Print

PrintBrian Tayan is a Researcher with the Corporate Governance Research Initiative at Stanford Graduate School of Business. This post is based on a recent paper by Mr. Tayan.

Recently, attention has been paid to corporate culture, “tone at the top,” and the impact that these have on organizational outcomes. While corporate leaders and outside observers contend that culture is a critical contributor to employee engagement, motivation, and performance, the nature of this relationship and the mechanisms for instilling the desired values in employee conduct is not well understood.

For example, a survey by Deloitte finds that 94 percent of executives believe that workplace culture is important to business success, and 62 percent believe that “clearly defined and communicated core values and beliefs” are important. Graham, Harvey, Popadak, and Rajgopal (2016) find evidence that governance practices and financial incentives can reinforce culture; however, they also find that incentives can work in opposition to culture, particularly when they “reward employees for achieving a metric without regard to the actions they took to achieve that metric.” According to a participant in their study, “People invariably will do what you pay them to do even when you’re saying something different.”

The tensions between corporate culture, financial incentives, and employee conduct is illustrated by the Wells Fargo cross-selling scandal.

Wells Fargo Culture, Values, and Management

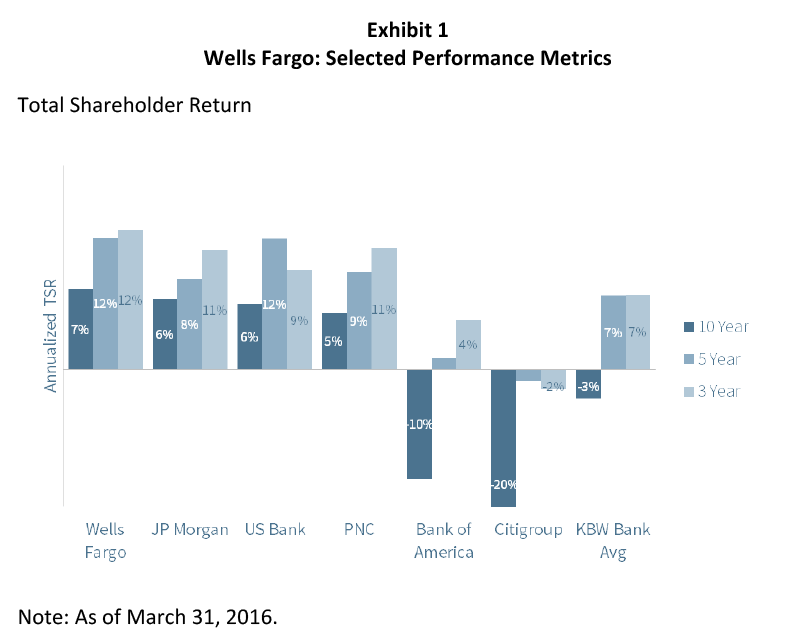

Wells Fargo has long had a reputation for sound management. The company used its financial strength to purchase Wachovia during the height of the financial crisis—forming what is now the third largest bank in the country by assets—and emerged from the ensuing recession largely unscathed, with operating and stock price performance among the top of its peer group (Exhibit 1). Fortune magazine praised Wells Fargo for “a history of avoiding the rest of the industry’s dumbest mistakes.” American Banker called Wells Fargo “the big bank least tarnished by the scandals and reputational crises.” In 2013, it named Chairman and CEO John Stumpf “Banker of the Year.” Carrie Tolstedt, who ran the company’s vast retail banking division, was named the “Most Powerful Woman in Banking.” Wells Fargo ranked 7th on Barron’s 2015 list of the “Most Respected Companies.”

Wells Fargo’s success is built on a cultural and economic model that combines deep customer relations and an actively engaged sales culture. The company’s operating philosophy includes the following elements:

Vision and Values. Wells Fargo’s vision is to “satisfy our customers’ needs, and help them succeed financially.” The company emphasizes that:

Our vision has nothing to do with transactions, pushing products, or getting bigger for the sake of bigness. It’s about building lifelong relationships one customer at a time. … We strive to be recognized by our stakeholders as setting the standard among the world’s great companies for integrity and principled performance. This is more than just doing the right thing. We also have to do it in the right way.

The company takes these statements seriously. According to Stumpf, “[Our vision] is at the center of our culture, it’s important to our success, and frankly it’s been probably the most significant contributor to our long-term performance.” … “If I have any one job here, it’s keeper for the culture.”

