeting proposals submitted to the SEC on substantive grounds since the SEC’s Division of Corporate Finance began publishing no-action letters on its website on October 1, 2007.

IV. Special Meeting Proposal Trends

A. Overall Trends

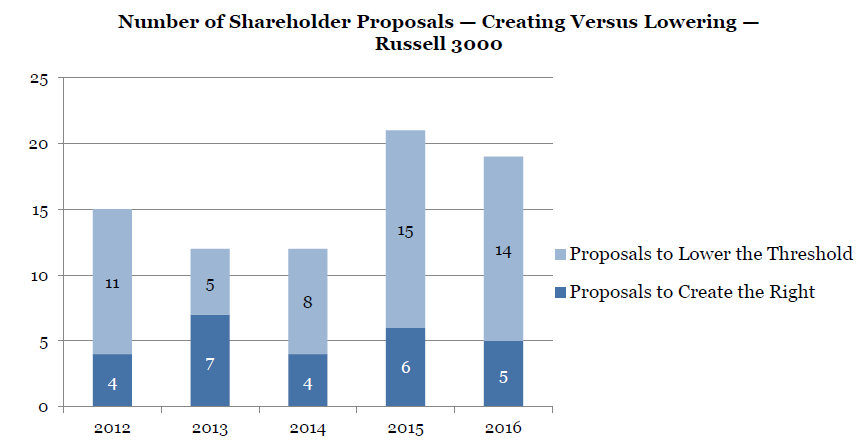

- This proxy season saw a similar number of special meeting proposals to last year. The number of proposals submitted by shareholders seeking either to create the right to call special meetings or to lower the threshold requirement for share ownership held steady during 2016, with 19 proposals going to a vote at Russell 3000 companies, compared with 21 such proposals going to a vote in 2015. With the exception of last year, a higher number of special meeting shareholder proposals has not been submitted since 2011, when there were at total of 27 such proposals. The high water mark for special meeting shareholder proposals came in 2009, in which a total of 52 such proposals were submitted to a vote.

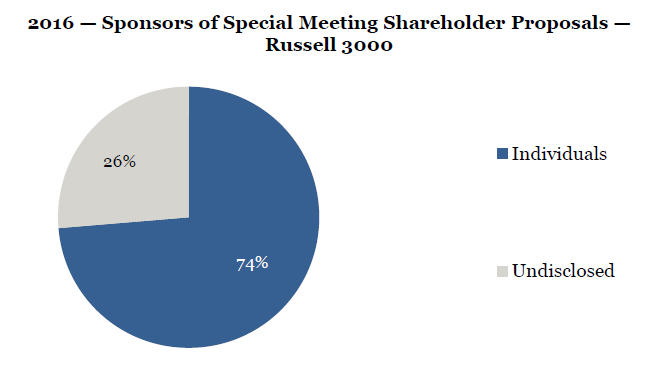

- As in 2015, the majority of proposals were submitted by individual activist shareholders. Three proponents—John Chevedden, James McRitchie and Shawn McCreight—submitted 100% of the shareholder proposals submitted by individuals.

B. Creating the Right Versus Lowering the Threshold

The increase in special meeting shareholder proposals over the past two years has resulted from a greater increase in the number of shareholder proposals to lower the threshold for an existing right than to create the right.

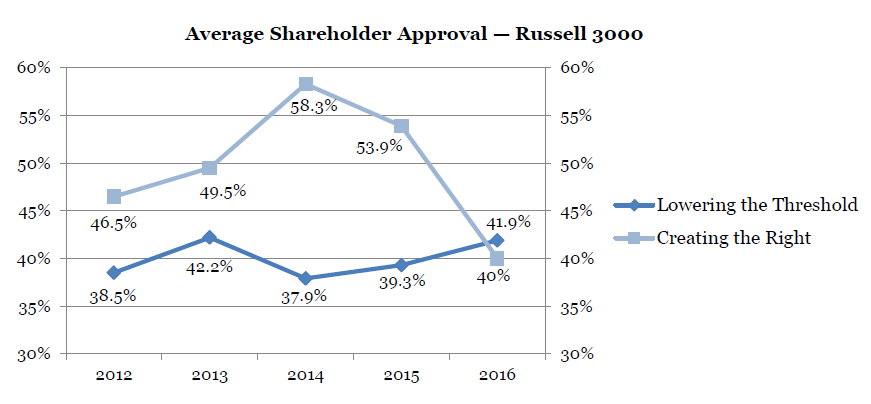

Shareholder proposals to create the right to call a special meeting have historically been more likely to receive majority or close-to-majority support than shareholder proposals to lower the threshold. Over the past five years, 53.6% of proposals (or 15 of 28) to create the right have passed, whereas 13.5% of all proposals (or seven of 52) to lower the threshold of an existing right have passed.

