Print

PrintRupal Patel and David Ellis are partners at EY. This post is based on an EY publication by Ms. Patel and Mr. Ellis. Related research from the Program on Corporate Governance about CEO pay includes Paying for Long-Term Performance (discussed on the Forum here) and the book Pay without Performance: The Unfulfilled Promise of Executive Compensation, both by Lucian Bebchuk and Jesse Fried.

In recent months executive pay has received an unprecedented level of attention from a wide range of stakeholders. While Remuneration Committees, executives and investors in many businesses may feel that current pay structures are working well and fit for purpose, the intensity of noise we are experiencing tells us that it is no longer reasonable for any organisation to assume that there is nothing it needs to be concerned about.

First indications from the 2017 AGM season show that in many cases the noise in the system is now turning into real opposition. Many would seek to explain away this opposition as being specific to a business, or focussed on a discrete issue. We at EY believe that this is now wishful thinking.

Much of the noise in the system derives from the view held by some that executive pay is simply too high. A suggested solution is to regulate pay by imposing a cap on the amount an individual may receive. Whilst capping executive pay would be relatively straightforward to execute, we believe that it will not fix the root problem and could create considerable complexity in itself.

That is not to say that change in the executive pay arena would not be welcome. There is work to be done in several areas including governance, communication and alignment of interest. However, one aspect on which stakeholders appear to be agreed is the need for the simplification of executive pay.

EY’s view is that this simplification agenda cannot be addressed by tweaking aspects of the traditional package. This is not about the number of performance measures used or the length of deferral applied. It is about acknowledging that a desire for simplification requires agreement on what is core to an executive pay strategy and to focus on that exclusively.

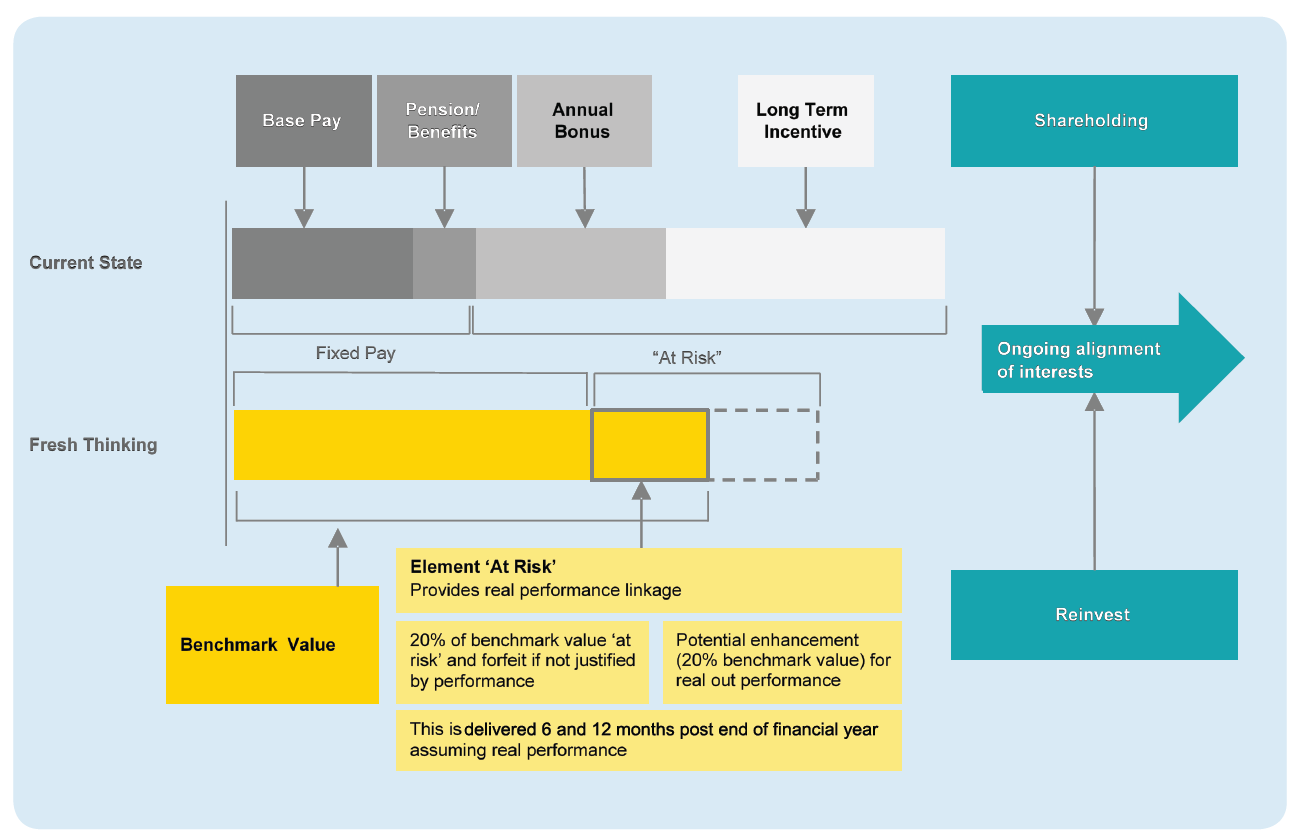

EY feels that many aspects of the today’s pay structures, which have been viewed as integral to the traditional model, may not be the most efficient way to deliver remuneration or may simply be no longer relevant.

Whilst there are any number of alternative structures and possible approaches to improve the status quo, EY believe the current challenges cannot be addressed by existing remuneration models. Accordingly we have designed a new model, the One Element Pay Model.

Under such a model, companies:

- Pay executives for the work they do.

- Pay them a bit more if they generate better than expected outcomes.

- Pay them a bit less if they undershoot expectations.

- Require that they buy shares every year with a meaningful portion of their remuneration.

EY believe the One Element Pay Model for executives can offer advantages not only to businesses of many shapes and sizes, but also the diverse group of stakeholders in the executive pay debate.