Print

PrintSharon Hannes is Professor of Law and Dean of the Faculty at Tel Aviv University Buchmann Faculty of Law; Asaf Eckstein is Lecturer on corporate law and securities law at Ono Academic College. This post is based on their recent paper.

In our new paper, we propose a novel framework for an incentive pay scheme for proxy advisory firms. Proxy advisory firms play an influential role and wield extensive influence over major corporate decisions in the United States and all over the world. The leading proxy advisory firms—Institutional Shareholder Services (“ISS”) and Glass, Lewis & Co. (“Glass Lewis”), which together account for 97 percent of the industry—were said to be “de facto corporate governance regulators,” or “de facto arbiters of U.S. corporate governance,” and their voting recommendations were described as “a milestone” for many crucial deals. As once noted by Chief Justice Leo Strine:

[P]owerful CEOs come on the bended knee to Rockville, Maryland, where ISS resides, to persuade the managers of ISS of the merits of their views about issues like proposed mergers, executive compensation, and poison pills.

The recognition of the major role played by proxy advisory firms has also sparked much criticism. Above all, critics have accused proxy advisors of having no “skin in the game.” Despite their great influence over companies’ votes and practices, proxy advisory firms “have no economic interest in the companies for which they are giving their recommendation.”

To alleviate this concern, we put forth a pay-for-performance framework for proxy advisory firms, in lieu of the currently used fixed fee arrangement. Our framework is suitable for vote recommendations that have a crucial impact on the welfare of the shareholders of the relevant company, such as votes on mergers and acquisitions.

We suggest that in case the advisory firm recommended against the bid and the shareholders decided (in line with the recommendation) to reject it (or if the bid was withdrawn for any other reason), the advisor fee shall be crafted to put the proxy advisor in a long position on the stock of the target company. However, if the bid was rejected (or otherwise withdrawn) contrary to the advisory firm’s recommendation, the advisory firm’s fee shall be crafted to put the proxy advisor in a short position on the target stock. Such a compensation structure would provide the proxy advisors with a healthy portion of skin in the game that is lacking today. Given the increasing number of failed M&A deals (in 2016 more than 20% of the announced 3.9 trillion global deal volume has eventually broke apart) proxy advisors should always be ready to bear the financial consequences of their recommendations.

Let us turn briefly to a real-life example in order to illustrate our proposal. On September 28, 2015, Williams Companies, Inc., a publicly traded energy infrastructure corporation, entered into a merger agreement with Energy Transfer Equity. Williams stockholder were offered a consideration of $43.50 per share, with the intention to create one of the world’s largest energy infrastructure companies. Williams’ share price just prior to announcing the deal on September 25, 2015 was $41.60.

Three out of the four of proxy advisory firms that covered the vote—ISS, Egan-Jones and Pensions & Investment Research Consultants Limited (“PIRC”)—recommended that Williams stockholders vote “FOR” the proposed transaction with Energy Transfer. Only Glass Lewis recommended that Williams shareholders vote “AGAINST” the proposed transaction.

Ultimately, the shareholders never had a chance to vote on the deal. The buyer, Transfer Equity, withdrew from the deal. Williams’ share price on the closing day of June 24, 2016, the day the deal broke apart, was $21.31. Williams’ share price half a year later, on December 23, 2016 was $31.56, and one year later on June 23, 2017, was $28.75.

In hindsight, Williams shareholders lost a lot of money because of the termination of the deal. However, Glass Lewis, who was against the deal, and had the bid had not been withdrawn might have caused its clients to vote against it, did not bear any direct cost. In contrast, ISS, Egan-Jones and PIRC who were all in favor of the deal, did not receive any reward for their recommendation, even though at least in hindsight it seems they provided valuable advice.

Our proposed pay scheme aims to correct both related shortfalls, and thus improve proxy advisors’ incentives to provide thoughtful advice.

The idea is to use part (or all) of the proxy advisor’s fee to buy suitable forward agreements on the stock of the target. Let us turn first to Glass Lewis, which recommended rejecting the bid. In such a case Glass Lewis would receive a forward agreement to buy the stock of Williams for $43.50, which is the price of the deal. This is because an advisor who is against the bid must manifest its belief in the long-term stand-alone value of the target. In contrast, ISS (or Egan-Jones and PIRC), which recommended accepting the bid, would receive a forward agreement to sell the stock of Williams for $43.50. This is because an advisor who is for the merger should manifest its belief that the long-term stand-alone value of the target would not meet the merger price.