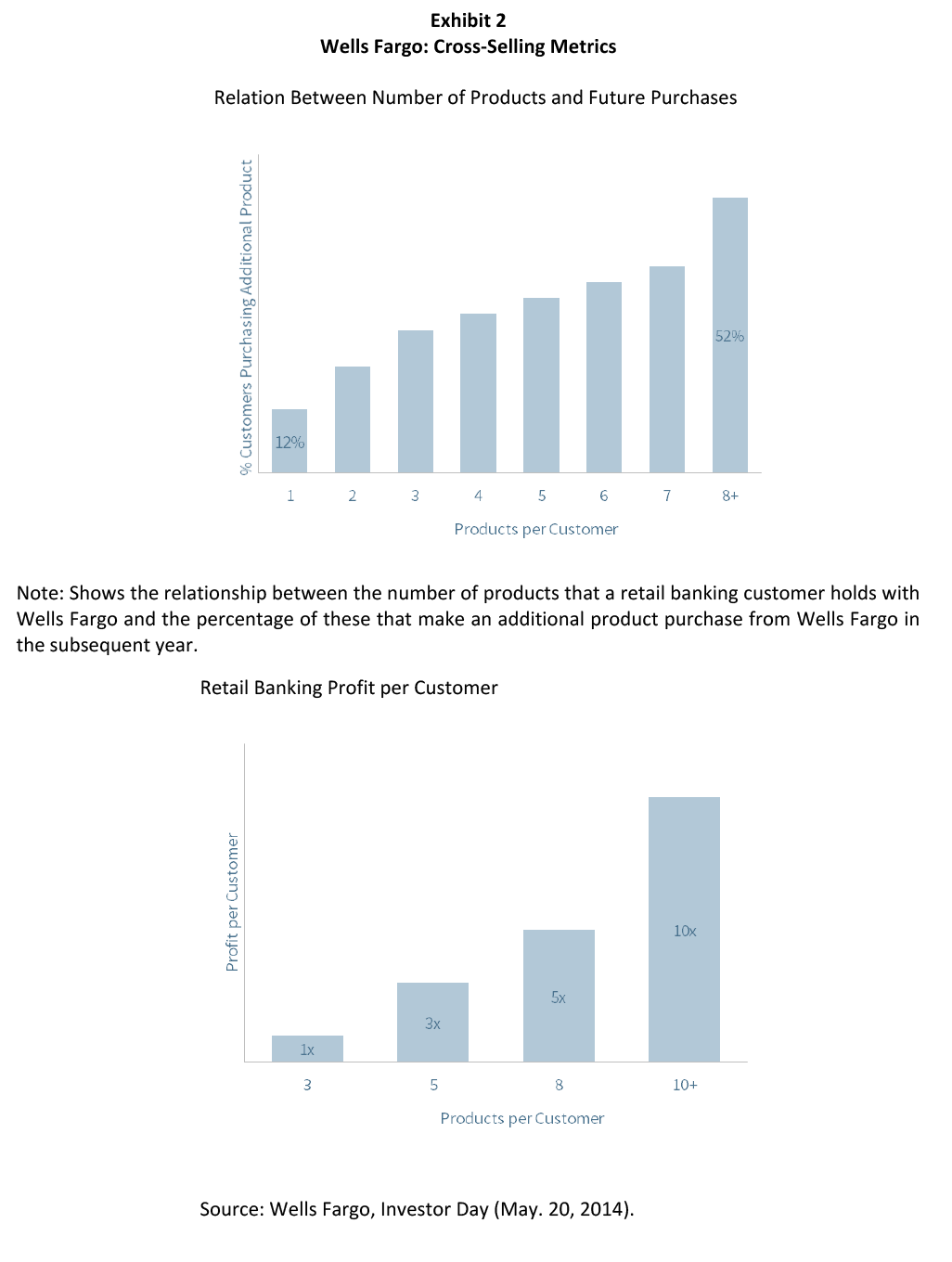

Cross-Selling. The more products that a customer has with Wells Fargo, the more information the bank has on that customer, allowing for better decisions about credit, products, and pricing. Customers with multiple products are also significantly more profitable (Exhibit 2). According to Stumpf:

To succeed at it [cross-selling], you have to do a thousand things right. It requires long-term persistence, significant investment in systems and training, proper team member incentives and recognition, [and] taking the time to understand your customers’ financial objectives.

