Print

PrintMatthew J. Bloomfield is Assistant Professor of Accounting at The Wharton School of the University of Pennsylvania. This post is based on his recent paper, forthcoming in the Journal of Financial Economics. Related research from the Program on Corporate Governance includes the book Pay without Performance: The Unfulfilled Promise of Executive Compensation; Executive Compensation as an Agency Problem; and Paying for Long-Term Performance (discussed on the Forum here), all by Lucian Bebchuk and Jesse Fried.

Some firms appear to structure their executives’ incentives as strategic weapons, designed to soften competition from industry rivals. In particular, firms incorporate revenue-based pay into their executives’ pay plans when doing so is most effective at making rivals back off. This approach to executive compensation is consistent with the theory of “strategic delegation,” and suggests that executive compensation plans play a key role in firms’ strategic positioning.

Background

How should performance be measured and rewarded? It’s a question that has fascinated economists, educators, consultants, and bosses for decades. Within the economics literature, the dominant perspective is that of a moral hazard framework, first formalized by Holmstrom (1979). Employees (“agents”) want to do whatever is in their best interest—shirk their difficult/unpleasant duties and/or extract personal benefits, all the while garnering as much compensation as possible. In contrast, bosses/owners (“principals”) want the agent to engage in productive activity to maximize firm profits/value—something the agent will only do insofar as it boosts their compensation. Viewed from this perspective, the purpose of a performance measurement system is to differentiate between productive and unproductive activity, so that productivity can be rewarded and encouraged. As such, the best compensation plan is that which elicits productive/profitable behavior as efficiently and effectively as possible. This framework has proven very powerful. In addition to being simple and intuitive, the moral hazard framework has demonstrated remarkable ability to explain observed compensation practices, both for rank-and-file employees, and for top-level managers and chief executive officers (“CEOs”). However, this framework does not fully explain the gamut of observed compensation practices.

Building upon Thomas Schelling’s game-theoretic framework of “strategic delegation,” Fershtman and Judd (1987) explore an alternative perspective: that an executive’s compensation contract can be designed to encourage somewhat self-destructive behavior, but in such a way that it boosts firm profits through its impact on rivals’ behavior. Such a contract does not encourage the agent to make the most profitable decisions. Instead, it encourages the agent to make decisions that elicit a favorable response from rivals—even if these decisions aren’t value-maximizing, on their own. For example, consider the case of the “Cournot oligopoly,” an industry with a few large firms that compete by choosing production quantities. The more units the firms produce, the lower the market price ends up being. To choose how much to produce, firms must consider the impact of their own quantity decision on the market price, as well as the impact of all of the rivals’ quantity decisions. That is, to decide how much to produce, firms must also guess how much the rivals will produce; the more rivals are anticipated to produce, the less the firm will choose to produce.

The nature of the strategic environment gives way to a rather unusual strategy. Instead of trying to choose the profit-maximizing quantity, a firm can improve its profits by convincing rivals that it intends to produce a quantity well above the profit-maximizing level. Rivals will respond by cutting their own production, thereby exerting less downward pressure on market prices. One viable way to achieve this is by giving the CEO incentives to increase revenue, instead of just to maximize profits. In so doing, the CEO is shielded from the costs of production, which makes the CEO want to produce more than would be profit-maximizing. Paradoxically, committing not to maximize profit is the best way to maximize profit. By using revenue-based pay, the firm softens competition from rivals, and the benefits of reduced competition more than off-set the lost profits from overproduction. In what follows, I refer to this strategic use of revenue-based pay as the “Fershtman and Judd strategy.”

The Fershtman and Judd strategy is not effective in all circumstances. It’s viability hinges critically on two factors. First, it requires that the industry be a Cournot oligopoly. The strategy is ineffective in competitive industries (because firms lack the market power required to influence rivals), and can backfire by inviting greater competition in other types of oligopolies (e.g., “Bertrand” oligopolies where firms compete by choosing prices, instead of quantities). Second, firms need a way to credibly relay their CEO’s incentives to rivals. If rivals aren’t aware of the CEO’s incentives to overproduce, then they won’t curb their own production, rendering the strategy ineffectual.

