Print

PrintBarbara Novick is Vice Chairman at BlackRock, Inc. This post is based on Ms. Novick’s testimony at the recent FTC hearing on common ownership.

Good morning, and thank you for inviting me to speak on institutional investors, diversification, and corporate governance. I make my comments from the perspective of a practitioner in asset management.

Investment Stewardship

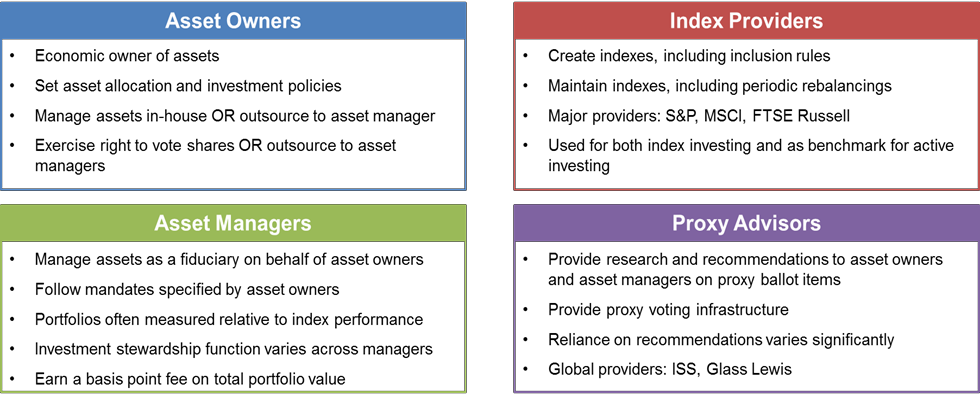

Investment stewardship is a critical element of the corporate accountability chain that empowers shareholders to engage and vote on issues relevant to the long-term success of a firm, and to hold company boards accountable. It is the very essence of how shareholders can exercise their rights to have a say in the governance of the firm in which they own a stake.

This clearly matters to the asset owners, who are the economic owner of the shares, as they participate directly in the fortunes of each company in their portfolio. It also matters to asset managers, who act as fiduciary agents on behalf of asset owners.

Voting in proxies is one of the primary ways that shareholders can express their views on matters important to the success of the company. Many asset owners choose to vote themselves. This includes both asset owners who manage their assets in-house, as well as some who outsource to asset managers. When an asset manager has the authority to vote on behalf of their clients, stewardship codes and regulations encourage, and in some cases mandate, them to do so.

Many asset owners and asset managers use the services of proxy advisors, who make voting recommendations. To understand the role of institutional investors in corporate governance, it is therefore important to understand the wider investment stewardship ecosystem and the different roles of the various participants.

Continuum of Active and Index Strategies

Before I address the debate on common ownership theories, which brings us here today, let me first note that common ownership itself is not about “active” versus “passive” investment. If the theory of common ownership has value, it must logically apply to any investment strategy in which an investor holds more than one company in a sector; that is, diversified investment in general.

Investment strategies are best thought of as a continuum, from the most actively managed to the most index-oriented, rather than as an active / passive dichotomy. All of these strategies may include investment in multiple companies in a sector.

Stock indexes are a critical component underlying both index and active portfolios. Index strategies are designed to closely track the performance of the index by tracking its composition. These strategies have grown significantly as they provide the average investor with low cost access to market returns.

Active strategies, by contrast, are intended to outperform the index by deviating from its composition. The degree of deviation varies significantly across the continuum from “enhanced index” strategies to “closet indexing” to much more concentrated portfolios.

One of the proposals suggested by commentators in the common ownership debate is to limit portfolios to holding one company per sector. If that were the case, virtually all diversified portfolios would no longer be viable. This includes the thousands of pension plans that help millions of individuals save for retirement.

Index Products Closely Track Index Composition

Index providers are another key participant in the ecosystem. Companies such as S&P, MSCI, and FTSE Russell create indexes that represent broad markets as well as specific sectors and geographies, using a variety of methodologies. Indexes are rule-based, as determined by the index provider, and are intended to represent the investable market or a specific sector or asset class. Index portfolios are adjusted when the index provider adds or drops a company from the index. Understanding stock inclusion rules and index rebalancings is therefore essential to managing equity portfolios, whether index or active.