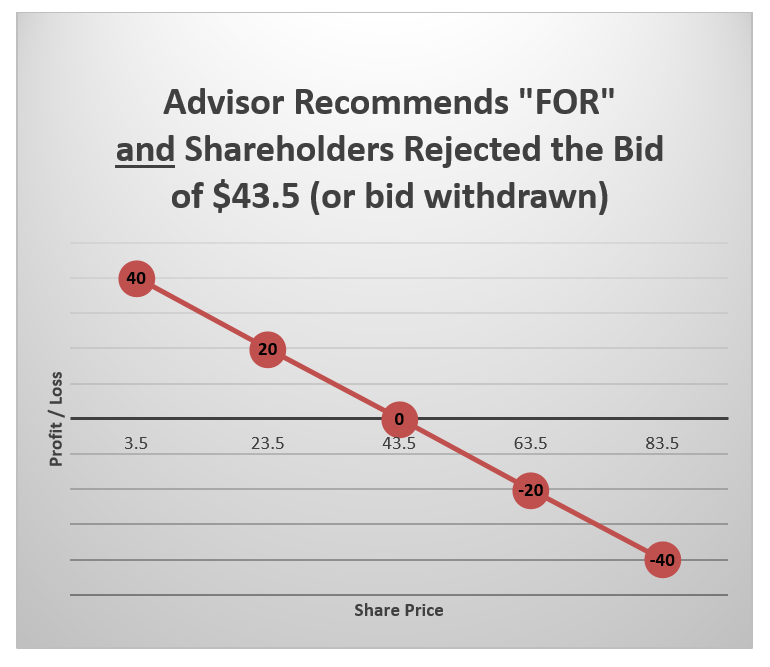

Figure 1 below illustrates the payoff structure that Glass Lewis faces when it holds such a forward agreement to buy Williams shares.

Figure 1

Figure 2 shows that a forward agreement (to buy the shares of Williams for the strike price of $43.50) yields a profit of one dollar for any dollar that Williams’ share price tops the deal price upon the closure of the agreement. When Williams’ share price passes the deal price, the forward agreement promises its holder to buy Williams shares below their market price. Alternatively, if Williams’ share price upon termination of the forward agreement falls short of $43.50, Glass Lewis would bear a loss. In such case, the forward agreement compels Glass Lewis to buy Williams shares above their market price.

Let us turn then to the fee structure of proxy advisors who recommend for the merger. Figure 2 below illustrates the payoff to the proxy advisors (ISS, Egan-Jones and PIRC) who were in favor of the deal in the Williams case.

Figure 2

Figure 2 shows that a forward agreement to sell the shares of Williams for a strike price of $43.50, yields a profit of one dollar for any dollar that Williams’ share price falls short of the deal price upon the closure of the agreement. When Williams’ share price passes the deal price, however, the forward agreement requires its holder to sell Williams’ shares below their market price. The opposite is true if Williams’ share price upon termination of the forward agreement falls short of $43.50, yielding a profit for ISS. In such case, the forward agreement promises ISS to sell Williams shares above their market price. Recall that ISS was for the deal. Their advice to the shareholders was to get rid of their shares for $43.50. If this turns out to be good advice, given that Williams’ shares fall short of this price after the deal breaks down, ISS would have gained from it. In the contrary scenario—they would lose.

The benefits of our proposed fee structure are quite straightforward. Our model of a long/short compensation scheme improves proxy advisors’ incentives, which in turn makes their recommendations more credible. This incentive-aligning compensation scheme therefore also alleviates concerns that were recently voiced by the U.S Congress, the SEC, practitioners, and the media. Unlike the current flat fee structure, under our proposed fee structure the advisor may suffer a direct financial loss from what turns out to be a bad recommendation. Similarly, the advisor can now profit from a good recommendation. Put differently, the advisor now has substantial skin in the game.

The complete paper is available for download here.