Results

I conduct an empirical examination of CEO pay packages to determine if there is evidence that firms utilize this strategy, in practice. To do so, I look to a change in the regulatory landscape to implement a quasi-experimental design. In 2006, the introduction of the Compensation, Discussion and Analysis (CD&A) section of the proxy statement dramatically increased the detail and credibility of public firms’ incentive pay disclosures, thereby enhancing the viability of the Fershtman and Judd strategy. This approach approximates that of a controlled experiment: oligopolistic Cournot firms, (who are predicted to increase their use of revenue-based pay in response to the new rules) form the “treatment” group; all other firms (whose reliance on revenue-based pay is not predicted to change in response to the new rules) form the “control” group.

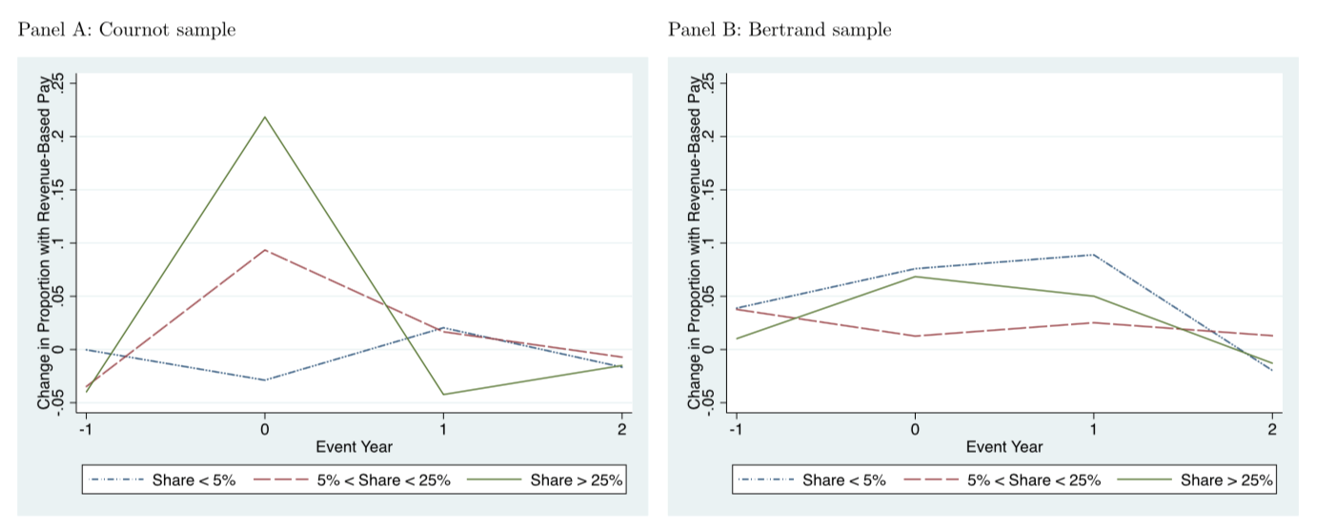

Figure 1. This figure illustrates the use of revenue-based pay in CEO compensation plans at large U.S. firms, surrounding the CD&A adoption year, marked as year zero. Panel A (Panel B) depicts Cournot (Bertrand) firms. For each year, the y-axis represents the year-over-year change in the proportion of CEO’s that have revenue-based pay. The red and green lines in Panel A reflect treatment firms; all others reflect control firms.

Control firms do not appear to react to the rule change at all. There are no sudden spikes or dips in the use of revenue-based pay among these firms. In contrast, among oligopolistic Cournot firms, usage of revenue-based pay increases by roughly 62% within one year of the rule change. Within this group of oligopolistic Cournot firms, the response is stronger among more intensely oligopolistic competitors. For moderately oligopolistic competitors (with market shares between 5% and 25%), reliance on revenue-based pay increases by 32%. For highly oligopolistic competitors (with market shares between 25% and 65%), reliance on revenue-based pay more than doubles, increasing by 125%. I provide a graphical depiction of the results in Figure 1.

In sum, the empirical evidence aligns with predictions from theory. After the introduction of a pay package disclosure mandate, firms appear to restructure their CEO’s compensation contracts as product market weapons, designed to make rivals reduce their own production. Not all firms engage in this strategy. Theory suggests that the strategy is only fruitful for oligopolistic Cournot competitors, and it is precisely these firms that are most likely to adjust their CEO’s pay packages to include revenue-based pay, shortly after the introduction of the CD&A.

The complete paper is available for download here.