Conservative Stable Management. Stumpf’s senior management team consisted of 11 direct reports with an average of 27 years of experience at Wells Fargo. Decisions were made collectively. According to former CEO Richard Kovacevich, “No single person has ever run Wells Fargo and no single person probably ever will. It’s a team game here.” Although the company maintains independent risk and oversight mechanisms, all senior leaders are responsible for ensuring that proper practices are embedded in their divisions:

The most important thing that we talk about inside the company right now is that the lever that we have to manage our reputation is to stick to our vision and values. If we are doing things for our customers that are the right things, then the company is going to be in very good shape. … We always consider the reputational impact of the things that we do. There is no manager at Wells Fargo who is responsible for reputation risk. All of our business managers in all of our lines of business are responsible.

Wells Fargo has been listed among Gallup’s “Great Places to Work” for multiple years, with employee engagement scores in the top quintile of U.S. companies.

Cross-Selling Scandal

In 2013, rumors circulated that Wells Fargo employees in Southern California were engaging in aggressive tactics to meet their daily cross-selling targets. According to the Los Angeles Times, approximately 30 employees were fired for opening new accounts and issuing debit or credit cards without customer knowledge, in some cases by forging signatures. “We found a breakdown in a small number of our team members,” a Wells Fargo spokesman stated. “Our team members do have goals. And sometimes they can be blinded by a goal.” According to another representative, “This is something we take very seriously. When we find lapses, we do something about it, including firing people.”

Some outside observers alleged that the bank’s practice of setting daily sales targets put excessive pressure on employees. Branch managers were assigned quotas for the number and types of products sold. If the branch did not hit its targets, the shortfall was added to the next day’s goals. Branch employees were provided financial incentive to meet cross-sell and customer-service targets, with personal bankers receiving bonuses up to 15 to 20 percent of their salary and tellers receiving up to 3 percent.