Additionally, in previous years, shareholder proposals to create the right received meaningfully higher average shareholder support than proposals seeking to lower the threshold of an existing right. This year, average shareholder support for shareholder proposals seeking to create the right to call a special meeting dropped significantly, though this seems to be the result of unusually low support at one company. When this company is removed from the calculation, average shareholder support for these proposals increased to 51.3%, which is more in line with average shareholder support observed in previous years.

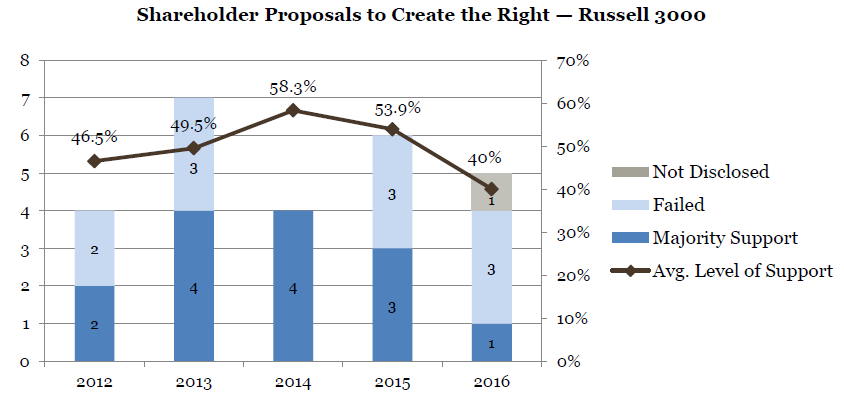

1. Creating the Right

Of the 19 proposals that went to a vote in 2016, five sought to create the special meeting right for the first time. Only one out of these five proposals received majority support this proxy season, representing a considerably lower success rate than observed in previous years.

This year, the average level of shareholder support for proposals seeking to create the right fell to 40% but, when corrected for one outlier, was 51.3%.

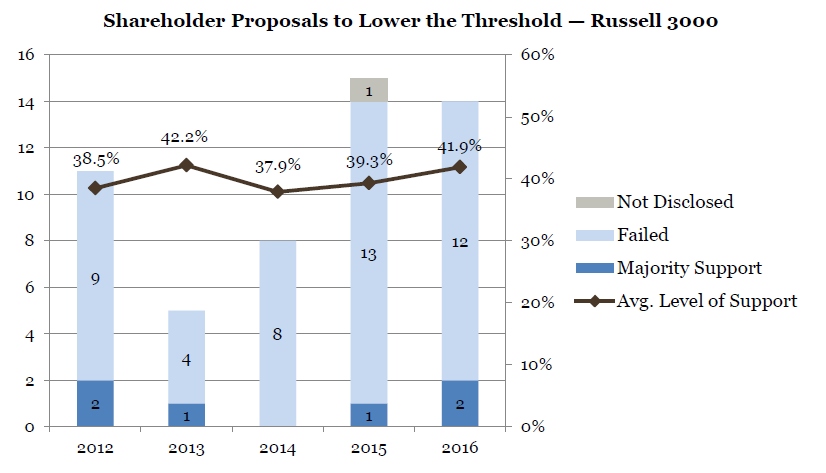

2. Lowering the Threshold

Of the 19 special meeting shareholder proposals that reached a vote in 2016, 14 proposed to lower the ownership threshold of an existing right. This number is consistent with 2015 but reflects a significant increase from previous years. Notwithstanding this increased number of proposals seeking to lower the threshold, only two of these proposals (submitted to CBRE Group, Inc. and Staples, Inc.) garnered majority support this year, which is generally consistent with the low success rate of these proposals in previous years.

The average level of shareholder support in 2016 for proposals seeking to lower the threshold was 41.9%, generally comparable to the shareholder support these proposals received over the past five years, which ranged from 37.9% to 42.2%.