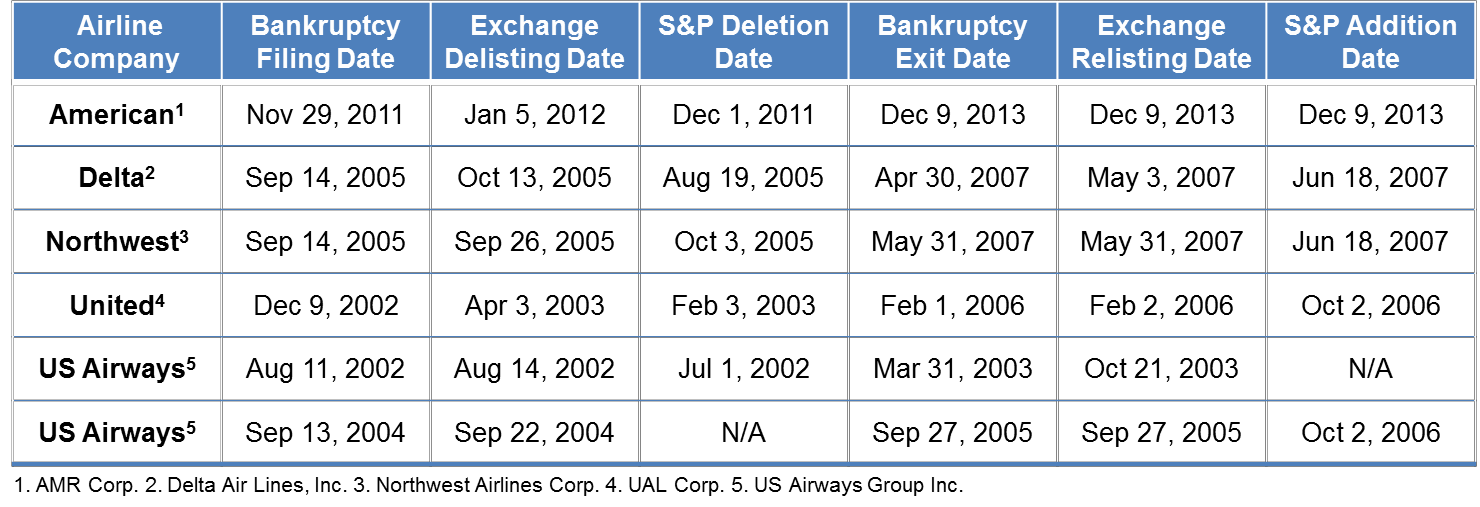

The often-cited paper Anti-Competitive Effects of Common Ownership assumes that managers continue to hold airlines during periods of bankruptcy. [1] The reality is quite different.

When a company declares bankruptcy, its stock is delisted from the stock exchange, and index providers promptly remove it from their indexes. In contrast, when a company exits bankruptcy, there can be a significant lag before its stock is returned to the relevant indexes. In the case of US Airways, which experienced two periods of bankruptcy for approximately 7 months and a year respectively, the stock was excluded from market indexes for over 4 years.

As a rule, managers of index investment strategies sell and buy stocks close to the timing of when these deletions and additions to the index occur. In the case of the airline paper, 28 of the 56 quarters of the study period are impacted by this incorrect assumption. [2]

Investment Stewardship: Engagement and Voting

Investment stewardship includes both engagement and voting. The objective of investment stewardship is to maximize long-term value for clients.

Engagement may include dialogue with companies in person and/or by phone as well as letters. Keeping in mind that a company’s Board represents its shareholders, the primary focus of engagement is on governance issues, as the quality and involvement of the Board is paramount to representing shareholders’ interests.

