Print

PrintJames F. Reda is a Managing Director at Arthur J. Gallagher & Co. This post is based on an Arthur J. Gallagher publication by Mr. Reda, David M. Schmidt, and Kimberly A. Glass. Related research from the Program on Corporate Governance includes Paying for Long-Term Performance by Lucian Bebchuk and Jesse Fried (discussed on the Forum here).

Over six years ago, the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”) was signed into law. Implementation of this Act by the Securities and Exchange Commission (“SEC”) continues to unfold slowly and with increasing uncertainty following this year’s election.

The initial proposal of the CEO pay ratio disclosure rule was released on Sept. 18, 2013 with comments due Dec. 2, 2013. The SEC had targeted fall of 2014 for action on this regulatory initiative, which was pushed back until the rules were finalized on Aug. 18, 2015. The final rules require that CEO total annual compensation, as stated in the summary compensation table, be compared to the median total annual compensation of all the other employees of the company, both foreign and domestic. The impact of these final rules on CEO pay remains a matter of speculation. Nonetheless, CEO pay ratio disclosures will become a part of the corporate executive compensation disclosure package for fiscal year reports beginning on or after Jan. 1, 2017, which for many would be at their 2018 annual shareholders’ meeting.

The SEC released three anticipated rule proposals in 2015 that have yet to be adopted: pay-for-performance comparison (April 2015), hedging policy disclosures (February 2015) and compensation recoupment (a.k.a. clawback) policies (July 2015). The final rules for all of these 2015 proposals will likely impact corporate governance, the way companies and boards structure incentives, and overall executive pay mix in the future.

The pay-for-performance proposal would add a table to existing named executive officer (NEO) compensation disclosures, comparing the executive compensation actually paid to the company’s total shareholder return (TSR) performance and the TSR performance of a peer group over a five-year period. The heavy emphasis on TSR in this pay-for-performance disclosure proposal may further increase the prevalence and scope of this metric. However, the proposed pay-for-performance guidelines were approved by the SEC by a 3-to-2 margin along party lines, making uncertain if the outstanding proposed guidelines will ever be finalized. Despite this uncertainty, shareholder interest in executive compensation structures that pay for performance will not diminish.

The hedging policy proposal requires the disclosure of details for any corporate provisions that allow an employee or director to hedge or offset any decrease in the fair market value of company stock. This is not an outright prohibition, but it would inform investors of situations where hedging policies run counter to the general intent of performance-based incentives.

The clawback policy disclosure proposal would require stock exchanges to adopt written policies for the recovery of excess incentive-based compensation from current or former executive officers that were the result of a materially noncompliant financial statement. This would impact the policies of all the companies listed on U.S. stock exchanges.

The only remaining Dodd-Frank compensation issue not yet addressed by the SEC is the disclosure relating to why a company has chosen the chairman and CEO structure that they have, whether the position is combined or held by two separate individuals. The SEC currently does not anticipate providing guidance for this provision of the Act, possibly because this issue is already addressed to some degree in the CD&A.

The CEO pay ratio now joins provisions related to executive compensation that have already been implemented to date, which involve shareholder votes: Say On Pay (SOP), Say When On Pay, and Say On Golden Parachute. In 2011, the inaugural year for SOP and Say When On Pay, just 44 companies (1.4% of companies with SOP proposals) failed to receive majority shareholder support. In the following year, the percent of failures increased to 2.6%, and remained above 2.4% in each succeeding year through 2015. In 2016, for the first time since the inaugural year, the failure percentage dropped below 2% (1.6%).

An analysis by Institutional Shareholder Services (“ISS”) indicates approximately three-quarters of the failed votes are due to pay-for-performance issues. Indeed, the leading factors causing SOP failures continue to be the pay-for-performance relationship, the rigor of performance goals, and problematic pay practices (“ISS Voting Analytics”).

