Print

PrintNeri Bukspan and Marc Siegel are partners in Financial Accounting Advisory Services at EY. This post is based on their EY memorandum.

Trends and observations

Background

In August 2020, the Securities and Exchange Commission (SEC) introduced an important new requirement for registrants to provide disclosures about human capital. The new requirements were introduced in connection with the SEC rulemaking streamlining some of the disclosure requirements for business, legal proceedings and risk factors under Regulation S-K.

Commencing with most reports filed after 9 November 2020, companies now provide in their annual reports and registration statements a description of human capital resources to the extent material to an understanding of their business. Specifically, a registrant must disclose a description of “human capital resources, including the number of persons employed” and “measures or objectives that the registrant focuses on in managing the business (such as depending on the nature of the registrant’s business and workforce, measures or objectives that address the development, attraction and retention of personnel).”

As companies adopted this new principles-based rule, many for the first time considered how to incorporate this type of data into their 10-K filings. Cross-functional teams came together to discuss questions such as these: What information should be included? How many pages should be provided? Should any, or how many, quantitative metrics be included? How should we align this disclosure with other human capital communications published outside the 10-K, such as in a sustainability report?

Are any specific human capital topics considered more important to include than others? What are the aspects of disclosure controls and procedures that should be considered?

Undoubtedly, the disclosure will continue to evolve as a result of market and investor feedback and analyses, lessons learned from peer and sector practices, and the SEC comment and review process, as well as companies’ enhanced data and information gathering practices in future years, given the need to comply quickly.

In this post, we outline how companies answered some of those questions during the initial year by providing some key takeaways from an analysis of selected filings of S&P 500 filers.

The rules we adopt today update various Regulation S-K items that essentially have not changed in over 30 years. Our economy, and the world economy, have changed markedly in that time, and many of our rules, which were well rooted in the characteristics of the economy of the 1970s and 1980s, simply have not kept up … Today’s rules reflect that important and multifaceted shift in our domestic and global economy. Our rules also are designed to elicit disclosure tailored to each company’s particular industry and business model while being flexible enough to continue to allow for fulsome disclosure as businesses evolve in the future.

—Jay Clayton, Former Chairman of the U.S. Securities and Exchange Commission

Findings

We included 143 S&P 500 companies in our results; [1] while this represents some early findings and does not present the entire population of the S&P 500, we believe our findings are useful to help inform those who are looking to make decisions about how to approach these disclosures in their future filings.

Length—We understand that companies had significant internal discussions about just how much information to include, given that the SEC rule outlined only one specific metric, the number of employees (which was previously required), while pointing to the inclusion of others using principles.

Not surprisingly, we observed a wide range of pages of human capital disclosures, from a single paragraph/quarter of a page to three pages. On average, companies included approximately one page, and the mode was one page as well.

Qualitative versus quantitative—A second area where a strategic decision needed to be made was the interplay between narrative discussion and specific metrics. The majority of companies employed mostly qualitative disclosure, describing how they considered human capital, including metrics to underscore and explain points. Approximately two-thirds of companies included at least one specific figure or metric in addition to the number of employees. As examples, some included a breakout of the employees by geography, number of part- and full-time employees, number or percentage of employees covered by collective bargaining agreements, or gender. Others included attrition rates and employee engagement survey results, as well as injury incident rates, to share information associated with employee safety.