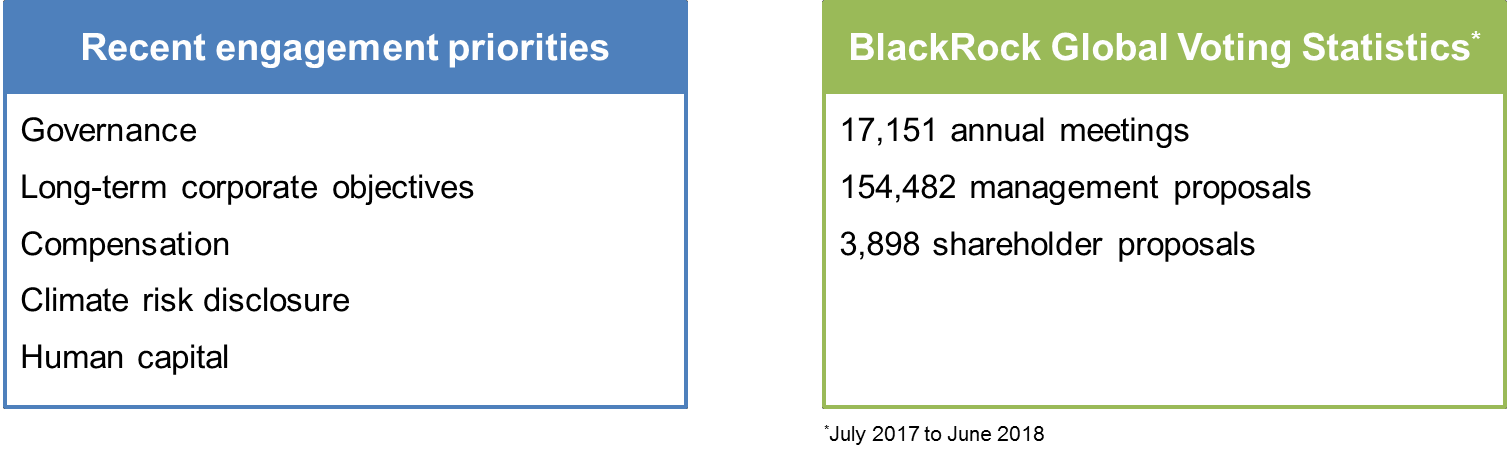

As a fiduciary, BlackRock engages on behalf of our clients with companies on issues impacting their long-term financial performance. Our engagement is focused on asking questions and providing our feedback. In addition to board governance, we have engaged with companies to understand their long-term strategy, assess the alignment of executive compensation with shareholder returns, encourage climate risk disclosure, and understand how the company is addressing human capital management. [3] Importantly, engagement is never about product pricing decisions. We represent a minority of the shares outstanding (generally in the single digits), and company Boards must also take the perspectives of many other shareholders into account.

Compensation

Let me briefly touch on compensation as it is one of our engagement priorities and compensation has been discussed in the context of common ownership. At BlackRock, when our Investment Stewardship team evaluates executive compensation, we start from the premise that Boards (and their compensation committees) should set pay policies that are aligned with the company’s long-term strategy. Compensation consultants retained by company Boards play a key role in designing these compensation plans. Plans are commonly based on own-firm performance relative to peer companies, as measured by metrics such as pre-tax income, margin improvement, shareholder returns and, notably, outperforming competitors.

Proponents of the common ownership theories believe that the presence of common owners incentivizes company executives to reduce competition, or compete less aggressively. This would mean CEOs are willing to place the minority interests of “common owners” above their own personal financial interests, since many are paid in company stock.