C. Management Responses to Special Meeting Shareholder Proposals

Following the SEC’s issuance of SLB 14H, which clarified the application of Rule 14a-8(i)(9) to exclude “directly conflicting” proposals and suggested that a special meeting shareholder proposal could not be excluded by submitting a management-sponsored proposal with a different eligibility threshold, issuers that received special meeting shareholder proposals were faced with three options, aside from negotiating with the proponents. These options are represented in the chart below, along with the companies that chose each option, the breakdown of which proposals sought to create the right and which sought to lower the threshold, and the results of the vote.

| Option | Companies | Results |

|---|---|---|

| 1. Include the shareholder proposal with an opposition statement from management (15 companies) |

|

Three of the 15 proposals sought to create the right; one received majority support (Average Support = 40.0%)

13 of the 15 proposals sought to lower the threshold; two received majority support (Average Support = 41.1%) |

| 2. Include the shareholder proposal with dueling management proposal (3 companies)* |

|

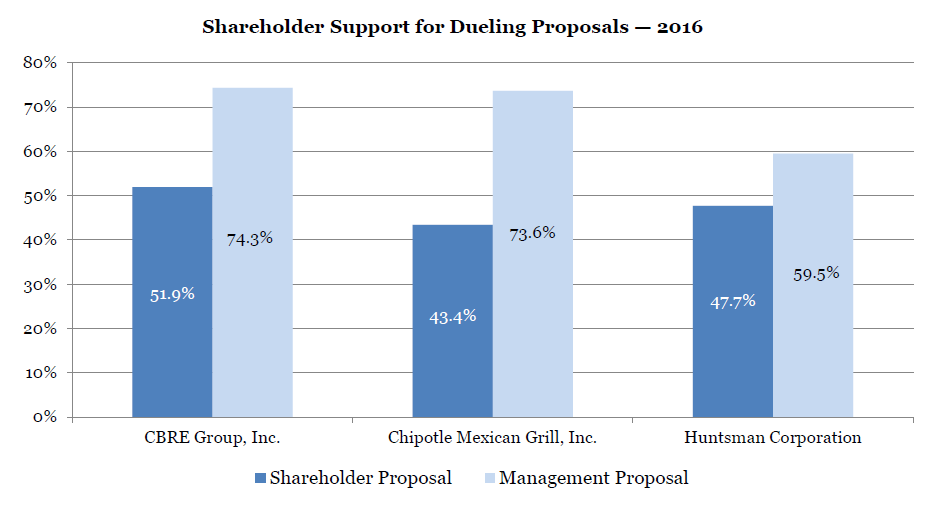

The proposal at CBRE sought to lower the threshold; it received majority support (Support = 51.9%)

The proposals at Chipotle and Huntsman sought to create the right; none received majority support |

| 3. Negotiate with shareholders to include a management proposal at a later date in 2016 (1 company)** | Rofin-Sinar Technologies Inc. | The management proposal sought to create the right with a 25% threshold; failed to receive the 80% support needed to pass. |

* In each case where the company submitted a competing management proposal, the management proposal garnered majority support.

** The annual meeting was originally scheduled for March 17, 2016. In connection with that meeting, the company’s management actually supported the shareholder proposal to create the right to call a special meeting for holders of 15% of the company’s stock, but the meeting was postponed. A subsequent meeting took place on June 29, 2016, at which a management proposal to create the right with a 25% threshold garnered 76.9% of the vote but failed to pass due to an 80% supermajority voting requirement.

D. Trends Among Companies Submitting Dueling Proposals

Three special meeting shareholder proposals were submitted along with dueling management proposals this year; two of them failed and one of them garnered majority support. This result is in contrast to last year, during which there were six pairs of competing special meeting proposals, and in five of those cases, the shareholder proposal received majority support.

Interestingly, the shareholder proposal that garnered majority support this year, which was submitted to a vote at CBRE Group, Inc., was part of a pair of competing proposals in which the management proposal also received majority support. This marks the first instance in which both proposals in a pair of dueling proposals received majority support. CBRE’s proxy materials addressed the possibility that both proposals might pass, stating that if the management proposal is approved, “it will be binding” and the management’s “Proposed Charter Agreement and related by-law amendments will become effective, regardless of the voting outcome on the Stockholder Proposal.” The company’s proxy materials further stated that in this scenario, the company “will not implement the Stockholder Proposal irrespective of its voting outcome (and even if the Stockholder Proposal also receives a majority affirmative vote …).”