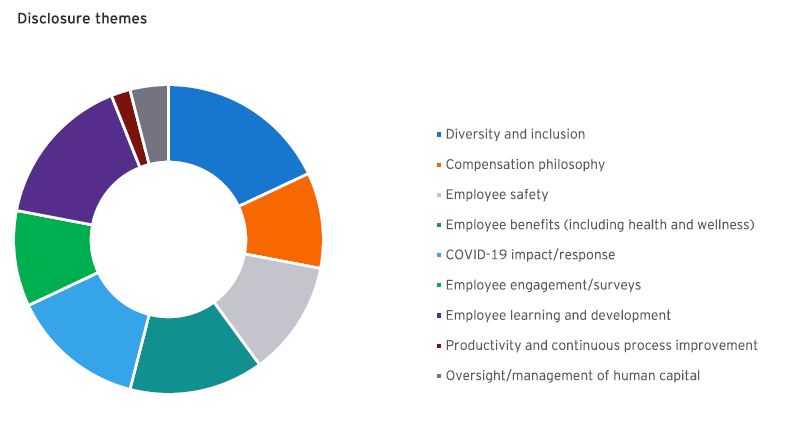

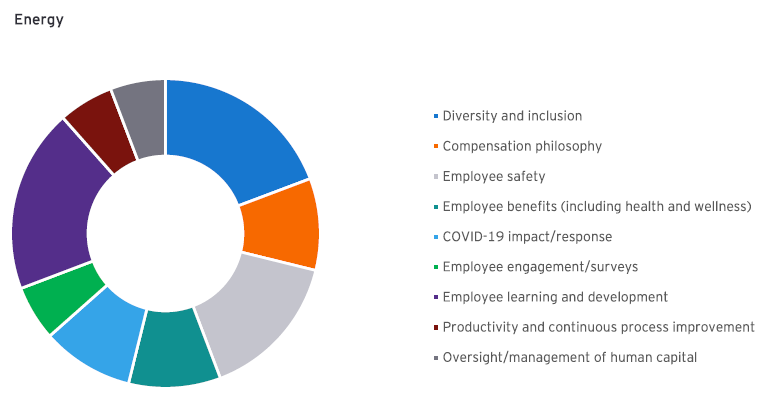

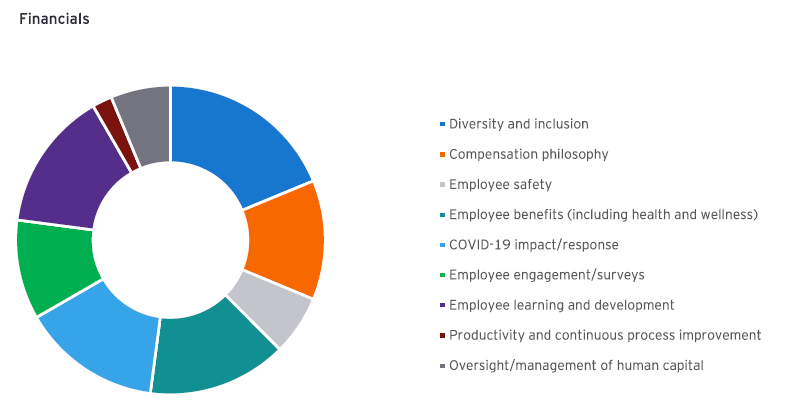

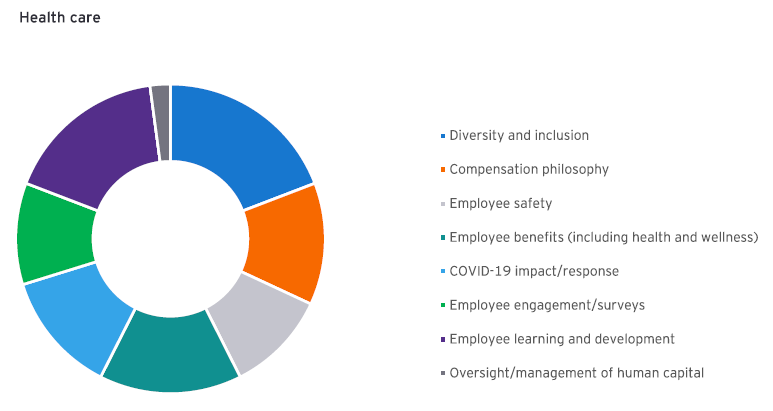

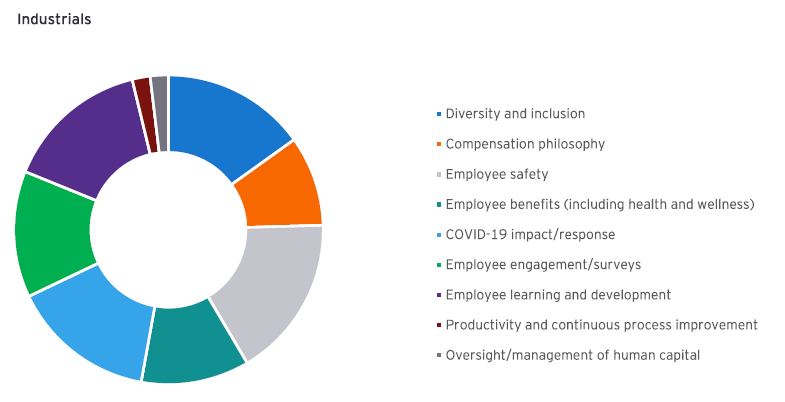

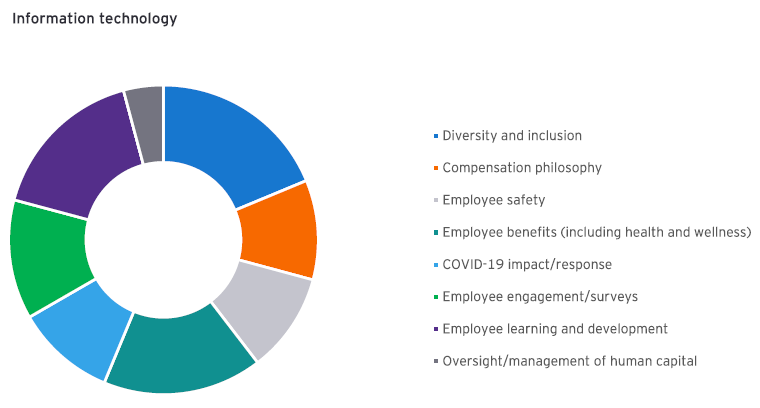

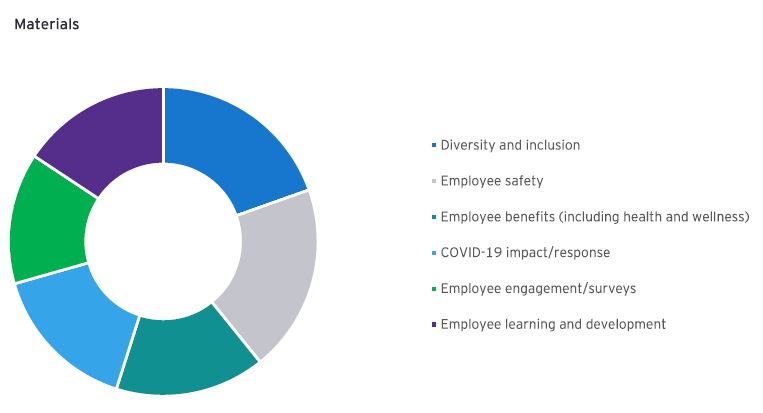

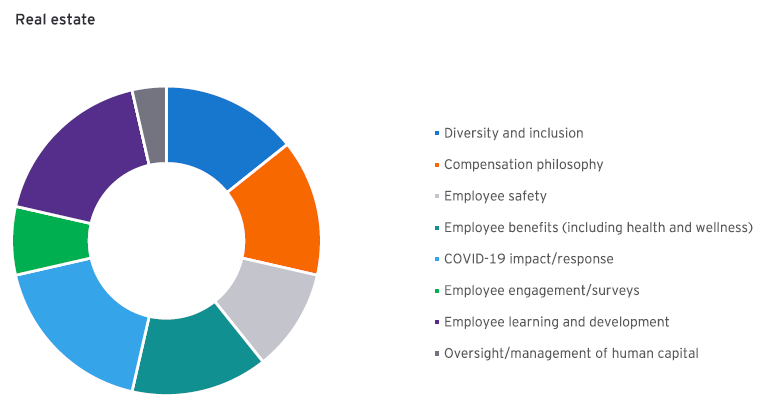

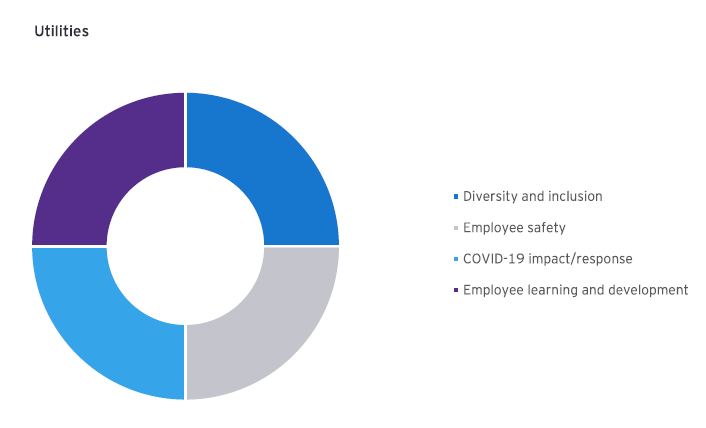

Key themes—Below is a summary of human capital disclosure themes noted in 10-K filings. The bigger the slice of pie, the more frequently this theme was discussed in 10-K filings. An industry breakdown of this analysis can be found in the appendix.

- Diversity, Equity and Inclusion (DE&I)—The most common theme discussed was DE&I. The majority had at least a qualitative discussion of the topic. More than a quarter of the companies included a metric showing the breakdown of employees by gender. A similar number also included specific figures around ethnic diversity.