Stewardship Codes and Regulatory Guidance

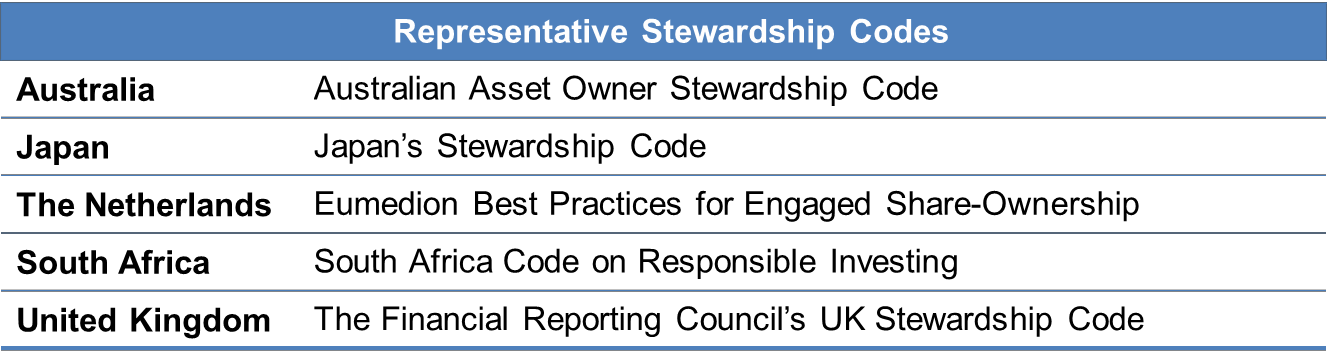

A broad consensus exists among policy makers and asset owners that traditional asset managers should take a serious approach to investment stewardship of client assets. Over the past two decades, public authorities and official sector entities have worked with the private sector to develop corporate governance principles and investment stewardship codes. Stewardship codes and other regulations encourage engagement by institutional investors, and often require asset managers to vote proxies on behalf of their clients.

In the US, the SEC and DoL issued guidance 15 to 20 years ago stating that as fiduciaries, fund managers must vote proxies when doing so is in the best interests of investors. [4]

Globally, we count close to 20 stewardship codes, from the UK to Australia to Japan and more. Additionally, collaborative private-sector forums have created governance principles and stewardship codes in certain jurisdictions lacking official sector codes.

In sum, these codes provide a framework for how asset managers should engage with companies to fulfill their fiduciary duty to asset owners. Calls by some commentators in the debate on common ownership theories to restrict engagement or eliminate proxy voting rights would directly contradict relevant regulations and stewardship codes. Restricting voting would disenfranchise our clients, the asset owners. The result of restricting voting by diversified asset managers could be to entrench the control of company management or to empower short-term actors, both at the expense of long-term value creation.

Voting Patterns Differ Considerably Across Asset Managers

At BlackRock, each proxy ballot item is evaluated on its merits against our publicly-available proxy voting guidelines, in the context of materiality to the company’s long-term financial performance. We believe voting is the ultimate expression of investment stewardship, and that a vote “against” management reflects a failure to make progress through engagement efforts.

