Print

PrintJohn Roe is Head of ISS Analytics at Institutional Shareholder Services, Inc. This post is based on an ISS publication by Mr. Roe.

Earlier this [month], ExxonMobil released a preliminary tally revealing that 62.3 percent of shareholders supported a non-binding shareholder resolution calling for “an annual assessment of the long-term portfolio impacts of technological advances and global climate change policies, at reasonable cost and omitting proprietary information.” A similar proposal filed just last year garnered only 38.1 percent shareholder support—which leads to the question, what’s changed so dramatically in the past year? We’ll get to that in a moment—but first, let’s take a look at shareholder proposals voted so far in 2017, and put those into some historical context.

Environmental proposals lead the way in 2017

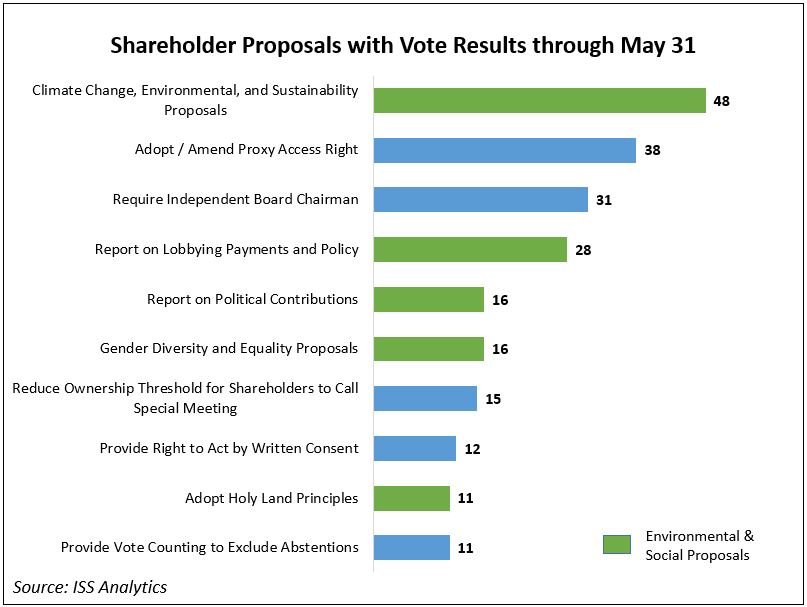

With 330 shareholder proposal results filed by U.S. companies so far this year, we have a good idea of where trends are headed for the full year. 2017 stands out as a year where environmental proposals are emerging more frequently and gaining widespread traction among investors.

On top of these results, more than 80 additional proposals will be voted on this month—and results from proposals voted in May are still being released.

Only eleven percent of voted shareholder proposals earned majority support so far in 2017

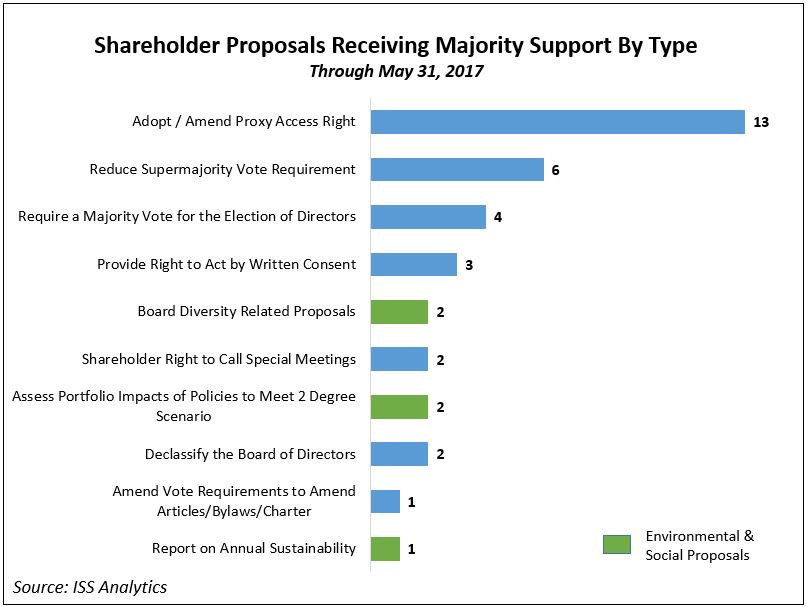

Of the 330 shareholder proposals with voting results published through May 31, and excluding proxy contest-related proposals, 36 have received at least 50% shareholder support. Among these, proxy access proposals are leading the way. The next two are more traditional governance-related proposals: voting rights related proposals and proposals requesting shareholders’ right to act by written consent. But interestingly, we’re beginning to see success with environmental and social proposals this year, much more than ever before. Already, we’re seeing shareholders have success with board diversity and climate change proposals—and these are in addition to ExxonMobil’s proposals, which had not yet been reported via 8-K as of June 1.