E. Trends Among Companies That Unilaterally Adopted the Right to Call Special Meetings

In 2016, two companies—Ally Financial Inc. and MetLife, Inc.—chose to amend their bylaws to provide shareholders holding a minimum of 25% of shares with the right to call special meetings and did not submit either a management or shareholder proposal to a vote. The move to provide the right by Ally Financial Inc. arose in conjunction with the company replacing plurality voting with majority voting in uncontested director elections and came shortly after the company appointed a new independent director to its board of directors, thereby expanding its board. Ally’s board chairman, Franklin Hobbs, had expressed frustration with what he felt was negative market perception being reflected in the Ally’s stock price, and the company was seeking ways to “better align management’s and shareholders’ interests.”

Though there is less context in MetLife’s case, the MetLife board stated that the “Board’s decision to proactively adopt such shareholder right incorporates feedback received during [its] regular investor outreach and reflects [the company’s] commitment to strong governance practices.”

F. Threshold Levels

As noted above, 14 of the special meeting shareholder proposals that went to a vote in 2016 sought to lower the ownership threshold of an existing right. Six of these proposals sought to lower the higher existing ownership threshold to a 10% ownership threshold. All but one of these failed, receiving average support of 40.0%. This is relatively consistent with 2015, in which all of these proposals failed, but represents a departure from earlier years. From 2011 through 2014, 29 shareholder proposals sought to lower the threshold of an existing right to 10%, three of which received majority support. At two of these three companies, the existing special meeting right was set at 50%; at the remaining company, the existing right was set at 25%.

Similar to 2015, the current voting trends seems to indicate that shareholders are likely to support some right to call a special meeting. This year’s voting results indicate, however, that shareholders may not necessarily support a 10% threshold. At 18 of the 19 companies that received a shareholder proposal in 2016, shareholders seemed to prefer thresholds of at least 15%, but most often 25%. The voting results at these 19 companies can be broken down as follows:

- Dueling Proposals. When confronted with a shareholder proposal that competed with a management proposal, two companies’ shareholders supported management-sponsored thresholds of 25% and rejected shareholder-sponsored thresholds of 10%. In the case of CBRE Group, Inc. both the management and shareholder proposals received the required majority vote required to pass but management elected to implement the management-sponsored threshold of 30% instead of the shareholder-sponsored threshold of 10%.

- Shareholder Proposals Seeking to Create the Special Meeting Right. When confronted with a shareholder proposal to create the special meeting right, three companies’ shareholders voted to create a special meeting right for holders of 20-25% of the company’s stock.

- Shareholder Proposals Seeking to Lower the Threshold of an Existing Right. When confronted with a shareholder proposal to lower the threshold of an existing right in the absence of a competing management proposal, the vast majority of shareholders rejected entreaties to lower the existing thresholds, which ranged from 15% to 50%. Of the fourteen companies affected:

- At twelve companies, shareholders opted to retain the companies’ preexisting thresholds of 15-30% and voted against shareholder proposals seeking to lower the threshold. Ten of these existing thresholds were set at 25%.

- At one company, shareholders voted in favor of a shareholder proposal to lower the threshold to 15%.

- At one company, CBRE Group, Inc., shareholders voted in favor of a shareholder proposal to lower the threshold to 10%, but since they also voted in favor of the management proposal, only the management-selected threshold of 30% (down from 50%) was implemented.

Similar to 2015, these results suggest that companies that have a special meeting right in the 15-25% range could, depending on the circumstances, be more successful in warding off potential future attempts to lower the threshold.

V. Takeaways

If faced with a shareholder proposal relating to the ability of shareholders to call a special meeting, management should take into consideration whether the proposal seeks to create the right for the first time or to lower the threshold of an existing right. In addition, the likelihood of a proposal garnering majority support depends, in part, on the proposal’s thresholds for triggering the right and the composition of the company’s shareholder base.

In light of the SEC’s new guidance on the application of Rule 14a-8(i)(9), issuers can no longer rely on Rule 14a-8(i)(9) to exclude a special meeting shareholder proposal by virtue of submitting a management- sponsored proposal with a higher threshold. Some companies will find it advantageous to adopt the right to call special meetings unilaterally, permitting the company to maintain control over the specifics of the bylaw and, in specific circumstances, allowing the issuer to petition the SEC for no-action relief to exclude the shareholder proposal under Rule 14a-8(i)(10) for having “substantially implemented” the proposal.

Regardless, as with many governance proposals, it is critical to engage with the company’s shareholders and understand their positions prior to deciding on an approach. In addition, issuers should take into account the possibility that failure to substantially implement a special meeting shareholder proposal that received majority support can yield negative vote recommendations from the proxy advisory firms against one or more of the company’s directors.

The complete publication, including footnotes, is available here.