Print

PrintLia Der Marderosian, Brian Johnson, Erika Robinson, and David Westenberg are partners at Wilmer Cutler Pickering Hale and Dorr LLP. This post is based on a WilmerHale publication.

US Market Review and Outlook

Review

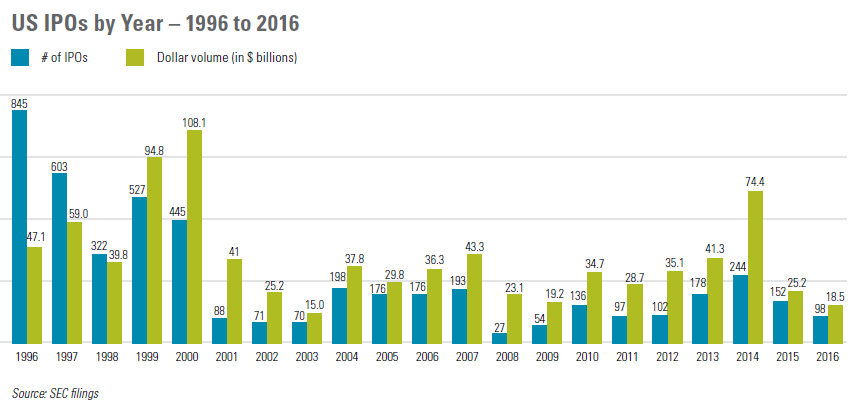

The IPO market produced 98 IPOs in 2016, the second down year in row, coming in 36% below the tally of 152 IPOs in 2015. In the 12-year period preceding 2015, which saw an annual average of 138 IPOs, there were only three years in which IPO totals failed to reach the 100-IPO threshold.

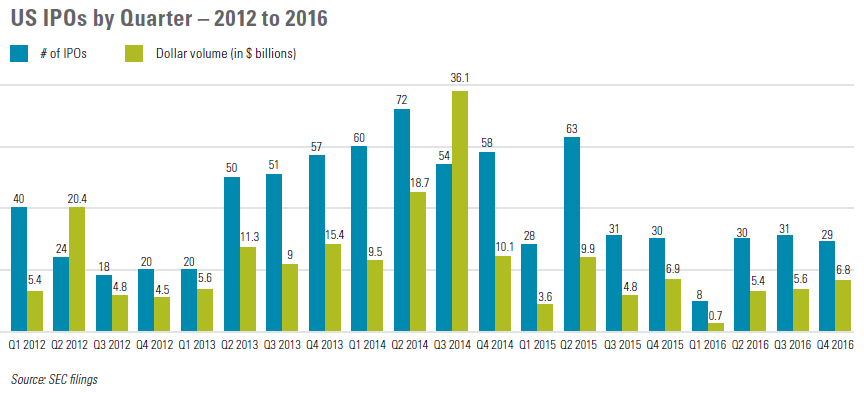

The year started slowly, with the first quarter producing only eight IPOs, but the pace of new offerings subsequently improved and steadied, with the succeeding three quarters producing 30, 31 and 29 IPOs, respectively. The quarterly average of 31 IPOs that has prevailed over the past two years is less than two-thirds the quarterly average of 53 IPOs produced during 2013 and 2014.

Gross proceeds in 2016 were $18.54 billion, 66% below the $25.17 billion raised in 2015 and the lowest annual tally since the $15.05 billion raised in 2003. Average annual gross proceeds for the 12-year period preceding 2016 were $35.73 billion—93% higher than the corresponding figure for 2016. IPOs by emerging growth companies (EGCs) accounted for 84% of the year’s IPOs, down from 93% in 2015. Since the enactment of the JOBS Act in 2012, 85% of all IPOs have been by EGCs.

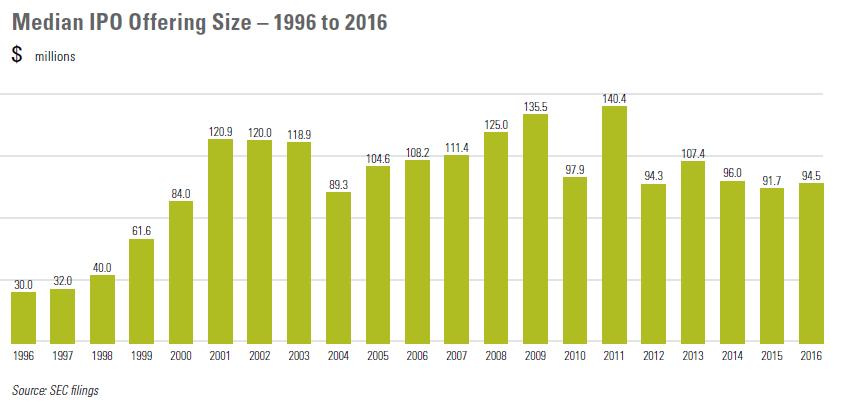

The median offering size for all 2016 IPOs was $94.5 million, or 3% above the $91.7 million figure for all 2015 IPOs, but 6% lower than the $101.0 million median for the five-year period preceding 2015.

The median offering size for life sciences IPOs in 2016 was $55.5 million, or 23% below the $71.8 million figure for life sciences IPOs in 2015 and 11% below the $62.4 million median size for life sciences IPOs in the five-year period preceding 2015. By contrast, the median offering size for non-life sciences IPOs in 2016 was $131.6 million—up 2% from the $128.5 million median in 2015 and up 3% from the $128.1 million median for the five-year period preceding 2015.

In 2016, the median offering size for IPOs by EGCs was $77.5 million, compared to $368.6 million for IPOs by non-EGCs—both tallies representing the lowest annual levels since 2012. From 2012 to 2015, the median EGC IPO offering size was $87.0 million, compared to $425.5 million for non-EGC IPOs.

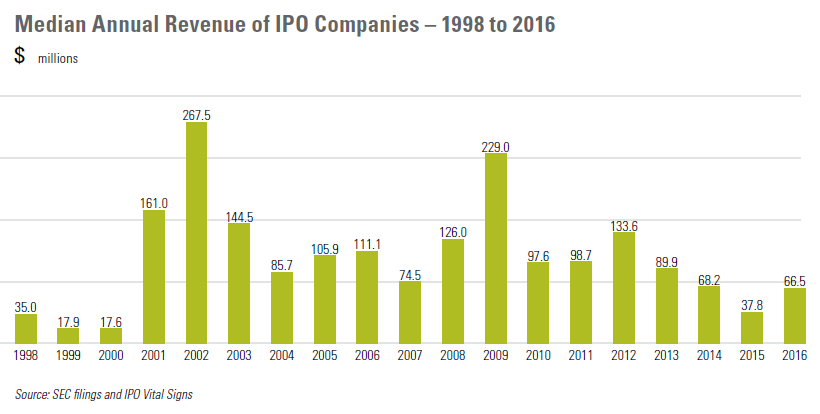

The median annual revenue of all IPO companies in 2016 was $66.5 million, or 76% above the $37.8 million median figure for 2015, but well below the $92.7 million median figure for the five-year period from 2010 through 2014. The median life sciences IPO company in 2016 had annual revenue of $2.3 million, compared to $205.8 million for all other IPO companies.

EGC IPO companies in 2016 had median annual revenue of $39.2 million, compared to $1.54 billion for non-EGC IPO companies. The median annual revenue for non-life sciences EGC IPO companies in 2016 was $113.8 million, 5% above the $108.2 median that prevailed from the enactment of the JOBS Act through 2015.

The percentage of profitable IPO companies increased to 36% in 2016 from 30% in 2015. Only four life sciences IPO companies in 2016, or 10% of the total, were profitable, matching the percentage over the five-year period preceding 2016. In 2016, 53% of non-life sciences IPO companies were profitable, down slightly from 55% for the five-year period preceding 2016.

