Print

PrintEthan Klingsberg and Paul Tiger are partners and Andrea Basham is counsel at Freshfields Bruckhaus Deringer US LLP. This post is based on a Freshfields memorandum by Mr. Klingsberg, Mr. Tiger, Ms. Basham and Tomas Rua.

Amid the growing economic fallout of the COVID-19 pandemic, the White House’s top economic adviser, Larry Kudlow, signaled earlier this month that the Trump Administration was considering taking equity stakes in coronavirus-impacted companies as a condition to providing economic assistance—“equity for a bailout” in the common parlance. Though contrary to established conservative orthodoxy, which has traditionally eschewed government ownership of private companies, President Trump was quick to publicly endorse the idea, and this concept has now been authorized under the economic stimulus package passed by Congress and signed into law by the President on March 27. Of note, the Coronavirus Aid, Relief and Economic Security Act (the “CARES Act”) includes a $500 billion appropriation for the Treasury Department to provide “loans, loan guarantees and other investments” to states, municipalities and certain eligible companies, including, among others, passenger air carriers, cargo air carriers and “businesses critical to maintaining national security.” In the case of any passenger air carrier, cargo air carrier or “business critical to maintaining national security” that has publicly listed securities, the CARES Act requires the Treasury Department to receive warrants or other equity interests in connection with extending any loan or loan guarantee. In addition, while disbursements under the CARES Act are subject to oversight by a special committee of the Congress as well as an inspector general to be appointed by the President and confirmed by the Senate, the Secretary of the Treasury (and therefore Mr. Trump) nonetheless has significant discretion to structure aid and we believe in some cases—even where not required by the CARES Act—the Administration may condition any aid on receiving preferred stock, warrants, options and/or other equity instruments.

With the passage of the CARES Act, boards of prospective aid recipients should begin familiarizing themselves with the implications of issuing equity to the U.S. government in exchange for aid or a bailout. Regardless of the size of any government equity investment, a pristine board process will be a priority due to the high profile and extraordinary nature of such a transaction and the risk that it may appear to be a sweetheart deal for the government in hindsight (see, e.g., the lawsuits (albeit ultimately unsuccessful and against the government, rather than the issuer) following the 2008-09 financial crisis that were largely premised on the allegation that AIG issued equity to the government at too low a valuation).

The board will need to be fully engaged and well-informed, and minutes should be detailed enough to facilitate a director’s ability to explain the foundations for decision-making at a future deposition. Despite time, governmental and market pressures, this is not a transaction to execute without a firm foundation for the fulfillment of the duty of care.

The key issues for the board to consider are:

How to value the company and what are the company’s liquidity needs?

These are critical questions and the answers will require management to revisit, with the board, the internal forecasts for the company. This will be a stressful undertaking in view of macro, industry-wide and internal uncertainties and the dynamism of the current environment. Management may need to resort to probability-weighting of different scenarios. Consultation with outside experts is a good way to help with this exercise. Formal “fairness opinions” are unlikely to be available for a minority investment, but that does not mean that expert analysis of the company’s prospects and of the valuation implications of these prospects should not be in the record of the board’s deliberations. At the end of the day, a good-faith effort to assess future financial prospects, including liquidity and earnings, is the best way to insulate the board from liability. Throwing up one’s hands amid the crisis and sighing, “Who knows?,” is not an acceptable way to make these fundamental assessments.

What alternatives are available?

In addition to understanding what is available from the banking and financial sponsor sector, boards should take into account the pool of strategic companies with significant amounts of excess cash that have an interest in keeping their eco-systems functional and therefore may be open to making an investment. Although likely not an option for some distressed companies, directors would be well-served to ask about outreach to these cash-rich mega-caps and other financing sources. Directors need to take into account, however, that an equity investment from one of these strategic corporate investors may face antitrust delays unless the investor is willing to take non-voting securities and forgo governance rights.

Is the transaction triggering not only dilution, but also a sale of control?

