Print

PrintPatrick Verwijmeren is Professor of Corporate Finance and Rex Wang Renjie is a PhD candidate in Finance at the Erasmus School of Economics at the Erasmus University Rotterdam. This post is based on a recent paper by Professor Verwijmeren and Mr. Wang Renjie.

A directorship is rarely a full-time job. Most directors have other occupations and many directors serve on multiple boards. Given that attention is not unlimited for directors, in our paper Director Attention and Firm Value, we ask the question whether directors can still fulfill their job effectively when their other occupations happen to require more of their attention.

We rely on a sample of S&P 1500 firms over the 1996 to 2014 period with at least one outside director with multiple directorships. These directors need to distribute attention among their directorships, which provides a useful setting to study the effect of director attention. As we cannot observe exactly how much time or energy directors spend on each of their directorships, our identification strategy is designed to exploit plausibly exogenous variation in how directors allocate attention across their directorships. The following simple thought experiment illustrates our approach. Consider two otherwise identical companies in a given industry and quarter. Director A sits on the board of company 1 and on the board of firm “Car” in a totally different industry, namely the automotive industry. Director B sits on the board of company 2 and on another firm that is not in the automotive industry. Suppose now that there is an attention-grabbing event in the automotive industry. Assuming limited attention, director A may shift attention towards company Car and away from company 1. The manager at company 1 consequently receives less monitoring and advice. In contrast, company 2 is not affected since its director is not related to the automotive industry. Thus, we can identify the impact of variation in director attention on firm value by studying the changes in the value of company 1 relative to that of company 2 around the time when director A is distracted.

A noteworthy feature of our identification strategy is that we consider the source of distraction at the industry-level rather than at the firm-level. A firm-level approach has the crucial disadvantage that firm-level shocks could be driven by the ability of the director. For instance, if we classify director A as distracted when company Car does poorly (as opposed to the whole automotive industry), then this could simply be attributed to the bad performance of director A. Director A might be a poor monitor and/or adviser, and as a result, both company Car and company 1 can underperform at the same time. Considering industry-level shocks mitigates this concern as it is less likely that the ability of one single director affects the performance of the whole industry.

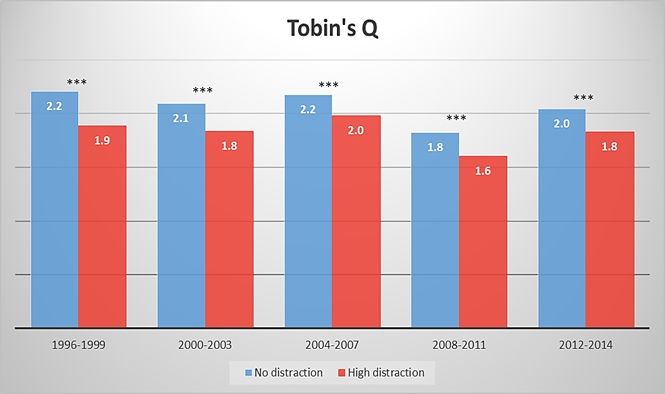

We construct a firm-level distraction measure by examining shocks to unrelated industries in which directors have additional directorships. To obtain insights into whether this measure really captures director attention, we examine board meeting attendance and show that directors that our measure identifies as distracted indeed attend fewer board meetings. We employ this measure of director distraction to study how director attention affects firm value. By examining Tobin’s Q and stock performance, we find that firm value drops significantly when board members are distracted, as illustrated in Figure 1. A deviation from no distraction to the average distraction level is associated with a 2.6% discount in quarterly Tobin’s Q, and a stock market underperformance of about 66 basis points per quarter. This effect is particularly strong when the distracted directors are independent and/or sit on an important committee of the board.

Figure 1: The effect of director distraction on Tobin’s Q

We investigate multiple potential channels to better understand the negative effect of director distraction on firm value. When managers receive less monitoring from distracted directors, two potential agency problems might be exacerbated: (1) managers engage in empire building and make value-destroying investment decisions, or (2) managers become more passive and enjoy a quiet life. Alternatively, managers might miss important advice or have to delay making important decisions when it is difficult to schedule meetings with distracted directors for discussion and approval. We find that firms with more director distraction invest significantly less and are less likely to announce takeovers. These changes are due to firms with distracted directors being less active rather than them postponing their investments. The acquisitions that are still being announced when directors are distracted do not destroy value. Overall, our findings are mostly in line with managers preferring a quiet life.

In sum, we exploit a new and exogenous source of time-variation in the monitoring intensity of directors with multiple directorships and find strong evidence that director distraction has a negative impact on firm value. We thus document the potential costs of having busy directors. Our findings support policies restricting the number of directorships that an individual is allowed to have. Nevertheless, it is important to note that we do not argue that directors with multiple directorships are detrimental to shareholder value per se, since firms could benefit from the knowledge and network of a director who serves on multiple boards.

The complete paper is available for download here.