Print

PrintPaul Leake and Mark A. McDermott are partners at Skadden, Arps, Slate, Meagher & Flom LLP. This post is based on their Skadden memorandum.

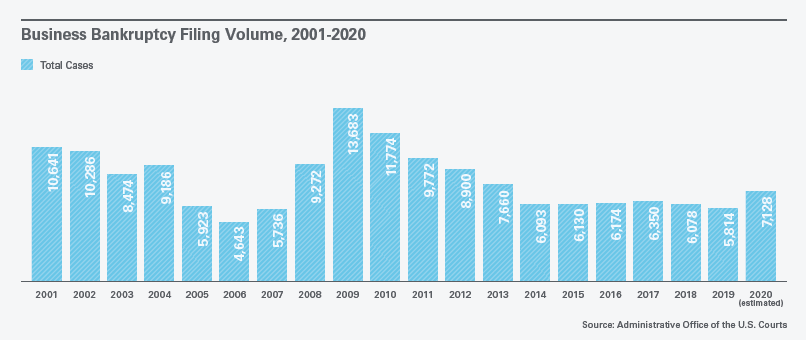

The COVID-19 pandemic has caused massive disruption across the globe, resulting in a significant uptick in U.S. restructuring activity. According to AACER, a database of U.S. bankruptcy statistics, an estimated 7,128 business bankruptcies were filed in 2020, representing a 29% increase over the same period last year. Although Chapter 11 filings increased in 2020, many experts believe we have yet to see the full extent of the surge in filings that will occur in the aftermath of the COVID-19 crisis.

Business bankruptcies peaked at 13,683 in 2009 at the height of the financial crisis and steadily declined in the years thereafter before leveling off to approximately 6,000 filings per year from 2014 to 2019. Although Chapter 11 filings rose in 2020, we did not see the same volume of filings as occurred in 2009. This is in large part due to the unprecedented support provided by the federal government, which allowed many companies that otherwise would have had to file for bankruptcy to weather the economic effects of the pandemic. Looking ahead, while COVID-19 vaccines are now being distributed, uncertainty remains as to when they will be widely available, whether the second stimulus package—including $284 billion in additional loans under the Paycheck Protection Program (PPP)—will be sufficient support for small businesses in the interim, whether certain consumer trends (e.g., business travel) will return to pre-pandemic levels, and how quickly the economy and troubled companies can rebound. These and other factors will affect the volume of Chapter 11 filings in 2021 and beyond.

The chart below depicts corporate Chapter 11 filing volume over time.

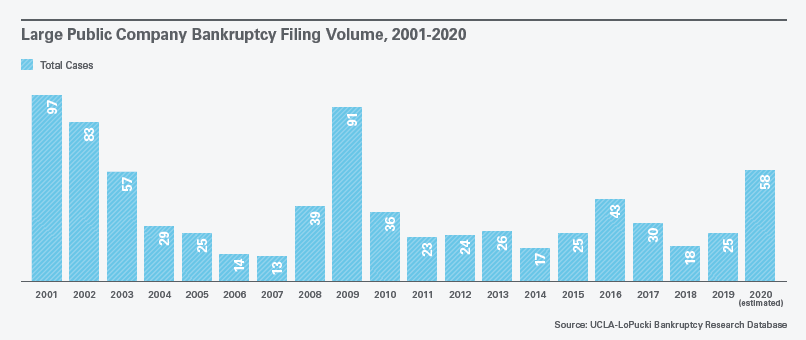

Large public company Chapter 11 filings (i.e., public companies with assets greater than $310 million) follow similar trends. Fifty-eight large public companies filed for Chapter 11 in 2020, up from 25 filings in 2019 but well below the more than 90 filings of large companies in 2001 and 2009, when the dot-com crash and financial crisis, respectively, sent the number of filings higher. The chart below shows the volume of large public company Chapter 11 cases over time. Although filings rose in 2020, many large troubled public companies were able to access the capital markets and/or negotiate consensual out-of-court restructurings with their creditors, which may have contributed to the lower level of filings than in 2001 and 2009.

Early in the COVID-19 pandemic, many companies sought to maximize liquidity in order to weather the storm, drawing down on their revolving credit facilities to do so. U.S. companies are estimated to have drawn down more than $175 billion from revolving credit facilities in March 2020. Some companies sought to preserve liquidity by deferring interest payments, stretching out payables, accelerating receivables and extending debt maturities. Other companies sought to take advantage of market volatility by engaging in debt-for-equity and debt-for-debt exchanges. These common liability management tactics were largely successful in extending the runway for many companies.