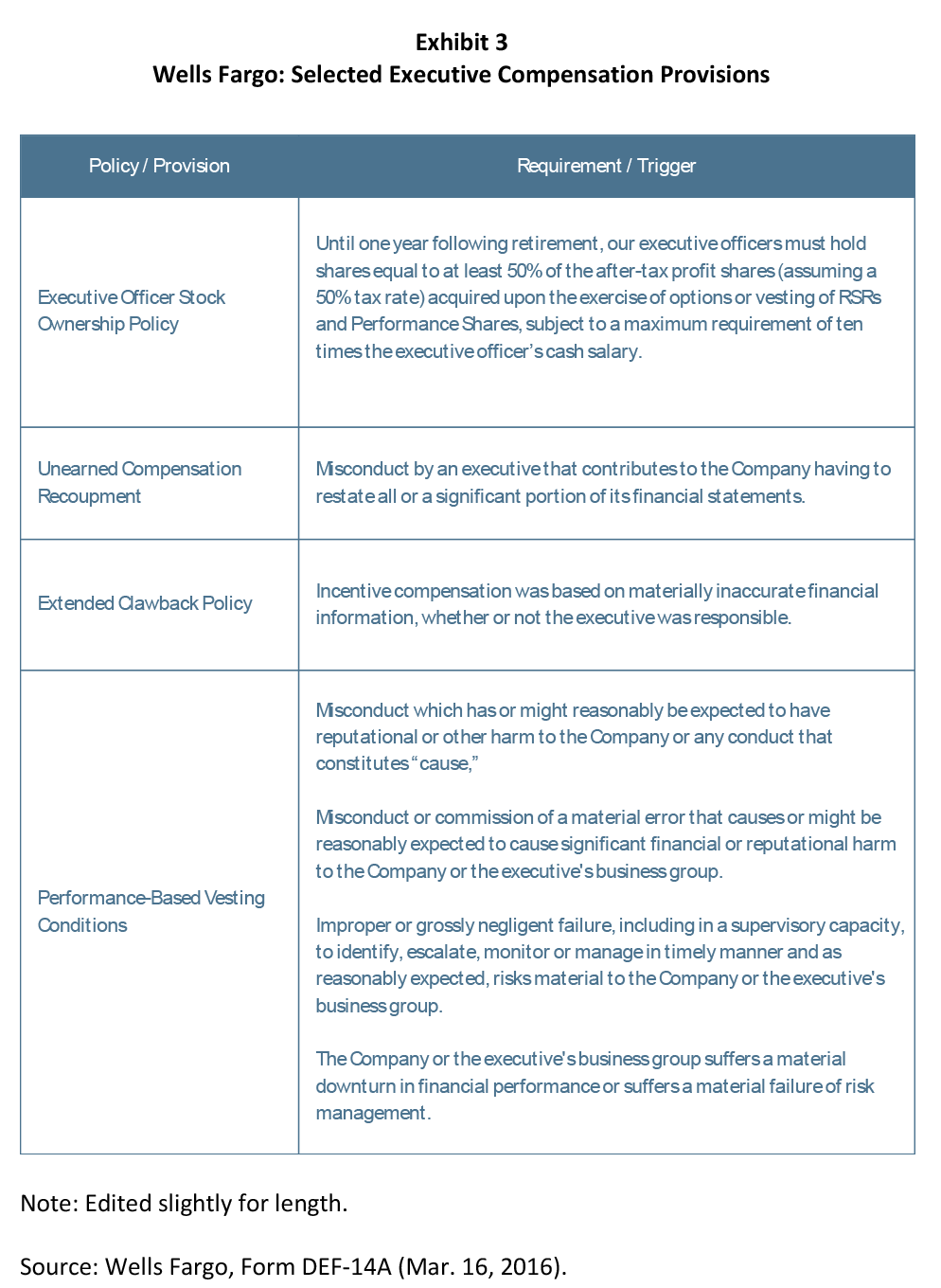

Tim Sloan, at the time chief financial officer of Wells Fargo, refuted criticism of the company’s sales system: “I’m not aware of any overbearing sales culture.” Wells Fargo had multiple controls in place to prevent abuse. Employee handbooks explicitly stated that “splitting a customer deposit and opening multiple accounts for the purpose of increasing potential incentive compensation is considered a sales integrity violation.” The company maintained an ethics program to instruct bank employees on spotting and addressing conflicts of interest. It also maintained a whistleblower hotline to notify senior management of violations. Furthermore, the senior management incentive system had protections consistent with best practices for minimizing risk, including bonuses tied to instilling the company’s vision and values in its culture, bonuses tied to risk management, prohibitions against hedging or pledging equity awards, hold-past retirement provisions for equity awards, and numerous triggers for clawbacks and recoupment of bonuses in the cases where they were inappropriately earned (Exhibit 3). Of note, cross-sales and products-per-household were not included as specific performance metrics in senior executive bonus calculations even though they were for branch-level employees.