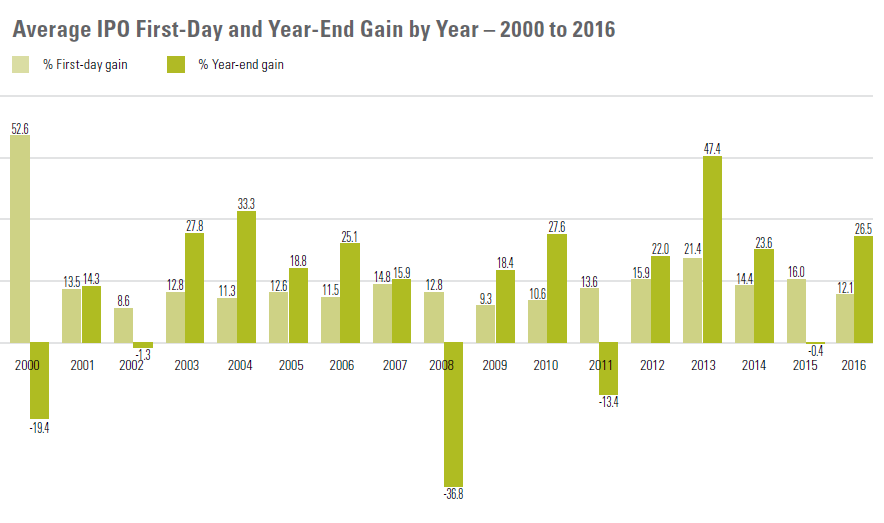

In 2016, the average IPO produced a first-day gain of 12%, compared to 16% for the average IPO in 2015. The 2016 figure is the lowest since 2010. The average life sciences IPO company gained 6% in first-day trading in 2016, compared to 16% for the year’s non-life sciences IPO companies. This represents a reversal from 2015, when the average life sciences company rose 18% on its first trading day—3% higher than the gain achieved by non-life sciences IPO companies. There was a solitary “moonshot” (an IPO that doubles in price on its opening day) in 2016—down from an annual average of six moonshots between 2013 and 2015.

In 2016, 24% of IPOs were “broken” (IPOs whose stock closes below the offering price on their first day). This figure is down from 26% in 2015. Life sciences company IPOs were twice as likely as other IPOs to be broken in 2016, with 35% of life sciences company IPOs closing first-day trading at a loss, compared to 17% of non-life sciences company IPOs.

At year-end, the average 2016 life sciences IPO company was trading 16% above its offering price and the average non-life sciences IPO company was trading 34% above its offering price. Overall, the average 2016 IPO company ended the year 26% above its offering price. The year’s best performers were a pair of tech companies, Acacia Communications (trading 168% above its offering price at year-end) and Impinj (up 152%), followed by life sciences companies Novan (up 146%) and AveXis (up 139%).

At the end of 2016, 30% of the year’s IPO companies were trading below their offering price—life sciences companies faring worse than their non-life sciences counterparts, with a figure of 45%, compared to 19% for non-life sciences IPO companies—while 44% of all 2016 IPOs were trading at least 25% above their offering price.

Individual components of the IPO market fared as follows in 2016:

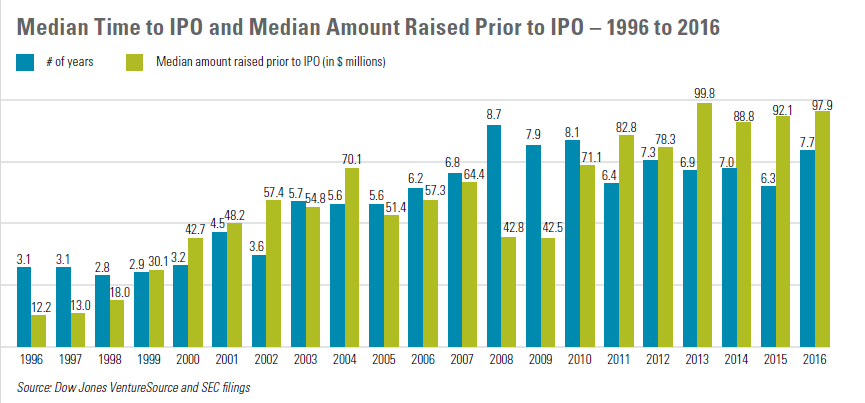

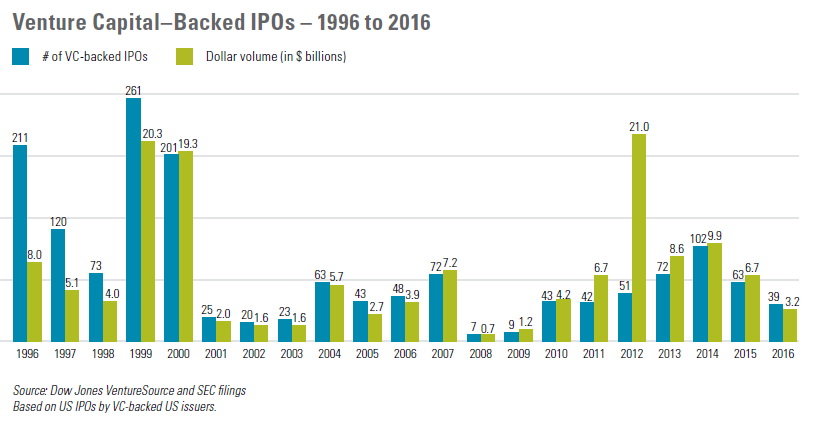

- VC-Backed IPOs: The number of IPOs by venture capital-backed US issuers declined 38%, from 63 in 2015 to 39 in 2016, but VC-backed IPOs still accounted for 50% of all US-issuer IPOs in 2016. The median offering size for US venturebacked IPOs declined 4%, from $77.9 million in 2015 to $75.0 million in 2016. The median deal size for non-VC-backed companies was $147.0 million in 2016, up 30% from $113.3 million in 2015. The average 2016 US-issuer VC-backed IPO gained 30% from its offering price through year-end. The median amount of time from initial funding to an IPO increased from 6.3 years in 2015 to 7.7 years in 2016—the highest annual level since 2010—while the median amount raised prior to an IPO, at $97.9 million, was the second-highest figure since 1996.

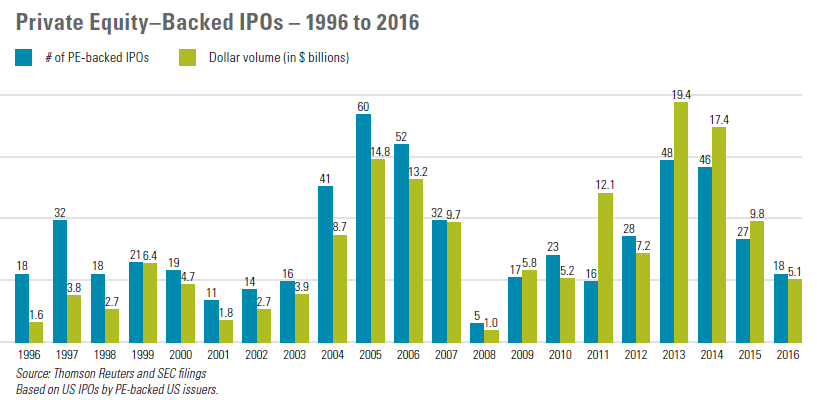

- PE-Backed IPOs: Private equity-backed IPOs by US issuers declined by one-third, from 27 in 2015 to 18 in 2016, accounting for 23% of all US-issuer IPOs in each year. The median deal size for PE-backed IPOs in 2015 was $250.0 million—more than triple the $75.0 million figure for all other IPOs. The average PE-backed IPO in 2015 gained 34% from its offering price through year-end.

- Life Sciences IPOs: There were 40 life sciences company IPOs in 2016, compared to 72 in 2015 and 98 in 2014. Although the portion of the IPO market accounted for by life sciences companies declined to 41% from 47% in 2015, this market share compares favorably to the 40% figure in 2014 and is well above the 17% figure for the five-year period preceding 2014. The average life sciences IPO company in 2016 ended the year up 16% from its offering price, compared to a 34% year-end gain for non-life sciences IPO companies.

- Tech IPOs: Deal flow in the technology sector declined by 29%, from 35 IPOs in 2015 to 25 IPOs in 2016—the lowest annual number since 2009—but the sector’s share of the US IPO market increased from 23% to 26%. The 2015 figure was a low point for the sector, reached after five consecutive years of decline from the 46% US market share achieved in 2011. The average tech IPO ended the year with a gain of 37% from its offering price, compared to 23% for non-tech IPOs.

- Foreign-Issuer IPOs: The number of US IPOs by foreign issuers declined by 43%, from 35 in 2015 (23% of the market) to 20 in 2016 (20% of the market). Among foreign issuers, Chinese companies led the year with six IPOs, followed by Bermuda companies (three IPOs) and companies from Switzerland and the Netherlands (each with a pair of IPOs). The average foreign issuer IPO company ended the year trading 12% above its offering price.

In 2016, 40 companies based in the eastern United States (east of the Mississippi River) completed IPOs, compared to 38 for western US-based issuers. California led the state rankings with 19 IPOs, followed by Massachusetts (with 12 IPOs), Texas (with six IPOs) and Georgia and Illinois (each with five IPOs).

