Print

PrintMaria Castañón Moats is Leader, Paul DeNicola is Principal, and Leah Malone Director at the Governance Insights Center, PricewaterhouseCoopers LLP. This post is based on their PwC memorandum. Related research from the Program on Corporate Governance includes The Long-Term Effects of Hedge Fund Activism by Lucian Bebchuk, Alon Brav, and Wei Jiang (discussed on the Forum here); Dancing with Activists by Lucian Bebchuk, Alon Brav, Wei Jiang, and Thomas Keusch (discussed on the Forum here); and Who Bleeds When the Wolves Bite? A Flesh-and-Blood Perspective on Hedge Fund Activism and Our Strange Corporate Governance System by Leo E. Strine, Jr. (discussed on the Forum here).

This post is divided into two principal parts. The introduction analyzes the most important current trends in shareholder activism. The chapters that follow take a longer-term perspective.

We take an expansive view of shareholder activism. For many people, the phrase may conjure images of hedge funds waging proxy battles as they try to win control of their target’s board. That’s a part of activism, to be sure. But, for the purposes of this post, the term refers to the efforts of any investor to leverage their rights and privileges as an owner to change a company’s practices or strategy.

In this sense, shareholder activism may include an institutional investor’s engagement with companies around governance matters or a retail investor’s shareholder proposal, as well as a hedge fund’s proxy fight.

Shareholder activism in 2021

The COVID-19 crisis has left its mark on all aspects of society and business. Shareholder activism is no exception. In 2020, activists targeted fewer companies and put less capital to work in their campaigns as the pandemic roiled financial markets and sparked a deep economic recession. But there is ample evidence of a resurgence in 2021. What do boards of directors need to know to navigate this environment?

The pandemic’s impact

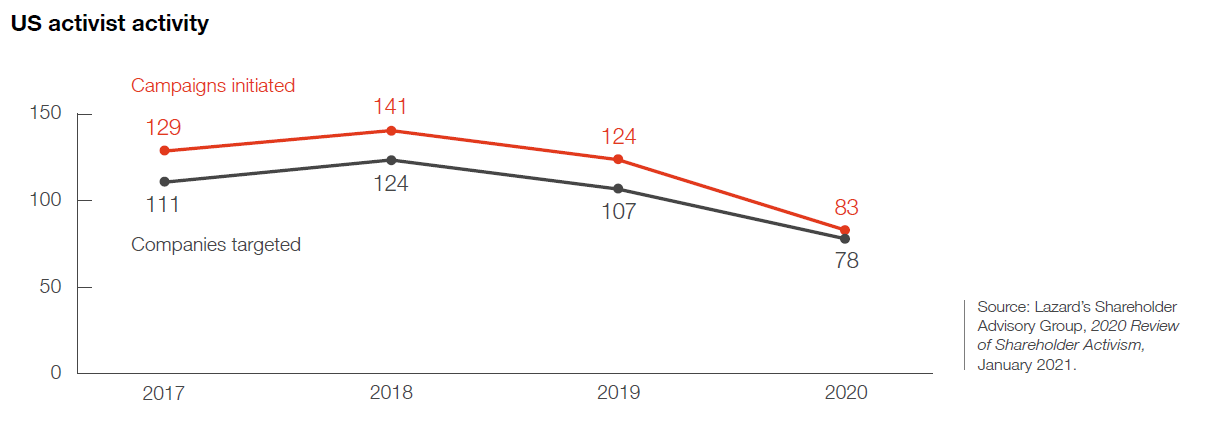

Shareholder activism slowed considerably as COVID-19 spread. In the US, activists launched 34% fewer campaigns and targeted 25% fewer companies in 2020 than they had the previous year. [1] But the fourth quarter of 2020 saw activity begin to rebound. During the first quarter of 2021, the number of campaigns launched increased 48% over the first quarter of the prior year. Activists initiated 37 campaigns, almost half of 2020’s total activity. [2]