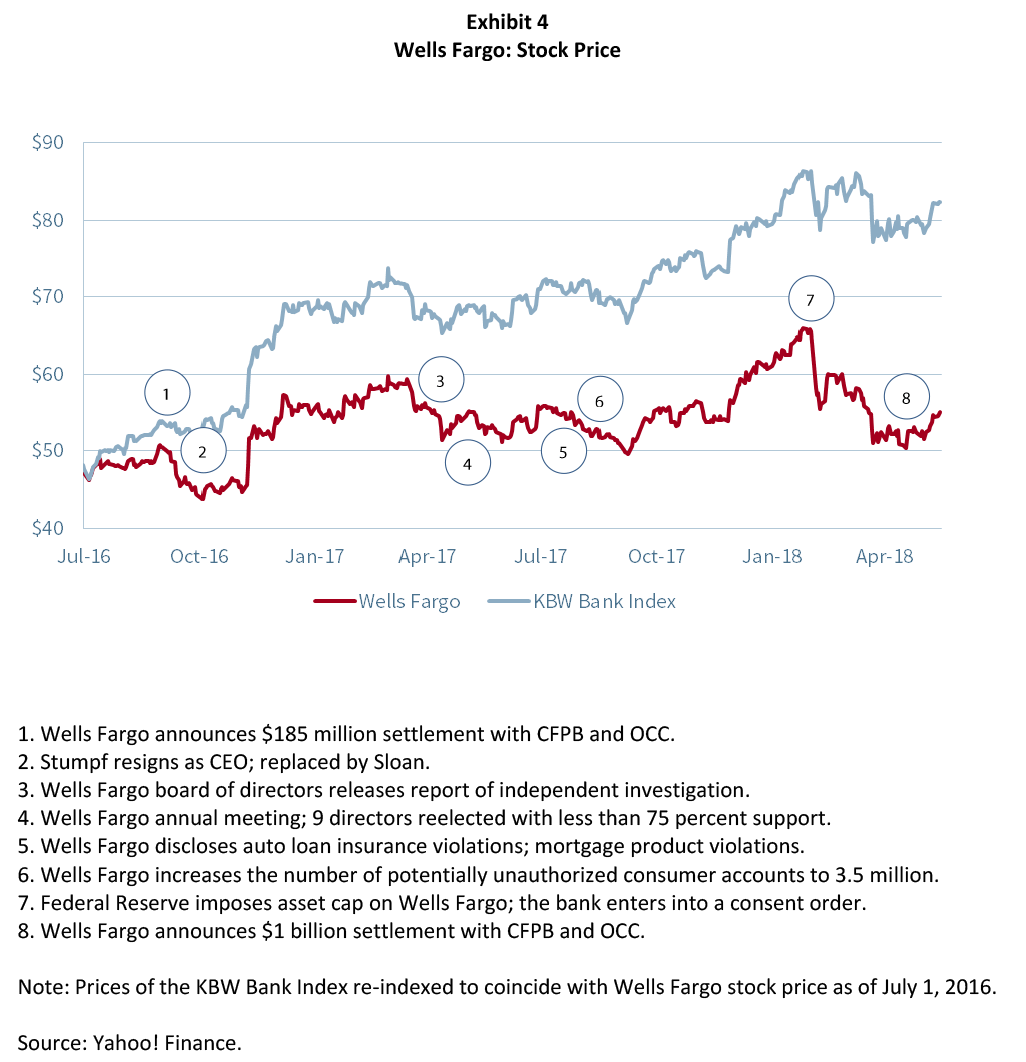

In the end, these protections were not sufficient to stem a problem that proved to be more systemic and intractable than senior management realized. In September 2016, Wells Fargo announced that it would pay $185 million to settle a lawsuit filed by regulators and the city and county of Los Angeles, admitting that employees had opened as many as 2 million accounts without customer authorization over a five-year period. Although large, the fine was smaller than penalties paid by other financial institutions to settle crisis-era violations. Wells Fargo stock price fell 2 percent on the news (Exhibit 4). Richard Cordray, director of the Consumer Financial Protection Bureau, criticized the bank for failing to:

… monitor its program carefully, allowing thousands of employees to game the system and inflate their sales figures to meet their sales targets and claim higher bonuses under extreme pressure. Rather than put its customers first, Wells Fargo built and sustained a cross-selling program where the bank and many of its employees served themselves instead, violating the basic ethics of a banking institution including the key norm of trust.

A Wells Fargo spokesman responded that, “We never want products, including credit lines, to be opened without a customer’s consent and understanding. In rare situations when a customer tells us they did not request a product they have, our practice is to close it and refund any associated fees.” In a release, the banks said that, “Wells Fargo is committed to putting our customers’ interests first 100 percent of the time, and we regret and take responsibility for any instances where customers may have received a product that they did not request.”

The bank announced a number of actions and remedies, several of which had been put in place in preceding years. The company hired an independent consulting firm to review all account openings since 2011 to identify potentially unauthorized accounts. $2.6 million was refunded to customers for fees associated with those accounts. 5,300 employees were terminated over a five-year period. Carrie Tolstedt, who led the retail banking division, retired. Wells Fargo eliminated product sales goals and reconfigured branch-level incentives to emphasize customer service rather than cross-sell metrics. The company also developed new procedures for verifying account openings and introduced additional training and control mechanisms to prevent violations.

Nevertheless, in the subsequent weeks, senior management and the board of directors struggled to find a balance between recognizing the severity of the bank’s infractions, admitting fault, and convincing the public that the problem was contained. They emphasized that the practice of opening unauthorized accounts was confined to a small number of employees: “99 percent of the people were getting it right, 1 percent of people in community banking were not. … It was people trying to meet minimum goals to hang on to their jobs.” They also asserted that these actions were not indicative of the broader culture:

I want to make very clear, that we never directed nor wanted our team members to provide products and services to customers that they did not want. That is not good for our customers and that is not good for our business. It is against everything we stand for as a company.

If [employees] are not going to do the thing that we ask them to do—put customers first, honor our vision and values—I don’t want them here. I really don’t… The 1 percent that did it wrong, who we fired, terminated, in no way reflects our culture nor reflects the great work the other vast majority of the people do. That’s a false narrative.

They also pointed out that the financial impact to the customer and the bank was extremely limited. Of the 2 million potentially unauthorized accounts, only 115,000 incurred fees; those fees totaled $2.6 million, or an average of $25 per account, which the bank had refunded. Affected customers did not react negatively:

We’ve had very, very low volumes of customer reaction since that happened. … We sent 115,000 letters out to people saying that you may have a product that you didn’t want and here is the refund of any fees that you incurred as a result of it. And we got very little feedback from that as well.

