Print

PrintSteve W. Klemash is America’s Leader, Jamie C. Smith is Associate Director, and Kellie C. Huennekens is Associate Director, all at EY Center for Board Matters. This post is based on their EY memorandum.

Board leadership structures have evolved dramatically over the past 20 years. Today, 92% of S&P 1500 companies have independent board leadership, up from just 10% in 2000. This change corresponds to a rise in independent directors, as well as the continuing separation of chair and CEO roles.

Today, 60% of S&P 1500 companies have separate individuals serving as chair and CEO, more than doubling the 27% that separated the roles in 2000. But while the shift towards independent board leadership is clear, the form that leadership takes, and the responsibilities assigned to those leaders, differ among companies.

We reviewed S&P 1500 companies and found that, among the various independent leadership structures, independent board chairs have been experiencing the fastest increase since 2000. We also found marked differences between the levels of authority commonly assigned to the different independent leadership roles, as well as emerging disclosure and engagement trends that raise the profile and highlight the strength of independent board leaders.

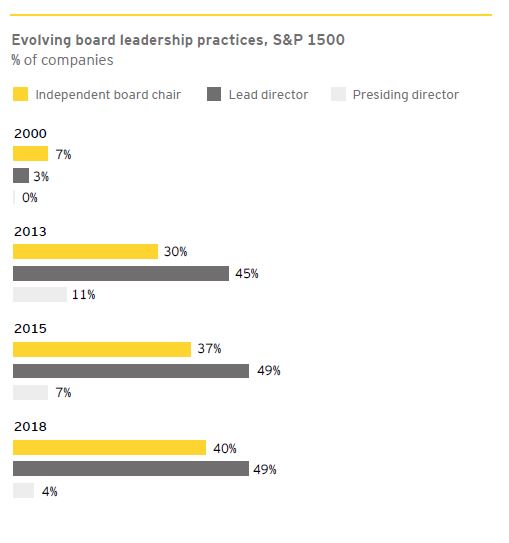

Continuing trend toward independent chairs

When it comes to independent board leadership, views on best practice vary. Corporate disclosures differ on why one type of leadership structure may be more effective for a particular company. Also, what works best may change over time based on company-specific circumstances and board dynamics. Views among investors differ too. For some investors, there is no substitute for an independent board chair, while others find lead directors to be sufficient provided the responsibilities are clearly defined and robust.

The evolving independent board leadership landscape reflects this varied approach. While overall more S&P 1500 companies are appointing independent chairs, S&P 500 companies are still far more likely to have lead directors. The practice of appointing presiding directors, who are often viewed as having a more passive role, continues to decline.

Boards should use the annual self-evaluation process or a time of transition as an opportunity to reconsider the appropriate board leadership structure given the company’s specific circumstances.

Increase in independent board leaders parallels rise in independent directors

The shift to independent board leaders goes hand-in-hand with another governance shift over the same time period: a significant increase in independent directors. In 2000, 65% of S&P 1500 directors were considered independent vs. 83% in 2018.

Most S&P 1500 boards today include only one or two directors who are not independent, going well beyond listing standards that require a majority of independent directors. Even controlled companies, which are not required to have a majority independent board, usually comply with or exceed this threshold.

A note about the data

Not all companies have independent board leadership, and a small number of companies have both independent chairs and lead or presiding directors. While a majority of S&P 1500 companies separate the chair and CEO positions, most have a non-independent director (often a current or former company executive) serving as chair.

Title matters: how key responsibilities differ

Lead director positions serve as a kind of compromise in terms of board leadership structures. They maintain the unified leadership of the combined CEO/chair while providing an independent counterbalance to management’s leadership on the board. They do not command the same authority as a board chair, but their role is generally more robust than that of a presiding director.

Our review of the key responsibilities assigned to independent chairs, lead and presiding directors at companies in the 2018 Fortune 100 illustrates this differentiation among the roles. The role of independent chair is distinct in regard to responsibilities related to calling and chairing meetings of the full board and shareholder meetings. Most lead directors have many of the same powers as that of an independent chair, such as calling and chairing meetings of the independent directors and approving board meeting agendas, schedules and information. The authority of presiding directors is generally more limited.

Lead directors do not command the same authority as a board chair, but their role is generally more robust than that of a presiding director.

Spotlighting independent board leaders in disclosures and engagement

U.S. Securities and Exchange Commission rules require companies to disclose in the proxy statement their board leadership structure, including why that structure was determined to be appropriate for the company, how the structure and the board’s risk oversight responsibilities relate to each other, and whether the same person serves as CEO and board chair. Where the CEO and chair positions are combined, companies must disclose whether they have a lead independent director and, if so, explain the specific role the lead director plays in the leadership of the board. [1]

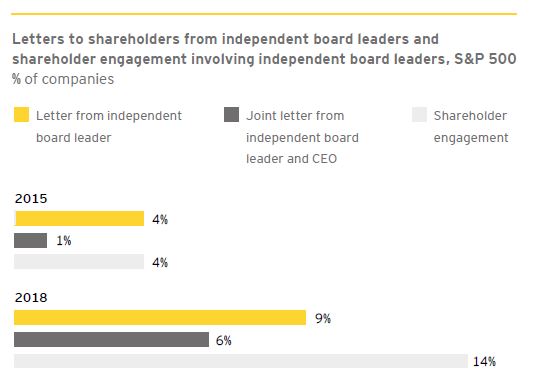

Companies continue to identify ways to use the proxy as an effective tool for engagement and communication with stakeholders. One way they are accomplishing this is with letters to shareholders from the independent board leader, or the full board itself, which communicate the board’s message around prominent governance topics such as board composition and effectiveness, board oversight of strategy, shareholder engagement, and key governance and pay changes.

Having such a letter come from the independent board leader highlights that individual’s role and can showcase the strength and authority of that independent position vis-a-vis the CEO. In 2018, 15% of S&P 500 companies included a letter to shareholders either from the independent board leader alone or jointly from the independent board leader and the CEO, which is three times the number in 2015. Around 60% of these letters were from lead directors and around 40% were from independent chairs, which may reflect additional efforts by lead directors to more clearly demonstrate independent leadership on a board that is chaired by the CEO.

Direct engagement with shareholders, as appropriate, is another avenue for building shareholder trust in the strength of independent board leadership, including by raising the profile of the independent board leader and showcasing that individual’s qualifications and expertise. And the practice is on the rise: this year 14% of S&P 500 companies disclosed that the board’s independent leader was directly involved in engagement conversations with shareholders over the past year, up from 4% in 2015. More than a third (36%) of the lead directors, and almost half (47%) of the independent chairs involved in these engagement conversations also wrote letters to shareholders in the proxy statement.

Other emerging trends that highlight the strength of independent board leadership include discussion in the proxy statement of how the current independent board leader is uniquely qualified for the role based on his or her relevant expertise and leadership qualities, and key focus areas or activities of that leader over the previous year.

Questions for the board to consider

- How is the independent board leader selected and their performance evaluated? Are those processes robust?

- Do the key responsibilities assigned to the independent board leader sufficiently empower that individual to provide strong independent leadership? And are those responsibilities clearly defined in the company’s governance documents and communicated to investors?

- Does the board understand how key shareholders view its leadership structure? And how is it addressing any related shareholder interests or areas of focus?

- Are there opportunities to better communicate the strengths of the board’s current leadership

structure and the effectiveness of the current independent board leader? - What is the process for evaluating the board’s leadership structure? Are there opportunities to enhance that evaluation?

Endnotes

1SEC Proxy Disclosure Enhancements Rule, 16 December 2009.(go back)