The majority-supported environmental & social shareholder proposals appearing in the list above, while small in number, may signal an important shift in shareholder thinking and willingness to act. In comparison, last year only one climate change proposal was majority-supported, a request for a report on sustainability including greenhouse gas goals at CLARCOR.

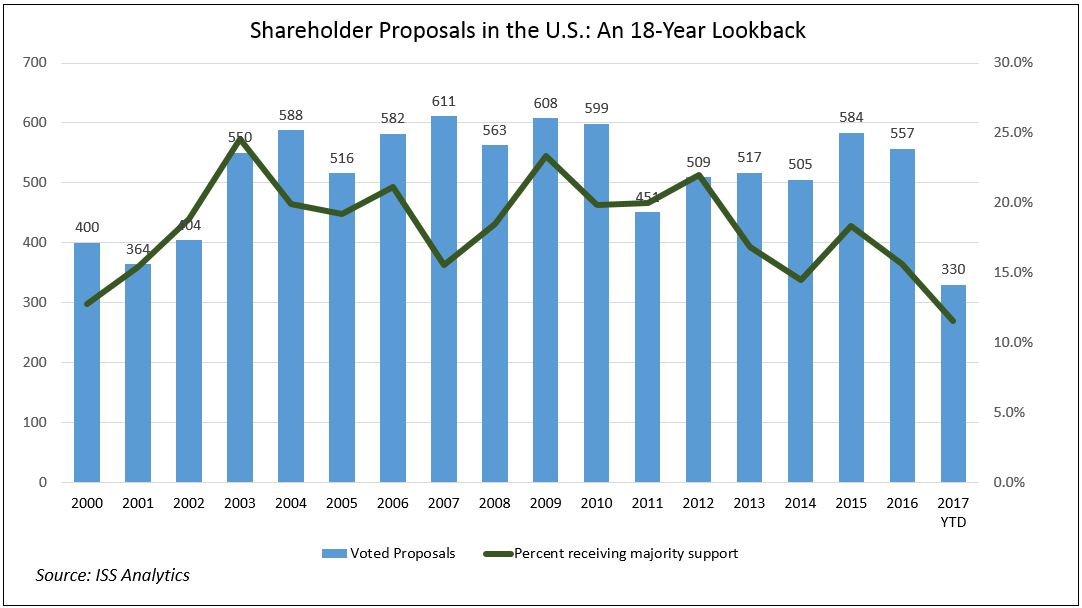

Majority support rate lowest in 18 years

Since 2015, much of the shareholder proposal dialogue has been focused on proxy access—but taking a longer view provides some perspective on how today’s proposal activity compares to years past. Notably, 2017 is on track to have the lowest percentage of majority-supported proposals in the last 18 years.

Looking across all U.S. companies that ISS covers, we find more than 9,200 shareholder proposals with published vote results filed since 2000. And although much has been made of the proxy access success, the number of proposals making it to the vote over the last few years has not made it back to the 600+ peaks back in 2007 and 2009. The reasons for this are many, and may include:

- Greater proactive focus on governance issues among issuers

- Increased dialogue between companies and shareholders, leading to issues being resolved off the ballot more often

- Fewer opportunities to “clean up” legacy practices such as staggered boards and plurality vote standards among larger companies

At ExxonMobil, same proposals but new results: a sign of the trend reversing?

ExxonMobil provides a glimpse at what may become an increasing trend: old proposals with new results. With a reported vote result increase of 24 percentage points on a substantially similar proposal over the 2016 result, ExxonMobil’s outcome begs the question: Is the change due to new voters casting votes, or is it a “change of heart” among longer-term investors? While the data is still coming in, it doesn’t appear to be a shift in the shareholder base—according to FactSet Research, nine of the top ten shareholders in 2016 were still in the top ten in 2017, as were seventeen of the top twenty holders. In fact, shareholders exiting the top twenty holders list accounted for less than 1.5 percent of all shares outstanding.

The conclusion is, then, that shareholders who voted against the proposal in 2016 changed how they voted in 2017. While N-PX filings for many large institutional holders will be available later in the year to confirm the votes cast, widely-reported statements by large holders such as BlackRock and State Street indicate that they are changing how they look at, and act upon, these issues.

The results of these changes may be two-fold: One, reversing the trend of a smaller percentage of proposals earning majority support, and two, emboldening would-be proponents to file an increasing number of environmental & social proposals.

What’s Next? Private ordering a possible replacement for public policy

With the recent announcement that the United States will withdraw from the Paris climate accord, we’re beginning to see a groundswell of broad-based investor and issuer support for issues that public policy may be pulling back on. Notably, Goldman Sachs CEO Lloyd Blankfein issued his first tweet ever [on June 1, 2017], using the platform to establish his position on environmental issues.

Other institutional investors, asset owners, and issuers have affirmed their support for emerging and legacy environmental and social issues. It appears that many proxy voters are adjusting their voting policies on related shareholder proposals. As these policies become more widespread, there is the potential for a significant shift in the outcomes of shareholder proposals in general, leaving us with the question: is 2017 the nadir for support of shareholder resolutions? Time will tell.