Outlook

IPO market activity in the coming year will depend on a number of factors, including the following:

- Economic Growth: The US economy lost momentum over the last three months of 2016 and the year ended with an annual growth rate of 1.6%—its weakest performance in five years. After raising its benchmark interest rate only once in the preceding decade, the Federal Reserve increased the rate in December 2016 and again in March 2017, and further rate hikes are widely expected in the coming year. These factors—together with uncertainty regarding the specific terms and timing of the Trump Administration’s tax and economic programs, the bumpy slowdown in China’s economic growth, the unknown outcome of Brexit, and political uncertainty in the Eurozone—all contribute to a hazy economic outlook in early 2017.

- Capital Market Conditions: Following mixed results in 2015, the major US stock indices posted solid gains in 2016, with the Dow Jones Industrial Average up 14% and the S&P 500 and Nasdaq Composite Index each up 9%. Seemingly enthused by the pro-business orientation of the new administration, the major indices rose further, to record levels, in the first quarter of 2017, although the capital markets could begin to cool if economic growth weakens. Sustained strength in capital market conditions would likely contribute to increased IPO activity but, by itself, may be insufficient to restore IPO deal flow to the levels seen from 2013 to 2015.

- Venture Capital Pipeline: Despite the decline in US venture-backed IPOs for the second consecutive year, the pool of VC-backed IPO candidates remains large and vibrant, including approximately 150 “unicorns” (private tech companies valued at $1 billion or more). While access to plentiful private financing at attractive valuations tends to encourage VC-backed companies to delay their IPOs, investors at some point will seek cash returns as opposed to paper gains. The solid aftermarket performance of VC-backed IPOs in 2016 is likely to generate demand for additional IPOs in 2017.

- Private Equity Impact: Having increased their fundraising for the fourth consecutive year, private equity firms are now sitting on record levels of committed capital. PE firms are eager to put their reserves to work, but the supply of capital is intensifying competition for quality deals and driving up prices. Despite increases in the level of equity invested in deals, which decreases investor returns, PE firms are facing pressure to exit investments—via IPOs or sales of portfolio companies—and return capital to investors.

- Impact of JOBS Act: Although it was intended to encourage EGCs to go public, the JOBS Act—combined with other regulatory and market changes—has made it easier for EGCs to stay private longer and has provided them with greater flexibility in timing their IPOs. The result has been a large and growing pool of qualified IPO candidates. The extent to which these companies decide to pursue IPOs, and the timing of these decisions, will have a substantial effect on the overall IPO market.

The IPO market has begun 2017 on a hopeful note, with 20 IPOs in the first quarter of the year—more than double the tally in the first quarter of 2016. In January, the impending AppDynamics IPO was poised to test investor appetite for IPOs by tech unicorns, until Cisco agreed at the last minute to acquire the company for $3.7 billion in cash. Snap’s very successful IPO in early March could jump-start the market and inspire other qualified companies to follow suit.

Some Facts About the IPO Market

Profile of Successful IPO Candidates

What does it really take to go public? There is no single profile of a successful IPO company, but in general the most attractive candidates have the following attributes:

- Outstanding Management: An investment truism is that investors invest in people, and this is even truer for companies going public. Every company going public needs experienced and talented management with high integrity, a vision for the future, lots of energy to withstand the rigors of the IPO process, and a proven ability to execute.

- Market Differentiation: IPO candidates need a superior technology, product or service in a large and growing market. Ideally, they are viewed as market leaders. Appropriate intellectual property protection is expected of technology companies, and in some sectors patents are de rigueur.

- Substantial Revenue: With some exceptions, substantial revenue is expected—at least $50 million to $75 million annually—in order to provide a platform for attractive levels of profitability and market capitalization.

- Revenue Growth: Consistent and strong revenue growth—25% or more annually—is usually needed, unless the company has other compelling features. The company should be able to anticipate continued and predictable expansion to avoid the market punishment that accompanies revenue and earnings surprises.

- Profitability: Strong IPO candidates generally have track records of earnings and a demonstrated ability to enhance margins over time.

- Market Capitalization: The company’s potential market capitalization should be at least $200 million to $250 million, in order to facilitate development of a liquid trading market. If a large portion of the company will be owned by insiders following the IPO, a larger market cap may be needed to provide ample float.

How Do You Compare?

Set forth below are selected metrics about the IPO market, based on combined data for all US IPOs from 2013 through 2016.

| Percentage of IPO companies qualifying as EGCs under JOBS Act |

86% |

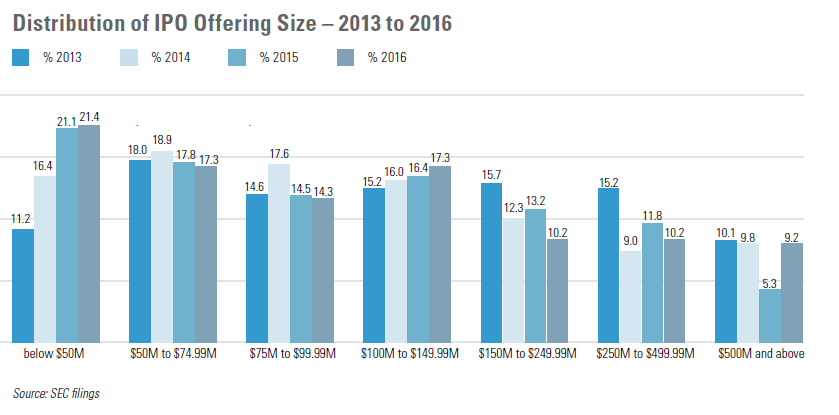

| Median offering size | $98.5 million (17% below $50 million and 9% above $500 million) |

| Median annual revenue of IPO companies | $64.5 million (45% below $50 million and 20% above $500 million) |

| Percentage of IPO companies that are profitable | 36% |

| State of incorporation of IPO companies | Delaware—94% No other state over 1% |

| Percentage of IPOs including selling stockholders, and median percentage of offering represented by those shares |

Percentage of IPOs—25% Median percentage of offering—32% |

| Percentage of IPOs including directed share programs, and median percentage of offering represented by those shares |

Percentage of IPOs—39% Median percentage of offering—5% |

| Percentage of IPO companies disclosing adoption of ESPP |

45% |

| Percentage of IPO companies using a “Big 4” accounting firm |

80% |

| Stock exchange on which the company’s common stock is listed |

Nasdaq—64% NYSE—36% |

| Median underwriting discount | 7% |

| Number of SEC comments contained in initial comment letter |

Median—31 25th percentile—24 75th percentile—42 |

| Median number of Form S-1 amendments (excluding exhibits-only amendments) filed before effectiveness |

Five |

| Time elapsed from initial confidential submission to initial public filing of Form S-1 (EGCs only) |

Median—67 calendar days 25th percentile—45 calendar days 75th percentile—109 calendar days |

| Time elapsed from initial confidential submission (if EGC) or initial public filing to effectiveness of the Form S-1 |

Median—118 calendar days 25th percentile—91 calendar days 75th percentile—175 calendar days |

| Median offering expenses | Legal—$1,500,000 Accounting—$850,000 Total—$3,200,000 |

Other factors can vary based on a company’s industry and size. For example, many life sciences companies will have much smaller revenue and not be profitable. More mature companies are likely to have greater revenue and market caps, but slower growth rates. Highgrowth companies are likely to be smaller, and usually have a shorter history of profitability.

Beyond these objective measures, IPO candidates need to be ready for public ownership in a range of other areas, including accounting preparation; corporate governance; financial and disclosure controls and procedures; external communications; legal and regulatory compliance; and a variety of corporate housekeeping tasks.

Change and Continuity in Securities Regulation

The election of Donald Trump as President and the continued Republican control of Congress raise questions as to what changes may be expected at the SEC and what may stay the same. President Trump has already nominated a new SEC chair—corporate lawyer Jay Clayton—and has two more commissioner openings to fill. Although President Trump has called for repeal of the Dodd-Frank Act, he has provided few specifics about possible changes to the federal securities laws and what role he expects the SEC to play. With the new Republican administration’s deregulatory focus and the House and Senate both under Republican control, there is the potential for significant changes in policy and direction to be implemented at the SEC.

Many key components of securities regulation, however, will likely remain unchanged. Despite concerns about various aspects of the SEC’s approach to regulation and enforcement, both Republicans and Democrats appear to recognize the importance of the SEC’s role in maintaining the preeminence and integrity of the US securities markets. Accordingly, challenges to the SEC’s core focus are unlikely to develop. In addition, although the leadership at the SEC is changing, most of the experienced professional staff at the SEC likely will remain in place, thereby providing some continuity in how the SEC carries out its mission.