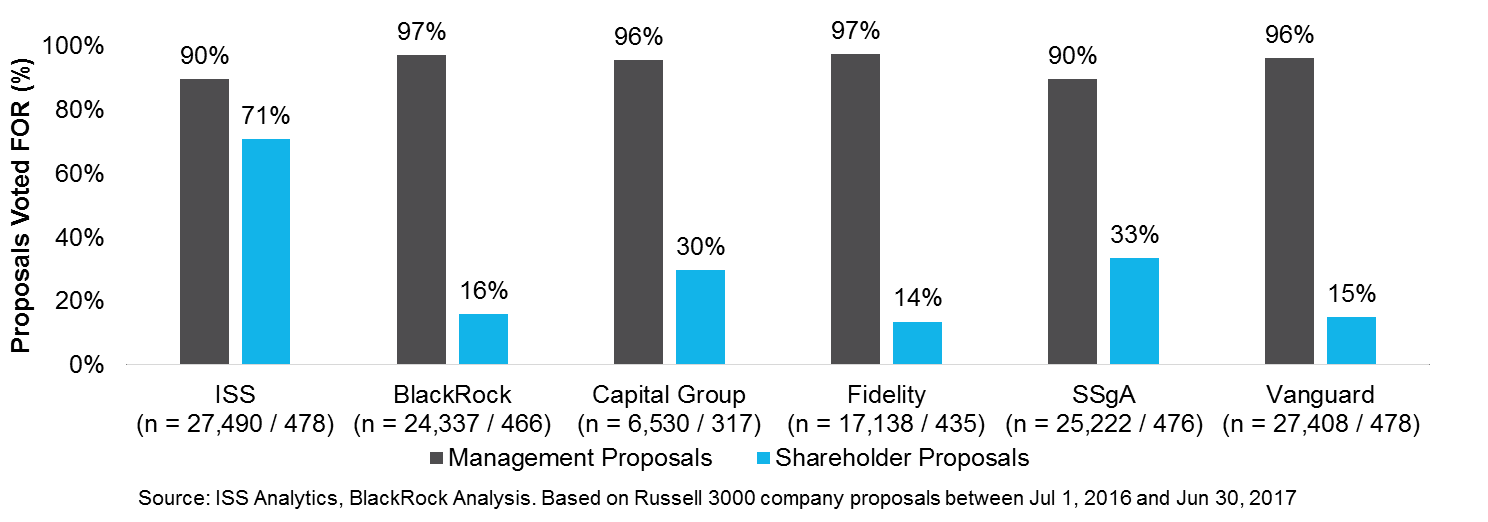

In 2017, 98% of the 28,000 ballot items from companies in the Russell 3000 index were management proposals. Items such as the election of directors or reappointment of auditors, which are generally considered routine items, received more than 95% voting in favor. The exception are “say-on-pay” votes, which often receive less support, especially if proxy advisory firms have recommended “against”. The remaining 2% of ballot items are shareholder proposals; roughly half of these relate to environmental and social issues. As this chart highlights, the voting on these items shows that these managers do not simply follow ISS recommendations and there is no particular pattern of voting across these managers. [5]

Given the focus on competition at this hearing, it is worth noting that the proxy advisory firm ISS uses over 380 management agenda codes to categorize voting items for their proxy reports, and not a single agenda code relates to product pricing.

Some have estimated that proxy advisors influence between 10% and 25% of the vote. [6] This far exceeds the influence of any individual, or even multiple, asset managers. Given the influence of proxy advisors on voting, any study on shareholder voting must incorporate this effect. However, it is notably absent from the papers on common ownership.

Conclusion

To summarize, the investment stewardship ecosystem is complex, involving a diverse set of participants, from asset owners to asset managers, index providers and proxy advisors, compensation consultants, and company boards.

Asset managers provide investors with diversified portfolios to meet their investment needs. As part of their fiduciary duty, they engage with portfolio companies, not to influence pricing, but rather to protect and enhance the long-term value of their clients’ assets.

Engagement by institutional investors plays an important role in the corporate accountability chain and has value not just for shareholders, but for society as a whole.

Thank you.

Moderated Q&A

Panel Q&A discussion included feedback from all panelists. This documents reflects only feedback from Barbara Novick.

Question: There are at least three different kinds of engagement. The first sort is the engagement over high-profile contests, which are high stakes contests with real potential impact on firm value. In those engagements, BlackRock, State Street, and Vanguard often collectively hold the decisive votes. There is a second sort of engagement over market-wide and governance issues. The third sort of engagement is on firm-specific performance and firm-specific pay. Take us inside the room. When you talk about engagement, what are you talking about?

First, let me make it very clear that BlackRock does not act in concert with any other firms on our voting on any topics. When you look at the voting data, our voting is different from that of State Street and Vanguard. There is no concept of aggregating across firms. We do not compare notes beforehand. And our voting records reflect varying views.

Our Stewardship team seeks to advance governance practices in sectors and markets where we have identified an issue that may be material to long-term shareholder value. We think about engaging with companies on behalf of our clients for a number of key reasons. For example, we may engage when we are preparing to vote at the company’s shareholder meeting and need to clarify the information in company disclosures. We may also engage when there has been an event at the company that has impacted its performance or may impact long-term company value. We may engage if our corporate governance risk analysis has identified the company as lagging its peers on environmental, social or governance matters that may impact long-term value.

Another instance in which we might engage is when the company is in a sector or market where there is a thematic governance issue material to shareholder value. Let me give you an example from this year. We announced our engagement priorities earlier this year. We are very transparent about our priorities, and we publish our voting guidelines online, in addition to regular reports about our engagement and voting activities. [7] One of the issues we identified as a priority was board composition and diversity, as diverse boards lead to better decision making.