Mergers and acquisitions (M&A) have historically been among shareholder activists’ top objectives. This could mean pushing a company they invest in to sell all or part of itself, or to seek better terms if it’s already in talks to be acquired. These kinds of outcomes remained activists’ most common goals in 2020 and into the first quarter of 2021. [3] With the pandemic causing economic turmoil worldwide, activists pushed more companies to unlock value by breaking themselves up or selling business units. Such moves were the most common objective of M&A-focused campaigns last year. [4]

The strong start to 2021 suggests that the 2020 slowdown was temporary. Several activist hedge funds made no secret of the fact that they were taking advantage of the steep decline in equity prices during the early days of the pandemic to build up stakes in potential target companies. Investments like this position activists to continue to increase their activities in 2021.

The pandemic has put boards and management teams to the test. It may also open their companies up to additional shareholder scrutiny, as well as make them an activist target, if their performance is underwhelming.

ESG in focus

Environmental, social, and governance (ESG) matters remain a priority for institutional investors when engaging with the companies whose shares they hold—and climate change is arguably at the top of their agenda. In addition, widespread protests against racial injustice in 2020 prompted several of the largest asset managers to emphasize diversity and inclusion (D&I) in their public statements and proxy voting policies to a greater degree than in years past.

ESG is expanding beyond being just a concern of institutional investors. Hedge fund activists are increasingly pushing companies to increase disclosures and adopt more sustainable business practices. They see better ESG metrics as a path to unlock value. Some traditional activists have begun to press companies in which they invest on ESG matters. [5] A handful of recently launched firms are dedicated specifically to ESG-focused investing and activism. Some have even undertaken proxy fights in the hope of placing their own directors on company boards.

Other emerging trends

Special-purpose acquisition companies (SPACs) have emerged as a popular alternative to an initial public offering for some private companies. They aren’t new, but the volume of deals involving SPACs is. By March 2021, the volume of SPAC transactions had already surpassed 2020’s total. [6]

Shareholder activists have tapped into this trend. They’re using SPACs as a way to raise capital for M&A. Many of the most active hedge fund activists have launched SPACs recently. Early 2021 saw the emergence of what could be a new frontier in shareholder activism. Retail investors used social media and stock-trading apps to coordinate the buying of a handful of consumer brands’ shares. Within a month, they had pushed prices of the stocks to dizzying heights. And even more quickly, the shares collapsed as the investors moved on. Is this risk here to stay? Or simply an internet-enabled fad?

It’s too soon to say. But there may be good reason for boards to consider the risks that this kind of investor behavior poses to their companies. One key difference between the shareholders behind this phenomenon and traditional activists is that these investors didn’t seek any changes in strategy, disclosure, or capital allocation from the companies they targeted. That may change in the future. It’s a risk that may be worth monitoring.

Activists: Who they are and what they want

An asset manager overseeing trillions of dollars in securities pledges to vote against the boards of companies that fall short on ESG matters. A hedge fund a fraction of that size threatens a proxy fight at a company it feels has too much cash on the balance sheet. Both fall under the umbrella of shareholder activism: seeking change because they think management isn’t maximizing their targets’ potential. But while they may share an ultimate goal, their tactics can differ greatly.