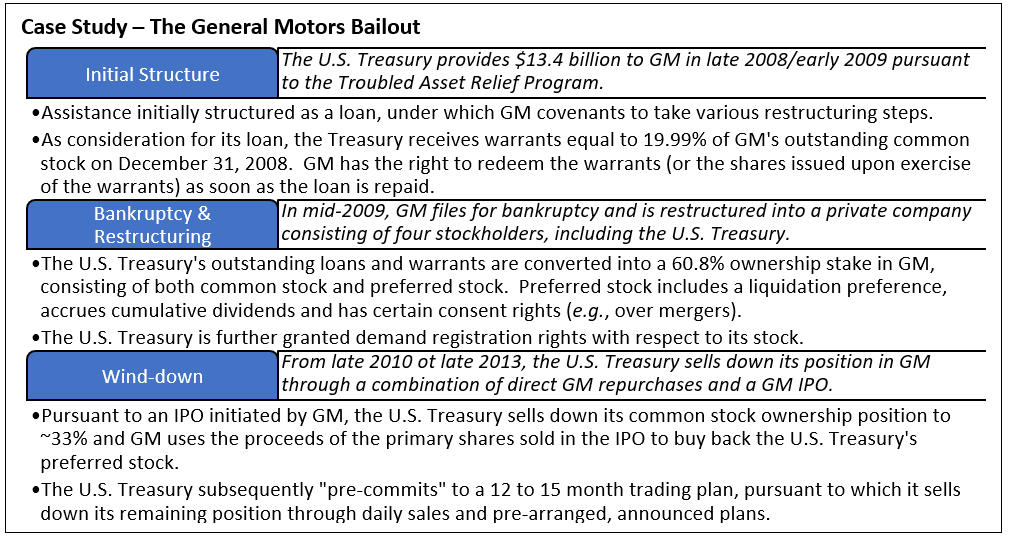

- The initial Troubled Asset Relief Program investments in 2008-09 (see below Case Study—The General Motors Bailout) took the form of non-voting preferred stock and/or warrants, which do not carry any voting power unless and until exercised. Whether the Trump Administration will take a different tact remains to be seen, but we believe that adherence to the 2008-09 model is likely. Indeed, where the CARES Act contemplates—and in fact requires—the government to receive equity to provide aid (i.e., in the case of publicly traded passenger air carriers, cargo air carriers and “businesses critical to maintaining national security”), it provides that “The Secretary shall not exercise voting power with respect to any shares of common stock [so] acquired.” We also expect that, based on precedent, the U.S. government will agree to limit transfers of any common stock issuable upon the conversion of preferred stock or the exercise of warrants so that any such transfer does not result in any single holder, together with its affiliates, having beneficial ownership of more than a reasonable percentage of the outstanding common stock, such as 10%.

- Avoiding any grant of voting power preserves value for the existing stockholders by not transferring actual or negative control or creating a large bloc of voting power that may be sold to a less friendly holder down the road.

- In addition, limiting the government to a non-voting position may help mitigate involvement by the government in the company’s business.

- Alternatively, to the extent the government seeks to acquire voting securities that it intends to vote, the board should consider pushing for an arrangement, through a trust or undertakings, that neuters the government’s voting power—g., by requiring shares to be voted in proportion to the votes of the broader stockholder base—thereby eliminating the potential for conflicts of interest between the government and stockholders.

- In addition, whether as part of the certificate of designation for a preferred security or a separate undertaking, the government may require control rights, such as a veto over buybacks and dividends, or other strategic decisions relating to allocation of capital, M&A, executive compensation and board and management composition. The CARES Act also imposes certain mandatory restrictions on businesses receiving aid, which are described in further detail below. Giving up control over these matters must be weighed carefully by the directors. Control over these matters is a valuable asset of the corporation and there may be questions about the government’s ability to be a responsible caretaker of these rights.

What are the execution risks and potential unforeseen impediments?

Is an equity issuance permitted under the company’s governing documents?