With SOP now entrenched in the psyche of compensation committees along with evolving ISS standards, improving disclosure of measures used, the values associated with those measures, and how they can be expected to drive performance should continue to be a priority for all public companies. The SEC requires company proxy statements to disclose the specifics of their executive compensation policies in clear language for investors. This requirement has developed from the assertion by the SEC that if executive compensation performance targets are central to a company’s decision-making process, these targets must be disclosed to investors. ISS is also explicit in the need for “robustness of disclosure,” as this is a component of their qualitative assessment of SOP proposals.

ISS bases its SOP recommendation on three separate quantitative tests and a thorough qualitative review of various factors relating to performance-based pay, such as the ratio of performance-based compensation to total compensation, the ratio of performance-based equity to time-based equity, financial and operational performance, realizable pay, and the completeness of disclosure and rigor of performance goals. Beginning with meetings on or after Feb. 1, 2017, the qualitative assessment will also include a review of the company’s performance relative to other financial metrics besides TSR for the same peer group used in the quantitative screens.

It seems clear that companies will be under constant pressure to include in their proxy statements complete pay-for-performance disclosures such as minimum, target, and maximum performance goals and corresponding payout levels. The SEC rules require that all performance measures and goals be released and compared with actual results for both short- and long-term incentive plans.

This study provides a behind-the-scenes look at how incentives are being structured to connect pay and performance. Because incentive compensation comprises the bulk of executive pay packages at publicly traded companies, boards of directors and senior management are continually searching for the right performance measures to balance rewards with financial, stock price and operational performance as well as non-financial and individual performance.

Once companies get beyond the difficulties of designing executive programs that adequately balance pay versus performance, they then have the added pressure of clearly explaining their pay-for-performance formula to investors.

There are four broad issues for publicly traded companies relating to performance-based compensation:

- Selection of short- and long-term performance measures that have been approved by shareholders (i.e., contained in incentive and equity plans);

- Adequate disclosure of performance goals (measures and levels) in the proxy filing;

- Review of the risk associated with performance plans and appropriate proxy disclosure; and

- Clawback of incentive payouts if financial statements have been restated, causing the performance goals to not be met (included in Dodd-Frank, proposed regulations issued but final rules pending).

Outside advisors, lawyers and consultants play a substantial role in the process of setting and describing performance measures and goals because designing the appropriate compensation package for senior executives is a difficult process. The unique environment of the company and the individual needs of executives must be considered as compensation programs are designed. In addition to these considerations, public scrutiny of executive pay decisions and practices complicates the overall process of setting executive pay.

Most public companies have redesigned their incentive programs over the last several years to ensure there is a link between performance achievement for the company and executive, and performance achievement for shareholders. Indeed, we continue to see increases in the use of performance-vested grants as a means for more closely linking pay to performance. A disconnect stemming from faulty incentive design could expose an executive and the board of directors to unwelcome scrutiny from shareholders and the general public. Additionally, the risk of a negative SOP recommendation and vote can lead to increased costs in responding to a failed SOP vote.

In order to investigate what (and how much) is being shared in annual proxy statements about executive pay packages and how incentive pay is designed, Arthur J. Gallagher & Co.’s Human Resources & Compensation Consulting Practice has conducted a study of the 2016 annual proxy statement disclosures for 200 of the top U.S. companies (based on revenue and market capitalization). This is the eighth consecutive year this in-depth analysis has been conducted for the top 200 public companies. A list of the companies studied is included in Appendix 1 of the complete publication (available here). The sector mix was led by capital goods companies. Industry details are shown in Appendix 2 of the complete publication (available here).

Executive Compensation Overview

There are five elements to executive compensation:

- Base salary, including cost of living, merit and promotional increases;

- Short-term incentives (also referred to as annual bonuses), which measure performance over a period of one year or less and are almost always paid in cash;

- Long-term incentives, which are typically denominated in shares of stock and reward performance for a period of time greater than one year;

- Benefits and perquisites, including basic benefits, supplemental executive retirement plans (SERPs), retirement, personal use of aircraft, financial counseling and other excess benefit plans; and

- Severance, including severance with or without a change in control, death, disability, or other.