Institutional investors

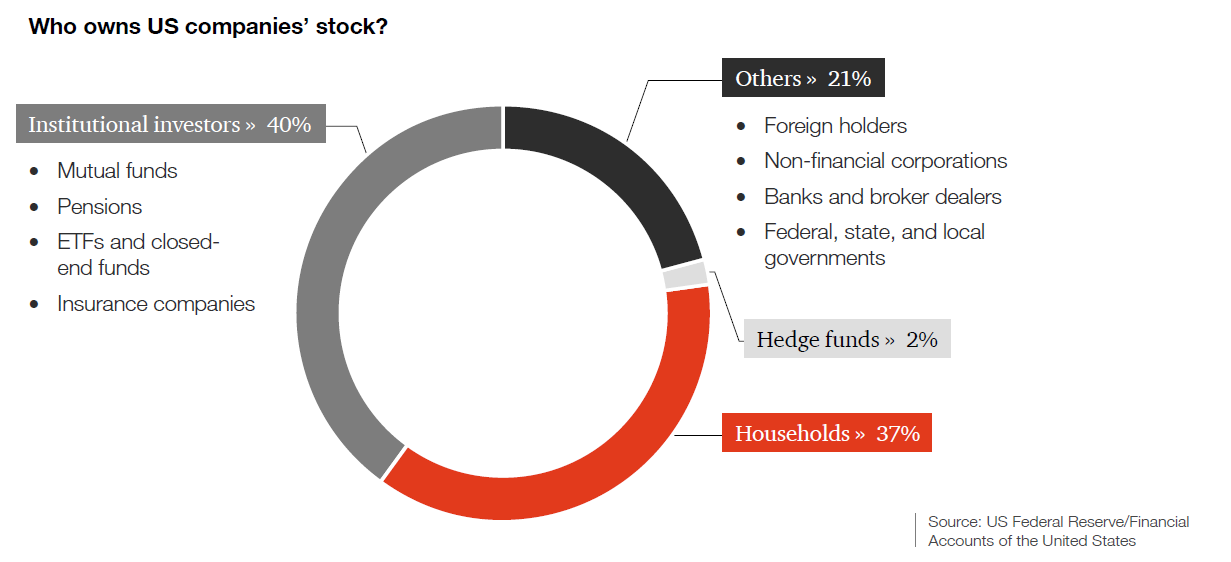

Pension funds, insurance companies, and firms that manage mutual funds and exchange traded funds are all examples of institutional investors. Not only do institutional investors own a larger proportion of publicly traded companies’ shares than retail investors do, but they also vote their shares at a much higher rate. This makes them influential stakeholders for many public companies.

Institutional investors are normally long-term shareholders. Many benchmark their holdings to broad stock market indexes like the S&P 500. Others offer index funds to retail investors, who are attracted by their low fees. Passive funds can’t just sell a position if they think a stock is underperforming, or if they believe the company’s governance practices hinder its longterm value. Activism is one of the only levers they have to address these concerns. Through activism, they can bring attention to their concerns and drive the change that they believe will create long-term value—including through changes in corporate governance practices. The largest asset managers are vocal about their belief that companies with strong corporate governance practices can deliver better value in the long run.

Hedge funds

Hedge funds attract big dollars from investors seeking above-average returns. So they are always looking for untapped value. Hedge fund activists often see that untapped value in the way a company is run or the strategy it pursues. They see ineffective management, a stale board, or a company missing out on new opportunities. They see the potential for a new capital allocation strategy or changes in operations that will increase share value. And when their efforts to engage with executives or directors about these ideas fail, they often try to get board representation to help achieve their goals.

Hedge fund activists traditionally focused on capital allocation issues, such as dividends and share buybacks. Many then began looking for company combinations and break-ups— mergers, carve outs, and spin-offs. Now there is a greater focus on operational activism, which has more of a long-term focus. Activists join the board (or appoint independent directors), replace members of management, and help execute a new strategy. While many hedge funds had been thought of as being too focused on short-term gains, the longer-term operational activism has helped to shift that perception somewhat.

Other investors

Traditional asset managers and hedge funds account for most activist activity. And because they manage the most money—and vote the most shares—they have the greatest ability to make a serious push for change. But they aren’t the only shareholder activists.

Religious groups, nonprofits, and other advocacy organizations also use the tools of shareholder activism, most notably shareholder proposals, to encourage companies to change.

There are also a small handful of individuals who have made a name for themselves as activist shareholders through retail investing. In fact, these shareholders are responsible for a majority of all shareholder proposals that go to a vote each proxy season. Historically, they have tended to focus on “good governance” matters—majority-vote director elections, declassified boards, and so on. Recently they have broadened their strategy to include ESG and other matters as well.

Tactics: How activists pursue their goals

Some shareholders turn to activism because they feel it’s an effective way to increase the value of the companies whose stock they own. Others do so to address governance practices they believe are hurting long-term value. Or they take issue with the company’s products or business practices. Activism can take many forms. But the goal is the same: to motivate management and boards to make changes in the way their companies are run.