Directors should confirm:

- Whether sufficient shares of stock are authorized for issuance in the company’s existing charter.

- Whether creation of another class of stock (e., preferred stock) would be necessary, whether doing so would be permitted under the company’s existing charter absent a charter amendment and, if not, what work-arounds would be available through contractual or trust arrangements.

- Whether amendment of an existing stockholder rights plan (aka a “poison pill”) would be necessary.

Is stockholder approval required under either the company’s charter or stock exchange rules?

Companies listed on the NYSE or on NASDAQ are generally required to obtain stockholder approval prior to issuing 20% or more of their pre-issuance outstanding common stock or voting power in a private offering. Both NYSE and NASDAQ provide an exception to the stockholder approval requirement, however, if (a) the delay necessary to secure the stockholder approval would seriously jeopardize the financial viability of the company and (b) reliance by the company on this exception is expressly approved by the audit committee of the board. A company seeking to make use of this exception must follow the notice and approval rules of the applicable exchange and approval can typically be obtained relatively quickly if the requirements are met. A number of companies in the 2008 financial crisis availed themselves of this exception in connection with similar investments, and we would expect companies in the current environment to again utilize it, particularly if they are distressed enough to require an equity investment exceeding 20% of their currently outstanding common stock. Of course, the U.S. government may elect to also invest in non-voting securities, which could permit it to invest in more than 20% of a company without subjecting the issuance to a stockholder vote or requiring reliance on the financial viability exemption. As a practical matter, however, a company may wish to use the 20% threshold as one argument to limit the government’s equity investment in these circumstances.

Will any obligations be triggered under material contracts?

In fulfilling its duty of care in approving the investment, the board should understand if any of the company’s material contracts contain consent or termination rights relating to changes in ownership—particularly if a significant, controlling stake is contemplated. Additionally, the board should confirm whether the company’s loan agreements contain negative covenants that might be implicated. Issuing non-voting stock could avoid tripping certain of these restrictions, but obtaining a third party consent may be easier than negotiating with the Trump Administration.

Is action required under any stockholder arrangements?

Companies with significant stockholders—whether financial or strategic, and at private or public companies—will want to carefully review any stockholders’ agreements and related arrangements to ensure no consent or anti-dilution protections are implicated or risk interfering with the company’s ability to act quickly to issue the equity and accept the other bailout funds.

What will be the interplay between this investment and the growing number of non-U.S. national security and foreign investment regimes that may apply to the company?

For those companies with significant operations outside the U.S., directors should be mindful of foreign national security regime filing requirements—the equivalent of CFIUS in foreign jurisdictions. Additionally, the board should understand that post-closing, new acquisitions by the company may come under greater scrutiny under foreign national security regimes given the U.S. government’s ownership stake.

What restrictions will U.S. law impose on businesses receiving aid?

Under the CARES Act, for so long as a company has a U.S. government loan or loan guarantee outstanding and for twelve months thereafter, the company may not engage in buybacks or pay dividends or make other capital distributions in respect of its common stock. During this period, the company must also cap executive compensation (including compensation paid in shares, cash or other financial benefits) such that if an officer or employee’s total 2019 compensation was (a) more than $425,000 (other than for certain unionized employees), he or she does not receive total compensation during any 12 consecutive months exceeding what he or she received in 2019 or receive severance pay exceeding two times his or her 2019 compensation, or (b) more than $3,000,000, he or she does not receive total compensation during any 12 consecutive months exceeding the sum of (i) $3,000,000 and (ii) 50% of the amount by which his or her 2019 compensation exceeded $3,000,000. Separately, any company receiving aid must maintain its employment levels as of March 24, 2020 until September 30, 2020 to the extent practicable and in no case reduce such levels by more than 10%.

How will the government exit its ownership position?