There are multiple factors that impact the alignment of pay and performance, and are crucial to the overall executive program design:

- Performance measures;

- Pay-for-performance formula (minimum, target, and maximum levels for performance goals and payout levels);

- Long-term incentive pay mix; and

- Severance pay [1]

Overview of Study

Objectives

The objectives of this research study were:

- To identify the primary characteristics of short- and long-term incentive plan designs;

- To identify trends in long-term incentive programs, including stock options, time-based restricted stock, and performance-based programs;

- To review target setting as compared with actual results; and

- To analyze the trends in plan design disclosure over time.

Data

The data used for this study was collected from SEC filings (in most cases from proxy statements) based on information provided in the CD&A and related tables. The data was disclosed by companies in a variety of ways, including tables, descriptive text and footnotes.

Procedures

The pay-for-performance formula characteristics examined in this study include:

- Performance measures (types of measures and weightings);

- Performance levels (at threshold, target and maximum); and

- Payout levels (at threshold, target and maximum).

For the purposes of providing comparable analysis given the variability of reporting and data, judgments were made as to the best ways to combine data. The data was carefully reviewed for completeness and accuracy. Proxies that were reviewed were filed through September 2016 with fiscal years ending in 2015 or early 2016 (May 2016 was the fiscal year-end cutoff).

Incentives Design Overview

Performance Measures Overview

Performance can be measured against a fixed goal (such as an earnings target) or a relative goal (as compared against a peer group of companies or industry index). Long-term incentive plans (LTIPs) often use relative measures that can be disclosed without revealing strategically important information. Companies using measures expressed as levels or percent changes might not always disclose the goal values, claiming disclosure could cause competitive harm.

Performance measures can be segregated into two main categories: market-based (stock price or TSR) and financial-based (earnings per share, return on assets, etc.). Some refer to these performance classes as “external” and “internal.”

Ideally, a balanced incentive program (including short- and long-term incentives) should include financial goals and stock-appreciation goals as well as absolute goals and relative goals. Thus, if the company does well against its business plan but underperforms its industry, the incentive payout will fairly reflect overall performance. On the flip side, if a company does not hit its internal goals but outperforms its peers and/or the broader stock market, then some level of payout may be warranted.

This past year, interesting design features were noted. A large oil company implemented a bonus payout cap of 100% of target if the company experiences either negative earnings or negative TSR. A similar cap can also be found in several performance equity designs where performance equity payouts are capped at target if TSR is negative. A version of this was seen at a major industrial company, whereby if absolute TSR performance is negative, payout at target would be the maximum regardless of performance compared to performance targets. In addition, if the absolute TSR performance is positive, a minimum of 25% of target performance equity will vest. A large telecommunications company provides for discretion to reduce the payout up to 25% if TSR is negative over the performance period.

Pay-For-Performance Formula Overview

Investors are generally aware of executive compensation issues and are interested to see if pay corresponds with performance. Indeed, with SOP voting an annual event for most companies, pay-for-performance has become a core issue for investors and a priority measurement item for proxy advisory firms such as ISS, Glass Lewis and others. As a result, companies are more focused than ever on ensuring that shareholders agree with their strategies by more clearly communicating their goals.

Performance-based compensation is used by almost all companies to balance executive pay with corporate and individual performance. A fair balance can be struck between the goals of shareholders and senior management under the oversight of the board of directors, but it is not a simple task. The selection of performance measures and corresponding performance levels can be one of the most difficult aspects of designing an incentive compensation program.

Goals should be reasonable and aligned with the business plan and investor communications. In addition, the threshold payout for an incentive plan should be adjusted to be fair to both executives and shareholders. Likewise, the maximum performance and payout level should be set appropriately to encourage stretch levels of performance without providing a windfall payout.