We engage on diversity with the objective of understanding the board’s approach to achieving diversity of thought. In January 2018, BlackRock’s stewardship team wrote to the nearly 300 companies in the Russell 1000 with fewer than two women on their board. We identified companies based on low gender representation in the boardroom, which we consider a potential signal of weakness in the nominating process. I am pleased to announce that we’ve observed a continued increase of women on boards in the last year. For instance, ISS recently published a study that found that nearly 20% of Russell 3000 directorships are held by women. The nearly two-percentage-point increase over the prior year is the highest increase in the past decade. [8]

This example also showcases BlackRock’s engagement-first approach to investment stewardship, emphasizing direct dialogues with companies. Long-established governance practices can be deeply embedded, and change simply doesn’t happen overnight or as a result

of a single shareholder vote. Board quality remains a focal point of our conversations with many companies.

An industry-specific example is opioids. In light of the risks presented to certain pharmaceutical companies stemming from the opioid epidemic in the US, we have engaged with companies across the pharmaceutical sector about their enterprise risk management practices and anticipated public policy changes that might affect their long-term strategy. [9] For example, we engaged on how companies were addressing these risks to their businesses and complying with existing laws. For those companies that are in the business of manufacturing opioids, many had taken steps to enhance oversight of supply chain risks, had elevated the issue to a board-level risk committee, and had instituted more robust remedial measures.

In terms of how often we meet with individual companies, the answer is that it very much depends on how many of these issues are on the table. We also meet with companies when they request a meeting. Let me provide a few statistics from our 2018 proxy season report, which is publicly available on our website. [10] BlackRock participated in 2,049 company engagements with 1,400 unique companies. We voted in 17,151 meetings across 158,942 proposals in 89 different countries. In the US alone, there were 3,904 meetings voted with 31,265 proposals. Our Investment Stewardship team has 40 people globally. As you can see based on the volume of our engagements, we do not conduct a deep dive into the minutiae and try to manage these companies in these meetings, nor do we discuss product pricing in these meetings. We focus on the board and its role and effectiveness in counseling and overseeing management.

Let me also briefly discuss the topic of disclosure. A recent piece published in the Wall Street Journal by John Bogle suggested that asset managers should provide more transparency on their engagement with companies. [11] I would like to point out that John Bogle rejects all of the proposed remedies except for disclosure. He notes that index funds have been revolutionary for retirement security and undermining retirement security would be a threat to our national interest.

Disclosure is generally a positive, and at BlackRock we embrace transparency. We voluntarily post a lot of information on our stewardship activities to our web page, including: our engagement priorities each year, our voting guidelines, bulletins addressing special topics, actual vote reports by issuer annually, summary statistical reporting on our voting patterns, quarterly and annual reports highlighting engagements undertaken or concluded during the relevant time period, and thought leadership papers called ViewPoints. We are incredibly transparent, and we support raising the bar on transparency industry-wide.

Question: Barbara, you mentioned the impact of your initiatives on gender diversity. Larry Fink has talked in his letter about ESG initiatives and you have talked about firearms. How is it possible to promote these goals and not also have the power to promote anti-competitive goals? Is the reason that BlackRock doesn’t promote anti-competitive goals because you don’t have the power or because you don’t view it to be in your interests?

Keep in mind that we hold minority stakes in companies on behalf of asset owners, and these stakes are generally in single digits. On gender diversity, if we were the only voice out there supporting diversity of thought on boards, it would fall on deaf ears. In contrast, if there is a chorus of voices on an issue, the message then resonates with a company as something important to consider. For example, if you look at the issue of over-boarding—the issue of board directors sitting on an excess number of corporate boards—there has been an increase in engagement over time as more asset owners have spoken up. This is just one example of how more and more asset owners are weighing in on governance issues. We are not seeing this same trend on competition issues; in fact, we are not seeing engagement at all on competition issues.

No single minority shareholder has the control to significantly influence companies on these issues. In fact, the sole participant in the stewardship ecosystem that has the most influence is the proxy advisory firms. It has been estimated that these firms have a 25% influence on say-on-pay. [12] Although this represents multiples of the voting power of any asset manager, the influence of proxy advisory firms has not been accounted for in the common ownership dialogue.