Below, we explore possible changes in key areas of securities regulation, including within the SEC’s Division of Corporation Finance (which oversees the review of all IPO filings and disclosure obligations of all public companies), that may be coming under the new administration.

Mechanisms for Change

The Trump Administration could seek to implement changes in securities regulation by asking Congress, with or without SEC involvement, to amend or replace the relevant statutes; adopt legislation to change SEC rules or regulations; and/or decrease or redirect the SEC’s budget. In addition, the new administration could advocate that the SEC amend or repeal existing or pending SEC rules and regulations; issue interpretive guidance; and/or change enforcement and other staff priorities.

The processes for changing statutes and regulations are complicated and generally time-consuming. Set forth below is a summary of the potential methods for making changes to existing requirements at the SEC.

- Statutory Changes: Congress could adopt new legislation to amend and/ or replace existing statutes applicable to the SEC based on recommendations from the administration, from the SEC or on its own behalf. For example, the proposed CHOICE Act, which was introduced in the last Congress and passed by the House Financial Services Committee in September 2016, seeks to amend or repeal large portions of the Dodd-Frank Act. The adoption of new legislation would likely involve protracted and complicated negotiations both within the Republican Party and with Democrats, although it is always possible that some less controversial legislation could be adopted quickly.

- Changes to Existing SEC Rules:

- The SEC could vote to repeal or amend previously adopted rules and regulations. Such a repeal or amendment would ordinarily be subject to the notice and comment process, as well as cost-benefit analyses in certain cases, and likely would take months to implement. The SEC could invoke the “good cause” exception to notice and comment (reserved essentially for emergencies) to accomplish a rule change immediately. Nevertheless, the SEC would have to show a compelling reason to dispense with the public notice and comment period if challenged. It also may be possible for the SEC to propose repeal of a current rule and, at the same time, announce that it will not enforce the rule until the new rulemaking is complete. The SEC also could adopt rules on a temporary basis, while seeking comment (for example, an interim final rule suspending certain requirements). Similarly, for rules that have been adopted but have not yet taken effect, or whose compliance dates have not yet been reached, the SEC could extend effective dates to provide it time to conduct a notice and comment rulemaking. An indefinite suspension of a rule could raise legal issues under the Administrative Procedures Act and might be challenged in court.

- Congress also could repeal or amend any SEC regulation by adopting new legislation to make such a change. The process for adopting new legislation is the same as discussed above. In addition, subject to certain limitations, the Congressional Review Act establishes certain time periods during which Congress can review and disapprove a final rule. The new Congress has already acted on this basis to repeal several regulatory requirements, and is pursuing repeal of other regulations.

- Changes to SEC Guidance and Interpretations: The SEC may also issue guidance and interpretations, which are not subject to a notice and comment period as long as they do not amount to a “legislative rule”:

- In determining whether “guidance” or an “interpretation” voted on by the SEC is a legislative rule requiring notice and comment on the one hand, or a policy statement or interpretive rule not requiring notice and comment on the other, a court will look to the actual legal effect of SEC action and the SEC’s own characterization of its action. A court also will consider whether the SEC action creates a substantial regulatory change. Adoption of a binding norm will likely be classified as a legislative rule. A statement on how the SEC intends to enforce an existing legal norm will probably be regarded as a policy statement. A construction of an existing norm is likely to be classified as an interpretive rule. Therefore, as long as the SEC does not adopt new binding norms for a rule, issuing new guidance and interpretations could be done more expeditiously than changes to the rule itself.

- The CHOICE Act contains provisions that would prohibit the SEC from voting on any interpretation or guidance without conducting formal notice and comment. Given that the CHOICE Act originally was offered under a Democratic administration, however, a Republican administration may not reintroduce this provision, because Congress may not want to constrain the new leadership of the SEC. On the other hand, Congress and others tend to object to what they view as rulemaking through interpretation by an independent agency, so the approach in the CHOICE Act may reappear in new legislation.

- The SEC staff also could change the SEC’s direction through issuance of guidance on which the commissioners do not vote. Staff-issued guidance, such as “FAQs” often published regarding a new rule, would not amount to a legislative rule. In general, however, new leadership brought in by the new SEC chair would be unlikely to change course on matters of significance without at least seeking concurrence from the SEC chair. Moreover, certain Republicans have criticized “informal rulemaking” by the SEC staff through means such as enforcement decisions, no-action letters or accounting guidance, rather than statutorily mandated procedures, thereby raising the question as to whether such methods will continue to be utilized.

Division of Corporation Finance

In the wake of the election, there may be changes in the specific subject areas governed by, and the priorities of, the Division of Corporation Finance:

- Financial Reporting Regulations: The SEC has been engaged in efforts to improve and modernize financial reporting and has sought public comment on how to prioritize the information companies disclose to better serve investors. At the same time, the FAST Act directed the SEC to study Regulation S-K and issue a report to Congress containing, among other things, “specific and detailed recommendations on modernizing and simplifying [disclosure requirements] in a manner that reduces the costs and burdens on companies while still providing all material information.” The SEC issued the report on November 23, 2016, and is required to propose regulations to implement its recommendations within one year after issuance of the report. In light of the FAST Act, disclosure effectiveness and simplification efforts may well continue under the new SEC leadership, although the focus may shift more dramatically toward reducing regulatory burdens.

- Corporate Disclosure Rules: Certain enhanced corporate disclosure requirements for public companies that have been proposed or are under consideration at the SEC are likely to be reconsidered under new leadership:

- Pay Ratio Disclosure. In 2015, as required by the Dodd-Frank Act, the SEC adopted amendments to Item 402 of Regulation S-K to require public companies to disclose the median of the annual total compensation of all their employees (excluding the CEO), the annual total compensation of their CEO, and the ratio of the median of the annual total compensation of all employees to the annual total compensation of the CEO. The rule change becomes effective in 2017. This provision of the Dodd-Frank Act and the corresponding rule, which would be repealed by the CHOICE Act, are likely to be reconsidered by the Trump Administration. The SEC’s Acting Chairman Michael S. Piwowar has already announced—in early February—that he is seeking public comment on challenges that companies have experienced as they prepare for compliance with the rule, and has directed the staff to reconsider the implementation of the rule based on any comments submitted.

- Conflict Minerals Disclosure. In 2012, as directed by the Dodd-Frank Act, the SEC adopted rules requiring public companies to publicly disclose their use of conflict minerals that originated in the Democratic Republic of the Congo or an adjoining country. This disclosure rule is anticipated to receive new scrutiny with the change in the administration. In late January, Acting SEC Chairman Piwowar directed the staff to reconsider whether certain guidance on the conflict minerals rule is still appropriate and whether any additional relief would be appropriate. A similar rule regarding resource extraction was repealed under the Congressional Review Act in February 2017.

- Political Spending Disclosure. Certain Democrats and investor groups have urged the SEC to require public companies to disclose their political spending. Such a rule, which already was not an SEC priority, is highly unlikely to be proposed or adopted in the new political environment.

- Focus on Smaller Companies: Certain Republicans have been strong proponents of amending the SEC regulatory regime to take into consideration the needs of smaller companies, including tailoring market structure requirements and disclosure rules to make the requirements more user friendly for smaller companies. Similarly, the CHOICE Act includes provisions intended to assist smaller companies, including an increase in the thresholds for requiring audits of internal control over financial reporting. Going forward, it is likely that the SEC, under new leadership, will place more emphasis on reducing compliance costs and increasing access to capital for smaller companies.

- Executive Compensation: The three remaining corporate finance governance and compensation-related rulemaking mandates from the Dodd-Frank Act that have been proposed but not adopted by the SEC relate to: pay-for-performance (requiring disclosure regarding the relationship between executive compensation and total shareholder return); hedging (requiring disclosure of hedging activities by corporate employees and directors); and clawbacks (requiring disgorgement of incentive compensation paid to executive officers during the three-year period preceding a financial restatement caused by material noncompliance with financial reporting requirements). We expect that these rule proposals likely will not move forward in their current form, and may become moot if Congress eliminates the rulemaking mandates. The CHOICE Act would repeal or amend Dodd-Frank provisions and related rules regarding disclosure of hedging activities, clawbacks of executive compensation, and the frequency of required “say-on-pay” shareholder votes on executive compensation.

Conclusion

It is impossible to predict what the SEC’s agenda will look like after the appointment of a new chair and two new commissioners. What is clear is that there is likely to be a different regulatory approach on a number of fronts.