Disclosure Overview

Because the relationship between pay and performance is often complex, communicating the purpose and design details of the executive performance program is challenging. However, despite changing disclosure expectations and interpretations, the interest in pay-for-performance continues to grow and is expected to be standardized as proposed by the SEC. Specifically, the proposed amendments to Item 402 of Regulation S-K to implement Section 14(i) of the Securities Exchange Act of 1934 (the “Exchange Act”), as added by Section 953(a) of the Dodd-Frank act. Section 14(i) directs the Commission to adopt rules requiring registrants to disclose in a clear manner the relationship between executive compensation actually paid and the financial performance of the registrant. Under the rules proposed in April 2015, companies would need to disclose five years of annual compensation paid to the CEO and the average annual compensation paid to the other named executive officers relative to total shareholder return. In addition, companies would be required to show the relationship between company TSR and the TSR of the company’s peer group. This would represent a completely new disclosure for most companies as just 12% of the Top 200 companies provide some type of pay versus TSR performance disclosure.

Study Highlights

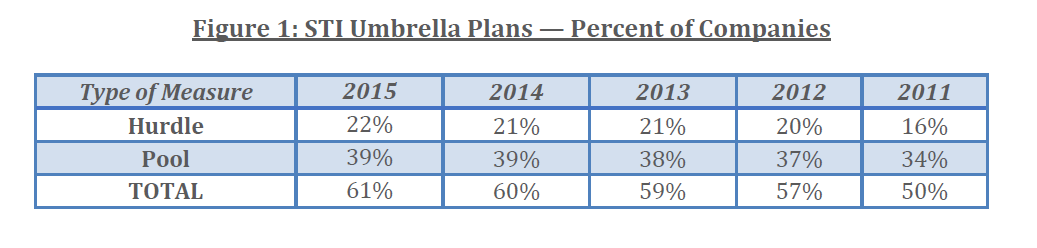

Umbrella Plans

Of the 200 companies reviewed last year, 61% of companies with short-term incentive plans (“STIPs”) indicated the use of “umbrella” STIP plans (also referred to as “inside/outside” plans or “plan within a plan”), which along with prior-year results, were the highest in the past five years. Companies with these types of plans often disclose fewer performance metrics than companies without these plans, in part due to the inclusion of more qualitative rather than quantitative measures. Similar to other performance-based programs, umbrella plans must follow specific guidelines in order to qualify as performance-based compensation that is in compliance with Internal Revenue Code 162(m), and thus tax deductible.

Two somewhat different plan designs are evident. The plan design found most often involves creating a bonus pool, usually based on a percentage of an income measure (“outside plan”). Sixty-four percent (64%) of umbrella plans use this approach. Each executive covered under this plan is allocated a percentage of the pool, which represents the maximum allowable payout to each person. Actual payouts are based on an “inside plan” which often includes a combination of financial/formulaic performance measures with corresponding threshold, target and maximum levels, and qualitative individual or discretionary goals.

Because the outside plan is based on a financial measure that is approved by shareholders and meets the other 162(m) requirements, these individual/discretionary amounts are considered performance-based and therefore are tax deductible.

To qualify for 162(m) deductibility, an executive’s payment must be below the disclosed maximum amount, and the sum of payments to all executives must be less than or equal to the pool amount. Additionally, a reduction in one executive’s payment cannot result in an increase to another executive’s payment. Once the pool and individual amounts have been established, only negative discretion can be used to adjust the payout amounts.

The second plan type used by 36% of companies with umbrella plans involves establishing a financial hurdle or hurdles which must be achieved before bonus payments can be made. These hurdles are designed to cover the amounts necessary to pay bonuses to the top executives. The actual bonus pool is usually a multiple of salaries of those executives participating in the plan. As described above, performance and individual goals can be created for determining the actual payment amounts. Because there is an overarching financial hurdle or threshold and payment limits established for the executives, this type of plan would qualify for 162(m) tax deductibility.

Individual Objectives in STIPs and Use of Discretion

Many companies use individual performance measures in their STIPs. Of the 198 companies with some form of a short-term incentive, including companies with umbrella plans, 27% included individual, specific objectives for one or more NEOs. Twenty-four percent (24%) of CEOs had individual objectives. When considering non-umbrella companies, 23% use individual objectives as part of the overall performance assessment. Individual objectives can be based on a combination of financial and non-financial measures.

Of the executives that had individual objectives in 2015 (56% of CEOs and 57% of other NEOs) had a separate weighting for individual objectives ranging from 10% to 50%. In other cases, the final award was based on an adjustment to a calculated, formulaic amount using discretion, or a predetermined plus and minus range.