The practice also did not have a material impact on the company’s overall cross-sell ratios, increasing the reported metric by a maximum of 0.02 products per household. According to one executive, “The story line is worse than the economics at this point.”

Nevertheless, although the financial impact was trivial, the reputational damage proved to be enormous. When CEO John Stumpf appeared before the U.S. Senate, the narrative of the scandal changed significantly. Senators criticized the company for perpetuating fraud on its customers, putting excessive pressure on low-level employees, and failing to hold senior management responsible. In particular, they were sharply critical that the board of directors had not clawed back significant pay from John Stumpf or former retail banking head Carrie Tolstedt, who retired earlier in the summer with a pay package valued at $124.6 million. Senator Elizabeth Warren of Massachusetts told Stumpf:

You know, here’s what really gets me about this, Mr. Stumpf. If one of your tellers took a handful of $20 bills out of the cash drawer, they’d probably be looking at criminal charges for theft. They could end up in prison. But you squeezed your employees to the breaking point so they would cheat customers and you could drive up the value of your stock and put hundreds of millions of dollars in your own pocket. And when it all blew up, you kept your job, you kept your multimillion dollar bonuses and you went on television to blame thousands of $12-an-hour employees who were just trying to meet cross-sell quotas that made you rich. This is about accountability. You should resign. You should give back the money that you took while this scam was going on and you should be criminally investigated by both the Department of Justice and the Securities and Exchange Commission.

Following the hearings, the board of directors announced that it hired external counsel Shearman & Sterling to conduct an independent investigation of the matter. Stumpf was asked to forfeit $41 million and Tolstedt $19 million in outstanding, unvested equity awards. It was one of the largest clawbacks of CEO pay in history and the largest of a financial institution. The board stipulated that additional clawbacks might occur. Neither executive would receive a bonus for 2016, and Stumpf agreed to forgo a salary while the investigation was underway.

Two weeks later, Stumpf resigned without explanation. He received no severance and reiterated a commitment not to sell shares during the investigation. The company announced that it would separate the chairman and CEO roles. Tim Sloan, chief operating officer, became CEO. Lead independent director Stephen Sanger became nonexecutive chairman; and Elizabeth Duke, director and former Federal Reserve governor, filled a newly created position as vice chairman.

Independent Investigation Report

In April 2017, the board of directors released the results of its independent investigation which sharply criticized the bank’s leadership, sales culture, performance systems, and organizational structure as root causes of the cross-selling scandal.

Performance and Incentives. The report faulted the company’s practice of publishing performance scorecards for creating “pressure on employees to sell unwanted or unneeded products to customers and, in some cases, to open unauthorized accounts.” Employees “feared being penalized” for failing to meet goals, even in situations where these goals were unreasonably high:

In many instances, community bank leadership recognized that their plans were unattainable. They were commonly referred to as 50/50 plans, meaning that there was an expectation that only half the regions would be able to meet them.

The head of strategic planning for the community bank was quoted as saying that the goal-setting process is a “balancing act” and recognized that “low goals cause lower performance and high goals increase the percentage of cheating.”

The report also blamed management for, “tolerating low quality accounts as a necessary by-product of a sales-driven organization.”:

Management characterized these low quality accounts, including products later canceled or never used and products that the customer did not want or need, as “slippage” and believed a certain amount of slippage was the cost of doing business in any retail environment.

The report faulted management for failing to identify “the relationship between the goals and bad behavior [even though] that relationship is clearly seen in the data. As sales goals became more difficult to achieve, the rate of misconduct rose.” Of note, the report found that “employees who engaged in misconduct most frequently associated their behavior with sales pressure, rather than compensation incentives.”

Organizational structure. In addition, the report asserted that “corporate control functions were constrained by [a] decentralized organizational structure” and described the corporate control functions as maintaining “a culture of substantial deference to the business units.”

Group risk leaders “took the lead in assessing and addressing risk within their business units” and yet were “answerable principally to the heads of their businesses.” For example, the community bank group risk officer reported directly to the head of the community bank and only on a dotted-line basis to the central chief risk officer. As a result,

Risk management … generally took place in the lines of business, with the business people and the group risk officers and their staffs as the “first line of defense.”