Investors, particularly those teams focused on proxy voting and stewardship policies, continue to show interest in this area. For example, in a letter from State Street Global Advisors in January 2021, the investment firm indicated that its voting policies with respect to the nominating governance committee of investees would depend on the specific disclosure of board-level diversity and workforce-level diversity in upcoming proxy seasons.

- Employee benefits—A description of benefits offered to employees was one of the top disclosure themes in our sample. Many companies noted that attracting and retaining talent was a key business objective, and the benefits offered to employees were described to highlight how the companies attempted to meet that goal using a variety of compensation and benefits means.

- Employee learning and development—Employee learning and development was another topic discussed, including objectives and practices to attract, develop and enhance employees’ skill sets. Many disclosed, in a narrative form, training programs and opportunities offered, while some supplemented this discussion with a dollar amount invested in training during 2020.

I would expect that the material human capital information for a manufacturing company will be vastly different from that of a biotech startup, and again vastly different from that of a large healthcare provider. And the human capital considerations for a multi-national car manufacturer will be different from that of a regional home manufacturer. It would run counter to our proven disclosure system, particularly as we first increase regulatory emphasis in an area of such wide variance, for us to attempt to prescribe specific, rigid metrics that would not capture or effectively communicate these substantial differences.

—Jay Clayton, Former Chairman of the U.S. Securities and Exchange Commission

- Employee safety—While COVID-19 impacts were often discussed separately, many companies highlighted employee safety as a focus area for management of the business, specifically those with manufacturing and industrial activities. Some disclosed specific incident rates or goals/objectives related to employee safety, while others described their policies and procedures at a higher level.

- Employee engagement/surveys—Many companies discussed their use of employee surveys to evaluate the level of satisfaction of their people and areas that can be improved. Most did not disclose specific findings from the surveys or trends.

- Compensation philosophy—Some companies discussed compensation philosophy, most often at a high level.

- COVID-19 impact/response—Many companies separately discussed their responses to the global COVID-19 pandemic, including as it relates to their workforce. In this disclosure, companies discussed aspects of well-being, health and safety, and work-from-home arrangements. Some included this discussion in the Management, Discussion & Analysis (MD&A) section of their 10-K, while others included it as part of the new human capital disclosures in Item 1.

Further information related to these disclosures by sector can be found in the appendix.

Future considerations

This was the first year of disclosures in this area. Our analysis shows a wide disparity in the extent and areas discussed, as well as depth and approach that companies used to craft their disclosures, including in their use of measures, quantitative goals and targets, as well as key human capital-related performance indicators. Such variation is inherent in the nature of a principles-based disclosure regime: the varying human capital practices employed by companies, coupled with it being a first year for these disclosures. It is our expectation that these disclosures will continue to evolve and be refined, with greater adoption of leading practices, and given the potential for greater investor scrutiny, as well as regulatory interpretation. As noted above, this SEC rule became effective November 2020, and, as such, the disclosures in our sample represent the initial efforts of companies to comply with the newrequirements with little lead time. During 2021, as investor pressure increases and the SEC has signaled that environmental, social, and governance (ESG) will be a priority, we expect companies to continue to evolve their human capital disclosures, enhance their ability to collect data, and consider further disclosure controls and processes that could allow for more to be included in the 10-K.

Frequently asked questions

1. When do we need to adopt the rule?

It is effective for annual reports and registration statements filed on or after 9 November 2020.

2. Where are the new disclosures made?

They are to be included, to the extent appropriate, in Item 101 disclosures of Form 10-K (in the description of the business). The disclosures may also be made elsewhere (e.g., in the MD&A section.

But, in that instance, Item 101 should have a cross-reference to the other section. Note that these disclosures are not required in quarterly filings.

3. Who is required to adopt the rule?

SEC registrants, except for most Foreign Private Issuers (FPls). An FPI would be required to adopt the rule if it chose to file in the US using Form 10-K.

The rule is also required for Emerging Growth Companies.

It is not mandatory for Smaller Reporting Companies (SRCs). An SRC can choose to comply with paragraph (h) instead of any of the other paragraphs in Item 101. The SEC did not add human capital disclosures to paragraph (h), thus giving SRCs the option to disclose voluntarily.

4. Should I talk about my supply chain personnel, or contractors, even though they are not technically employees?

It depends on whether or not the disclosure would be material to an understanding of the registrant’s business. The SEC included the following in the final rule:

“We note that, under the principles-based approach we are adopting, to the extent that a measure, for example, of a registrant’s part-time employees, full-time employees, independent contractors and contingent workers, and employee turnover, in all or a portion of the registrant’s business, is material to an understanding of the registrant’s business, the registrant must disclose this information .”