IPOs—Then and Now

As we mark the twentieth anniversary of our IPO Report, we couldn’t help but step back and reflect on changes in the IPO process over the past two decades.

From a distance, the IPO process has scarcely changed: You gather at an organizational meeting, hold multiple drafting and diligence sessions, prepare a Form S-1, meet at a financial printer to file the Form S-1 with the SEC, resolve SEC comments, pitch investors on a road show, price the offering, sign the underwriting agreement, finalize the prospectus, and then close the deal. Even the 7% underwriting discount for firm-commitment IPOs is still firmly ensconced, except on larger deals. But below 30,000 feet, many things have changed—particularly in light of the JOBS Act.

More Extensive Preparation

Far more preparation—legal, accounting, financial, governance, investor relations and organizational—is now required for an IPO, and more of the work comes earlier in the process. IPO candidates used to select a managing underwriter and hold an organizational meeting to kick off the IPO process, with little advance preparation. Now, if the company has not invested several months or more in getting ready to go public, the IPO schedule will lag behind underwriter expectations as well as the pace of other companies in the IPO queue.

Additional Disclosure Requirements

Disclosure requirements have mushroomed. Companies need to provide much more extensive and elaborate disclosure in areas such as Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A); executive compensation; risk factors; and the financial statements and footnotes. Much of this additional disclosure stems from new and expanded SEC rules (sometimes mandated by federal legislation), but some simply reflects more demanding investor expectations. As a result of these changes, prospectuses have ballooned in length, routinely exceeding 200 pages (including financial statements) and requiring summaries of five to ten pages or more.

Accounting Changes

Accounting issues have assumed unprecedented importance since the enactment of the Sarbanes-Oxley Act. Auditors have become more cautious and risk-averse; audits take longer and cost more; the SEC has become more active in accounting standard-setting and less deferential to companies and their auditors on judgment calls; and new accounting and auditing requirements abound. Among many important rule changes, “non-GAAP financial measures”—which are now frequently included in IPO prospectuses—must be reconciled to GAAP results and presented in a manner that is balanced, that gives equal or greater prominence to the corresponding GAAP measure, and that is not misleading.

Plain English

SEC rules now require prospectuses to be written in “plain English” complying with the principles of short sentences; definite, concrete, everyday words; active voice; tabular presentation or bullet lists for complex material, whenever possible; no legal jargon or highly technical business terms; and no multiple negatives.

Lengthier (But More Transparent) SEC Review

With more information presented in the Form S-1, SEC review takes longer. It used to be possible to clear all SEC comments after only one or two comment letters. Now, four or more sets of comments are typical, and it is almost unheard of to print preliminary prospectuses and begin a road show based on the initial Form S-1 filing or the company’s response to the first comment letter alone. The SEC now publicly releases comment letters and company responses shortly after completing its review of registration statements, providing more visibility into the SEC review process.

Changes in Underwriting and Offering Practices

IPOs with joint bookrunners now represent the majority of all offerings. Most IPOs now have three or four managing underwriters, but syndicates have become much smaller. Road shows frequently include trips to Europe and often utilize charter airplanes to reduce wear and tear on the company’s executives and permit tighter scheduling. Marketing reach is expanded with electronic road shows. Since 2002, the roles of investment bankers and research analysts in the offering process have been separated. Free writing prospectuses can now be used to update information without recirculating a revised preliminary prospectus. Lockup agreements in IPOs almost universally last 180 days, and lockup releases for directors and officers must be publicly announced at least two business days in advance.

New Exchanges and Offering Formats

Nasdaq is now a “national securities exchange”; the Nasdaq National Market has been segmented into the Nasdaq Global Market and the Nasdaq Global Select Market; and the Nasdaq SmallCap Market has been reborn as the Nasdaq Capital Market. The New York Stock Exchange has added NYSE MKT (the former American Stock Exchange) for small growth companies to compete with Nasdaq for IPO listings. Both Nasdaq and the NYSE have become larger and more global through acquisitions, and each is now operated by a public company. In all markets, online and auction formats have grown with the expansion of the Internet, although they account for only a tiny fraction of the overall IPO market.

Longer Timeline

The overall IPO timeline has stretched markedly. Prior to 2000 or so, an IPO candidate could reasonably expect to complete its IPO within 45 to 60 days after the initial filing. Today’s norm is twice that. The longer the IPO process, the more opportunities for the offering to be delayed or scuttled due to poor market conditions or adverse company developments, causing many proposed IPOs to proceed in fits and starts and resulting in many more Form S-1 withdrawals than historically were seen.

Streamlined Filing and Pricing

The SEC’s EDGAR system has made filing simpler, and the information contained in EDGAR filings is instantly available to everyone with Internet access. The format of EDGAR submissions has become more reader-friendly, and a next-generation EDGAR system has been launched. Rule 430A under the Securities Act permits a Form S-1 to be declared effective without including final pricing information, eliminating the need to file a “pricing amendment.” Rule 462(b) provides for immediate registration of additional shares, allowing an IPO to be readily upsized by up to 20% in aggregate gross proceeds.

Heightened Scrutiny and Potential Liability

Each director can be held liable for a material misstatement or omission in the Form S-1 unless he or she is able to demonstrate that, after reasonable investigation, he or she had reasonable grounds to believe that there was no such misstatement or omission. Following an IPO, a company’s directors and officers signing a periodic SEC report can likewise be held liable for a material misstatement or omission in the report. Conduct of directors and officers is increasingly scrutinized, and the company’s CEO and CFO are required to provide personal certifications in connection with each Form 10-Q and Form 10-K. Willful false certifications can result in fines of up to $5 million and imprisonment for up to 20 years.

More Demanding and Complex Investor Relations

A newly public company enters a world of largely unfamiliar and often time-consuming investor relations responsibilities. Investor relations expectations have become more demanding and the legal and cultural environment more complex. Quarterly earnings calls are now standard practice but have not replaced one-on-one calls and meetings. Institutional investors increasingly demand direct board-stockholder engagement on governance and other matters. All investor communications must pass muster under Regulation FD (which prohibits selective disclosure of material nonpublic information to analysts or stockholders). Social media, which barely existed ten years ago, is now an essential component of effective investor relations as well as a tool that can be used against a company by financial activists and dissident stockholders.

Other Regulatory Changes

The NASD has combined with the member regulation, enforcement and arbitration functions of the NYSE to form the Financial Industry Regulatory Authority (FINRA), the principal self-regulatory organization for securities firms in the United States. State securities “blue sky” regulation of IPOs has been largely preempted. The accounting profession is now regulated by the Public Company Accounting Oversight Board (PCAOB), which in turn is overseen by the SEC.

The JOBS Act

Enacted on April 5, 2012, the JOBS Act effected profound changes to the securities laws, with broad implications for pre-IPO companies and the conduct of IPOs, as well as for public companies. Perhaps most importantly, the JOBS Act created an “IPO on-ramp” that permits EGCs to:

- submit a draft Form S-1 to the SEC for confidential review (the Form S-1 and all amendments must be filed publicly no later than 15 days before the road show commences);

- provide reduced financial statement, MD&A, selected financial data and executive compensation disclosures;

- choose not to be subject to any accounting standards that are adopted or revised on or after April 5, 2012, unless and until these standards are required to be applied to nonpublic companies; and

- engage in oral or written “test-the-waters” communications with eligible institutional investors to determine their investment interest in a contemplated IPO, either prior to or following the date of filing of the Form S-1.

EGCs are also exempt from the Dodd-Frank Act requirement to seek stockholder approval of “say-on-pay” advisory votes on executive compensation arrangements; the requirement under Section 404(b) of the Sarbanes-Oxley Act that an independent registered public accounting firm audit and report on the effectiveness of a company’s internal control over financial reporting; and certain future auditing standards adopted by the PCAOB.