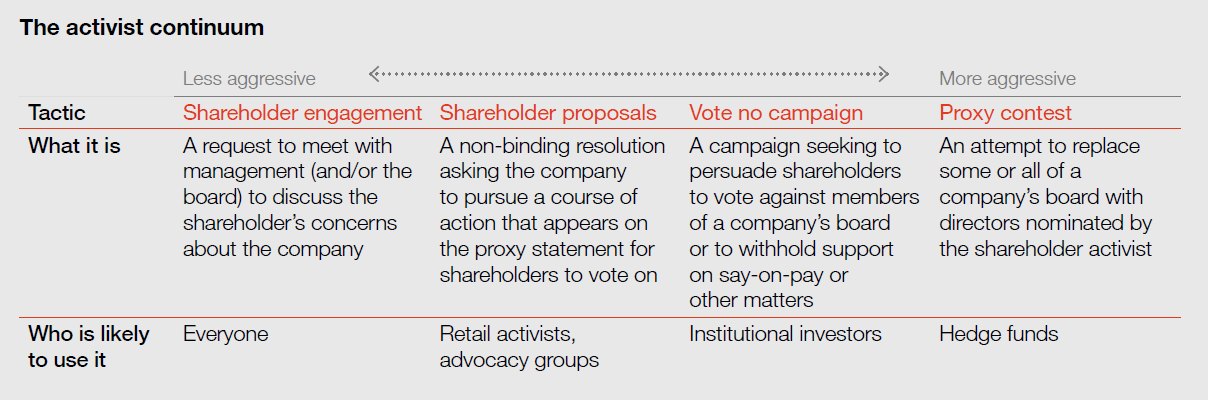

The tactics that shareholders use will depend on their objectives. What makes sense for an institutional investor with a long time horizon may not work for a hedge fund looking for a quicker return. You might even think about activist tactics as a continuum that begins with routine shareholder engagement. Not every request to meet with management is a prelude to more drastic forms of activism. But many shareholders who seek change will start by attempting to persuade. Others are more likely to start at the more aggressive end of the activist spectrum.

Shareholder proposals

In some cases, investors view a shareholder proposal as a way to begin the conversation with a company. Other times, institutional and retail investors submit—or threaten to submit—a shareholder proposal if direct engagement with the company and its directors doesn’t produce changes.

Top proponents of shareholder proposals in 2020

| Proponent | # of proposals | Share of total |

|---|---|---|

| John Chevedden (& associates) | 223 | 31% |

| As You Sow Foundation | 63 | 9% |

| Mercy Investment Services | 34 | 5% |

| Trillium Asset Management | 34 | 5% |

| New York City Comptroller | 25 | 3% |

Source: Gibson Dunn, Shareholder Proposal Developments During the 2020 Proxy Season, August 2020.

These proposals often focus on governance practices or policies, executive compensation, or the company’s behavior as a corporate citizen. Proponents watch how the major institutional investors are voting on issues and have a sense of which shareholders may be likely to support their proposal going in. They also often reach out to other shareholders to encourage support for the measure. By the time the company receives the shareholder proposal, its sponsor may already know whether it will pass. A company may receive the same proposal over multiple years with increasing support until it finally achieves a majority.

Vote no campaigns

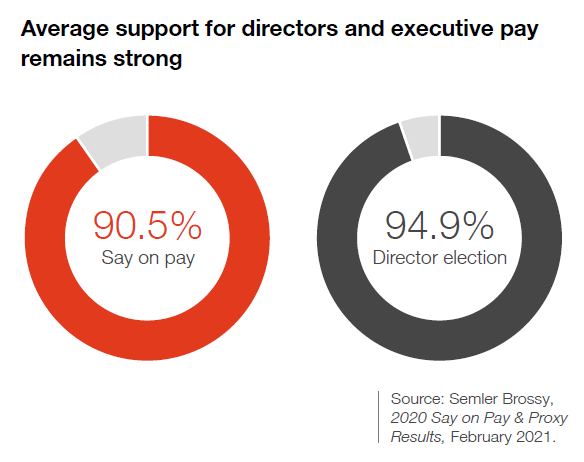

“Vote no” campaigns urge shareholders to vote against (or withhold their votes from) director candidates or other matters such as say on pay. Vote no campaigns can send a strong signal about shifting shareholder priorities.

