Print

PrintSteve W. Klemash is Americas Leader, Kellie C. Huennekens is Associate Director, and Jamie Smith is Associate Director, at the EY Center for Board Matters. This post is based on their EY publication.

In this age of innovation and transformation, today’s board members face increasingly complex challenges in overseeing corporate culture, strategy and risk oversight.

The digital revolution has facilitated radical changes in business models and made cybersecurity a strategic business imperative. Intangible assets have become a primary driver of long-term value, making the talent agenda mission-critical. Companies are adapting to changes in the labor market, digitization and automation, and a growing spotlight on corporate values and purpose. And all of this is occurring against a backdrop of rising geopolitical tensions and trade policy challenges.

We have tracked board structures since 2013, examining how S&P 500 companies are using board committee structure to address oversight needs. This post is based on a review of the 418 proxy statements filed as of 15 May 2018. The same set of companies in 2018 and 2013 were examined to provide consistency in the review.

Findings

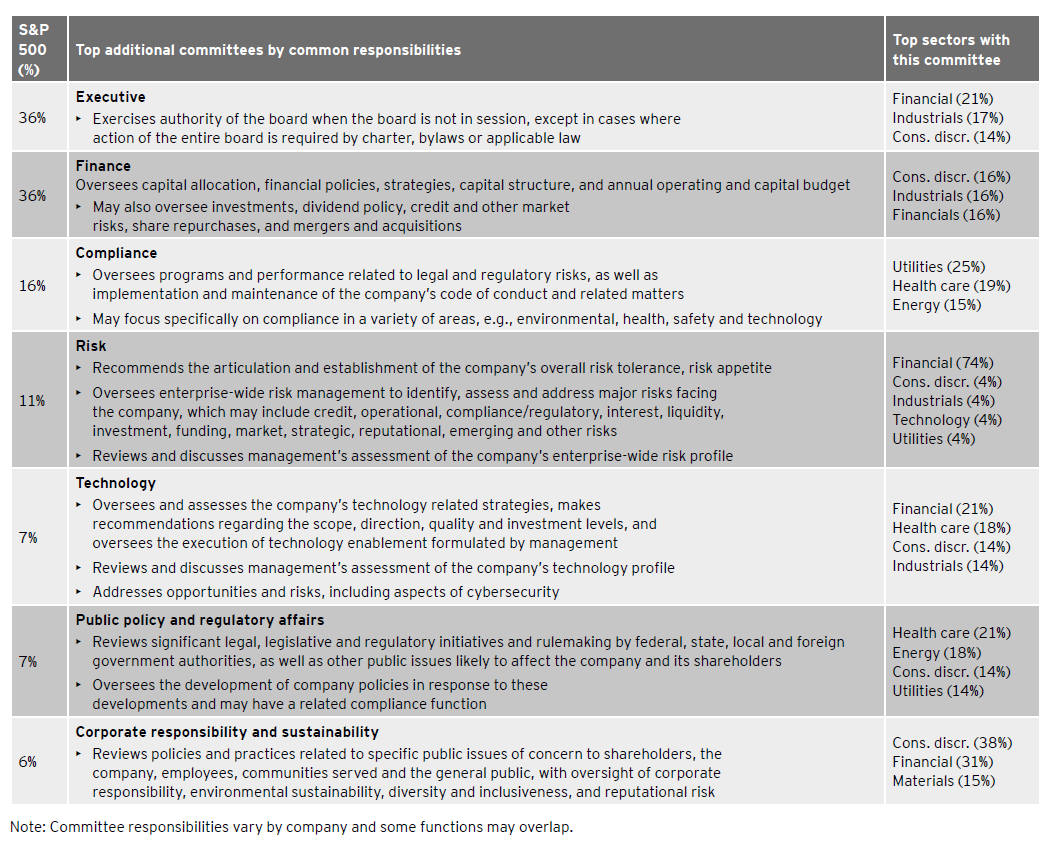

Amid sustained and unprecedented change, board committee structures stayed largely the same over the past six years. Across all industries, boards primarily rely on the three “key” committees generally required by the stock exchanges—audit, compensation, and nominating and governance. [1] Bank holding companies (BHCs) of a certain size, whether public or privately held, are required to also have separate risk committees—a “fourth key committee” so to speak. [2] Above and beyond these committees, institutions typically have one additional standing board committee (“additional committee”) (usually an executive or finance committee). During 2013-18, the portion of companies with at least one additional committee grew marginally from 74% to 76%, and the average number of additional committees remained largely consistent.

The most common committees remained the same. More than one-third of S&P 500 companies had an executive or finance committee. Use of executive committees declined slightly from 38% to 36%, while finance committees held steady at around 36%. Other committees were much less common.

Industry matters. Financial, telecommunications and utilities companies average two or more additional committees. Health care, consumer staples, industrials, consumer discretionary and materials average one to two. Energy, real estate and technology companies average less than one.

Few additional committees focus on emerging risk and innovation. Compliance, risk and technology committees grew marginally. In 2018, the overall percentage of S&P 500 companies with these committees remained low at 16%, 11% and 7%, respectively. Other types of committees largely held steady or declined.

A variety of additional committees oversee technology matters. Ten percent of companies assigned oversight of cybersecurity, digital transformation and information technology to an additional committee. These were typically technology, risk or compliance committees.

Our perspective

Today’s boards are navigating a sustained, highly disruptive and competitive environment. Board agendas have become increasingly packed with complex and evolving oversight topics, and key committee responsibilities have stretched beyond their core purview. Challenging the committee structure as part of the board assessment process may help the board determine the most effective oversight approach based on the company’s unique circumstances.

The ideal board committee structure is appropriate for the company’s specific needs and the board’s unique culture, is forward-looking, and supports the board’s ability to think strategically and comprehensively about key elements of the company business.

A closer look at the big banks

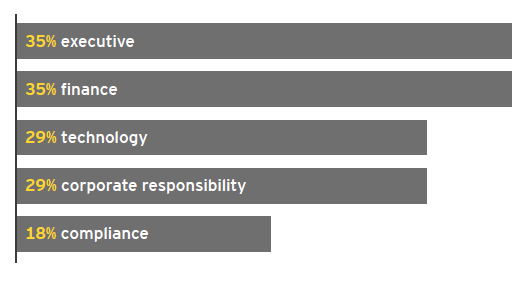

Large BHCs are unusual in that they are required to have a board- level risk committee. For these firms, other common additional committees included:

Questions for the board to consider

- Is the board’s committee structure appropriate to forward-looking board priorities and company specific needs?

- Is the board size and composition adaptable to changing committee responsibilities as needed based on the company’s evolving oversight needs?

- Is the board familiar with how peer companies are addressing board oversight responsibilities?

- Do assessments of board effectiveness reveal possible pressure points that might be resolved with changes in committee structure?

- As committees assess their own effectiveness and performance, is their capacity, workload and areas of expertise part of that assessment?

- As new directors join the board and bring new areas of expertise, does the board consider whether the current committee structure fully leverages those new director skills?

Endnotes

1Subject to certain exemptions, companies listed on the NYSE or NASDAQ must have independent audit, compensation and nominating/corporate governance committees. As an alternative to a nominating/corporate governance committee, director nominees may be selected by a majority of the independent directors for NASDAQ-listed companies.(go back)

2The Federal Reserve’s Enhanced Prudential Standards require separate risk committees for large publicly held US bank holding companies with total consolidated assets of \$10 billion or more.(go back)