Print

PrintBen Burney is Senior Advisor at Exequity, LLP. This post is based on an Exequity memorandum by Mr. Burney. Related research from the Program on Corporate Governance includes Paying for Long-Term Performance by Lucian Bebchuk and Jesse Fried (discussed on the Forum here).

Our analysis finds company size as measured by employee count is the primary driver of the CEO Pay Ratio; company revenue and market capitalization are secondary drivers. Deeper analysis uncovers industry trends that may provide companies additional context as they compare their CEO Pay Ratios to those of their peers. Ultimately, despite some interesting trends uncovered, analysis of the CEO Pay Ratio data provides little actionable intelligence for companies and questionable, if any, value for investors. More concerning, we find potential avenues for critics of executive pay to manipulate the data to serve their interests or constituencies. The purpose of this post is to provide guidance on what the data says—and what it doesn’t.

What Drives the CEO Pay Ratio?

A common question related to the CEO Pay Ratio is: Does CEO pay or median employee pay [1] have a greater impact on the CEO Pay Ratio? We note, this question is akin to asking whether the value of an investment is more influenced by the stock price or the number of shares. As much as the number of shares and the stock price both impact the value of an investment, both CEO pay and median employee pay impact the CEO Pay Ratio.

But what about the key drivers of CEO pay and median employee pay? As is well known, CEO pay is most heavily influenced by revenues and market cap—the two primary determinates compensation committees use when making decisions on setting target pay levels. Median employee pay bears little relation to either revenues or market cap but, as our research uncovers, is highly, though inversely, correlated with employee count, i.e., higher employee counts are correlated with lower median employee pay. With these facts in mind, the more important question is: What is the impact of company size on the CEO Pay Ratio?

To explore impacts on CEO Pay Ratio and to generate potential insights, we gathered available CEO Pay Ratio data from 372 S&P 500 companies and performed statistical analyses. To analyze the data collected, we calculated correlations [2] between CEO pay, median employee pay, CEO Pay Ratio, and company size, as measured by revenues, employee count, and market capitalization. Our analysis finds:

- Employee count is strongly and positively correlated with the CEO Pay Ratio, 0.58, meaning the more employees a company employs, the higher the CEO Pay Ratio.

- Median employee pay is strongly and inversely correlated with the CEO Pay Ratio, -0.74, meaning the lower the median pay, the higher the CEO Pay Ratio; (though we would note, median employee pay is also an input to the CEO Pay Ratio, so this finding is less meaningful than the relationship between employee count and the CEO Pay Ratio).

- CEO pay correlates well with the CEO Pay Ratio, 0.53, but ranks below median employee pay and employee count (again noting that CEO pay is an input to the CEO Pay Ratio).

- Revenues correlate well with CEO pay, 0.46, but bear little relation to median employee pay, -0.07.

- Employee count is inversely correlated with median employee pay, -0.46, and positively correlated with CEO pay, 0.28; this is notable because it means higher employee counts are associated with both lower median employee pay and higher CEO pay.

- Employee count is strongly correlated with revenues, 0.79.

- Market cap is weakly correlated with both median employee pay, 0.15, and the CEO Pay Ratio, 0.19.

The most notable finding is that in the aggregate and excluding the pay figures, CEO Pay Ratios are driven primarily by the number of employees at a company. This finding is significantly more meaningful than whether CEO pay or median employee pay have a greater impact on the CEO Pay Ratio because employee count is not an input in the CEO Pay Ratio itself (as the pay figures are).