The vote doesn’t actually have to fail for a vote no campaign to achieve results. Overall shareholder support both for directors and for say on pay is typically above 90%. So if support levels fall to the 60s or 70s, it sends a stark message about shareholder dissatisfaction. It also generates media scrutiny, and can affect a director’s reputation. Directors often serve on multiple boards, and low support levels at one company can affect how that director is viewed at his or her other companies as well.

Proxy fights

Shareholder activists may conclude that the best way to achieve their goals is to replace some or all of a company’s board. In that case, they advance their own slate of director candidates and try to persuade other shareholders to vote for them. Proxy contests can be expensive and controversial. Historically, they’ve been most closely associated with activist hedge funds.

The precise activism playbook may vary from investor to investor, but there are several steps hedge funds commonly take to make the threat of a proxy fight more credible. They may try to win the support of a company’s other shareholders by circulating a lengthy white paper that lays out the case for the changes they’d like to see. Or they may publish an open letter to the company’s management or board listing their concerns. It’s a virtual certainty that documents like these will end up in the hands of the media, further ratcheting up the pressure.

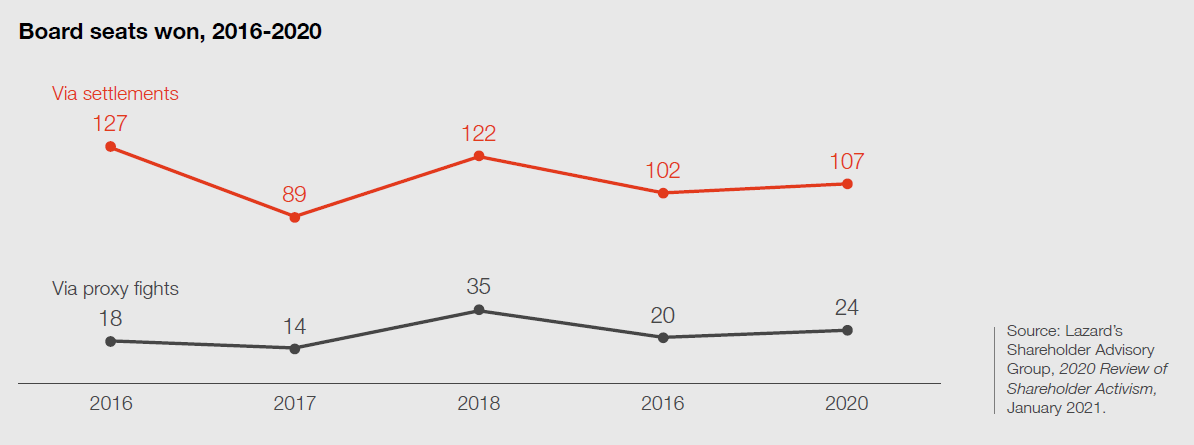

Proxy fights are long, expensive, and draining for a company. Success isn’t assured for the hedge fund, either. That’s why activists and the companies they target sometimes reach a settlement that heads off a full-blown proxy contest. As a result, the activist may receive seats on the company’s board or assurances from management that some of the changes it seeks will be enacted. From 2016 to 2020, 83% of the board seats won by activists came

via settlements. [7]

Some institutional investors have grown concerned in recent years that companies are settling too easily. Before rushing to settle, they urge companies to at least reach out to their significant shareholders to solicit their views. Sometimes these investors agree with the activist—and sometimes they want the company to hold their ground against the activist.

Risk factors: The red flags that can lure activists

Every shareholder activist has a unique agenda. But history shows that companies that attract activist engagement tend to have some issues in common. Poor performance in the stock market, weak earnings compared to peers, governance missteps, and lack of attention to ESG matters can all trigger shareholder activism.

