Print

PrintAustin Vanbastelaer and Charles Gray are consultants at Semler Brossy Consulting Group, LLC. This post is based on a Semler Brossy memorandum by Mr. Vanbastelaer, Mr. Gray, Todd Sirras, Kayla Dahlerbruch, and Justin Beck. Related research from the Program on Corporate Governance includes the book Pay without Performance: The Unfulfilled Promise of Executive Compensation and Executive Compensation as an Agency Problem, both by Lucian Bebchuk and Jesse Fried.

CEO pay gets most of the attention for the Say on Pay vote. It’s less clear how shareholders interpret and evaluate pay levels for the other named executive officers excluding the CEO (“NEOs”) and to what degree these values impact Say on Pay outcomes. We looked at S&P 500 Say on Pay results from the past three years to understand how NEO compensation influences Say on Pay voting and made four key observations:

- Shareholder support typically decreases as CEO or NEO pay increases, particularly when high pay is not aligned with company size.

- Voters are more responsive to CEO pay than to pay for a company’s other NEOs.

- However, pay levels for a company’s other NEOs also impact vote results.

- High pay for an entire executive team and/or diverging pay between a CEO and NEOs within an executive team can negatively impact vote results.

Top quartile CEO and NEO pay has resulted in lower vote support among S&P 500 companies in the past three years

Shareholder support typically decreases as CEO or NEO pay increases, particularly when high pay is not aligned with company size

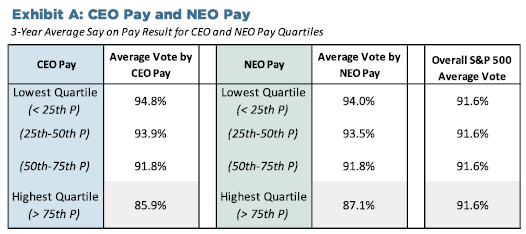

Top quartile CEO and NEO pay has resulted in lower vote support among S&P 500 companies in the past three years. Average Say on Pay support for all S&P 500 companies over the past three years was 91.6% (Exhibit A). By comparison, average vote support was 570 basis points lower among the highest quartile CEO pay group and 450 basis points lower among the highest quartile NEO pay group.

Additional context about company size is needed to fully capture the dynamic between executive pay levels and Say on Pay outcomes. Since we know CEO and NEO pay are largely driven by company size, we divided the S&P 500 companies into quartiles based on pay and revenue. Measuring pay and revenue allows us to assess whether executive pay levels align with company size, and to what degree relative pay levels affect Say on Pay.

Voters are more responsive to CEO pay than to pay for a company’s other NEOs

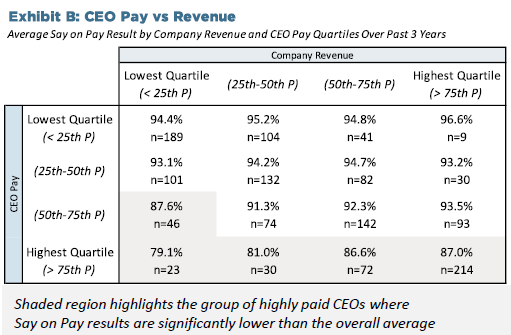

As CEO pay magnitude outpaces company size, Say on Pay support declines. Among the S&P 500’s highest paid CEOs, companies in the lowest revenue quartile received 79.1% average Say on Pay support, compared to 87.0% among companies in the highest revenue quartile. Vote results in Exhibit B support the common notion that shareholders are critical of highly paid CEOs, particularly when pay is misaligned with company size. But to what degree do shareholders look beyond the CEO to evaluate pay for the rest of the executive team?

Competitive CEO pay alone does not always provide companies with a free pass in Say on Pay voting

Pay levels for a company’s other NEOs impact vote results

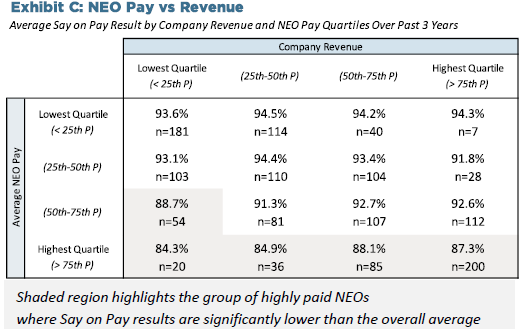

Media and proxy advisor focus on CEO pay creates a perception that NEO pay is not relevant to Say on Pay. However, three-year vote history for the S&P 500 tells us that Say on Pay is not just about CEO pay. Shareholders are responsive to how companies pay their entire executive team. Similar to the findings for CEO pay, average Say on Pay support was lowest among companies where average NEO pay (excluding the CEO) outpaces company size.

Vote patterns suggest that NEO pay has less of an impact on Say on Pay support, but investors will still criticize outliers that pay in the top quartile. In particular, the smaller companies in the top quartile NEO pay group received lower vote support than the larger companies. It’s important that a company maintains pay levels for the rest of its NEOs that don’t go too far beyond other similarly sized companies—competitive CEO pay alone does not always provide companies with a free pass in Say on Pay voting.

High pay for an entire executive team and/or diverging pay between a CEO and other NEOs can negatively impact vote results

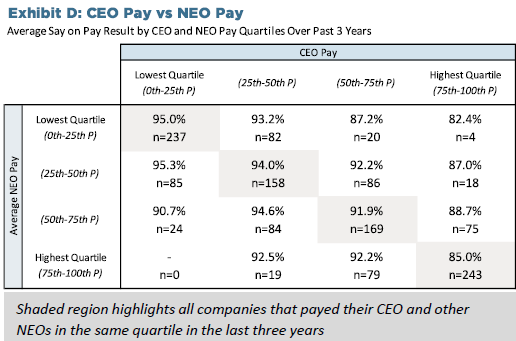

Exhibit D illustrates the relationship between a company’s CEO and average NEO pay and to what degree relative pay within a team affects Say on Pay. CEO and NEO pay positioning are typically aligned—over half the S&P 500 pays its CEO and NEOs in the same quartile. Among these companies, there is a strong inverse relationship between executive pay and Say on Pay outcomes. However, we also observe that voters are responsive to CEO and NEO pay alignment within an executive team. Although very few companies pay their CEOs in the bottom quartile and pay their NEOs in the top quartile, or vice versa, vote history suggests that vote support declines as pay for one outpaces the other. Among companies with bottom quartile CEO pay, Say on Pay support declines significantly for those that pay NEOs above median. And among companies with bottom quartile NEO pay, Say on Pay support declines significantly for those that pay CEOs above median. Executive pay should be aligned with the company’s size, as well as with pay for the company’s other executives. Companies open themselves up to shareholder scrutiny during Say on Pay voting if pay for their CEO or NEOs goes above a competitive range relative to size or relative to other executives on the team.

Pay levels for the entire executive team should be carefully evaluated

Our study suggests that shareholders consider NEO pay in addition to CEO pay when making Say on Pay votes, as vote results are lower when CEO or NEO pay is misaligned. CEO pay receives a majority of the attention from proxy advisors and media and has a greater impact on Say on Pay outcomes, but it’s important to make sure that pay for all NEOs is being carefully evaluated.

Differentiation in roles and levels of responsibility, as well as considerations around succession planning, drive pay dynamics for all NEOs. It’s common that companies will pay above market for premium talent that they see as a prospective future leader for their business. However, the rationale behind such decisions should be defensible and explained in the proxy. Pay magnitude for all executive positions tends to reflect company size, and companies should be cognizant that investors will be wary if pay for the entire executive team is too high relative to company size.