Many countries passed economic stimulus legislation in response to the economic impact of the COVID-19 pandemic. In the U.S., the first stimulus package, known as the CARES Act, provided federal funding for businesses in three broad categories:

- $350 billion to support small businesses through programs administered by the Small Business Administration, including the Paycheck Protection Program;

- $45 billion of support in the form of grants and loans from Treasury to passenger air carriers and related businesses, cargo air carriers and businesses critical to maintaining national security; and

- authority for Treasury to invest more than $450 billion in lending programs to be established by the Federal Reserve.

The Federal Reserve programs include two “Main Street” programs intended to provide credit to medium-sized U.S. businesses (companies with either no more than 10,000 employees or no more than $2.5 billion in 2019 revenues). (See our client alert, updated on June 10, 2020, “Updated Guide to the Main Street Lending Program.”) The Federal Reserve also announced a corporate bond purchase program in March 2020. Through the program, the Federal Reserve is authorized to buy both newly issued debt on the primary market and debt that is already trading on the secondary market. In response to the Federal Reserve’s announcement, the capital markets opened up dramatically, allowing many companies to raise much-needed capital.

The recently enacted second stimulus package provides targeted aid to small businesses through $284 billion in additional loans under the PPP. The latest package includes stricter terms that appear intended to address one of the main criticisms of the prior legislation, which allowed a large proportion of the funds to flow to a small number of borrowers. (One percent of borrowers received a quarter of the loans under the prior PPP.) Under the new legislation, only borrowers with fewer than 300 employees that experienced at least a 25% drop in sales from a year earlier in at least one quarter will be eligible. The new legislation also reduces loans under the PPP from $10 million to $2 million and prohibits publicly traded companies from applying this time around. In addition to funding for small businesses, the package provides $15 billion in grants to support entertainment-related businesses such as live venues, movie theaters, museum operators and other cultural providers that have been particularly hard hit by the pandemic.

2021 Outlook

Although the economic stimulus package and the capital markets may have helped a substantial portion of corporate America in the short term, a number of companies have not had and will not have the same access to capital. Consumer-facing industries, including brick-and-mortar retail, restaurants, lodging, travel, cruise lines and airlines, among others, continue to feel the economic effects of stay-at-home orders and travel restrictions. Meanwhile, thousands of other companies remain exposed to significant supply chain disruptions as a result of the unprecedented nature of the COVID-19 pandemic and its profound impact on the global economy. A 2020 study by the supply chain risk management firm Interos found that more than 90% of companies expect that the disruption in the global supply chain caused by the COVID-19 pandemic will have a long-lasting impact on their businesses. Of the 450 senior decision-makers in the U.S. who took the survey, 98% said that their organization’s supply chain was disrupted by the pandemic. Disruption took many forms, including supply shortages, demand reduction and price swings, posing a threat to the operational stability of many companies. Some experts predict that the true impact of the pandemic will not be clear until mid-2021 as the initial effects of the crisis ripple through the global supply chain.

Some experts predict that the true impact of the pandemic will not be clear until mid-2021 as the initial effects of the crisis ripple through the global supply chain.

The United States’ record-high corporate debt levels may exacerbate the economic damage caused by COVID-19. Low interest rates and easy access to credit allowed large U.S. companies to borrow approximately $10.5 trillion of debt through August 2020, according to Bank of America Global Research, which is approximately 50% of the country’s gross domestic product (GDP)—the highest ratio of corporate debt to GDP in U.S. history. This amount of debt represents a rise of 59% from its last peak in 2008, when corporate debt was at $6.6 trillion, approximately 44% of GDP. Of that total, approximately $1.2 trillion is in the form of leveraged loans and about $5 trillion will become due in the next five years. The economic impact of COVID-19, when combined with this level of debt, may serve as the catalyst for the next wave of restructuring.

Many uncertainties remain heading into 2021. Companies that anticipate facing liquidity or covenant issues or that have a significant amount of debt coming due in the next couple of years should be proactive in evaluating their liability management options to ensure that they are well-positioned to not only withstand the pandemic but also be successful in the long term.