A Brief Guide to Selected IPO Terminology, Old and New

- Bookrunner—lead managing underwriter primarily responsible for organizing and conducting the road show, building the “book” of orders, and agreeing with the company on the price and size of the IPO

- Comfort—written assurances, based on specified procedures but not constituting an audit, provided by the company’s auditor to the underwriters with respect to financial information

and other numerical measures derived from the company’s accounting records and contained in the prospectus - Confidential submission—submission by an EGC of draft Form S-1 for confidential SEC review

- DRS—“draft registration statement” confidentially submitted by EGC to SEC

- EGC—“emerging growth company” under the JOBS Act, generally defined as a company with total annual gross revenues of less than $1.07 billion (increased from $1 billion in April 2017)

- FWP—written communication that is used to correct or supplement information contained in a statutory prospectus (stands for “free writing prospectus”)

- Green shoe—option granted by the company and/or selling stockholders that permits the underwriters to purchase additional shares (up to 15% of the IPO), at the IPO price

- Lockup—agreement with underwriters prohibiting a stockholder from selling shares acquired prior to the IPO for a specified period of time following the IPO (typically 180 days)

- Red herring—preliminary prospectus containing the estimated price range and number of shares offered, distributed to potential investors in road show meetings

- Road show—meetings held by the managing underwriters and company management with prospective investors to market shares in an IPO

- Staff—SEC staff employees, including lawyers, accountants, financial analysts, economists, engineers, investigators and administrative employees

The Changing Tides of Corporate Governance

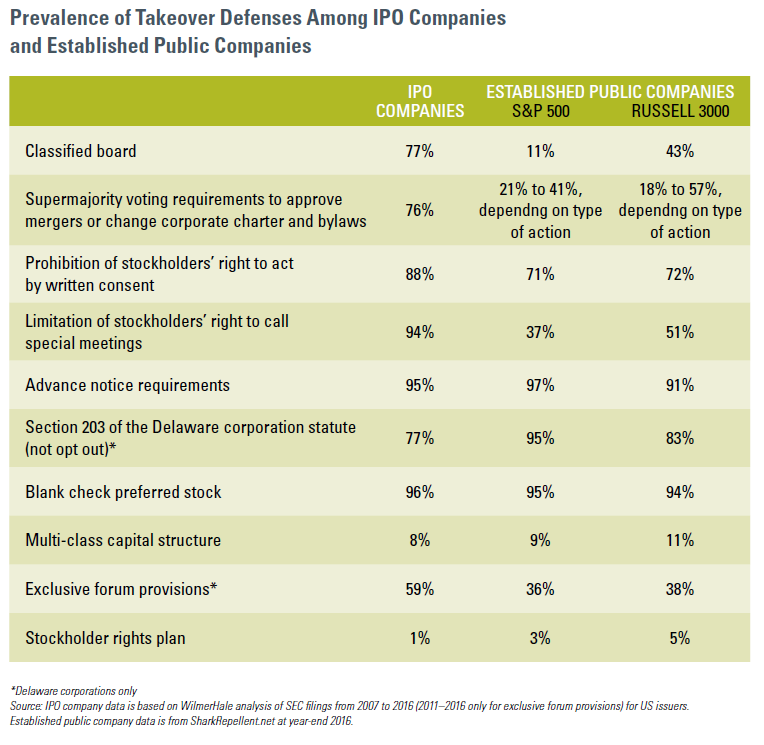

During the past several years, there has been a growing divide between the corporate governance provisions adopted by companies going public compared to those maintained by established public companies. This is especially apparent when the governance practices of IPO companies are compared to those of companies in the S&P 500 index.

To some extent, perhaps even a great extent, the differences make sense and it is unlikely there will ever be complete convergence. However, newly public companies should expect to come under pressure from institutional investors and proxy advisory firms to begin to evolve their governance practices sooner than was the case in the past.

The Great Divide

The current divide in governance practices has more to do with the elimination by established public companies of previously standard provisions, often in response to direct or indirect pressure from stockholders and proxy advisory firms, than with an increased prevalence of these provisions among IPO companies.

The biggest gaps in governance practices relate to how the board of directors is elected, with more than 80% of companies going public in recent years continuing to adopt a classified board structure under which only one-third of the director seats are voted on by stockholders each year. In contrast, nearly 90% of S&P 500 companies provide for annual election of all directors, even though a majority of S&P 500 companies had classified boards as recently as 2006. Another example of the current split in practices is the vote standard applicable to electing directors, with a plurality vote standard continuing to be the norm among IPO companies while almost 90% of S&P 500 companies have adopted a majority vote standard. Prior to 2006, virtually no company had anything but a plurality standard in place.

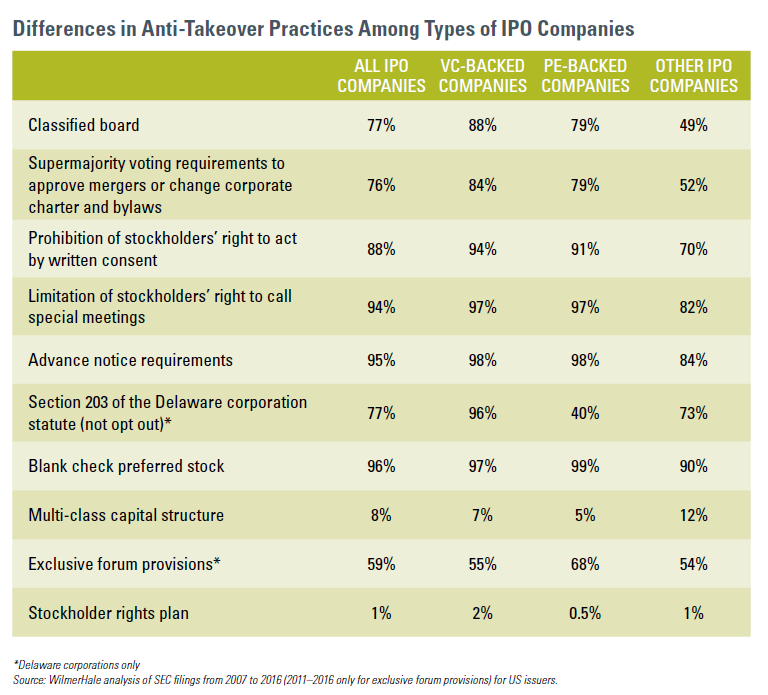

Beyond the differences in adoption rates for the common anti-takeover provisions highlighted in the table to the right, differences also exist with respect to a number of other corporate governance and compensation-related practices. For example, IPO companies are much less likely than established public companies to:

- allow proxy access (this practice is unheard of among IPO companies, whereas over half of S&P 500 companies now provide proxy access, up from a mere handful of public companies, of any size, prior to 2014);

- maintain limits on the number of other boards on which the company’s directors and officers may serve (often referred to as an over-boarding policy);

- adopt a clawback policy for executive compensation;

- adopt minimum equity ownership requirements for directors and officers;

- grant performance-based equity awards (as opposed to equity awards that vest based solely on continued employment); or

- primarily rely on formulas, rather than discretion, to determine payouts under cash bonus programs.

Despite these differences, some practices remain commonplace across public companies, with more than 90% of IPO companies and more than 90% of S&P 500 companies imposing advance notice requirements and authorizing “blank check” preferred stock. In addition, exclusive forum provisions, which are a relatively recent phenomenon, are increasingly being adopted by both types of companies.

The incidence of dual- or multi-class capital structures is also reasonably consistent between IPO companies and established public companies, although much more recent attention has been focused on a handful of well-known companies going public with multi-class structures that include greater disparity in voting power among classes than historically seen.

IPO Companies Often Face Different Considerations

As a general matter, companies adopt takeover defenses in order to help:

- ensure stability and continuity in decision-making and leadership that will enable the company to focus on long-term value creation;

- provide the board with adequate time to evaluate and react in an informed manner to unsolicited acquisition proposals;

- provide negotiating leverage for the board; and

- maximize overall stockholder value by providing economic disincentives against inadequate, unfair or coercive bids.

The consideration of which takeover defenses to implement is somewhat different for IPO companies than for established public companies because:

- the need for takeover defenses may be greater given the IPO company’s state of development, high growth prospects and low market capitalization—any or all of which may make the company more vulnerable to a hostile takeover attempt;

- the existence of strong takeover defenses has not historically had an adverse effect on the marketing of IPOs; and

- anti-takeover provisions that need to be implemented in the corporate charter can be put in place easily prior to the IPO, but will be virtually impossible to adopt after the company is public.

Furthermore, in contrast to the profiles of many established public companies, the governance practices of IPO companies often reflect the high concentration of ownership that will continue to exist following the IPO; the more hands-on nature of the board of directors in place at the time of an IPO (which results in part from the meaningful ownership stakes that many directors hold); and the greater need for flexibility in designing compensation programs that goes hand-in-hand with the uncertainties inherent in companies pursuing new and innovative business models.