Question: Do interventions by activist investors impose sufficient market discipline where management is lagging to prevent anti-competitive behavior?

We heard earlier this idea that activist voters are cultivating index investors’ votes. In the 2017-2018 proxy year, there were 19 contests voted where an activist had proposed dissident nominees to the Board. To put this in perspective, we voted in favor of about 20% of these and we voted against about 80%. Other firms voted differently, contest by contest. Stewardship and engagement is about hearing the perspectives of all the parties and making a decision in your best judgement to be in the best long-term economic interests of shareholders.

Question: There are different ways investors communicate with firms. Are the people on quarterly earnings calls the same people that are engaging on stewardship issues?

It is important to recognize that earnings calls are open to the public. With that said, different asset managers will have different answers. At BlackRock, our equity assets are 90% index and 10% active. On the index side, there is probably no one on the earnings call focused on these issues. On the active side, it would be a portfolio manager or equity research analyst who has a strong interest in the company who would be on the call.

Question: You have portfolio managers that know a lot about the company and proxy stewardship groups with a broad responsibility to encourage votes. What is the interaction between these two parties?

In many cases, we have holdings that are only in an index portfolio. We manage against so many different indexes that it is likely that we have some holdings in most companies in one of our index portfolios. Where there is overlap with an active holding, our Investment Stewardship team has encouraged the stewardship analysts and active equity analysts to speak with each other, although they are not required to form a consensus opinion. For example, at BlackRock, we allow a split vote in which not all of the shares in BlackRock-managed portfolios are voted the same way. This can occur when an active portfolio manager may have a different view from that of the stewardship team, as it is ultimately the responsibility of the portfolio manager to ensure that ballots are cast in the best long-term economic interest of their investors. Split votes are not just a matter of policy; they can sometimes be a matter of satisfying our fiduciary duties.

In addition to split votes, we estimate that 25% of our equity separate account clients retain their votes, meaning the clients are voting directly and their votes may or may not be aligned with our views. There are also votes we outsource to an independent fiduciary for regulatory reasons, and these votes may differ from our own.

Question: Does the common owner have board representation? To the extent that there are large shareholders who have influence on boards, should the same antitrust concerns that motivate the Clayton Act also bar common ownership?

Traditional asset managers do not nominate directors or put shareholder proposals on a ballot. Most asset managers do not put proposals on the ballot, much less engage in a proxy fight on director elections.

Question: Have discussions about common ownership changed your approach to stewardship?

To date, discussions on common ownership have not chilled our enthusiasm for engagement or voting. There are laws that encourage and may even require us to vote. We think informed voting, which requires engagement, is a sensible approach. If the laws change, we will re-evaluate and follow the new laws. While a lot of time is spent discussing the common ownership remedies, we have fundamental doubts about the underlying models and analysis. We believe the research is much ado about nothing, and there is not in fact a problem. As a result, these proposed remedies are not warranted and we don’t see any reason to change our approach to stewardship.

Question: Do you have any closing thoughts?

I’d like to mention two topics that have not come up yet.

First, diversification is important to investors as diversification plays an important role in mitigating risk by spreading assets across sectors, industries, and companies. It is foundational to modern portfolio theory, and the benefits of it have been recognized by regulators, asset managers, and asset owners alike. [13]

Some of the proponents of common ownership theories have suggested that diversification across sectors is sufficient to protect investors, however, this is not true. Diversification within a sector allows investors to hedge against the idiosyncratic risk of owning one company versus another within a given sector. In any given year, companies within a specific sector may have incongruent performances. To put this in perspective, in 2017, JP Morgan was up 24% while Wells Fargo was up 10%. And this year, in the aerospace industry, Lockheed Martin is down 10% year-to-date, while Boeing is up 17%. [14]

Second, some of the proponents of common ownership theories have claimed that only wealthy people invest in mutual funds, however, this is not true. According to ICI’s data, 100 million individuals own mutual funds, and 56% of households’ mutual fund assets are held in retirement accounts. The data shows that the median household income of mutual fund investors is $100,000. [15] This means half of mutual fund owning households earn less than $100,000 per year. Given that employees of large companies and federal government employees invest in mutual funds as participants in defined contribution plans, the range of incomes and wealth of mutual fund investors is wide.