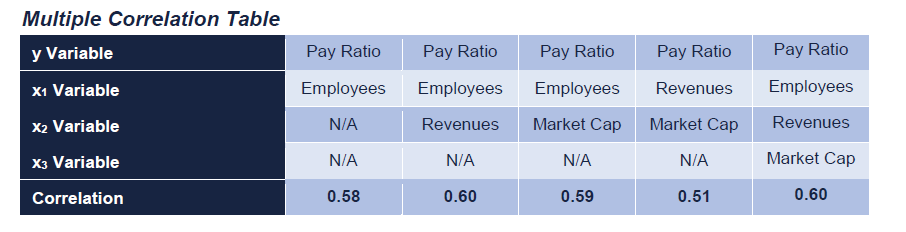

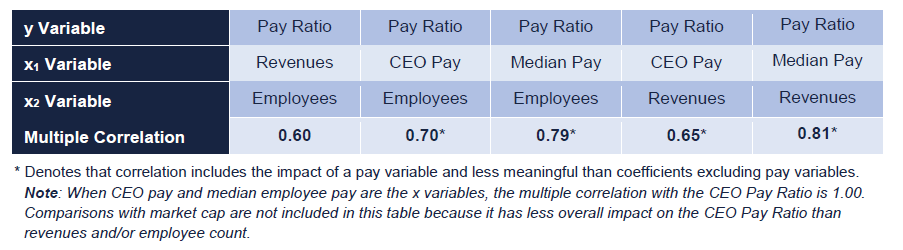

Since employee count is much more associated with median employee pay, however, we sought to answer a logical follow-up question: Does including revenues or market cap to the calculation materially increase the overall correlation with the CEO Pay Ratio? What is the combined impact? To find the answer, we calculated the multiple correlation coefficients [3] of these variables with the CEO Pay Ratio. Interestingly, the combined impact of other size variables only marginally increases the overall correlations with employee pay.

Including pay variables in the mix improves correlations, but the fact remains that company size alone is nearly as strongly correlated with the CEO Pay Ratio as median employee pay—one of the CEO Pay Ratios’ two components.

The more complicated data analysis reinforces the initial finding: CEO Pay Ratios are defined largely by employee count. In our view, this is evidence supporting the notion that the CEO Pay Ratio disclosure provides investors with little, if any, meaningful information they can use to make investment decisions.

Industry Observations

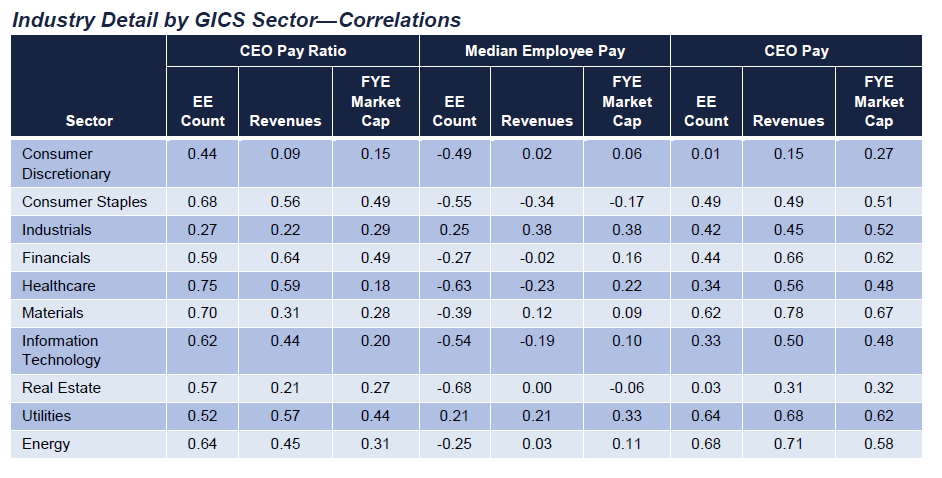

Observers have noted CEO Pay Ratios within certain industries are lower due to largely higher median employee pay. We would also note the employee counts of companies in certain industry sectors such as Consumer Discretionary and Consumer Staples often have substantially higher employee counts relative to most other sectors. Employees in certain industries, particularly Energy and Utilities tend to have workforces with higher median employee pay levels, due to the nature of work performed by their median employees in comparison to those at companies in other industries. Such industry differences may be of

interest when comparing one company’s CEO Pay Ratio against “industry peers,” though we note even within industry sectors (and also compensation peer groups), there are commonly significant business models rendering comparisons of limited use.

Notably, within these industries, trends identified from among the broader data set generally hold true: employee count is typically equivalently or more positively correlated with the CEO Pay Ratio and negatively correlated with median employee pay. Industrials companies, however, buck the trend. For these companies in aggregate, employee count is less strongly correlated with the CEO Pay Ratio

and unlike most other industries, median employee pay is positively correlated with employee count. The reason may be the mix of companies represented in Industrials, which range from airlines to manufacturing companies to business services. Employee population of these companies are very different, resulting in notable dispersions in median employee pay. For Industrials, as with other industries, CEO pay follows the broader trend (bigger size, higher pay).

Manipulating CEO Pay Ratio Data

As noted earlier, one of the primary rationales labor unions and other critics of executive compensation put forth in support of the then-pending Dodd-Frank rule was one of investors being more fully informed. The implication is that CEO Pay Ratios may impact or be associated with corporate performance—similar to how observers and critics of executive compensation often selectively compare pay and performance data to draw conclusions about disparities between pay and performance. To support the notion that CEO Pay Ratios impact performance, we expect some observers may attempt to draw misleading comparisons between CEO Pay Ratios and company performance to find headline-grabbing conclusions.