Discretion, excluding negative discretion related to umbrella plans, was used at 64% of companies with STIPs in 2015 to determine at least a portion of the bonuses paid to executives. This was an increase from 61% in 2014 but similar to 63% in 2013.

Discretion can reflect individual performance or overall company performance relative to the industry, can recognize special contributions, or be based on other factors that the CEO or compensation committee deem valuable to the company. The use of discretion is not related to the use of individual objectives, although these practices can overlap.

Realizable and Realized Pay Analysis

Several years ago much had been written and discussed on this topic. Many compensation consultants have argued that this is a more appropriate measure for comparing executive pay with performance than using the target or grant date value. ISS has given a nod to this point of view by including a realizable pay analysis as part of a company’s qualitative review. Indeed, when this version of pay-for-performance was promoted by executive compensation consulting firms, a number of leading corporations began including a realizable pay analysis in their proxy statements. However, based on this top 200 review, this type of disclosure has not gained much traction.

Of the 200 companies reviewed, just 16 companies (8%) included a realizable pay versus performance analysis, the same number of companies in 2014. This is down from 20 companies in 2013. And because t a new pay-for performance disclosure required by the SEC is expected to be effective in 2018, declines in realized pay disclosures are expected to continue.

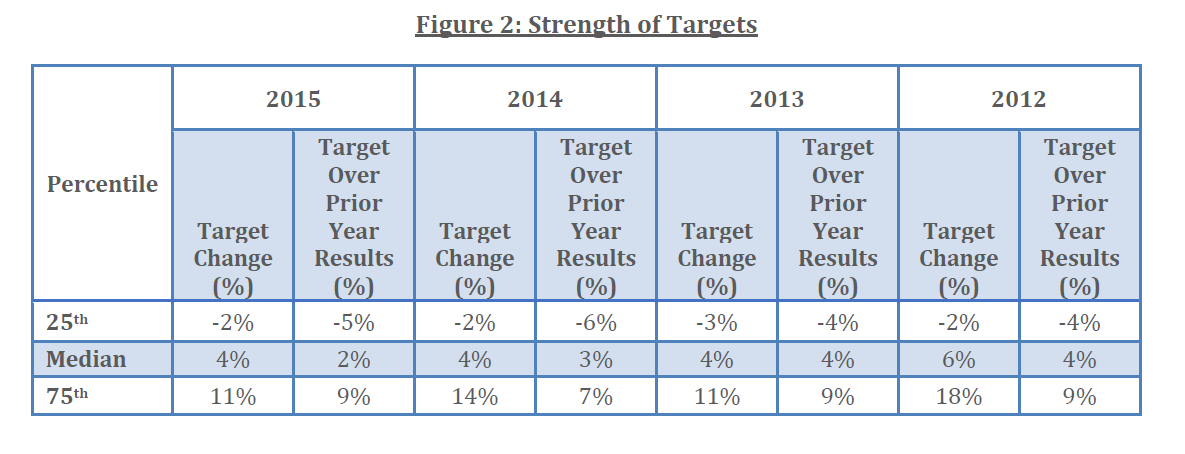

Setting STIP Targets

The median year-over-year increase in target goals (target over prior-year target) for 2015 was again 4%, matching 2013 and 2014. Thirty-seven percent (37%) of target performance goals were set at levels that were lower than the prior-year actual results and 31% of goals were below the prior year target value.

The difference between the 25th percentile to 75th percentile target change remains quite narrow, with a difference of 13 percentage points (-2% to 11%) in 2015, down from 20 points in 2012 (see Figure 2).

Pay-For-Performance

An examination of 2015 short-term incentive payouts relative to target indicates there was an increase in the percentage of NEOs that were paid above target. Among companies that reported short-term incentive payouts in 2015, 62% of NEOs were paid at or above target levels as compared with 63% in 2014, 60% in 2013, and 62% in 2012.