Poor financial or share performance

Shareholders are rarely happy to see a company underperforming its peers, hanging on to divisions that don’t fit with the rest of its business, or hoarding too much cash on a balance sheet. Whether they turn to activism as a result often depends on their investment strategy. The chances also tick up if there are other governance concerns.

Hedge fund activists are typically looking to unlock value they believe is going unrealized. Companies with a low ratio of market value to book value, excessive cash on hand, or lots of monetizable assets like real estate may fall into their crosshairs. Institutional investors are commonly less likely to support activism at a company unless it also suffers from one or more of the governance weaknesses discussed on the next page.

Governance weaknesses

Governance problems can both indicate other weaknesses at a company, and can have a detrimental effect on its value. Issues that may prompt investors to engage with a company, to submit a shareholder proposal, or take even more drastic measures may include:

- Board structure and composition. Many institutional investors are intensely focused on board composition, and in particular on board diversity. Companies that make it difficult to vote out underperforming directors can also draw the ire of shareholders. These may include:

- – Classified boards

- – Election of directors by plurality vote

- – “Zombie directors” who remain on the board after failing to receive majority support

Even absent these structural issues, some shareholders will engage with companies around board tenure and refreshment.

- Executive compensation. Companies with problematic pay practices, pay that is out of alignment with company performance, or that don’t respond after a low say-on-pay vote can all become targets of shareholder activism.

- Material weakness. Less frequently, disclosure of a material weakness can sometimes prompt shareholders to vote against audit committee members. It’s especially likely if the company is not seen to be taking appropriate action to remediate the issue.

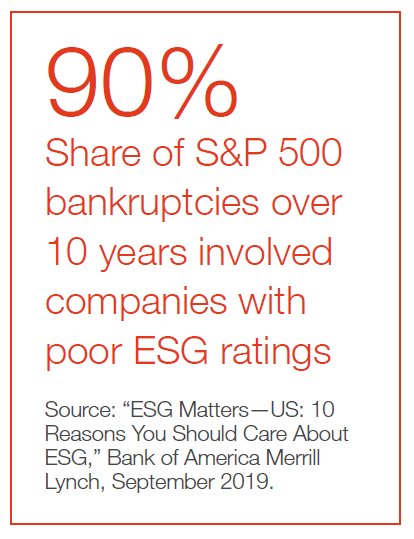

ESG shortcomings

Perceived poor practices in the ESG realm can also make a company an activist target. Sometimes this relates to the environment, such as lack of disclosure around risks related to climate change. It could crop up with respect to corporate social responsibility, including inadequate labor, health, or safety practices. The extent of political spending and lobbying can also increase a company’s risk for becoming a target of shareholder activism.

Many of the largest asset managers have called for more disclosure in this area. They want companies to discuss how issues such as climate change and D&I factor into their strategies. And they want to know companies’ plans for confronting those challenges.

Hedge funds are increasingly focused on ESG as a catalyst for their activist campaigns. They see a connection between ESG performance and shareholder value. Several funds that have launched recently put the connection between sustainable practices and value creation at the center of their missions.

Ignoring shareholder concerns

Lack of responsiveness to investors can bring unwelcome attention. Sometimes an issue that has come up during shareholder engagement may evolve into a shareholder proposal. Other times, if the company hasn’t taken action in response to a concern, the consequences can be more severe. For example, if a company’s say-on-pay vote garners low support levels, shareholders expect to see changes in the company’s incentive plans. If those changes don’t come, shareholders may launch a campaign to vote against the directors on the compensation committee. The bottom line: It rarely hurts to hear a shareholder out, determine whether their arguments have merit, and, if so, consider acting in response.

Heading off an activist

Shareholder activism can come as a surprise. When a hedge fund presses a company to divest an underperforming asset or put itself up for sale, it can leave the management team and board scrambling. They may ask themselves why they didn’t see it coming. Even being on the receiving end of a shareholder proposal can feel like an unwelcome intrusion.

Directors have a key role to play in being prepared. They can anticipate which activists may engage with the company, the issues they may raise, and how other shareholders might respond. They can push management to address issues that may attract activist attention. Not only can these actions help ward off an activist, but they may also help improve the company’s performance and its relationship with key stakeholders.

