Print

PrintViola Lutz is Associate Director and Mélanie Comble is an Associate with ISS ESG climate solutions. This post is based on their recent ISS ESG memorandum. Related research from the Program on Corporate Governance includes The Illusory Promise of Stakeholder Governance by Lucian A. Bebchuk and Roberto Tallarita (discussed on the Forum here) and Socially Responsible Firms by Alan Ferrell, Hao Liang, and Luc Renneboog (discussed on the Forum here).

More than a decade after the first Green Bond issuance, the original model of Use-of-Proceeds deals, where proceeds are spent on specifically identified projects, appears insufficient to meet international sustainability targets. The market has seen a number of new structures in the past year alone—from sustainability-linked bonds dedicated to general corporate purposes to transition bonds. As the market grows and continues to innovate, the question is: how can one ensure transparency and trust and what lessons can be drawn from the Green Bond Principles’ success story?

Use of Proceeds Bonds Remain Key to Moving Investment Towards Green and Social Projects

The International Capital Market Association’s (ICMA) Green, Social and Sustainability Bond Principles ensure the allocation of bonds’ proceeds exclusively to green or social business activities. This allocation tenet launched and supported the rise of a credible and trusted sustainable bond market. But the pace at which the real economy needs to shift must accelerate. This pushes the sustainable debt capital market to move toward financing transition and progress, instead of focusing only on existing green and social projects.

General Corporate Purposes Bonds Provide a Necessary Forward-Looking Dimension to the Sustainable Bond Market

Moving away from specific activities and funding commitments, general corporate purposes bonds allow investors to support the overall sustainability strategy of the issuer, thus avoiding the burden of project-per-project accountability. By diversifying sustainable issuance processes and widening the range of potential issuers, general corporate purposes bonds could change the market’s paradigm and scale. To accompany this evolution, the ICMA is expanding its set of voluntary guidelines to promote transparency beyond Use of Proceeds bonds.

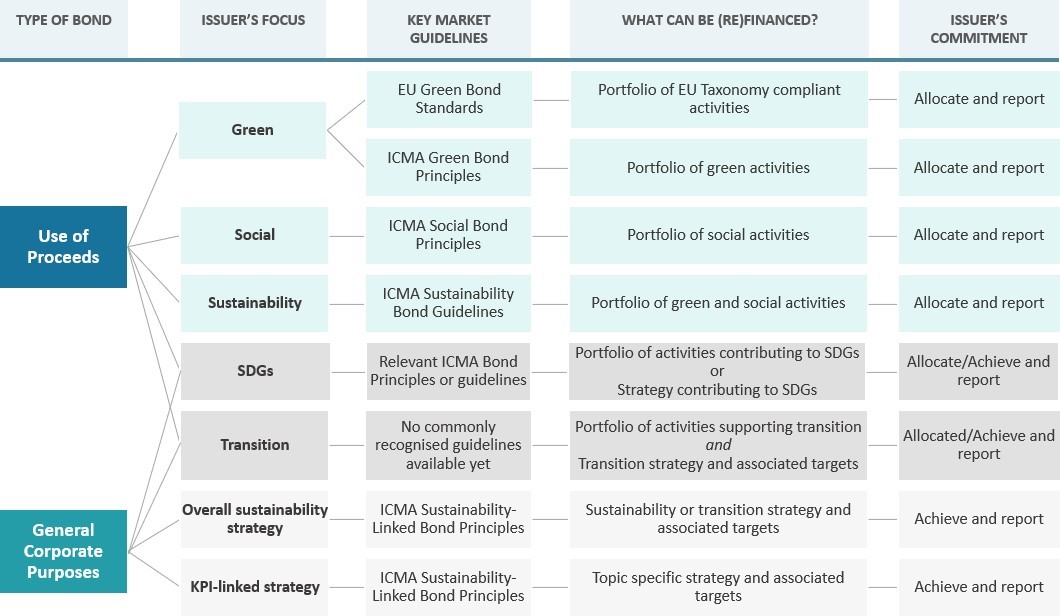

Figure 1: Breakdown of types of bond’s structure depending on issuer’s sustainability focus [1]

Let’s have a look at how to systemize the different options that the sustainable debt capital market offers to date, as illustrated in the table above.

How to be Transparent and Credible When Issuing a General Corporate Purposes Bond

- First, carefully label issuances to clearly communicate what is going to be financed and achieved through bond proceeds. As the market is flourishing with new labels, some issuances faced controversy due to misleading denominations. Choosing the one that most clearly conveys the bond’s purpose while remaining consistent with existing market practices is key to issuing a credible sustainable bond.

- Second, be holistic when defining bond parameters to avoid reputational risks. Issuers can commit on achieving some or all of their sustainability strategy but should always consider both positive impacts and potential adverse effects when doing so. A holistic ESG assessment puts the KPIs selected and derived targets in context with overall sustainability goals and objectives, assessing and making transparent by which means KPI-related targets are met, to what extent collateral risks are mitigated, and that ‘do no harm’ safeguards are in place.

- Finally, select the approach that best expresses what issuers are committing to achieve. The newly released ICMA Sustainability Linked-Bonds Principles provide key guidance on commitments, disclosure, and reporting for general corporate purpose bonds’ issuers. According to those principles, issuers should define KPIs and calibrate associated targets to communicate their sustainability achievement to investors over time. To conduct this exercise, issuers can use internally defined KPIs, externally provided KPIs, or aggregated ESG scores from a provider. To judge the credibility of KPI selection, the rationale for using internal or external KPIs should be transparent and externally verified.

Use-of-Proceeds and General Corporate Purposes Bonds Must Coexist to Reach the International Sustainability Targets

In light of this significant development, issuers need to be transparent on their rationale for issuing general corporate purpose bonds and what they are committing to achieve. Independent external reviews will help create trust in those new instruments by assessing the credibility of issuers’ ESG strategy and business model, of ESG metrics and governance procedures underlying issuances, and of the narrative for those transactions. The collective aim should be to allow Use of Proceeds and General Corporate Purposes issuances to coexist to allow the market to continue capitalizing on these tools, shifting capital toward green and social projects while embracing forward-looking opportunities and supporting transition.

Endnotes

1The transition focus displayed in Figure 1 can be achieved by issuing both Use of Proceeds and General Corporate Purposes bonds. While recognised market guidelines on transition bonds are still to be developed, issuers should refer to existing ICMA Principles for guidance for transparency, disclosure and credibility and get an independent External Review.(go back)