As we saw in 2008 and 2009, when the U.S. government took equity stakes in companies in the bank and auto industries, its goal was not necessarily to be a long-term investor in those companies. We expect companies to impose restrictions on the government that would limit private transfers both to competitors and of significant ownership percentages to a one or more affiliated purchasers, so an exit through public resales is likely to be the government’s most viable option. Accordingly, any company in which the U.S. government invests a significant amount is likely to have to grant the U.S. government registration rights to facilitate the government’s eventual exit either in part or in whole, and those registration rights are likely to include (as in the case of General Motors) the right of the government to demand not only registration but also the ability to require the company to facilitate underwritten offerings of its securities. This should be in the company’s interest as a registered underwritten offering presents an opportunity for the company to manage an orderly exit. Without registration rights, the government will not be able to sell the restricted securities it receives pursuant to a private financing for at least six months. After the six-month mark, it can only sell securities if the company is current in complying with its filing requirements. Note that the recent SEC accommodations permitting companies to delay filings of quarterly and annual reports due to current market conditions will permit a company to be considered “current” notwithstanding a delay (assuming the company ultimately files the report prior to the expiration of the accommodation period). In addition, if the government is considered an “affiliate” of the issuer (e.g., due to representation on the board or magnitude of voting power), the government will also be subject to manner of sale and volume limitations on the amount of securities it can sell over any three-month period. We expect that the government will be transparent with the market about its exit plans similar to how it announced its intentions to sell GM stock between 2010 and 2013, in part to avoid surprises that could result in negative fluctuations in a company’s stock price.

Should creditors be considered as part of a board’s decision-making process?

Generally, if boards are fulfilling their duty of care by having a firm foundation to determine that the decision to issue equity to the government in a transaction is in the best interests of the company and its stockholders, they should be insulated from any exposure for breach of a duty to creditors under “zone of insolvency” doctrines. To the extent such doctrines exist, the advice is the same as for satisfaction of the duty of care as described above.

Can directors take other stakeholders into account?

Many states have implemented constituency statutes, which permit directors to look beyond maximizing stockholder value and focus on the protection of the interests of other constituencies materially impacted by the company, including employees, customers and local communities. For states without constituency statutes, including Delaware, boards may consider the broader interests of stakeholders to the extent the board has a reasonable foundation for a good faith belief that doing so will result in the creation of value for existing stockholders. Again, this is an area where management has to do its homework, together with outside experts where available, to build a record for the board that protecting these other constituencies will enhance the value of the stock at least in the long-term, if not in the short-term.

How and when will the dilution, execution risks and other implications of the government’s investment be explained to stockholders and other constituencies?

- This is where the hard work on building a strong foundation for satisfaction of the duty of care can help pay off. The board and the IR function should be in sync on the plans for the public explanation of the bases for the government’s investment, including explanations of the underlying financial and liquidity drivers, why the board believed that superior alternatives were not available, and what the impact of the investment will be on stockholders and other constituencies.

- Companies should be mindful that any information insiders have about a potential equity investment by the government is likely to be considered “material non-public information” under SEC rules, which accordingly would subject anyone who trades while in possession of that information to potential insider trading liability. Accordingly, companies should as a formal matter prohibit directors, officers and other employees in the know from trading during the pendency of any negotiations with the government and should consider a formal company-wide blackout in accordance with its insider trading policies if appropriate.

- A public company that issues equity securities to the U.S. government will have to announce the issuance on Form 8-K within four business days and will have to include in that disclosure (a) an explanation of any amendment to the incorporation documents of the company and attach the amended document(s) as exhibit(s), (b) any other material agreement entered into with the government, such as a stockholders’ agreement setting forth any restrictions on voting, any trust into which voting securities may be placed, or any warrant agreement, and any limitations on buybacks, dividends, layoffs or executive compensation or other material restrictions, and (c) the terms of the security issued and the amount paid.

* * * * *

As the effects of the COVID-19 pandemic continue rippling through the U.S. economy, boards of distressed companies may face pressure to act quickly to secure government assistance. Given the potential for compressed decision-making timelines, lack of negotiating leverage, and market and legal scrutiny, directors should consider thinking through the issues raised above in the context of the company’s particular circumstances sooner rather than later.