John Stumpf believed that this system “better managed risk by spreading decision-making and produced better business decisions because they were made closer to the customer.”

The board report also criticized control functions for not understanding the systemic nature of sales practice violations:

Certain of the control functions often adopted a narrow “transactional” approach to issues as they arose. They focused on the specific employee complaint or individual lawsuit that was before them, missing opportunities to put them together in a way that might have revealed sales practice problems to be more significant and systemic than was appreciated.

The chief operational risk officer:

did not view sales practices or compensation issues as within her mandate, but as the responsibility of the lines of businesses and other control functions (the law department, HR, audit and investigations). She viewed sales gaming as a known problem that was well-managed, contained and small.

The legal department focused:

principally on quantifiable monetary costs—damages, fines, penalties, restitution. Confident those costs would be relatively modest, the law department did not appreciate that sales integrity issues reflected a systemic breakdown.

Human resources:

had a great deal of information recorded in its systems, [but] it had not developed the means to consolidate information on sales practices issues and to report on them.

The internal audit department:

generally found that processes and controls designed to detect, investigate and remediate sales practice violations were effective at mitigating sales practices-related risks. … As a general matter, however, audit did not attempt to determine the root cause of unethical sales practices.

The report concluded that:

while the advisability of centralization was subject to considerable disagreement within Wells Fargo, events show that a strong centralized risk function is most suited to the effective management of risk.

Leadership. Furthermore, the board report criticized CEO John Stumpf and community banking head Carrie Tolstedt for leadership failures.

According to the report, Stumpf did not appreciate the scope and scale of sales practices violations: “Stumpf’s commitment to the sales culture … led him to minimize problems with it, even when plausibly brought to his attention.” For example, he did not react negatively to learning that 1 percent of employees were terminated in 2013 for sales practices violations: “In his view, the fact that 1 percent of Wells Fargo employees were terminated meant that 99 percent of employees were doing their jobs correctly.” Consistent with this, the report found that Stumpf “was not perceived within Wells Fargo as someone who wanted to hear bad news or deal with conflict.”

The report acknowledged the contribution that Tolstedt made to the bank’s financial performance:

She was credited with the community bank’s strong financial results over the years, and was perceived as someone who ran a “tight ship” with everything “buttoned down.” Community bank employee engagement and customer satisfaction surveys reinforced the positive view of her leadership and management. Stumpf had enormous respect for Tolstedt’s intellect, work ethic, acumen and discipline, and thought she was the “most brilliant” community banker he had ever met.

At the same time, it was critical of her management style, describing her as “obsessed with control, especially of negative information about the community bank” and faulting her for maintaining “an ‘inner circle’ of staff that supported her, reinforced her views, and protected her.” She “resisted and rejected the near-unanimous view of senior regional bank leaders that the sales goals were unreasonable and led to negative outcomes and improper behavior.”

Tolstedt and certain of her inner circle were insular and defensive and did not like to be challenged or hear negative information. Even senior leaders within the Community Bank were frequently afraid of or discouraged from airing contrary views.

Stumpf “was aware of Tolstedt’s shortcomings as a leader but also viewed her as having significant strengths.” … He “was accepting of Tolstedt’s flaws in part because of her other strengths and her ability to drive results, including cross-sell.”

Board of Directors. Finally, the report evaluated the process by which the board of directors oversaw sales-practice violations and concluded that “the board was regularly engaged on the issue; however, management reports did not accurately convey the scope of the problem.” The report found that:

Tolstedt effectively challenged and resisted scrutiny from both within and outside the community bank. She and her group risk officer not only failed to escalate issues outside the community bank, but also worked to impede such escalation. … Tolstedt never voluntarily escalated sales practice issues, and when called upon specifically to do so, she and the community bank provided reports that were generalized, incomplete, and viewed by many as misleading.

Following the initial Los Angeles Times article highlighting potential violations, “sales practices” was included as a “noteworthy risk” in reports to the full board and the board’s risk committee. Beginning in 2014 and continuing thereafter, the board received reports from the community bank, the corporate risk office, and corporate human resources that “sales practice issues were receiving scrutiny and attention and, by early 2015, that the risks associated with them had decreased.”

Board members expressed the view that “they were misinformed” by a presentation made to the risk committee in May 2015 that underreported the number of employees terminated for sales-practice violations, that reports made by Tolstedt to the committee in October 2015 “minimized and understated” the problem, and that metrics in these reports suggested that potential abuses were “subsiding.”