Of the companies that disclosed long-term incentive performance and payout information, the percentage that were paid at or above target was 61% in 2015, up slightly from 60% in 2014, 57% in 2013 and 52% in 2012.

Also reviewed was how STIP target levels are set relative to the prior-year target to see if decreasing the target value resulted in companies more able to exceed target. Companies with reduced targets from the prior year achieved above-target performance for a given measure at a lower rate as compared to companies that increased performance targets (57% vs. 62%). In 2014 the results were reversed (63% vs. 58%).

Here are additional findings of note. Sixty-one companies, or 31% of all companies with STI plans, included one or more measures with a lower target than the previous year. Excluding discretionary plans, some of which include measures with targets but no weights, the percentage increases to 36%. Finally, when looking at all disclosed STI measures, 64% had target values greater than prior-year target values, while 63% of targets were set above prior-year actual results. Five percent of target values did not change from the prior year.

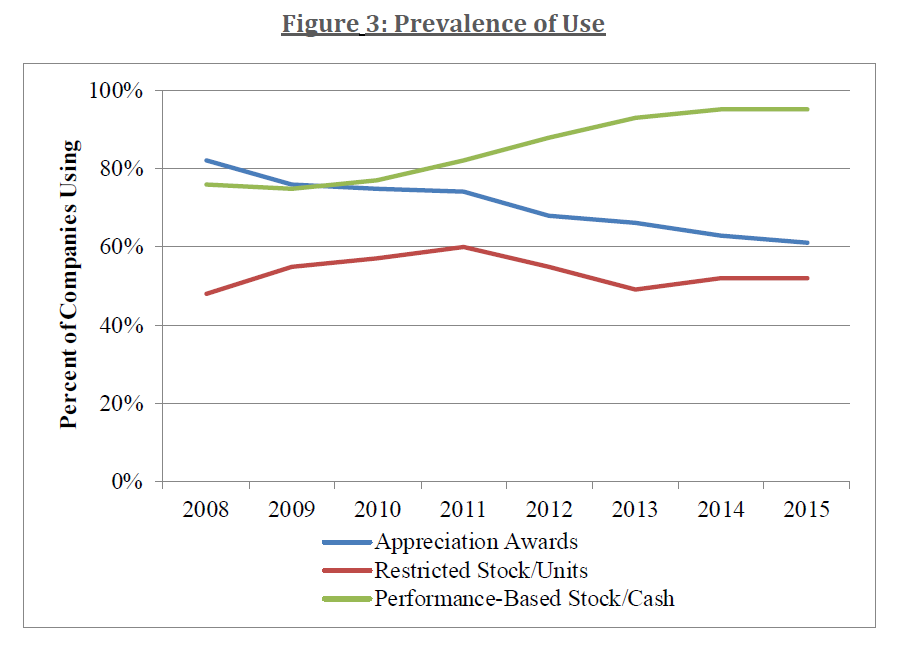

Stock Option Grants Receding

Continuing in 2015 and for the seventh consecutive year was the shift away from appreciation awards (stock options/stock appreciation rights (“SARs”)) and towards performance awards that are earned based on achieving performance goals. Also, for the sixth consecutive year, the prevalence of grants of performance-based awards exceeded the prevalence of time-based appreciation awards, and the gap continues to grow. Since 2009 when the prevalence was about even, performance-based awards have increased to nearly 30 percentage points higher than stock options/SARs (95% vs. 61%). Nonetheless, appreciation awards are still more prevalent than time-based restricted stock, even though the gap has narrowed over time as time-vested share grants have declined moderately. For example, in 2008, the difference in prevalence was 34 percentage points (82% vs. 48%), but in 2015 the difference was just 9 points (61% vs. 52%).

The collective use of performance-based awards (which includes performance shares/units, performance-based restricted stock, performance stock options, premium stock options, and long-term cash plans) totaled 95% in 2014 and 2015, up from 93% in 2013, 88% in 2012, 82% in 2011 and 77% in 2010. On the flip side, the prevalence of stock option/SAR grants, in total, has declined steadily from 82% in 2008 to 61% in 2015.