Take a candid look at your company

Directors should always make it their business to stay informed about their company’s strategy and how effectively it’s being executed. This requires looking at the company’s performance with a critical eye. However, the data directors get can sometimes be so granular that it’s hard to see the big picture. Other times, it might be so high level that important details are easily overlooked.

Focusing on common triggers for activist engagement may help boards cut through the noise. Asking how the company’s ESG disclosures compare to best practices, for example, or how the dividend stacks up against peers that have been targeted by activists may help bring clarity. Ask to hear from outside experts, industry analysts, investment bankers, or others from outside the company to get a better understanding of how the company is seen by investors and potential activists. Make sure to ask for outsiders’ “unvarnished” views—ones that haven’t been toned down (or whitewashed by management).

If there are issues, take proactive steps to address them. This can reduce the chance of becoming an activist target. It can also strengthen your credibility with the company’s shareholders. Even if the company chooses not to make any changes, going through the critical process will help company executives and directors reaffirm and articulate why they believe the company is on the right course.

Know your shareholders

Ensure that the board is informed when an activist takes a significant position in the company or in an industry competitor. And make sure the board hears about broader activism trends that could affect the company in the future. Understanding what these shareholders may seek will help the company assess its risk of becoming a target and help it know what tactics to expect.

And of course, directors should keep up to date on the views of the company’s largest shareholders. This includes carefully watching any changes to their public engagement priorities or proxy voting agendas.

Create an engagement plan

Once a company identifies areas that may attract activist attention, engaging with other shareholders around these topics can help prepare for—and in some cases may help to avoid—an activist campaign. Being transparent about the company’s vulnerabilities and its strategic choices can help change a shareholder’s view of the issue, and demonstrate that the board is fulfilling its oversight responsibilities. Even before the company receives an activist overture, some companies may find it helpful to start getting directors involved in discussions with major investors. If shareholder activists do target the company, directors will already have credibility with other investors. That may make them more effective spokespeople for the company’s position.

How to respond to an activist

When an activist comes calling, the company response is critical. An ineffective response may make things worse by giving the impression that the company’s management and board are not attuned to shareholder concerns. While the activist’s scrutiny may be unwelcome, that doesn’t mean their concerns are without merit. An encounter with a shareholder activist may make the company stronger in the long run— if it’s handled effectively.

Objectively consider the issues on the table

Hedge fund activists usually do extensive homework before they approach a company. Based on that research, they develop specific proposals for unlocking value—at least in the short term. And they have often discussed these ideas with other shareholders. Assume the company’s institutional investors have already spent time evaluating the activist’s suggestions. Investors will expect the company’s executives and board to do the same—even when it’s uncomfortable. And it often is. They might be looking for changes in the boardroom, which may feel like a personal affront to the directors around the table. Or they may be looking for a change in management, which will almost certainly feel like an attack on the CEO. But none of these ideas should be dismissed out of hand.

It’s also important to take a shareholder proposal or vote no campaign seriously. Take a step back. Few companies are perfect when it comes to corporate governance. Perhaps the company’s practices are justified. But are there areas that could be improved? Changes that have been avoided as a result of status quo bias? If that’s the case, shareholder pressure could be a valuable wakeup call—as long as it isn’t ignored.

Determine how best to respond to the investor

When it comes to hedge fund activists, the strategy may differ. If the fund approaches with a private request, it may make sense to respond. This gives the company a chance to hear about the activist’s criticisms. It may also lay the groundwork for future private conversations— which can be helpful if the company later wants to negotiate a settlement with the activist. When hedge fund activists take their campaigns public, however, the smartest move may be

to say very little. There’s very little potential benefit for a company in trading blows with a hedge

fund activist in the media.

For companies that have received a shareholder proposal or been targeted for a vote no campaign, their best bet is to reach out to the investor. Discuss their specific concerns. When dealing with a shareholder proposal, the company and the shareholder may be able to agree on some action at the company in exchange for withdrawing the proposal. Shareholders don’t always insist on immediate action. They know change can take time, and often they are satisfied if the company demonstrates that it has a plan in place to address the issue. Communication might not put an end to a vote no campaign, but understanding the shareholder’s perspective will help the company respond.