Following the lawsuit by the Los Angeles City Attorney, the board hired a third-party consultant to investigate sales practices and conduct an analysis of potential customer harm. The board did not learn the total number of employees terminated for violations until it was included in the settlement agreement in September 2016.

Wells Fargo response. With the release of the report, Wells Fargo announced a series of steps to centralize and strengthen control functions. The board also announced that it would claw back an additional $47.3 million in outstanding stock option awards from Tolstedt and an additional $28 million in previously vested equity awards from Stumpf.

Long-Term Overhang

The board report and related actions did not put an end to shareholder and regulatory pressure. At the company’s 2017 annual meeting, 9 of the company’s 15 directors received less than 75 percent support and 4 received less than 60 percent, including board chairman Stephen Sanger (56 percent), head of the risk committee Enrique Hernandez (53 percent), head of the corporate responsibility committee Federico Peña (54 percent), and Cynthia Milligan who headed the credit committee (57 percent). The bank subsequently announced the resignations of 6 directors, including Sanger, who was replaced by Elizabeth Duke as board chair.

Wells Fargo continued its efforts to reexamine all aspects of its business. In August 2017, the company increased its estimate of the number of potentially unauthorized consumer accounts to 3.5 million and issued an additional $2.8 million in refunds. The bank also announced that it identified sales practice violations in both its auto and mortgage lending divisions. In February 2018, citing “widespread consumer abuses,” the Federal Reserve Board took the unprecedented action of placing a strict limit on the company’s asset size, forbidding the bank from growing past the $1.95 trillion in assets it had at year end until it demonstrated an improvement in corporate controls. According to Federal Reserve Board Chair Janet Yellen:

We cannot tolerate pervasive and persistent misconduct at any bank and the consumers harmed by Wells Fargo expect that robust and comprehensive reforms will be put in place to make certain that the abuses do not occur again. The enforcement action we are taking today will ensure that Wells Fargo will not expand until it is able to do so safely and with the protections needed to manage all of its risks and protect its customers.

In April 2018, the bank agreed to a $1 billion settlement with the Consumer Financial Protection Bureau and the Office of the Comptroller of the Currency to resolve auto and mortgage lending violations. Two weeks later it agreed to pay $480 million to settle a securities class action lawsuit over cross-selling. In December 2018, the company settled with 50 state attorneys general to resolve civil claims for cross-selling, auto lending, and mortgage lending violations and agreed to pay $575 million.

Why This Matters

- The Wells Fargo compensation system emphasized cross-selling as a performance metric for awarding incentive pay to employees. The company also published scorecards that ranked individual branches on sales metrics, including cross-selling. Was the company wrong to use cross-selling as a metric in its incentive systems? Would the program have worked better if structured differently? The independent report suggests that employee pressure was a greater contributor to misconduct than financial incentives. Is this assessment correct?

- Branch-level employees were incentivized to increase products per household but the senior-executive bonus system did not include this metric. Did this disconnect contribute to a failure to recognize the problem earlier?

- Wells Fargo prides itself on its vision and values and culture. By several measures, these have been highly beneficial to the company’s performance. What factors should senior executives consider to ensure that compensation and performance systems encourage the achievement of company objectives without compromising culture?

- The dollars involved in the Wells Fargo cross-selling scandal were small (less than $6 million in direct fees) but the reputational damage to the bank was massive. How can a company prepare against problems that do not seem to be “material” in a financial sense but ultimately have a material impact on the business and its reputation?

- The independent investigation concludes that “a strong centralized risk function is most suited to the effective management of risk.” Is this conclusion correct? What steps can executives in a decentralized organization take to minimize gaps in oversight without creating unnecessary bureaucracy?

- The Wells Fargo cross-selling scandal highlights the challenge of a high-performing executive whose behavior ultimately does not align with company values. How much autonomy should high-performing executives be afforded? How can a company balance autonomy and accountability?

- The independent investigation largely exonerates the Wells Fargo board of directors. How much blame does the board deserve? What could it have done differently to prevent the cross-selling issue from snowballing?

- Wells Fargo had the elements in place of a properly functioning governance system, including risk management, audit, legal, and human resources. Furthermore, each of these groups was—at least to some degree—aware of sales practice violations in the consumer bank. And yet no one recognized the systemic nature of the problem or took the necessary steps to address it. How can a company gauge whether its governance system is effective in identifying and mitigating risk?

The complete paper is available for download here.