Appendix

Methodology

We assessed 10-Ks filed by S&P 500 companies between 8 November 2020 (the effective date of the Rule) and 15 February 2021, capturing the following information:

- Company industry

- Page length of human capital disclosure section

- Themes (e.g., diversity, equity and inclusion) outlined in the disclosure

- Metrics included in the disclosure (yes/no)

Industry highlights

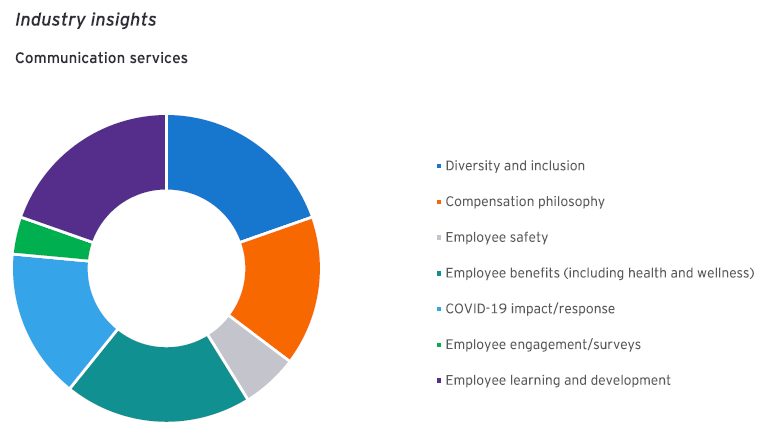

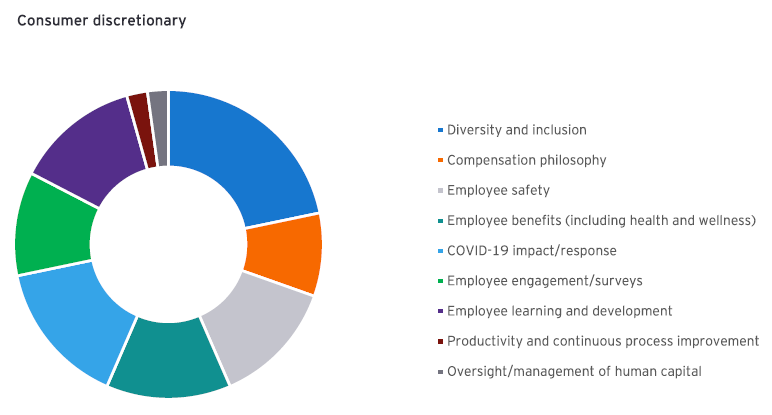

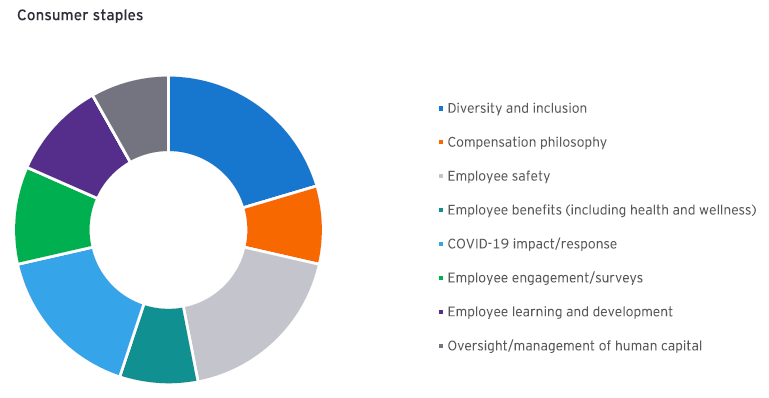

A few trends were noted in the human capital disclosures by industry:

- Four topics were observed by at least one company within each industry across all industries: diversity, equity and inclusion; employee safety; COVID-19 impact/response; and employee learning and development.

- In the compensation philosophy and employee engagement/surveys, two topics saw the greatest variability across industries. Approximately 80% of filings in the communication services and real estate industries discussed this, whereas 0% of the materials industry and the utilities industry discussed it.

- Less than 40% of companies disclosed oversight/management of human capital across all industries.

- On average, companies included in the real estate, industrials, energy, materials and communication services industries discussed the greatest number of themes in their human capital disclosure.

- The utilities industry discussed the fewest number of themes, which included the following four: diversity, equity and inclusion; employee safety; COVID-19 impact/response; and employee learning and development.

The details of our findings by sector are included below. These charts depict how frequently a theme was discussed as compared to other themes.

Endnotes

1Obtained from filings made through February 15, 2021.(go back)