The steep shift from appreciation awards to performance awards can be attributed to the impact of SOP and the influence of ISS, particularly their classification of time-based stock options as non-performance-based grants. See Figure 3 for further details.

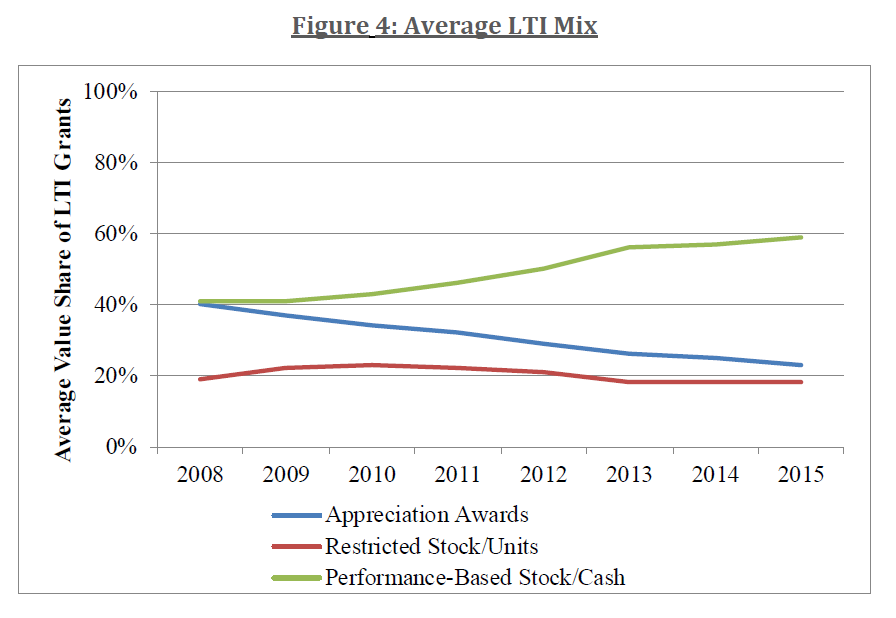

In addition to the decrease in prevalence of appreciation awards, the value provided in the form of stock options/SARs is also declining. In 2008, an average of 40% of the total LTI value was provided in the form of appreciation awards, 41% in performance-based awards, and 19% in time-based restricted stock/units.

By 2015, the average of Top 200 performance-based awards had increased to 59% of the total LTI value with a corresponding decrease in stock options/SARs (with time-based restricted stock/units remaining relatively flat). See Figure 4.

Detailed Observations

Performance Measures Used in Incentive Plans

Short-Term Incentive Plans

Findings include the following:

- Earnings per share (EPS) was the most common single measure used by the companies in the study that disclosed their performance measures. Thirty-eight percent (38%) of companies with non-discretionary STIPs used EPS in 2015, which is slightly lower than last year (40%).

- Ninety percent (90%) of companies disclosing specific measures and metrics used at least one type of income-based measure in 2015, which is lower than last year (93%). This category includes EPS, net income, operating income, EBITDA, etc.

- Other common measures used in 2015 included revenue (42%), cash flow (33%), and capital efficiency ratios (21%, which was slightly lower than last year’s 24%).

- Total shareholder return (TSR), the most commonly used measure in an LTIP, is not often used in a STIP. Only 2% of companies with STIPs used TSR in 2014 or 2015 as one of their performance measures.

- For companies disclosing measures, the use of non-financial measures (such as customer satisfaction, production goals, and new-business market share) were disclosed at 50% of companies, relatively consistent with previous years.

- Thirty-eight percent (38%) of companies with STIPs and LTIPs used one or more of the same measures in both incentive programs, which is slightly more than 37% in 2014.

- Median performance over target was 1.4% as compared with 7.0% in

- Median payout was 10.8% over target as compared with 21.5% in 2014.

The complete publication, including Appendix, is available here.

Endnotes

1For more information, refer to our 2015 article entitled “Executive Severance Arrangements: How and Why They are Changing,” https://www.ajg.com/media/1697729/executive-severance-arrangements-how-and-why-they-are-changing.pdf(go back)