Finally, I will note that we have a Goldilocks problem. When it comes to investment stewardship, we find that some people believe we do too much and others believe we don’t do enough. I believe investment stewardship is beneficial for shareholders and the efforts of shareholders have had a positive influence on the governance of corporations.

Given the importance of diversification and the importance of investment stewardship, I would advise caution before pursuing the proposed remedies, especially given the flaws in the underlying theory.

Endnotes

1José Azar, Martin C. Schmalz, and Isabel Tecu, Anti-Competitive Effects of Common Ownership (May, 2018), available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2427345 (Airline Paper).(go back)

2There were 29 total quarters in which one of more of the airlines was in bankruptcy. The Airline Paper methodology looked to whether an issuer was 13F reportable as of the last day of each quarter. Because one of the airlines emerged from bankruptcy and became 13F reportable in the same quarter, bankruptcies impacted 28 quarters under their methodology.(go back)

3BlackRock Investment Stewardship, 2018 Priorities, available at https://www.blackrock.com/corporate/about-us/investment-stewardship/voting-guidelines-reports-position-papers#2018-priorities.(go back)

4SEC, Staff Legal Bulletin No. 20, Proxy Voting: Proxy Voting Responsibilities of Investment Advisers and Availability of Exemptions from the Proxy Rules for Proxy Advisory Firms (Jun. 30, 2014), available at https://www.sec.gov/interps/legal/cfslb20.htm; DoL, Field Assistance Bulletin No. 2018-01 (Apr. 23, 2018), available at https://www.dol.gov/agencies/ebsa/employers-and-advisers/guidance/field-assistance-bulletins/2018-01; DoL, Interpretive Bulletin Relating to the Exercise of Shareholder Rights and Written Statements of Investment Policy, Including Proxy Voting Policies or Guidelines (Dec. 29, 2016), available at https://www.gpo.gov/fdsys/pkg/FR-2016-12-29/pdf/2016-31515.pdf.(go back)

5BlackRock, ViewPoint, The Investment Stewardship Ecosystem (Jul. 2018), available at https://www.blackrock.com/corporate/literature/whitepaper/viewpoint-investment-stewardship-ecosystem-july-2018.pdf.(go back)

6See e.g., Nadya Malenko and Yao Shen, Boston College, The Role of Proxy Advisory Firms: Evidence from a Regression-Discontinuity Design (Aug. 2016), available at https://www2.bc.edu/nadya-malenko/Malenko,Shen%20(RFS%202016).pdf (Malenko and Shen paper).(go back)

7These materials can be found at: www.blackrock.com/stewardship.(go back)

8ISS Analytics, “Female CEOs on a Glass Cliff? A Look at Gender Diversity and Company Performance” (Oct. 26, 2018).(go back)

9See case study 6 in our 2017 Americas Q4 report. BlackRock, Investment Stewardship Report: Americas, Q4 2017 (Dec. 31, 2017), available at https://www.blackrock.com/corporate/literature/publication/blk-qtrly-commentary-2017-q4-amers.pdf.(go back)

10BlackRock, BlackRock Investment Stewardship 2018 Annual Report (Aug. 30, 2018), available at https://www.blackrock.com/corporate/literature/publication/blk-annual-stewardship-report-2018.pdf.(go back)

11John C. Bogle, Bogle Sounds a Warning on Index Funds (Nov. 29, 2018), available at https://www.wsj.com/articles/bogle-sounds-a-warning-on-index-funds-1543504551.(go back)

12Malenko and Shen paper at 3399: “We show that ISS recommendations move 25% of say-on-pay votes; this is evidence of rather strong influence.”(go back)

13Nobel Media AB 2014, The Prize in Economics (1990), available at http://www.nobelprize.org/nobel_prizes/economic-sciences/laureates/1990/press.html.(go back)

14Data from Yahoo Finance as of Dec. 4, 2018.(go back)

15Investment Company Institute, 2018 Investment Company Fact Book, Figure 7.2, available at https://www.ici.org/pdf/2018_factbook.pdf.(go back)