Enhanced Scrutiny Ahead

Notwithstanding the different considerations faced by IPO companies, the governance practices of newly public companies have started to come under challenge sooner than in the past. One major reason is a voting policy recently adopted by Institutional Shareholder Services (ISS), the leading proxy advisory firm, which has resulted in more negative vote recommendations on directors where, prior to an IPO, the company adopts charter or bylaw provisions considered by ISS to be adverse to stockholder rights, such as a classified board or a multiclass capital structure. Under its policy, ISS considers the following factors in making its voting recommendations:

- the level of impairment of stockholder rights caused by the provision;

- the company’s or the board’s rationale for adopting the provision;

- the provision’s impact on the ability of stockholders to change the company’s governance structure in the future (such as limitations on the stockholders’ right to amend the bylaws or charter, or supermajority vote requirements to amend the bylaws or charter);

- the ability of stockholders to hold directors accountable through annual director elections, or whether the company has a classified board structure; and

- any sunset provision that will in the future result in the elimination of the disfavored provision.

Importantly, ISS will now consider making a negative vote recommendation on directors at all future stockholder meetings until the adverse provision is either removed by the board or submitted to a vote of public stockholders.

The Council of Institutional Investors (CII) has also recently stepped up its efforts to influence governance practice at IPO companies. The CII’s new policy on Investor Expectations for New Public Companies calls for companies, upon going public, to have a “one share, one vote” structure, simple majority vote requirements, independent board leadership and an annually elected board. The CII policy further provides that CII expects IPO companies without such provisions to commit to their adoption over a reasonably limited period post-IPO.

It remains to be seen whether these changing tides will lead to a major course correction not unlike what has transpired among more established public companies, but directors of newly public companies are well advised to prepare for some potentially rough seas ahead.

Best Practices: It’s More Than Just Following the Rules

The last 15 years have witnessed an explosion in SEC and stock exchange requirements relating to corporate governance and executive compensation. But complying with applicable rules is just the first step in the life of a newly public company, as institutional investors, proxy advisory firms such as ISS and Glass Lewis, and others continue to offer a seemingly endless and frequently evolving supply of recommended “best practices.”

In the last year alone, new or revised model corporate governance guidelines were published by Investor Stewardship Group (discussed on the Forum here), whose signatories include many leading global money management firms; Council of Institutional Investors, a nonprofit association of employee benefit plans, foundations and endowments with significant combined assets; Business Roundtable, an association of CEOs of leading US companies (discussed on the Forum here); and another group of prominent CEOs and representatives of investment managers and institutional investors who published a self-styled “Commonsense Corporate Governance Principles” (discussed on the Forum here).

Moreover, as is the case each year, the proxy advisory firms also made numerous updates to their voting policies and rating systems, and as is becoming increasingly common, a number of prominent investor groups and money management funds continued their practice of sending letters to their portfolio companies, often highlighting desired governance or disclosure practices.

While lacking the force of law, best practices cannot be ignored, as some stakeholders routinely measure public companies against lists of desirable practices. The results of these assessments can influence proxy advisory firm recommendations and stockholder voting. As a result, public company boards find themselves devoting a significant portion of their time—too much of their time, many would lament—debating the merits of recommended practices while still ensuring compliance with applicable regulatory requirements.

The litany of topics swept in by the catchall phrase “best practices” ranges from some that are concrete and prudent to others that are aspirational or unrealistic. Nonetheless, directors who turn a deaf ear to stockholder expectations may find votes withheld in board elections, be required to include stockholder proposals in their proxy statements, or even find their actions questioned in litigation. In some cases, ignoring best practices could also result in a lost opportunity to truly improve the company’s operations and oversight.

Even if some of the provisions of the Dodd-Frank Act and/or the Sarbanes-Oxley Act are rolled back, as advocated by the new US presidential administration and some members of Congress, investors and other stakeholders are unlikely to curb their efforts to push companies to do more than the minimum required by applicable rules. Indeed, in certain areas such as climate change and sustainability, any repeal or retreat by regulators might be countered by increased activity by various non-governmental organizations and charitable foundations that are focused on sustainability and social issues.

Listed below are some of the practices and policies that public companies may be urged to follow. Needless to say, circumstances vary widely, and these may or may not be appropriate for a particular company.

Board of Directors

- Ensure that a substantial majority or all board members, other than the CEO, are independent.

- Separate the roles of chair and CEO, or designate a lead or presiding director if the chair and CEO are the same person.

- In uncontested elections, provide that directors are elected by majority vote rather than a plurality (i.e., require that a nominee receive more votes “for” his or her election than “against” his or her election, rather than allowing someone to be elected so long as he or she receives at least one vote under a plurality system).

- Limit to 90 or 180 days the maximum period of time that a director who did not receive a majority vote in support of his or her re-election is permitted to continue to serve as a director.

- Provide that all directors stand for annual election rather than maintaining a classified (or staggered) board system in which only one-third of the directors stand for re-election each year.

- Arrange for orientation training and continuing education for all directors.

- Conduct annual reviews of board and committee performance (required by NYSE rules) and individual director performance and provide proxy disclosure describing the board’s processes for evaluating directors.

- Develop a succession plan for the CEO and other top executives and provide proxy disclosure about the board’s processes relating to succession planning.

- Develop a director succession plan.

- Establish director term limits or stop considering long-tenured directors to be independent.

- Limit the number of other directorships the CEO and other executives or directors may hold to avoid situations where a director is “over-boarded.”

- Select director nominees in accordance with qualification standards that are established and published by the board.

- Increase board diversity and provide quantitative proxy disclosure about the percentage of women and minorities serving as directors.

- Require directors to offer to tender their resignations upon job changes.

- Create stock ownership guidelines or requirements for officers and directors.

- If board vacancies are filled by board action, permit stockholders to vote on new directors at the next annual meeting.

- Establish a process that provides stockholders a meaningful opportunity to suggest candidates for director nominations or otherwise communicate with the board.

- Allow stockholders to include the names of nominees for election in the proxy statement that is prepared by the company (generally referred to as “proxy access” which, in its most common form, allows a group of up to 20 stockholders who have collectively held at least 3% of a company’s voting stock for at least three years to nominate up to 20% of the total number of directors).

- Publicly disclose policies and procedures for direct engagement between directors and stockholders.

- Create a stockholder relations committee of the board.

Board Committees

- Ensure that a majority or all members of the audit committee qualify as “Audit Committee Financial Experts” under SEC rules.

- Prohibit current or former CEOs of public companies from serving on the compensation committee.

- Establish a separate nominating/governance committee consisting solely of independent directors (required by NYSE rules).

Executive Compensation

- Require directors and executives to retain equity awards for a specified minimum period of time following vesting or through retirement.

- Grant performance-based equity awards (rather than time-based awards).

- For time-based equity awards, require a minimum vesting period.

- Prohibit or limit the acceleration of vesting of equity awards.

- Establish standards for Rule 10b5-1 trading plans adopted by insiders, such as minimum waiting periods before transactions under the plan commence, public disclosure requirements, and limitations on when plans may be entered into.

- Adopt a policy for the recoupment (or “clawback”) of incentive compensation that was determined on the basis on financial statements that are later restated.

- Avoid employment contracts with executives, especially contracts with multi-year guarantees.

- Avoid excessive pay differentials between the CEO and the other executive officers and between the CEO and the median employee.

- Do not use the same performance metrics for both short-term and long-term incentive programs.

- Avoid large bonus payouts without justifiable performance linkage or disclosure.

- Do not change performance metrics during a performance period.

- In annual proxy statement, explain how the company’s compensation programs support achievement of the company’s long-term strategy.

- Avoid excessive perks and do not provide for tax gross-ups for perks.

- Prohibit directors and officers from pledging or hedging company stock.

- Avoid single-trigger change-in-control provisions.

- Exclude the impact of stock repurchases from determinations of achievement of compensation performance targets.

- Do not provide for tax gross-ups for severance payments.

- Require stockholder approval of severance arrangements.

- Require stockholder approval for executive death benefits.

Stockholder Rights

- Do not adopt a poison pill without stockholder approval.

- Provide that a majority vote of stockholders may amend the corporate charter or bylaws and approve mergers.

- Permit stockholders to act by written consent.

- Allow stockholders holding at least 10% of the company’s shares to call special meetings.

- Do not utilize a multi-class capital structure with disparate voting or economic rights.

- Do not authorize blank check preferred stock.

Other Governance Matters

- Establish corporate governance guidelines (required by NYSE rules).

- Adopt a related person transaction policy.

- Adopt an insider trading policy.

- Adopt a disclosure policy.

- Establish a disclosure committee.

- Post corporate governance documents on corporate website (required by NYSE rules).

- Adopt simple majority voting (providing that a proposal is passed only if the votes for the proposal exceed the votes against the proposal, without taking into consideration abstentions or broker non-votes) for all matters on which stockholders vote.

Corporate Social Responsibility

- Publish a comprehensive sustainability report addressing how the company’s operations affect the environment and society.