For demonstrative purposes, we analyzed CEO Pay Ratios, CEO pay, and median employee pay in relationship to 1-, 3-, and 5-year total shareholder return (TSR). Observers searching for meaning in the data, such as proponents of CEO Pay Ratio, could make the following claim:

2018 CEO Pay Ratio data show that companies with high median employee pay and/or low CEO Pay Ratios outperform those with low median employee pay and/or high CEO Pay Ratios. This proves that paying your workers more and your CEOs less results in better stock price performance.

This would be a startling claim. On its face, it could seemingly validate the usefulness of the CEO Pay Ratio—and with cherry-picked statistics, it is not technically inaccurate. In isolation, median 5-year TSR [4] for companies with the highest decile median employee pay is 117% versus 91% for the lowest decile median employee pay. For companies with the lowest decile CEO Pay Ratios, median performance was 95% versus those with the highest decile, 87%.

However, statistics can be cherry-picked both ways. It would also be possible to make the claim that higher CEO Pay Ratios result in better short-term performance because on a 1-year TSR basis, the companies with the higher CEO Pay Ratios outperformed (at the median of each decile) those with the lowest CEO Pay Ratios.

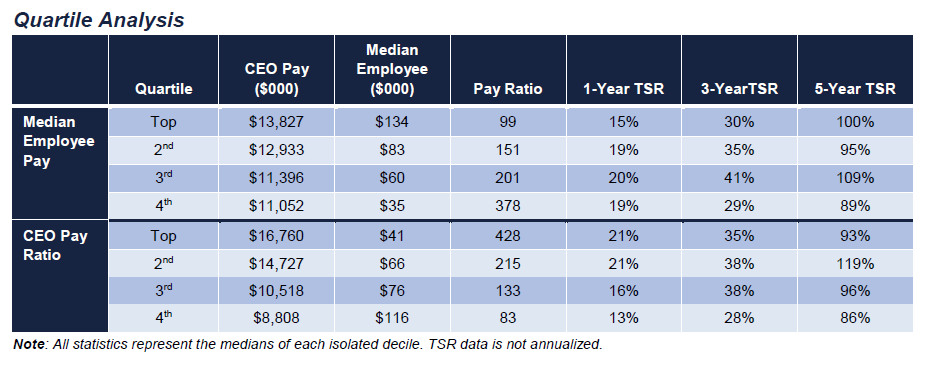

A more fulsome analysis would involve segmenting the full dataset, for example into quartiles, and calculating correlations between the variables to determine whether the data is meaningful. And in fact, the data is not meaningful. Correlations between median employee pay, the CEO Pay Ratio and 1-, 3-, and 5-year performance range from -0.05 to 0.03, meaning there is no meaningful relationship between median employee pay and performance or the CEO Pay Ratio and TSR. Segmenting the data into quartiles by each measure reinforces the fact that there appears to be no relationship between the CEO Pay Ratio and TSR performance. Therefore, drawing any affirmative conclusions about the “impact” of CEO Pay Ratios or median employee pay on performance is grossly misleading.

The decile analysis presented below is an example of how an observer could use data in isolation to draw startling, but misleading, conclusions using CEO Pay Ratio data.

The quartile analysis below demonstrates how more robust analyses that do not cherry pick CEO Pay Ratio data. A close inspection of the data reveals no discernable relationship between CEO Pay Ratio or median employee pay and performance.

Discussion

One of the key rationales which proponents of the CEO Pay Ratio cited was how the new disclosure

would provide investors with relevant information they could use to evaluate Say-on-Pay proposals and/or make investment decisions. However, even before companies were required to begin publishing the CEO Pay Ratios in their proxy statements, most reasonably dispassionate observers indicated they would be hesitant to draw conclusions, judging the figures to be of little use. Our analysis confirms there are few, if any, actionable insights arising from the data—and industry trends may be worthy of note, but they are not instructive. Ultimately, the CEO Pay Ratio is what we thought it is: A datapoint requiring disproportionately more effort to produce than will ever be realized in value to investors.

Endnotes

1Median employee pay is defined in Section 953(b) of the Dodd-Frank Wall Street Reform and Consumer Protection Act as “the median of the annual total compensation of all employees of the issuer, except the chief executive officer (or any equivalent position) of the issuer.”(go back)

2Correlation is a measure of how two variables relate to one another and range in value from -1.00 to +1.00. A correlation of -1.00 means the two variables move perfectly in opposite directions, whereas a correlation of +1.00 means they move perfectly in tandem. A correlation of 0.00 means the two variables are statistically unrelated, i.e., when one moves up, the other is no more likely to move up than down.(go back)

3A multiple correlation assesses the combined impact two variables have on a single other variable (i.e., two independent x variables compared to a dependent y variable).(go back)

4TSR figures presented here are not annualized.(go back)