Print

PrintAiyesha Dey is Høegh Family Associate Professor of Business Administration at Harvard Business School; Austin Starkweather is Assistant Professor of Finance at the University of South Carolina Darla Moore School of Business; and Joshua White is Assistant Professor of Finance at Vanderbilt University Owen Graduate School of Management. This post is based on their recent paper.

The market power of proxy advisory firms has attracted considerable attention from academics, practitioners, and regulators. A large body of research shows that recommendations by proxy advisors—such as those by Institutional Shareholder Services (ISS)—can substantially influence shareholder voting outcomes (e.g., Malenko and Shen, 2016). The academic literature, however, is mixed on whether their recommendations are value-enhancing, with some linking their advice to standardized executive pay plans and reduced company value (e.g., Larcker, McCall, and Ormazabal, 2015). Such criticisms and a decade-long review by the U.S. Securities and Exchange Commission (SEC) culminated in the promulgation of restrictive amendments to proxy advisory rules in July 2020 that SEC Chair Gary Gensler recently indicated the Commission may revisit.

In our research paper, Proxy Advisory Firms and Corporate Shareholder Engagement, we consider the role of proxy advisors through a different lens. Specifically, we examine whether and how proxy advisors influence companies’ shareholder engagement activities. Given the recent increase in demand for shareholder engagement by market participants and regulators, the findings of our research can add to our understanding of whether proxy advisors can have a disciplinary spillover effect by inducing desirable company behavior.

Our study exploits a level of opposition to advisory voting on executive compensation where ISS’s policies call for an explicit response. When Say-On-Pay voting support falls below 70%, ISS conducts a qualitative review of disclosed shareholder engagement efforts at the next annual meeting. For companies that fail to demonstrate an adequate engagement response, ISS’s policy is to recommend voting against Say-On-Pay as well as incumbent compensation committee members. When companies demonstrate multiple years of insufficient responsiveness, ISS may recommend voting against the entire board.

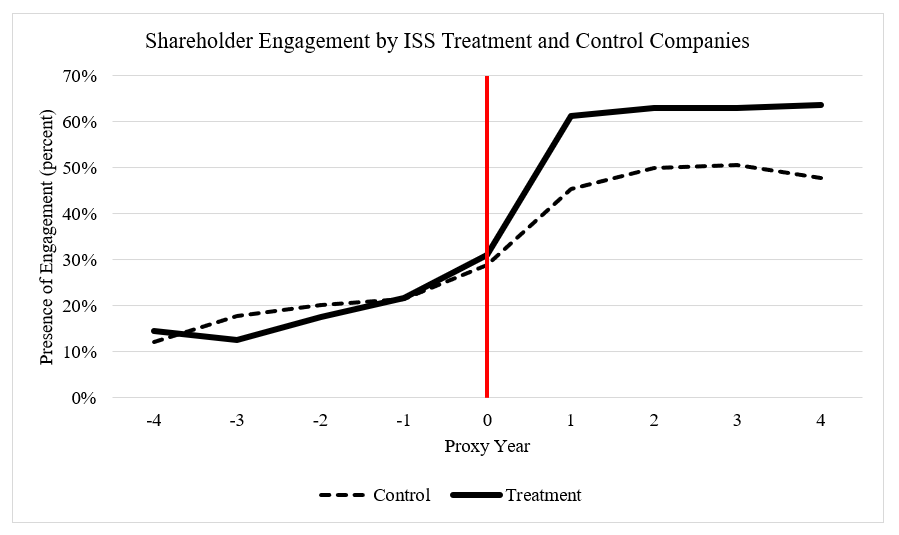

To study the influence of this policy on engagement, we examine a sample of companies from 2011 to 2019 that fall within a narrow bandwidth around the 70% voting support threshold, where we expect that receiving ISS scrutiny is as good as random. We verify this assumption by showing Say-On-Pay voting outcomes are smoothly distributed across the deterministic 70% threshold. Moreover, when comparing companies with Say-On-Pay voting support just below 70% (“treated”) and those just above it (“control”), we find no statistical differences in other characteristics, such as prior Say-On-Pay voting support, engagement levels, and stock returns. This research design allows us to control for the typical response to a low Say-On-Pay vote and attribute abnormal changes in investor engagement by treated companies as being causally influenced by ISS’s policy.

To measure company responsiveness, we first extract the text of shareholder engagement discussions in annual proxy statements and develop several novel measures of engagement. We find that the influence of ISS results in a swift increase in shareholder engagement efforts that is substantively larger than the response by control companies to a low Say-On-Pay vote. For example, the figure below shows that ISS treatment companies are 17% more likely to report shareholder engagement details in the proxy statement the year after the low vote (depicted by the red line). This difference represents a 32% increase relative to the sample average. In comparison to control companies, ISS-treated companies also provide more transparent discussions of their engagement efforts and speak with institutional investors owning a greater fraction of the company’s outstanding shares.

Importantly, as the figure depicts, we find that the engagement differences expand beyond the year of additional ISS scrutiny. Such findings suggest that once the infrastructure for engagement is in place, companies continue their interactions with shareholders to better explain company policies, obtain feedback, and potentially build allies. Additional analyses reveal that companies with weaker ex-ante governance and stock performance exhibit a stronger engagement response to ISS treatment, suggesting that ISS plays a substitute role for lower quality corporate governance in this setting. Ex-post analyses associate ISS treatment with improved stock liquidity, reduced information asymmetry, less frequent instances of shareholder activism, and no increases in myopic managerial behavior or reductions in director monitoring efforts.

We also examine the engagement effects of Glass Lewis, which currently calls for an engagement response when Say-On-Pay voting support falls below 80%. We find a proportionally smaller but significant impact on engagement due to the Glass Lewis policy, but it does not persist beyond the year of additional scrutiny.

Our study also conducts a textual analysis of the proxy statement to identify the topics of shareholder concerns raised during one-on-one conversations with the firm. Concerns about CEO compensation and incentives as well as elements of pay disclosure and transparency are the most commonly reported concerns by shareholders. Our analyses reveal that ISS-treated companies are more likely to alter elements of pay transparency (e.g., peer groups) and CEO compensation (e.g., time-vested equity) to align with shareholder concerns. These findings suggest that ISS-treated companies incorporate the voice of shareholders, which help shape corporate policies.

Taken together, our findings indicate that proxy advisors play an important but understudied role by encouraging greater company and investor interactions on governance issues. These results identify a disciplinary spillover effect of ISS through enhanced and enduring engagement between subject companies and shareholders.

A copy of the full study can be downloaded here.