- Integrate disclosure about sustainability issues into the company’s SEC filings.

- Make public disclosure about the company’s carbon footprint and other impacts of climate change.

- Adopt a policy regarding public disclosure of political contributions and lobbying activity.

- Adopt and disclose a broad equal employment opportunity and non-discrimination policy.

- Adopt international fair labor and human rights standards.

- Address income inequality issues, including gender pay gaps and the minimum wage.

One Share, How Many Votes?

While most companies go public with a single class of common stock that provides the same voting and economic rights to every stockholder (a “one share, one vote” model), an increasing number of companies are going public with a multi-class capital structure under which some or all pre-IPO stockholders hold shares of common stock that are entitled to multiple votes per share, while the public is issued a separate class of common stock that is entitled to only one vote per share, or in one very recent example, no general voting rights.

Purpose and Effect

Use of a multi-class capital structure enables the holders of the high-vote class of common stock to retain voting control over the company, even while selling a large number of shares of stock to the public. Supporters of this technique believe that it can enable company founders to pursue strategies to maximize long-term stockholder value rather than seeking to satisfy the quarter-to-quarter expectations of short-term investors. Critics, however, believe that a multi-class capital structure entrenches the holders of the high-vote stock, insulating them from takeover attempts and the will of the public stockholders, and that the mismatch between voting power and economic interest may increase the possibility that the holders of the high-vote stock will pursue a riskier business strategy.

A multi-class capital structure can also be employed to provide different classes of stock with equivalent voting rights but disparate economic rights, such as the right to receive dividends or distributions upon liquidation, or can be utilized for tax structuring reasons.

Timing of Implementation

If a multi-class capital structure is going to be implemented, it must be put in place prior to the company’s IPO, as both Nasdaq and NYSE restrict the ability of already public companies to implement multi-class capital structures.

A company may implement a multi-class capital structure either upon incorporation or at some later point prior to its IPO. Due to fiduciary duty limitations, if a multi-class capital structure is implemented after incorporation, all then-existing stockholders will hold high-vote stock unless they otherwise agree, and thereafter the company can issue any class of authorized stock (highvote, low-vote or no-vote) to subsequent stockholders. If a company implements a multi-class capital structure upon incorporation, it can elect to issue stock of any authorized class from the outset.

Prevalence

Multi-class capital structures are not new, but they are appearing with greater frequency and, in some instances, have greater disparity in voting power among classes than historically seen. As recently as 2008, no company went public with a multi-class capital structure, but since then almost 10% of all US companies completing IPOs have had a multi-class capital structure.

In addition, at least four public companies that employed a dual-class capital structure for their IPOs over the past 15 years subsequently authorized a third class of non-voting stock for potential use for stock-based acquisitions and equity-based employee compensation without dilution of the founders’ voting control. For each of these four companies, the post-IPO creation of non-voting stock resulted in stockholder litigation alleging breaches of fiduciary duty, suggesting that an IPO company that desires to have non-voting stock available for use after its IPO should consider building the non-voting stock into its capital structure prior to the IPO. In early March, Snap became the first company to do so, by offering non-voting shares to the public.

Structure

The most common approach to a multiclass capital structure in recent years has consisted of:

- Class A common stock, with one vote per share, sold to the public; and

- Class B common stock, with 10 votes per share, held by all pre-IPO stockholders (generally the result if the structure is implemented shortly before the IPO) or held only by the founders and other selected pre-IPO stockholders (generally indicating that the structure was implemented upon incorporation or early in the company’s life).

In most multi-class capital structures the disparate voting rights apply to all voting matters, except as otherwise required by applicable state corporate law, but the higher voting rights of the high-vote stock are sometimes limited to specific matters.

Market Practices

Implementation of a multi-class capital structure requires decisions to be made on a number of structural questions. To assess market practices, we reviewed the SEC filings of all VC-backed tech companies with multi-class capital structures that completed IPOs from 2007 to 2016. There were a total of 30 companies in the sample, representing approximately 10% of all US IPOs in this period. Below is a summary of our findings:

Number of Classes

- At the time of IPO:

- 29 of the 30 companies had two classes of stock (two of these companies subsequently created a third class of non-voting stock).

- One company had three classes of stock (high-vote, super-high-vote and low-vote).

Voting Rights

- Of the 30 companies, 27 provided that the high-vote stock had 10 votes per share:

- In 25 companies, the high-vote stock had 10 votes per share on all matters.

- In one company, the high-vote stock had 10 votes per share on changes of control and charter amendments and one vote per share on all other matters.

- In one company, the high-vote stock had 10 votes per share on changes of control or certain changes to equity incentive plans and one vote per share on all other matters.

- One company provided that the high-vote stock had 150 votes per share.

- One company provided that the high-vote stock had 20 votes per share.

- One company provided that one class of high-vote stock had 70 votes per share on all matters and the other class of high-vote stock had seven votes per share.

Holders of High-Vote Stock

- In 22 of the 30 companies, the high-vote stock was held by all pre-IPO stockholders.

- In two companies, the high-vote stock was held by founders and certain other pre-IPO stockholders.

- In four companies, the high-vote stock was held by founders only.

- In two companies, the high-vote stock was held by certain pre-IPO stockholders other than founders.

Stock Incentive Plans

- In 23 of the 30 companies, the high-vote stock was used for pre-IPO awards and the low-vote stock was used for post-IPO awards.

- In seven companies, the low-vote stock was used for all awards.

Preferred Stock Conversion

- In 23 of the 30 companies, preferred stock converted into high-vote stock in the IPO.

- In three companies, preferred stock converted into low-vote stock in the IPO.

- In two companies, one or more series of preferred stock converted into highvote stock in the IPO and one or more series of preferred stock converted into low-vote stock in the IPO.

- Two companies had no outstanding preferred stock at the time of the IPO.

Mandatory Conversion Events for High-Vote Stock

- Any transfer (with specified exceptions)—all 30 companies.

- Death or incapacity/disability of holder (sometimes with founder exception or delay)—20 companies.

- Class vote by high-vote holders—21 companies (2/3 vote in 12 companies, and majority vote in nine companies).

- Sunset provision—14 companies (11 companies with 5-10 years, one company with 12 years, one company with 17 years and one company with 20 years).

- Treatment of partnership distributions:

- In five companies, there are specific exceptions for transfers of highvote stock from partnerships to partners and from limited liability companies to members.

- In the other 26 companies, it appears the high-vote stock converts into lowvote stock upon a limited partnership’s distribution to its limited partners.

- Dilution tests:

- In 12 companies, the high-vote stock converts to low-vote stock when the high-vote stock represents less than a specified percentage (ranging from 5% to 25%) of all outstanding common stock.

- In two companies, the high-vote stock converts to low-vote stock when the high-vote stock represents less than a specified percentage (5% and 10%, respectively) of the voting power of all outstanding capital stock.

- In one company, the high-vote stock converts to low-vote stock when the high-vote stock represents less than 20% of the shares of high-vote stock outstanding at the time of the IPO.

- In one company, the high-vote stock converts to low-vote stock when less than a specified number of shares of high-vote stock (which represented 10.2% of the outstanding shares of high-vote stock plus low-vote stock at the time of the IPO) are outstanding.

Conclusion

Although disfavored by institutional investors and proxy advisory firms, a multi-class capital structure can serve legitimate purposes and further stockholder interests. The board of a company considering the implementation of a multi-class capital structure needs to balance its intended benefits against the risks of entrenchment (particularly if the specific structure chosen favors the founders or another small group of stockholders) and the potential for adverse investor sentiment.

The Sample Set

For our review of market practices, we reviewed the multi-class capital structures in the following IPOs:

- AppFolio (2015)

- Apptio (2016)

- Box (2015)

- Castlight Health (2014)

- Clearwire (2007)

- Facebook (2012)*

- Fitbit (2015)

- GoPro (2014)

- Groupon (2011)

- Internet Brands (2007)

- KAYAK Software (2012)

- KiOR (2011)

- LinkedIn (2011)

- MaxLinear (2010)

- MINDBODY (2015)

- Nutanix (2016)

- Pure Storage (2015)

- RingCentral (2013)

- Square (2015)

- Tableau Software (2013)

- The Trade Desk (2016)

- Twilio (2016)

- Veeva Systems (2013)

- Wayfair (2014)

- Workday (2012)

- Workiva (2014)

- Yelp (2012)

- Zillow (2011)*

- zulily (2013)

- Zynga (2011)

*subsequently authorized a class of non-voting common stock

The complete publication is available here.