Reach out to other shareholders

When activists are contemplating vote no campaigns or proxy fights, they will need support from other shareholders to be effective. It’s safe to assume they’re already engaging with the company’s other investors, so it’s important that management and the board make themselves heard as well. An approach from an activist can present an opportunity to discuss the issues they raise with other shareholders. Take the chance to articulate the company’s view about why its current course is in the best long-term interests of the company and all of its investors (if it is).

Ideally, the company already has an established relationship with those shareholders to build upon. If the company doesn’t believe the activist’s proposed changes are in its best longterm interests, investors will want to know why—and just as importantly, how the company reached this conclusion. On the other hand, if the company has decided to make some changes, be open about what those are. And consider disclosing the breadth of the company’s shareholder engagement efforts in the proxy statement to give yourself credit for your outreach. Often we hear that the suggestions activists make are ones that the company had already been considering.

Look for ways to build consensus

More companies than ever are finding ways to work with activists. Proxy contests are costly and time consuming. It may make sense to find common ground with shareholder activists to take these risks off the table.

Reaching an agreement with a shareholder activist may require the company to increase disclosure of certain information, change its capital allocation, or even add new directors to the board. These moves may not have been in the company’s plans before the activist encounter, but they may make sense if the alternatives include even more drastic changes—such as a proxy fight that could give the activist control of the board.

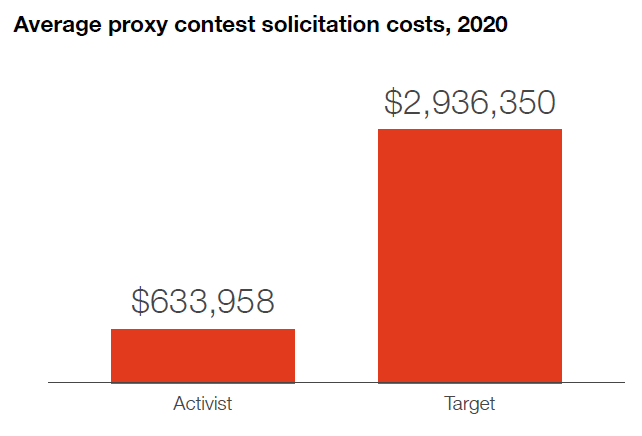

Activists are also motivated to reach agreement. Even though target companies typically spend many times as much on proxy solicitation efforts, the cost to an activist is also significant. If given the option, most activists would prefer to spend less time and money to achieve their goals. Once they agree, the activist and the company enter into a standstill agreement that sets the terms of their relationship going forward.

Even non-binding shareholder proposals can cause embarrassment if they pass—or even just receive unwanted media attention. It may make sense to see there’s middle ground between the company and the proponent that both can live with.

Source: Activist Insight, Proxy Fights 2020, October 2020.

Conclusion

Even as activism—by institutional investors, hedge funds, and others—continues at a healthy pace, many think the number of campaigns still could be on the upswing. For companies, listening and being prepared are crucial. Boards have an important role to play in helping to navigate the changing landscape of shareholder activism.

Endnotes

1Lazard’s Shareholder Advisory Group, 2020 Review of Shareholder Activism, January 2021.(go back)

2Lazard’s Shareholder Advisory Group, Q1 2021 Review of Shareholder Activism, April 2021.(go back)

3Lazard’s Shareholder Advisory Group, Q1 2021 Review of Shareholder Activism, April 2021.(go back)

4Lazard’s Shareholder Advisory Group, 2020 Review of Shareholder Activism, January 2021.(go back)

5“Hedge Fund Activists Pivot to ESG,” Institutional Investor, January 23, 2020.(go back)

6“Global SPAC deal volumes this year surpass total for 2020,” Reuters, March 9, 2021.(go back)

7Lazard’s Shareholder Advisory Group, 2020 Review of Shareholder Activism, January 2021.(go back)